The soaring price of petrol has seen inflation surge by 0.9% in the September quarter and 1.9% annually, according to Statistics New Zealand.

The average market expectation was for quarterly inflation of just 0.7% and an annual rate of 1.7%.

At 1.9% the annual rate of inflation is just below the targeted 'midpoint' level of the Reserve Bank's 1% to 3% targeted range.

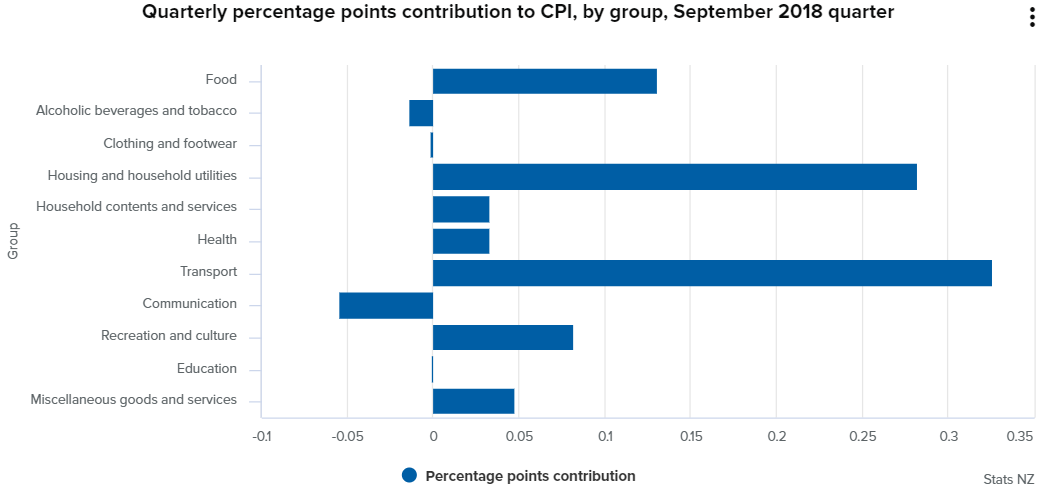

Here's the main influences in the quarterly figures:

- Transport rose 2.4%, influenced by higher prices for petrol (up 5.5%).

- Housing and household utilities rose 1.1%, influenced by higher prices for local authority rates (up 5.1%), construction (up 1.3%), and rentals for housing (up 0.4%).

- Food prices rose 0.6%, influenced by higher prices for vegetables (up 11%).

Normally with inflation reaching this sort of level, the expectation might be to see rising interest rates, but the RBNZ has indicated it will 'look through' short term spikes in inflation caused by external things such as rising oil prices.

Indeed it has talked about dropping official interest rates if need be, but such talk will likely be dampened by Tuesday's official inflation figures.

The New Zealand dollar spiked sharply on the news, rising from under US65.5c to nearly US66c before settling at around US65.8c.

ASB chief economist Nick Tuffley and economist Kim Mundy said there was upside surprise on both the tradables and non-tradable side of the equation over the quarter.

"Tradable inflation lifted 0.9% qoq, with much of the upside surprise contained to the transport component (+2.4% qoq). Petrol costs rose 5.5% over the quarter (higher than the 4.3% we had expected) and passenger transport services also rose more than expected. In particular, rising fuel costs appear to have had a marked impact on air travel costs (both domestically and internationally over the quarter).

"We expect the RBNZ to continue to look through much of this quarter’s rise. In saying this, the RBNZ will be watching for growing signs of any second-round impacts on broader prices. The extent to which this occurs depends on consumer demand remaining unchanged in other sectors of the economy, despite the higher fuel costs they are now facing."

Kiwibank chief economist Jarrod Kerr and senior economist Jeremy Couchman noted that the September quarter inflation result was "a significant step higher" than the RBNZ’s August Monetary Policy Statement (MPS) forecast of just 1.4% year-on-year.

"The RBNZ is starting to be backed into an awkward position, with its view that inflation will gradually rise to the target mid-point increasingly untenable," they said.

"For now at least, the RBNZ can still claim that much of the recent rise in inflation pressure is coming from cost-push inflation factors that can be looked through. These cost-push factors include higher world oil prices, a weaker currency and Government induced price hikes (such as petrol taxes and a chunky minimum wage hike).

"What the Bank is likely to remain focused on is the underlying engine of inflation, GDP growth. With business confidence still casting a shadow on the economy there remains the risk that internally generated inflation peters out.

"However, as the Bank has drummed home, price setting behaviour is being more driven by actual inflation. With headline inflation on the charge, momentum is likely to build in the figures. In addition, we see GDP growth picking up above trend into 2019, and inflation is likely to accelerate.

"We believe that ultimately the RBNZ will be forced to begin gradually hiking the OCR sooner than is currently signalled. We believe the RBNZ will be able to hike by May 2020, six months ahead of their schedule."

Stats NZ's prices senior manager Paul Pascoe said petrol prices increased 19% in the September 2018 year.

“This is the highest annual increase since June 2011.”

Petrol rose 5.5% in the September 2018 quarter. The average price of 91 octane, after discounts (for the whole of the September quarter), reached $2.18, up from $2.06 in the June quarter. The price of petrol rose continually throughout the quarter, and by the last week of September was 3.2% above the September quarter average pump price.

Multiple factors contributed to the petrol price increase this quarter. The exchange rate fell over the quarter, while crude oil prices rose. In addition, a regional fuel tax of 10 cents per litre plus GST was introduced in Auckland on 1 July.

"While petrol only makes up about 4% of the CPI, it can have a large impact on overall inflation," Pascoe said.

"It contributed about 30% to the quarterly CPI movement for September, and about 40% to the annual movement."

This is the first time petrol prices have risen for four consecutive quarters since September 2008, during the global financial crisis.

When petrol is removed from the CPI, the increase was 0.7% for the September 2018 quarter (compared with 0.9% overall), and 1.2% for the September 2018 year (compared with 1.9% overall).

A 3.5 cents per litre nationwide increase in petrol tax was introduced on 30 September. The effects of this price increase will be seen in the December 2018 quarter.

The falling exchange rate, which makes imports more expensive for New Zealanders, also contributed to a 2.6% rise in the price of audio-visual equipment such as televisions, cameras, and home theatre systems in the September 2018 quarter. This is the first quarterly rise for audio-visual equipment since September 2016, as quality adjustments generally cause price falls for these goods.

Consumer Price Inflation by Group

Select chart tabs

44 Comments

Just wait until we get the December Quarter figures. Just in time for people to review the Christmas Credit card spend. Did the Turkey really cost that much sweetheart?

Indeed, will be over 1% as there are more price pressures in this 4th Q so far. May good for Xmas though, NZD stronger!.

Don't bank on that NZ rise, it will last until the end of the week.. The NZ dollar is heading down to Chinatown.

Nic - any thoughts on how far NZD might fall?

approx to chinatown

Yes, few cars sold in February, very typical pattern, CC from Xmas. Me I'm looking for an EV around then.

'Petrol rose 5.5% in the September 2018 quarter. The average price of 91 octane, after discounts (for the whole of the September quarter), reached $2.18, up from $2.06 in the June quarter.'

Not sure where those numbers came from? Must be using the RPI (Rich Persons Inflation index) and not the PPI (Poor Persons Inflation Index).

Looks quite comparable to the data Interest provide

https://www.interest.co.nz/charts/commodities/oil-and-petrol

You can expect another big jump when the December quarter is reported. Remember this is lagging data, and price rises have been significant in the last month or two.

That depends, the oil price in the last few weeks has broken its tup rend and is now looking at $63US a barrel and not $83US a barrel for xmas.

November could of courses reverse October's month of consistent drop....its really unknown just where the price is going short term.

Cannot resist, the only surprise is that our economists are surprised.by

Cowpat | Mon, 15/10/2018 - 09:08

up1

Have to agree with Mr Kerr that CPI could very well overshoot economists forecasts.Whatever the case it is coming in stronger than prior forecasts. Against the Aussie this week , with RBA minutes,employment data and multiple global issues at the fore , NZD may win the trifecta or quadsomething against its cousin. Currency to watch , undoubtedly the JPY,, another sell off overseas could see it benefit the most.

What is the money supply growth David? ie: real inflation. Money doesn't grow on trees, it has to come from somewhere.

"While petrol only makes up about 4% of the CPI, it can have a large impact on overall inflation," Pascoe said

4% of household spending on petrol... Does everyone walk everywhere? Not by the look of the majority they don't!

Our household spends about 4% of income on petrol (directly that is). We have 2 cars.

Average take home pay is apparently about $720 a week in NZ, 4% is about $30, so about 12 litres of petrol per week. That'll get you about 100-200km a week. There's probably a bunch of people in Auckland doing that, but in more sensible cities like Christchurch that's more than enough for a suburb -> city centre commute and a couple of extra trips.

And of course, there's people like me bringing down the average by using approximately 0 litres in a week.

I would use double that most weeks. A full tank (60L) every 2nd or third week. My partner probably uses a little less than me.

And that's my point. I don't use a lot of petrol these days but those that are working, paying rent are getting hammered. The basket of goods doesn't work for either indebted owner occupiers or overly extended tenants. It's rigged to suit those of us that don't have to use petrol as much and inflation has been miscalculated for years which is why interest rates have been too low for far too long. This will end badly if we're not careful, because people don't stay uninformed forever when things start to get tighter.

For me and you, the weighting is too high. For Pragmatist, it's too low. This is not surprising when a stat is based on averages. No inflation measure can be everything to all people.

I think i'd be far below average for anybody with an active social life in Auckland.. I only travel about 10-12kms to work, and with the possible exception of the owner, I am the closest to work, others in the office do 60kms a day. I used to burn through a tank a week easily when i was travelling to running events and other social occasions.

Yes, I expect Aucklander's make up much of the top half of the distribution. One of the costs of living in a large city. Down here in Chch you can have an active social life without the car - I even bike to running events here, everywhere in the city is pretty accessible by bike.

those that live in the country would spend more on petrol than those that live in the cities, most in the city go to and from work and shop at local malls, country folk have to travel to town and sometimes to the bigger town for bigger items, not to mention if they have kids all the events they need to get to.

You could be right, but a 20-30km one way commute into Auckland every day would quickly stack up. I don't know what the proportion of country dwellers that have substantial commutes is like, but a couple of weekly trips to the nearest town probably wouldn't match the Auckland commuter. Besides, a large proportion of the country lives in small towns and cities and rarely leave them.

Who knows really - my real point is the 4% data doesn't seem crazy to me, although I'm sure that the outliers spending 10% would be outraged.

Agreed, but it is flat, has cycles lanes not shared by buses trying to crush you on a daily basis, and has much more consistent weather (less random rain events).

Yes, we are truly blessed. I do still get the occasional driver apparently attempting to kill me, but if you assume everyone is out to get you it seems pretty safe.

Inflation is 'mis-calculated' on purpose so it is not the reason interest rates are 'too low'.

Time to ramp up interest rates then. Really blow up the Ship.

It is going to end badly, Peak oil, CC....these factors alone guarantee its going to go badly over the medium term. Interest rates too low? no, very wrong, which is funny really when you spout that "ppl are not informed", willingly ignorant is more like it or simply wrong IMHO.

"getting hammered" which was a point I have been raising for a decade. ie you cant get inflation when a significant % of ppl are in this boat, they simply cant pay more.

is it not time the CPI bucket was updated, we now know nearly 40% rent and of that it takes a big percentage of income so why does it only make up a small percentage in the CPi basket

Got to keep the peasants in their place.. We couldn't have tenants earning income on bank interest now could we? Heaven forbid, that may give them a chance in life..

An outdated CPI measure allows central banks to flood markets with cheap credit for eternity and takes the pressure off policy makers from doing their jobs i.e. restructuring the economy and reallocating resources when most needed.

Successive governments in NZ have dodged important questions and delayed key decisions by conveniently hiding behind macroeconomic figures.

Something to consider: how far would NZ's GDP growth be from zilch (or under) in a normalised rate, low migration environment?

Thanks shareholder - the beef in my postings yesterday.

This current singular CPI weighting / calculation is now something of an anachronism – the economic structure and makeup of NZ has changed dramatically over the last decade or two.

Once there was a great, somewhat egalitarian middle.

But no longer – the disparities have stretched to historical extremes – and merrily quoting 1.9% and 0.4% means little to a large swath of the population focused on rising petrol, food and rental costs and trying to simply get by.

This disparity affects families, businesses, supplements, benefits and the well-being of the country in general.

No surprises here. If there was such, it would be that it's below 1%.

I keep an eye on truckstop diesel prices and over a year they look like this: (Caltex Zone C, less 8c/l discount via Kiwi Fuel Cards) - a basic input to most forms of serious transport, ag etc. Most bulk users will be around 8-20c/l less than that again.

- 2017 - June 23 - $0.8691 per litre

- 2018 - June 22 - $1.2391 per litre

- Today's quote (less my 8c/l discount) $1.4490 per litre

So some crude arithmetic:

(1.4490 - 0.8691)/0.8691 = 66.7% increase over 15.5 months.

Now there are at least four inputs to this increase:

- Per-barrel movements in USD price

- FX rates NZD-USD

- Price spreading by Z Energy to soften the Awkland fuel tax blow (Zone C is South Island - the northern bit)

- Other

But as this rather dismal series should reveal, this sort of base increase is gonna drive cost-push inflation into almost every corner of our little economy, spread out as we are over a big distance top to toe, and far, far away from the rest of the world. Less than 1% is some sorta October Surprise, frankly.

Great stuff Waymad, even if it's "back of envelope". I particularly get off on But as this rather dismal series should reveal, this sort of base increase is gonna drive cost-push inflation into almost every corner of our little economy, spread out as we are over a big distance top to toe, and far, far away from the rest of the world. Less than 1% is some sorta October Surprise, frankly.

I just got 7000k of ruc for my ute. Its gone up 10%. It was around $440 now over $480.

Well done Waymad.

Love a good series of numbers.

Inflation, actually no as you miss the fundamental point, to be able to charge more the buyers need to have the money.

So sure petrol goes up 20cents so it then costs say $10 more to fill the tank every week, however then I have $10 less in my wallet and with no more money coming in its simply less I spend elsewhere. This has been rinse and repeat since 2008, what makes you think its can change now? because I dont think we'll see much happening, too many ppl are financially badly off.

1.9% is pretty much perfect for a healthy economy. There's a lot of noise in here for no reason.

0.9% in one quarter = 3.6% if continues over a whole year. Given that it is primarily driven by sharp fall in NZD starting mid April, and a lot of the increased costs of imports haven't filtered into the economy yet, it seems pretty likely that it will continue for a while yet.

High inflation kills GDP growth which will have the govt worried next quarter.

3.6% seems pretty normal to me, despite still being unlikely. It might scare those heavily leveraged as interest rates would have to go up. Although the advantage for them is that their debt will be getting eaten faster as long as they can maintain their increased payments. Wake me when we hit double digits.

“1.9% is pretty much perfect for a healthy economy.”

That’s great news – and thus all that’s missing now is the arrival of a truly healthy economy.

That would require this government to focus on reducing inequality and housing costs. Shifting from income to land taxes would do it.

Also, the effect of inflation on the economy is that it gets people with cash deposits spending and investing more because their money is devaluing. So inflation is good for the economy to a point. That point is probably up to 5%.

https://ftalphaville.ft.com/2018/10/15/1539577800000/No--the-housing-cr…

might be of interest to you.

I think the inflation “sweet point” for a truly healthy economy is around 2 to 2.5% - it gives forward looking confidence in decision making but also removes panic / miss out type thinking.

And if it’s matched with rewarding savers with slightly above inflation returns then savers will make rational decisions in terms of a balancing savings and consumption.

That world once existed – I struggle to grasp the current nonsense flying around.

Interesting, though I'd think RBNZ would tolerate a little (a few months of) overshoot given it previously was too cautious and under-shot. They now appear to be more neutral in their outlook.

0.9 Sept Qtr actual. 1% Dec, Mar Qtr forecast equates to a 4% inflation rate. Wait for interest rates to rise, compounding the problem. Followed by the inevitable mortgage stress, and home loan defaults. Interesting times....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.