By Roger J Kerr*

Will the NZ dollar be able to claw back some value against the US dollar after a 2.5 cent fall from 0.6800 to lows of 0.6550 over the last two weeks and an overall 11% depreciation from 0.7400 since April?

Early signs are positive for a recovery in the Kiwi, as a weaker US dollar on Chinese/US trade talks resuming has lifted the Kiwi off its bottom at 0.6550 to trade up to 0.6635 at the time of publishing.

Judging by the headlines on global media newswires (Bloomberg, CNBC and BBC News) over this past week of “New Zealand bans most foreigners from buying homes”, the perception could easily be that we are putting up further shutters to the rest of the world and do not really care about the economic, investment and exchange rate consequences.

The real estate ban follows the banning of offshore oil and gas exploration earlier in the year.

As this column highlighted back in April when the NZD/USD exchange rate was 0.7400, the Labour Coalition Government’s policy change with the oil and gas exploration ban sent a very negative signal to the rest of the world and was thus negative for the Kiwi dollar. We are now eight cents lower and the timing of the legislation banning some foreigners buying real estate adds to and confirms the negative FX sentiment.

Whilst the legislation merely brings New Zealand into line with existing laws in Australia, the perception (rightly or wrongly) is New Zealand does not welcome foreign capital. A very odd position to take for a country that runs a large Balance of Payments deficit each year and requires the confidence of foreign investors and their money to fund that annual shortfall. A corollary of the current Government politician’s actions, with these anti-foreign investment policy shifts, is a listed company Chief Executive talking down his own share price.

Why would our political leaders take action that drives the share price of the NZ economy (the exchange rate) down? I doubt that the policy changes are deliberately designed to force the currency value lower, it just appears that they do not understand the unintended consequences and the negative implications for the wider economy.

The short-term upside of the currency slide is that exporters have windfall profitability gains which may allow them to reduce their prices in foreign currency to attract increased sales. However, selling on price alone is not a smart way to long-term success in export markets. The downside to the sharply lower currency value is that all imported consumer and capital goods go up in price. The local interest rate markets, bank economists and the RBNZ may be in for some unpleasant surprises in respect to their inflation forecasts being too low, as these currency related price increases feed through into the CPI over coming months.

The ban on foreigners buying residential properties largely relates to domestic political purposes of the Government pointing to something they are doing to make houses more affordable for first home buyers (in Auckland in particular). Unfortunately, the data does not support the change having any material impact on house prices as foreign buyers are less than 5% of the market. The Government policy change also does not explain why house prices in provincial New Zealand continue to increase at 8% per annum, nine months after the change of Government.

The reality is that confidence and incomes are up in provincial New Zealand with higher export commodity prices and now the lower NZ dollar boosting farm-gate incomes even further. Tourism also plays a major role in provincial economies and the growth in visitor numbers can be expected to continue.

A resumption of trade negotiations between the US and China after weeks of trading insults, may ease back some of the upward pressure on the US dollar in global forex markets. As expected, the Turkish economic/currency crisis has not spread into other markets. Whilst the economic repair and solution in Turkey is not that evident today, the impact on global markets appears to have already subsided.

There is some speculation that the US Federal Reserve may express some concern that the rising US interest rates and US dollar appreciation is damaging emerging market economies and thus a threat to world economic stability and growth. Such a statement from the Fed would reduce the likelihood of a fourth interest rate hike this year in December and thus be negative for the US dollar.

The worst appears to be over for the Kiwi dollar sell-off as this latest bout of USD strength appears to have now run its course. The economic fundamentals that drive the NZ dollar value (our commodity prices) still suggest an exchange rate nearer 0.7000, not 0.6500.

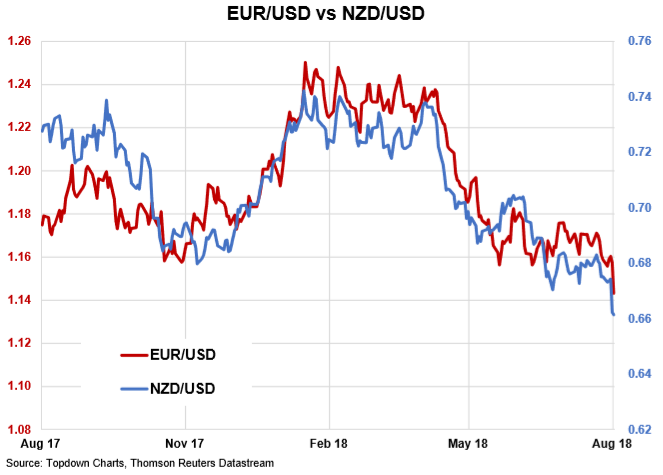

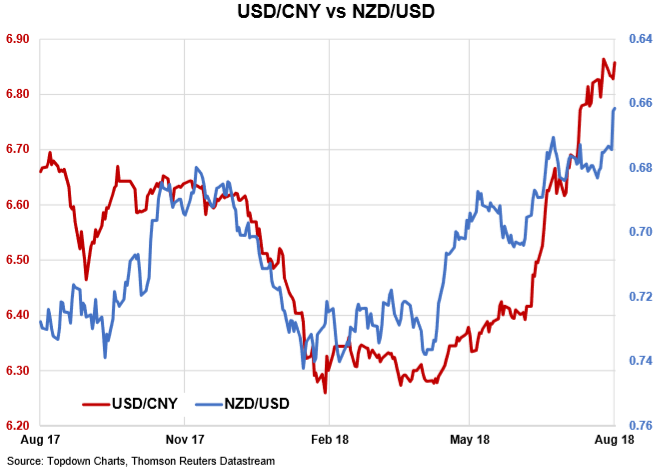

The weaker NZD against the USD over recent months has mirrored the movements of the Euro and Chinese Yuan (CNY) against the USD (refer charts below).

The Chinese authorities are now taking action to stabilise the Yuan from weakening any further as they want to avoid Trump criticism of manipulating their currency value through the trade/tariff negotiations.

Daily exchange rates

Select chart tabs

*Roger J Kerr is an independent treasury Management advisor. He has written commentaries on the NZ Dollar since 1981.

5 Comments

'The worst appears to be over for the Kiwi dollar sell-off as this latest bout of USD strength appears to have now run its course. The economic fundamentals that drive the NZ dollar value (our commodity prices) still suggest an exchange rate nearer 0.7000, not 0.6500.'

I'm afraid I have to disagree Roger. The fascination with commodity prices completely fails to take into account a number of key drivers for NZ strength. Reduced immigration, reduced capital flows (every house purchase by a foreign buyer is just a small part, but contributes The NZ dollar rate will trade far closer to US 60 cents before too long. Our growth, as other commentators have discussed at length along with myself was just a façade. The local business community are now realising that fact and it won't be too long before the markets do.

wealth effect of rising houses prices is not economy. It can shut off over night like 2008. provinces are growing as people move down the scale as who wants a million in debt for an old house in Auckland. kiwi loves 62 so i will bet its going there before it returns to 70 on usa bond crisis in early october. as roger makes predictions that are usually wrong thought would give it ago as well!!!! No oil and gas exploration is no big deal as demand is constantly down short and long term.

The argument is that it is our politics that have sent the NZD down, yet the charts suggest it is global events. To me they also suggest that interesting times are here for longer and that maybe we ain't seen nuffink yet.

Well spotted. Hold them to account and take everything 'experts' say with a pinch of salt. He's right about the oil and gas issue, though. Policy on the hoof without industry consultation is a no-no. Showed a total disregard for business, employment, foreign investment, the Taranaki region, and long-term energy needs.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.