Apparently bank traders in the NZ forex market were becoming increasingly concerned over recent months at the lack of volatility in the NZD/USD rate movements (hurting their monthly P&L numbers!).

The tight trading range between 0.6800 and 0.6900 was narrowing up as there was a total lack of fresh direction in the market.

Alas, Governor Orr of the RBNZ has ridden-in to the market’s rescue, yet again surprising all and sundry with an OCR Review statement more “dovish” (weaker economic outlook) than generally expected.

The immediate plunge in the Kiwi dollar last Wednesday afternoon, 27th March from above 0.6900 to just below 0.6800 has certainly lifted volatility. However, based on patterns witnessed over the last 12 months, post RBNZ statement related spikes up and down in the Kiwi dollar are never that sustainable.

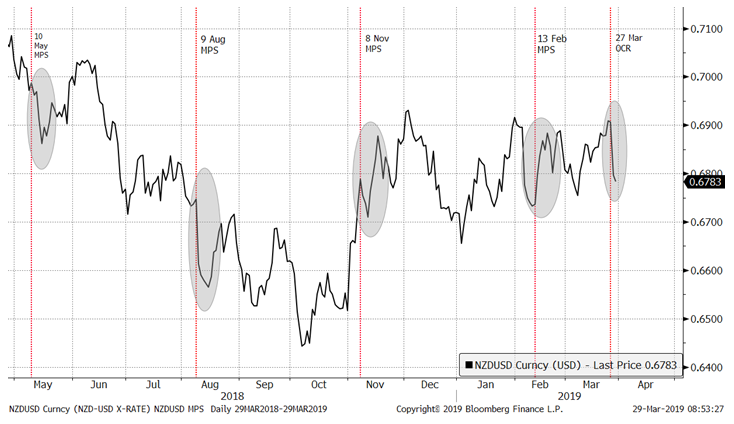

Some might say that Governor Orr is rapidly building a reputation of taking some delight in catching the FX markets wrong-footed on the messages being delivered by the RBNZ. The chart below highlights subsequent NZD/USD exchange rate movements to the RBNZ’s four Monetary Policy Statements (“MPS’s”) over the last 12 months and the OCR review last week.

- The 10 May 2018 and 9 August 2018 MPS’s were both more dovish than prior market expectations, causing immediate depreciation in the Kiwi dollar on the day. However, within a week or two the Kiwi dollar had bounced back up again. The NZD/USD rate did subsequently move lower in 2018 due to a stronger US dollar, trade war uncertainties and a depreciating Aussie dollar.

- The 8 November 2018 and 13 February 2019 MPS’s also surprised against prior market expectations. Both statements were more balanced on the economic outlook, whereas the markets were anticipating continuing dovish inferences from the RBNZ. Two subsequent sharp spikes upwards in the Kiwi were the result.

- The OCR review statement on 27th March again surprised everyone with the Governor stating that the balance of probability had shifted to a greater likelihood of a future OCR cut. The local FX market sold the Kiwi down one cent to below 0.6800. However, interestingly, there was no “follow-through” Kiwi selling from the offshore traders on Thursday night. They either think the RBNZ is on the wrong track, or they (more likely) have absolutely no interest to trade the Kiwi dollar at this time.

Part of the RBNZ’s remit with managing monetary policy is not to cause undue foreign exchange rate and interest rate volatility. Seems that they may not be meeting this objective, however on the other hand it could just be that the markets “get it wrong” every time.

The take-out from last week’s Kiwi dollar movements is not to expect continuing depreciation due to this subtle shift in stance or signalling by the RBNZ. The FX market’s responses are always short-lived and temporary. It always needs to be remembered that whether they will actually cut interest rates, or not, is totally dependent on the economic data that comes out over coming months.

What has really changed in the economy to justify a fresh monetary easing bias?

Conditions have not changed at all in the NZ economy since the last MPS on 13 February to justify the RBNZ’s renewed dovish tone.

Therefore, it is a deterioration in the global economic outlook over the last six weeks that has caused the RBNZ to signal the balance moving in favour of a rate cut. Perhaps Governor Orr was persuaded by a whole lot of other dovish central bankers at a recent conference he attended in Basle that the global economy was going to hell in a hand-cart. Global economic risks were certainly elevated late last year, but as this column has previously stated, things have changed dramatically since then:-

- Equity markets have recovered somewhat, albeit over-hyped tech stocks are now under the hammer.

- The Federal Reserve has done a U-turn on US interest rate hikes.

- Considerable progress has been made on resolving the previous trade wars, and a Sino/US trade agreement can be expected sometime in April.

My view is that there is a better than 50/50 chance that the global economy will not weaken any further and recover somewhat as confidence is restored to business investors/traders by the impending China/US trade agreement. The trade agreement will also be a boost to the NZ economy already enjoying high export commodity prices. The labour market here remains tight, capacity utilisation is high and business firms are experiencing cost increases that they will eventually be forced to recoup through price increases. Hardly an economic environment supporting even loose monetary policy. I do not see the RBNZ dropping their inflation forecast to below 1.00% to justify a cut in the OCR. Eventually the still positive economic data will force the RBNZ to change their tune once again.

The economy is not being helped by low business confidence levels caused by an over-zealous Government toying with a capital gains tax and an over-zealous RBNZ wanting to have the highest capitalised banks in the world. Both are unnecessary policy changes that will only work to increase the cost of capital and restrict capital investment formation, at a time when the economy needs the opposite. We do make it hard for ourselves in “Gods Own” little country.

Despite the RBNZ’s clear intention to drive the Kiwi dollar lower, greater forces are at work in the form of a long-awaited AUD recovery, high commodity prices and eventually a weaker USD on the trade deal to keep the Kiwi dollar between 0.6800 and 0.7000 over coming weeks/months.

NZD/USD Exchange Rate

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

21 Comments

Fear not Roger , for the currency shall stabilize again , possibly at lower than 69 cents to the US$, but in my uninformed opinion it may go back up to near 70 cents, simply because none of our economic fundamentals have changed in any way at all, and we can certainly say 'we have no new problems " .

Our interest rates are stable and have been for a decade ( lowest in my lifetime ) , inflation is low ( lowest in my almost 40 year working career), unemployment is in the mid 90's which is astonishing.

There is a budget surplus which means that the Government is living within its means

Our productive sectors are doing fine , in fact, most are ticking along nicely, exports are good , tourism remains robust.

Our terms of trade are the highest since I was a teenager in the early 1970's .

So I still reckon he wanted a lower Kiwi$ , and that's all there is to it .

I reckon we doing really well , and in fact if NZ Inc was a listed entity , I would be a shareholder ........... well on second thought maybe I am already .

I am a decade or so ahead of you. When I started work IBD’s ( term deposits) average rate about 3.25%. Had been, and stayed, like that for a long time. STG TT buy 2.1367 to NZ$ and 1 US$ bought you NZ 7/2d. Exchange rates were fixed, only changed when Muldoon or someone devalued. Different world completely then. No electronic wizardry, fastest communication was the telex. Think the question here today for NZ is one of cautious optimism and charting a course with an eye on the horizon for approaching storms. Always remember how Kirk’s government was going along reasonably well, even keeping Muldoon at bay sort of, and then skittled by an oil crisis caused by a Saudi palace revolt. There it is.

There are a few canaries in the mine worth listening to. EG lower tax take from businesses. Dairy companies struggling, mental health issues rising, infrastructure deficits and blowouts, bank lending restrictions. And remember govt surplus = private sector deficit. Along with that watch out for rapid price increases due to business costs leading to actual inflation and here we go again on an increasing interest rate spiral.

Boatman,

But how is all this possible with-in your view-a dreadfully incompetent government? How come they 'are living within their means' when-according to you-they are dragging the country down with irresponsible spending?

They have been very disciplined in their spending of the surplus that was bequethed to them by the previous Government .

That said , I still think they are a bumbling bunch of losers who should never have been let anywhere near the levers of power .

Well, It's hard to disagree with you on Tyford who looks out of his depths and indeed,Kiwibuild is a mess.

National's problems are a) Bridges and b) they've got no mates. ACT is a joke but presumably the good people of Epsom will do National's bidding and re-elect him,but that's it. The government's problem is that holding the 3 parties together is no easy task.The Greens have a real problem in their co-leader Marama Davidson who is clearly of the far left and could drag the party below 5%. Who knows what Peters will do?

If i had to guess right now,I think the government will scrape through again and they will continue 'to live within their means'. They will then be booted out at the following election.

It’s going to be an interesting 18 months until the next election. If National don’t look like making it, I will likely vote NZF in the hope they continue to moderate and frustrate the lefties. I’ll do my best to get my immediate family to do the same.

Perhaps Mr Orr is the messenger for tomorrow's RBA decision.

Our problem is we tend to believe most of what we read. My advice, don't. And yes you're right, Boatman we are often our own worst enemy aren't we? We are traditionally hard on ourselves. It's a part of our DNA.

A US/Sino trade deal is not far off, each for their own reasons. (Casual racism removed, Ed).

You have certainly changed your tone? I thought the next depression was just around the corner since the COL was sworn in? However, agree with your post..steady as she goes, and don't rock the boat.

You do realise the reason there has been no deterioration in the fundamentals (there has been in reality) that you can notice, is because the Kiwi is down over the last 18 months.

Falling exchange rates support the economy, and asset prices, when accompanied by expansions in the money supply.

Kiwi was at the top of its “economic support” band, I.e any higher and it would have been a net deflationary force to domestic assets.

The RBNZ is actually fighting a small liquidity trap onshore. Twice now multiple domestic interest rates pushed below the OCR level, thus threatening a contraction in credit if they don’t cut.

You think in traditional terms. I don’t.

RBNZ will cut 100bp by the end of the year.

Lord help us if they do. IMHO

As I said the other day the RBNZ is just talking the dollar down without actually doing anything,

Dont expect a rate cut at the next review.

could not agree more

I agree with this, I really dont see the reason for the record low OCR over the past 12 months.

Low unemployment, solid consumer spending, 2.8 % GDP growth.

A Orr has been itching to lower rates since he arrived, I really dont know why.

Now its driving savers into the record high housing and share markets (power companies on PEs of 20!)

this cant be good.

Does he know something we dont??

Any more cuts to TDs will see NZ savings eroded after tax and inflation adjustments.

Low interest rates are not one way traffic, some savers will have to pull back on spending, which is why a neutral OCR, say 2.5 to 3 % is of balanced benefit to the economy.

I hope we are not heading for stagnation, as per Japan.

That’s exactly where we are heading.

Mr Orr realizes that we are one giant pyramid scheme that is teetering at the same time as our cousins who sit upon another gargantuan pyramid are wobbling and collectively come under the umbrella of the same 4 extremely important banks.

... our housing market is now " too big to fail " .... ooops ... where have we heard those dreaded words before ... can the Reverse Banks save them by crushing the OCR even lower ( and snatching the bread & butter of retired folks term deposits in the process )

A CGT will bail out failed housing investors ... at the taxpayers expense ... as they'll be able to claim losses to off-set against future gains ...

... this government really hasn't thought it through , have they ...

You and the market have a very short memory Roger. Orr told us early in his term he would cut rates if GDP growth failed to exceed 3%. Nobody should have been surprised on March 27.

He's trying to talk up a rate cut so he doesn't have to actually make one.

To think that the Reserve Bank would even think about cutting the OCR by 1% by the end of the year is unthinkable IMHO

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.