By Roger J Kerr*

Global financial and investment market volatility, reflecting extreme uncertainty for the outlook of the world’s major economies going into 2019, has been the standout influence on currency movements of late.

Global financial and investment market volatility, reflecting extreme uncertainty for the outlook of the world’s major economies going into 2019, has been the standout influence on currency movements of late.

The sudden change in the future pricing of US interest rate levels from three 0.25% Fed Funds hikes in 2019 just a few short weeks ago, to virtually no increase at all in 2019 today has certainly been a factor that would normally be negative for the US dollar currency value.

The short-term US interest rate markets, as well as the long-term US Treasury Bond markets are now telling us that they expect the US economy to slow up in 2019 and inflation will not be a problem. However, to date the USD has not weakened on this dramatic shift in US interest rate sentiment and market pricing.

For the meantime, the US dollar is holding its ground in the investment market “risk-off”environment and there is always a natural demand by companies, funds and governments around the world to buy USD’s before the 31 December year-end.

Continuing uncertainties in Europe with France and Italy having their own internal problems, coupled with poorly performing European equity markets, have combined to prevent any Euro exchange rate strengthening against the USD at this time.

Once we get into January look for the global FX market sentiment and direction to change as the USD succumbs to the now much lower US interest rate pricing.

When this occurs the mood towards the USD value over 2019 should turn more negative as the sharp increase in the US Government’s budget deficit is cited as a reason to adjust USD currency holdings lower.

NZ property market not a reason to be negative on the NZ dollar

The gains by the USD last week from above $1.1400 to $1.1300 against the Euro were one factor in the Kiwi dollar pulling back to 0.6800 from just under 0.6900.

Also contributing to the downward correction in the NZD/USD rate was the RBNZ announcing increased capital requirements on the trading banks.

Tighter bank credit conditions and increased lending margins were seen by the markets as negative for the residential property market, thus negative for consumer demand/GDP growth in 2019.

The initial reaction is perhaps understandable, however the increased bank capital happens progressively over five years and most banks are already above the current minimum capital levels anyway.

The bank lending market remains highly competitive in New Zealand and these changes are unlikely to cause a more serious downturn in the property market.

The commercial and industrial property (and construction) markets remain buoyant with stretched resources the main problem.

The Auckland housing market has levelled off as it normally does, and a major reduction in property values from here is not expected.

Rising unemployment and mortgage interest rates would need to occur to cause major house price decreases. That does not seem at all likely in the current economic environment or likely to occur in 2019 either.

Aussie property market poorly analysed…

Doomsday predictions for the Australian residential property market have been coming thick and fast of late from the likes of global investment banks and the OECD economists.

The reality is that the central city apartment markets in Sydney and Melbourne were over-hyped and heavily over-supplied.

Sharp downwards value corrections are now occurring in that part of the property market.

However, across the suburban mortgage belts house values are not falling away to the same extent and a general housing collapse is just not likely with strong job security and low interest rates in Australia.

The investment bank and OECD economists are unfortunately not looking far enough away from their CBD glass towers.

I do not see the Aussie dollar depreciating further in 2019 due to these dire property market forecasts.

The AUD may struggle to make significant gains against the USD if their metal and mining commodity prices drop away on lower global economic growth forecasts.

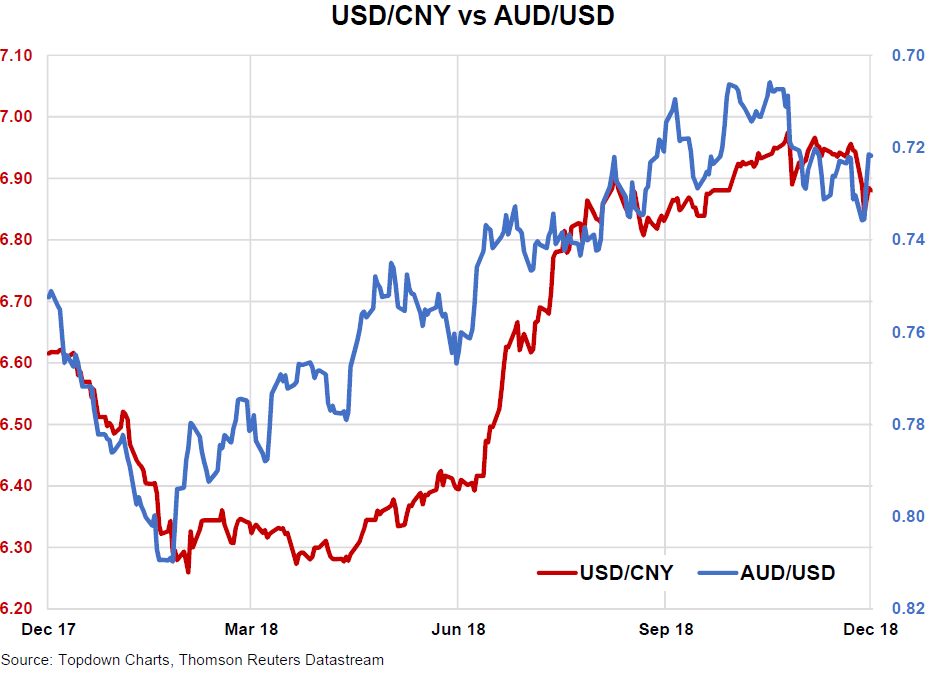

Outside of that scenario, a weaker USD on international currency markets suggests a recovery in the AUD/USD rate back to 0.7400/0.7500 in early 2019 (currently 0.7175). The turnaround in the Chinese Yuan’s fortunes against the USD through November/December also points to a AUD/USD rate closer to 0.7400 (refer chart below).

How the Kiwi dollar behaves in January…

Historical evidence does point to the Kiwi dollar making its own gains against the USD in early January as the local agri exporters are required to buy significant volumes of NZD’s to hedge export sales in thin/illiquid holiday FX markets.

Exchange rate movements are always exaggerated in such currency market conditions.

Other exporters who missed the boat to increase long-term hedging percentages at 0.6500 a few weeks ago should also be eager Kiwi dollar buyers at current levels.

The expected weaker USD against the Euro will add to the re-emerging positive Kiwi dollar sentiment in early 2019.

NZD/AUD spike upwards rapidly reverses (per its predictable pattern)

As anticipated, the NZD/AUD cross rate’s spike to above 0.9500 appears to have again been very short-lived.

The Australian banks with large and profitable subsidiaries in New Zealand would have taken the opportunity of the elevated NZD value against the Aussie dollar above 0.9500 to hedge projected 2019 NZD profits back to the AUD (i.e. buying AUD, selling NZD to hedge).

The amounts involved are billions of dollars and large enough to force the NZD/AUD cross-rate lower.

The AUD has more to catch up on against the USD than what the NZD has, therefore a slow slide in the NZD/AUD cross-rate back to 0.9300 is expected over the first few months of 2019.

NZ GDP number unlikely to be an Aussie shocker

The release of the September quarter’s GDP growth figures on Thursday 20th December will come out too late ahead of the Christmas holidays to materially impact on the NZ dollar value.

We should not expect a quarterly increase much above 0.50%, coming on top of the previous large 1.00% expansion in the June quarter.

A surprise quarterly increase above the consensus +0.60% would be positive for the Kiwi dollar.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

6 Comments

Always NZD bullish, and usually wrong...

The reason the USD hasn't collapsed despite market expectations of less US rate hikes is because it's worse everywhere else. Look at Australia for example, the market is now pricing a chance of rate cuts. China's data is looking very weak. Europe is slowing. US is the best of a bad bunch right now.

AUD/USD is heading into the 60's next year.

NZD/USD will do very well to remain above 65.

NZD/AUD could hit parity.

ZP - I think I'll pay more attention to Roger's indepth analysis than your rant. Roger I always enjoy your column and much like Tony Alexander's columns I find you both very valuable in that you cut through the BS and look at the real numbers and what's driving them - Thankyou

As usual, an alternative view is a bit much to handle so it gets called a 'rant'. The funniest thing about your comment is that Roger's 'analysis' has consistently missed the true driving forces behind USD/NZD/AUD movement. Every week it's a new driver lol.

I sincerely hope you have been following all of Roger's calls for your own hedging activities.

Zombie I love you

I haven’t seen a single analyst who’s bullish the buck for next year

Just for clarification... do you mean the USD when you say "buck"?

I have to say that I've stopped tracking analyst commentary overall on currency movements as virtually every one has a rather negative alpha, including the author above. For me, it is better to sift through various news items and personally decipher what it means for the currency instead of reading through various pontifications.

A few weeks ago, Roger finally correctly called a bottom. It was about the 7th time that has has predicted an imminent rise in the NZD since July. He finally got in right after many failures, and with numerous rationales as to what was driving the currency markets. Last week he predicted a trading range of 0.68 to 0.70. We are still fairly close to this range although not quite in it anymore, with the current value being 0.6785. One would have had rather good success in the past six months via speculating to the opposite side of his predicted future currency movements. His market discussion tends to focus on only the elements that support his bullish NZD case and tends to ignore the items that are bearish to the currency.

Still, fun to read the mindset of an NZD almost perma-bull.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.