By Roger J Kerr*

Any chance of a recovery back upwards in the Kiwi dollar’s value has been thwarted over this last week by a stronger USD and sharply weaker AUD on global FX markets.

The Australian dollar has depreciated to 0.7100 against the USD from a barrage of negative news, principally related to weaker Chinese economic data and the Emerging Market sell-off (Argentina, Brazil, Russia, China, Indonesia, India, South Africa).

The Trump administration probably believe they are making progress in pressurising the Chinese to relent on the trade war as the Chinese share market continues to weaken and their economic data softens.

The Aussie dollar has been badly caught in the cross-fire from the escalating trade wars between the US and China, and as highlighted in last week’s commentary, the currency markets are buying the USD against all currencies when the US increases import tariffs.

The continuing tumble in the AUD against the USD has dragged the Kiwi dollar down to 0.6530, below its previous 30 month low of 0.6550 two weeks ago. At 0.7100 the AUD/USD has reached its lowest point since mid-2015.

It has been one-way traffic down for the AUD against the USD over the last eight months since the highs of 0.8100 in January.

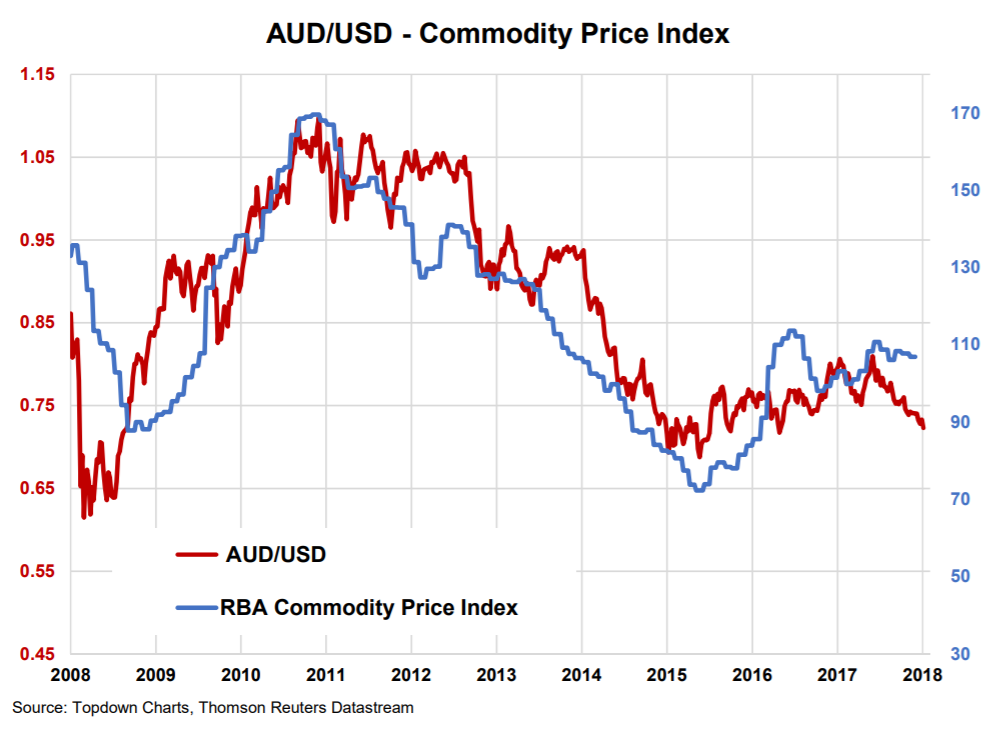

What is somewhat surprising is that the depreciation from the 0.7700 area has occurred without any related reduction in the metal and mining commodity prices that the AUD/USD exchange rate is normally tightly bound to (refer first chart below).

Several commentators are suggesting that the AUD is now being classified in the same economic bucket as plummeting Emerging Market currencies such as the Turkish Lire and Argentinian Peso.

That very negative classification of the Aussie dollar and/or the Australian economy seems a very long way away from the reality of their economy expanding by 0.70% in the June quarter (+3.4% annual rate).

Whilst there are a couple of negatives for Australia currently (political merry-go-rounds and the residential property market coming under pressures with increasing mortgage rates), in my view the AUD/USD exchange rate has well under-shot its fair value.

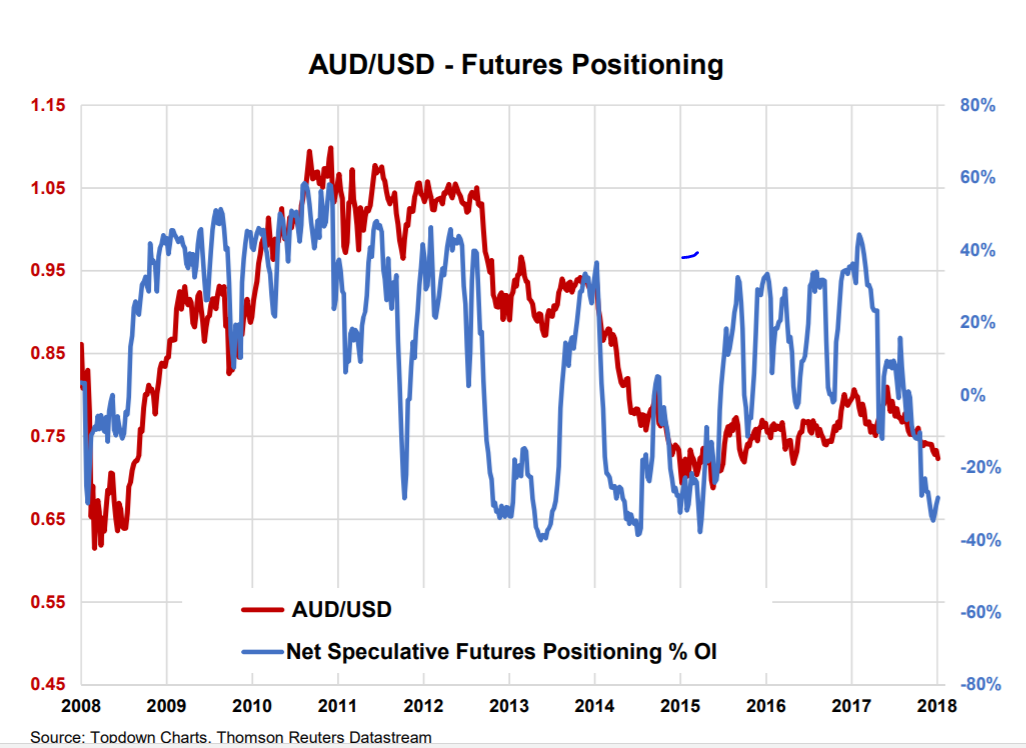

Similar to the speculative futures market positioning in the NZD/USD exchange rate where the Kiwi is at extreme short-sold levels, the speculators are now also heavily short-sold the AUD against the USD as well (refer second chart below).

The currency punters just need a good reason to unwind their positions, buying the AUD to take their profits.

The only potential positive news on the horizon for the Aussie dollar would be some form of concession from the Canadians and Chinese in their trade/tariff negotiations with the US.

President Donald Trump will be looking for some victories to point to ahead of the early-November US mid-term elections for the House of Representatives and Senate. The Republicans and Trump are performing poorly in the political opinion polls, despite the continuing US economic successes of more jobs and rising wages (2.9% increase over the last year, the highest since 2009).

Therefore, political expediency may mean that The Donald dials back some of his extreme trade/tariff demands on the Canadians and Chinese over coming weeks and concedes a little ground to get new deals done. It is all about cementing a deal and looking good for Trump.

The aforementioned analysis on the likely fortunes for the AUD/USD exchange rate over coming week/months is important for the Kiwi dollar and whether it can pull out of the downward slump it has been in since 0.7400 in April.

A recovery in the AUD back to where its driver (commodity prices) suggest it should be, nearer 0.7700, would certainly return the NZD/USD rate to 0.7000.

As the chart below displays, there are not too many occasions historically when the AUD/USD exchange rate radically diverges from its commodity price link.

It is hardly fresh news that the Australian economy is highly dependent on China for import/export trade.

Short-term currency speculation has pushed both the Kiwi dollar and Aussie dollar well below levels that their respective economic/commodity price fundamentals would justify.

It is not easy to predict exactly when and how these miss-alignments will correct themselves.

What we do know is that both FX markets are at extreme short-sold levels and thus a reversal on profit-taking seems more probable than further selling.

In New Zealand’s case, the increase in our Terms of Trade Index (export and import prices) in the June quarter to remain at record 40-year highs is completely at odds with this latest Kiwi dollar sell-off.

If the FX markets are classifying the NZ and Aussie economies/currencies in the same mould as Turkey and Argentina, it is a plainly ridiculous perspective that will not be sustainable. It is only a matter of time before we see the inevitable corrections.

Daily exchange rates

Select chart tabs

*Roger J Kerr is an independent treasury Management advisor. He has written commentaries on the NZ Dollar since 1981.

32 Comments

Thanks Roger, but an alternative view

Don't you think that the world may be cottoning on to the fact that levels of household debt in Australia and NZ (the two highest debt rates to GDP in the developed World) are both likely to have a major impact on domestic consumption and GDP growth over the coming years? Currencies are not all about commodity prices, they are about perceptions of the host nations future - See Brexit and pound performance over the last couple of years.

One way traffic for both the NZ dollar and Aussie from here and time to drop the hedge against either going higher

AUD and NZD were smashed during the GFC, paticularly against JPY. The reason was pure and simple: our currencies were targets of the carry trade and positions were unwound. It was an easy bet until SHTF.This is speculation at its most vivid and has little to do with the fact that both countries are commodity currencies. Yes, both currencies recovered, particularly after the flooding of the market with QE-back liquidity. Now that the interest rate differentials between source and target currencies has narrowed, I don't know if the opportunity is as easy as it was before. Personally, I held this view before about the carry trade before the GFC and held JPY. Not a strategy I would recommend to anyone, unless you were able to leverage in any way,

@JC yes we are seeing the repeat of the 2009 unwinding of the carry trade , BUT not to the same extent .

Our economic fundamentals have not changed we are still cutting down trees , picking fruit , milking cows , and cleaning hotel rooms .

Yes. As I mentioned, the interest rate differential is not as great now. Also, as our debt has not stopped growing among h'holds, the perception of risk is arguably higher. Mind you, NZD has fallen approx 10% relative to JPY in P12M. If you think about the current climate, that's quite substantial considering JPY is not the safe haven currency at present.

Please Roger, have a look at this chart and it will all make sense.

https://www.macrobusiness.com.au/wp-content/uploads/2018/09/6-4.gif

{kind=link}

Same goes for the NZD! Plot the NZ/US yield spread for longer durations and the driver will be clear.

The AUD is headed for the 60's. The NZD is headed for 60 or below.

Even the vampire is calling it lower:

https://www.macrobusiness.com.au/2018/09/goldman-trade-war-crunch-austr…

I came to the same conclusion, looking at the charts leading up to the series of currency crises leading up to 1998 suggests to me that the AUD and NZD will probably carry on down for a number of months yet. Comparisons to 2008 seem less relevant as that crisis started at the centre and moved out. Time for caution. People move capital for a lot of reasons, sometimes by choice, sometimes not.

The world seems to function like a giant banker's ramp. USD are lent out cheaply around the world and things pick up. LIBOR rises and suddenly the USD starts heading up and panic ensues, slowly at first, then rapidly.

When something big breaks and LIBOR starts falling is when we are in the eye of the storm, so far we are being buffeted by the leading edge of the hurricane. What will break first, China or Europe?

My favourite chart, expand it out to see what happens:

https://fred.stlouisfed.org/series/USD3MTD156N

There is nothing so funny as someone attempting to justify their positioning/advice in a market when it goes against them/their advice.

Can only imagine Roger's justifications to his clients when he is telling them to hedge and the currency keeps on dropping.

Now the Kiwi may rally as it is oversold, however as the old saying in the market - "the trend is your friend" - and currently the trend appears to indicate that the Kiwi is going lower.

You should check out Peter Schiff and Shamubeel Eaqub for a laugh.

Economists who have never been in business, get stuck in the data which is always 6-9 months behind the reality of what is happening in the immediate market-place.

Peter Schiff is actually in business as a gold merchant. Equab sells books telling renters what they want to hear.

Shamubeel Eaqub was the best - telling all and sundry how the housing market had peaked/not going higher and it was better to be a renter.

Anyone who listened to him/took his advice - would be literally 100's of thousands of dollars out of the money - his advice was so poor it beyond belief/bizarre that the press still go to him for his economic views.

Shamubeel actually frequents this site, here's his profile.

How do you know that's Shamubeel?

He wrote a very good article the other day about over-tourism in NZ:

https://www.stuff.co.nz/business/106821510/its-a-major-problem-when-tou…

Roger Kerr has been forecasting a higher NZD in his articles on this website for several months now. He has been somewhat successful in marking interim lows, but his 0.7 "fair value" has been getting further away with each succeeding lower low. Now that he has put another article about the impending increase in the NZD, I kinda expect it to rally for a few days or even more than a week. My expectation is that it will mark yet another lower high that will be followed by a new lower low. For now, the trend is down, which aligns with the majority of the fundamentals. Back in early July, he used the milk prices to justify an increasing NZD. That has dropped off the discussion, possibly because milk prices are not that flash at the moment.

A weaker NZ dollar is essentially what we had when the boom in property prices occurred 2014-2016. Cheaper for foreigners to buy, and then the NZ dollar subsequently strengthened and improved the 'foreign gains' for the speculators. Now we have a NZ dollar depreciating (reducing those foreign currency gains) at a time that we are removing foreigners from the purchase equation. I wonder how that feels for those that leveraged up with foreign bank debt?

Capital flight is suggested. From NZ back to HK and Singapore presumably, not necessarily by choice.

Yes, actually the trend is no longer our friend:

- NZD broken down from its 4 year (!) consolidation vs USD in June 18 which has created the 'shock effect' we're experiencing now

- NZD broken down from its 3.5 year (!) consolidation vs EUR also in June 18 which only made a confirmed break out last month

Don't forget that 10 years ago we've had 0.40EUR for 1NZD and 0.50USD - thats only 10 years ago...

Still don't understand what the 'fair value' is based upon... Feels more like a good game of monopoly - including the cheating element of robbing the bank every now and then.

Can only imagine Roger's justifications to his clients when he is telling them to hedge and the currency keeps on dropping."

He did that in 2015 as well.

Our currency was too high given that large amount of money we are printing. I'm already seeing price moves due to increased import costs. I've cut down my purchases from overseas as I've already taken advantage of the higher exchange rates we've had.

Consumer spending will decline with fuel added to the fire by tighter lending standards. Although it looks worse in Australia with Westpac tightening so much they seem to be losing market share for mortgages.

where is this money we are printing?

Money printing is outsourced to the banks. Most people see this via each new mortgage issued.

The supply of money is only increasing at 6% per year via mortgages. GDP growth is only 3.9%. there's nothing to see here move along.

a) "6%" see answer above, b) I strongly suspect real GSP isnt 3.9% or this "magic" number isnt reflected in ppls pockets day to day.

back to a) another test that's failing, the Q is just where is this extra money going? its certainly not going into CPI.

Now if you want to belive such, the Q I ask is why are you thinking like this? ie I see no point.

This isnt money printing as the issue gets "withdrawn" in closing the mortgage.

As grant936 eloquently states above Roger!s clients have been well rogered.I have a note above my computer,simply stating "beware of experts".I have kept it for almost two decades. Remaining objective is fundamental .

I concur with Roger , however he is not really considering the contagion effect , which means that once the weaker currencies are under pressure and falling , the invisible hand then moves up the ladder and takes on the next one up .

Secondly , risk id off

Thirdly the carry trade or investment flows we have benefited from , which were likely funds borrowedin the home country , are now getting better yields at home OR are costing more to service the borrowing costs .

He is right in that we are not as vulnerable as Turkey ( with debt ) Argentina ( Bankrupt ) South Africa ( chaos with no policy direction and a growing deficit ) Iran ( with sanctions) or Brazil (which is mismanaged and has had Lula the lefty loon in power to make a horses breakfast of things )

But we do have Labour in power who are bumbling from one crisis to the next with no leadership and a fractured coalition .

So who knows what could happen under a Labour Government .

My wallet is closed for now

and you think National would be better? those who spent 3~9 years hiding problems so they didnt have to deal with them? In walks Labour and has to deal with them on the fly? at least they appear to be actually dealing with issues, few of which seem to be their making.

After my best round of golf for some time(81),my day has been brightened even more by skimming through Roger's predictions.

To paraphrase Churchill,never in the course of human forecasting,has one person been so wrong,so often,on so much. Keep up the 'good' work.

An unjustified hammering.........of Roger

As they say, economic forecasters were invented to make astrologers look good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.