Summary of key points: -

- Relatively speaking, NZ to underperform the US of A in short to medium term

- “Boom-time” economic conditions, however a stack of countering negatives

- Expect little response from NZ policymakers

- NZ dollar’s favourable interest rate differential has long gone

Relatively speaking, NZ to underperform the US of A in short to medium term

Relative economic performance and relative levels of interest rates, stock markets and commodity prices are all the cornerstone determinants of exchange rate values and direction of travel. For the NZD/USD exchange rate outlook it is therefore important that the assessment of the relative strengths and weaknesses of the two economies/markets is categorised into appropriate time frames.

In the short to medium-term (six to nine months), the strength and speed of the US economic recovery over the remainder of this year just appears superior to that of New Zealand on numerous counts. In the medium to longer-term (into 2022), if the recently updated IMF global growth forecasts are accurate, growth and commodity currencies like the AUD and NZD look set to benefit from the strongest world GDP growth performance since 1980.

The path of this column’s forecast of a stronger USD against the Euro from $1.2300 in February to near $1.1500 remains intact, albeit it is a rather jagged line downwards. A softer tone this last week on the US monetary policy stance in a speech by Federal Reserve Chair Jerome Powell caused a minor pullback from below $1.1800 to above $1.1900 in the EUR/USD rate. Looking forward over coming months, US economic data will continue to print at a much higher level to a struggling European economy. Americans will be travelling inter-state big time for their summer holidays as the Covid vaccine is rolled out, so it is no surprise that US gaming, leisure, hospitality and travel stocks are reflecting that expected increase in economic activity.

The NZD/USD exchange rate has traded sideways in the 0.6950 to 0.7050 band over the last two weeks since the Government tax policy bombshell that catapulted the Kiwi dollar sharply lower as interest rate increases were removed from market forward pricing. Should the USD appreciate another 3.5% from $1.1900 to $1.1500 as anticipated against the Euro, that general USD strength would see the NZD/USD exchange rate at 0.6800. Local New Zealand-specific economic and market trends are not expected support the Kiwi dollar against this stronger USD trend. Indeed, as the following commentary will explain, the local factors all appear to be negative for our currency over coming months.

“Boom-time” economic conditions, however a stack of countering negatives

Based on any analysis and evaluation of market conditions currently occurring in New Zealand, the economy and therefore the currency value should be in a “boom” state at this time: -

- Interest rates are at record lows with unprecedented monetary stimulus.

- At 0.7000, the NZD/USD exchange rate is not over-valued or under-valued against historical ranges.

- Dairy, log and other commodity export prices are close to historical highs, in theory fuelling regional incomes, investment and spending.

- Increasing house prices are driving strong consumer demand from the “wealth” effect.

However, the current and near-term performance outlook for the overall economy is a long way from any boom label. The economy contracted 1% in the December 2020 quarter and will be flat or marginally negative in the March and June quarters. We are headed into a double-dip economic recession in 2021 following the impressive “V-shaped” recovery through the middle of 2020 when Kiwi’s spent their overseas travel money in the local economy.

The failure of the New Zealand economy to advantage and grow from the very favourable winds listed above is explained by the following counteracting forces: -

- Business and consumer confidence surveys still portray an uncertainty and wariness about the future due to the insidious nature of the Covid pandemic.

- Businesses across all sectors of the economy and annoyed and frustrated from external factors beyond their control i.e. labour shortages, supply chain/shipping disruption and delays, increased employment costs from Government policy changes, input costs all rising and increased regulatory compliance costs.

- The ending of strong immigrant inflows has removed a major positive impetus that the NZ economy has benefited from over the decade before the Covid pandemic hit us 12 months ago.

- Government policy delivery/implementation failures with Kiwibuild housing, “shovel-ready” infrastructure construction projects and now impending delays with the Covid vaccine roll-out due to bureaucratic ineptitude.

- Dry climatic conditions for the eastern agricultural production regions through this autumn is not looking good for future output volumes.

Expect little response from NZ policymakers

How the policymakers at the RBNZ and Government respond to this evolving and deteriorating economic picture will play a part in future NZ dollar exchange rate direction. Expect the RBNZ to re-state that the level of monetary accommodation needs to be maintained at the current high levels for a considerable time yet in their statements this week, 14 April (one-page review) and full MPS on 26 May. Governor Adrian Orr is a “dove” and like the RBA, he will want to see increases in real wages before changing the current super-loose monetary policy settings i.e. NZD negative.

The New Zealand Government (in the writer’s opinion) will struggle to understand the current economic situation described above, let alone devise new policies to improve the economy’s performance and benefit the standard of living across nationwide households.

Judging by the highest price increase intentions since 1992 in the recent ANZ business confidence survey, substantially higher inflation this year is inevitable. Therefore, we are headed for a period of flat/negative GDP growth with higher inflation (i.e. stagflation), which is a big change from the very positive environment (prior to March 2020) of relatively high GDP growth and very low inflation. On average, households will be worse off. In particular, the non-property owning, lower socio-economic sectors who are facing rent increases thanks to tax policy changes from a Labour Government (that is supposedly representing them).

Do not expect any innovative economic policy initiatives from Finance Minister Grant Robertson’s budget on 20 May to address the aforementioned economic challenges. Borrow, tax and hope appears to be their sole policy platform. Financial and investment markets, seeking reassurance and confidence from the Government that they are responding to the issues, stand to be disappointed.

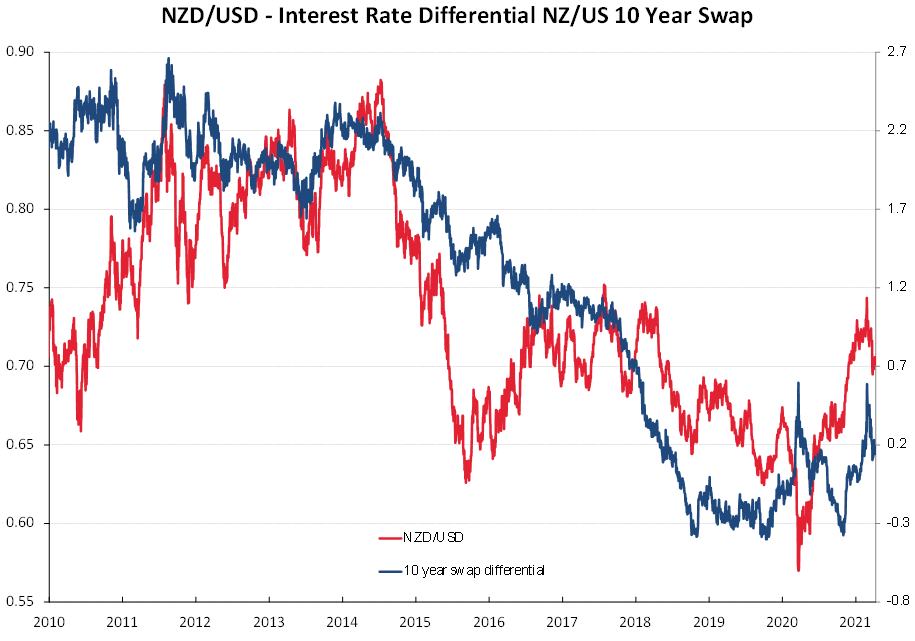

NZ dollar’s favourable interest rate differential has long gone

The 2%-plus interest rate differential advantage that attracted global funds into New Zealand and pushed the Kiwi dollar above 0.8000 (amongst other positives) in the 2011 to 2014 period has long since passed. Currently NZ 10-year swap interest rates are just 0.2% above those in the US, so there is absolutely no incentive to be buying and holding Kiwi dollars over US dollars.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

46 Comments

The tea-leaves seem to be concentrated in the bottom of the cup.

Clearly the Government isn't the only one having trouble addressing inflation/deflation/stagflation - otherwise described as a growth-requiring system 10 years past the peak of real (physical) growth.

We've been trying to fix virtually, something which is virtually impossible to fix. Interesting to watch some still chanting the mantra, in light of that. Sort of: Don't worry, she's unsinkable.....

"Do not expect any innovative economic policy initiatives from Finance Minister Grant Robertson’s budget on 20 May to address the aforementioned economic challenges. Borrow, tax and hope appears to be their sole policy platform. Financial and investment markets, seeking reassurance and confidence from the Government that they are responding to the issues, stand to be disappointed."

NZs greatest issues are the lack of vision and delivery skills of those at the top. When you elect idiots without a clue, you have to expect bad policy.

We have no alternative politicians aside from perhaps TOP or Greens who are actually interested in creating real economic growth by incentivising investment in business and not just their property portfolios. National will only keep the status quo of subsidising and protecting property investment, then faking growth with a reliance on nominal GDP growth by importing people (once it's possible again).

(As an aside, I'm surprised Kerr still seems to believe in a "wealth effect". Thought most people were moving on from that silliness.)

PS, Roger:

Westpac economists see no big increase in rents after housing policy changes

Reserve banks are losing control and so does government as have no vision and are just trying to cover with bandaids - all over, when need surgery.

The surgery had to occur after the GFC...but it was all too hard. You don't fix a crisis caused by excessive debt and excessive risk taking by doubling down on debt and risk taking, yet that was what the PTB chose to do. As a result we now have bloated asset bubbles, zombie corporations, chronic malinvestment, and zombified markets where price discovery is non-existent. This is a zombified global economy hooked up to the life support of QE and interest rate suppression.

Scary thing is, I can only think of one way it will all unwind - war!

The interconnectedness and ponzification of our global economy will mean the pool of plebs at the bottom will grow larger and larger until we either plug into the dystopian system or revolt... I'm guessing for the later (jingoism and need to blame will appoint more Trump like leaders in future).

That would have required asset owners to accept less free money. It was not a possibility allowed. They could not be asked to stand on their own two feet and bear responsibility for their own investment decisions.

Who would have thought it? Everybody should be thinking it!

When you base your economy on a housing bubble & MMT government spending, you'll get lazy and increasingly poor economic performance out in the wider economy. True capitalism based on savings, investment, productivity, creative destruction & dynamism of thought and action is being discouraged - nay, stamped out. We now have a 'post work' mindset enabled by monetary debasement and currency manipulation via QE and heavy handed interest rate suppression. There is no interest at all in lifting productivity: we are going hell-for-leather in the other direction with more holidays, more sick days, a 'work from home (or don't work at all)' mentality. When you have a so-called economic (housing) 'boom' during something as adverse as a global pandemic where tourism revenue has been vaporised, you don't have to be Einstein to realise that something has gone terribly wrong. Our economy could now best be summarised as 'Print, Borrow, and Hope'.

Unfortunately well put.

Last weeks Roy Morgan poll showed women overwhelmingly support Labour - I think it was 54% women and only 36% men. At the same time I saw an article on politicians body language and specifically Jacinda's body language and how its designed to be welcoming and empathetic - this appeals to women who look to Politicians body language whilst Men tend to listen to the words of politicians.

Looking at this article the Roy Morgan Poll says it all- labour are driving away men in droves becasue they are "saying alot but really saying and doing nothing. Women on the other hand - whilstever Jacinda is smiling and saying nice things will continue to believe in this government even when things deteriorate. That said Labour will be in a world of pain if Jacinda calls it a day.

ikimpaul,

There speaks a true dinosaur. Women just look at body language, while men actually listen. Evidence? Nil. You quote an article which makes claims about the PM's body language and a poll showing that woman overwhelmingly support labour and then simply conflate the two.

A very sexist theory drummed up by male chauvinist pigs. JA's hand-flapping and excessive grinning makes me unlikely to slow down in my car if I were to encounter her jaywalking, and even less likely to vote for her- Mrs. Dago.

I'm not sure I agree with you regarding Jacinda's appeal to women. I can only base this on my personal observations. My wife was the first in our household to comment that JA is good at talking, but not 'doing' (can't believe that after declaring a climate emergency, she still sees plastic produce bags at the grocery store, for e.g.). According to my wife (who goes to the gym, out with friends, social activities, hobbies and volunteering), she is coming across more and more women who can't believe they voted for Labour.

This is the poll https://www.roymorgan.com/findings/8679-nz-national-voting-intention-ma…. The stats are quite startling- I'm not sure there has ever been an 18% spread between women and men voting preferences in NZ. However in context -46% of women dont support labour.

this appeals to women who look to Politicians body language whilst Men tend to listen to the words of politicians.

LOL

I'm a man but this is ridiculous. The same phenomenon occurred the other way around when John Key 1.0 was in power.

Looking at the rise of Female leaders Globally I see a change in the wrong direction - Abject Failures - H Clark, Ardern, most of Labours Cabinet, May, Merkel, Pelosie, AOC, La Garde etc etc. Time to revert to a system of appointing those best qualified preferably with a history of success and ignoring sex or race.

Like who?

For all those listed examples you could add equally useless male examples: Duterte, Trump, Bolsonaro, Bojo, Putin, Key, Erdoğan etc.

I do find it highly perplexing how Mr Orr could rationally wait for higher wage growth (in REAL terms) when you just stated (rightly) that inflation is going to take off - AND probably exceed wage increases. If inflation exceeds wage rises, then people get worse off. Hence demand will fall etc.

RBNZ talks dovish drivel about looking through inflation but people on wages do not have that luxury and will not borrow more either.

All that stimulus that was pumped in could possibly be connected to inflation?

Although I fully accept that most of inflation is cost-push due to freight costs.

By the way, Minsky followed Keynes in stating that wage increases that increase demand do not detect form employment.

You are looking for someone to blame and it is not Adrian Orr. Read, Read and absorb

"The ending of strong immigrant inflows has removed a major positive impetus that the NZ economy has benefited from over the decade before the Covid pandemic hit us 12 months ago"

"Benefits"? You mean like papering over the cracks in our economic policy so politicians could get away with saying NZ was doing ok?

"Benefits" like bringing in more people than we were building houses to contain, or infrastructure to manage?

With benefits like these, who needs disbenefits?

EDIT: Sometimes the "read more" link is very close to the "report comment" link. Sorry Mike.

Yes I think it should have read "a major positive impetus that the house owning class has benefitted from". For the young, renters, Maori the strong immigrant inflow have been an absolute disaster. It has locked them out of the housing market, suppressed real wage growth and led to businesses believing they can import skills rather than training kiwis. Even most economists believe the statistic named "GDP" is a useless way of measuring the economic wellbeing of a country's citizens.

The silver lining in this dark cloud is that NZ may be forced to innovate and increase productivity as major earners like Tourism will not return to pre covid levels anytime soon.

... in all fairness to the current lightweight politicians in power , the previous Key-English government only grew the nation's GDP by flooding the country with immigrants .... take those 300 000 new citizens out of the picture , and we've been running on the spot economically , for over a decade ...

At a micro anecdotal level - Just opened my house and contents insurance renewal this morning. It has gone up 31% since last year. I had no salary review this year because of covid etc. But my property values have gone up about twice my salary, so I will pay it out of that .... ?

Some people's insurance policies will have gone down - insurers are less inclined these days to let Northland insurees subsidise the earthquake risk of (say) Wellington insurees. Bear in mind that your house value is replacement cost not the combined value of the land and house. As most of the value is in the land in most cities, your house insurance shouldn't have gone up with the market.

You know that every business is thinking in regards to wage & salary rises: "They'll just make their money from their house, innit". Probably they will think you are greedy if you ask for a raise. They'll be praying the borders open soon so they can once again access that infinite pool of cheap foreign labour.

Starts with J ends with apan.

Except we have way lower productivity.

If your job or business is more than 1 degree of separation from the government teat and the perpetual annual income increases. Then you are in for some serious pain. Especially if you have exposure to international competition. All of you work from home suckers will have your day of reckoning soon as well. When your job is being done by someone working from their home in Mumbai or Manila.

One way or another, we are all going to get our dose of austerity.

A good time for property investors to explore options in America. Increasing property prices and an appreciating currency will be a double win.

The current government has no clue about economic policy. Conditions will deteriorate over the next two years. Who will the government pick on next? Probably the farmers.

Carden provides a directly focused analysis of the secular stagnation thesis.

He suggests that supply-side constraints on productivity growth may be more

likely reasons for the recent slowdown in real economic growth in developed

countries

An interesting read here on productivity. - https://www.fraserinstitute.org/sites/default/files/costs-of-slow-growt…

In addition I think it will be interesting to see how the Nordics, some of whom rely on oil and gas for GDP leverage, sit in the rankings when oil falls to $25 at some stage in the near future. https://www.youtube.com/watch?v=y916mxoio0E

That's a new one... so the RBNZ now according the author... ignore inflation in assets, ignore inflation in consumer prices, and only raise interest rates when the peasants are getting wage increases above their station?

How does this reconcile with:

Under the current Policy Targets Agreement (PTA) the Reserve Bank is required to keep annual increases in the CPI between 1 and 3 percent on average over the medium term, with a focus on keeping future average inflation near the 2 percent target midpoint.

There was never a crisis in NZ. For some reason everyone feels that it will never happen in NZ, that it is immune. I have been in manufacturing my whole life and i can see (involved in manufacturing) the things are changing in NZ and Australia (including reduced demand and redundancies as a consequences). The cost of manufacturing is increasing, making it less and less competitive. Costs of everything in NZ is going up, and you can't buy anything so it goes up even more! We are already in stagflation, or we are heading there. The amount of money that is being pumped into the economy is staggering - but there is no value creation in that. Sure, many people are much wealthier on paper due to properties but in reality we are all way, way worst off. I'm keen to hear below how other manufacturing businesses are doing and how they feel about next 12 months....

Sad thing is no-one gives a shit until headlines in paper say X plant is closing with N staff redundancies...!

Why?! no long-term vision for our economy and no accompanying infrastructure investment for it! Seems we are content to just export raw agricultural based commodities and hope we have a 'China-like' market to keep it all going.

Current NZ Debt is $120 Billion and increasing by $128 Million a day - NZ Debt Clock.

Well, every recent government has rewarded unproductive asset occupation rather than productive enterprise. Because they were all property investors, as were their advisors and central bankers.

This gets us into the position we're now in. Greed and laziness did it.

How would NZ have performed had it been ravaged by Covid ?

false dichotomy!

Well written article by Roger Kerr - I agree him that the NZ economy will underperform because of the government’s poor decision-making & that;

“we are headed for a period of flat/negative GDP growth with higher inflation (i.e. stagflation), which is a big change from the very positive environment (prior to March 2020) of relatively high GDP growth and very low inflation. On average, households will be worse off. In particular, the non-property owning, lower socio-economic sectors who are facing rent increases thanks to tax policy changes from a Labour Government (that is supposedly representing them).”

Stagflation - Well done the last couple of Governments. If we just took our medicine in 2008 and let the risky and speculative choke on the nasty medicine they so clearly deserve, but no, we must protect our banking overlords at all costs. So we have passed the buck down to today...

Options - let the speculative take their super nasty medicine, or, financially decimate all savers (retired) and non asset owners who traditionally vote Labour. What to do.

Popcorn.

With property investors no longer buying, how is the RBNZ going to pump the rest of the $100 billion into the economy? Banks wont lend to anyone else. There won't be enough FHB to soak up the 40% of housing stock that investors buy. So that's NZ's QE cut off at the knees. What happens when property prices start falling and owner occupiers stop buying houses as well?

Its worse than that. FHB's will be unwilling to buy because of anticipated house price declines. Any recent purchases could be in trouble. If Ireland is anything to go by then investors will bail out and take a haircut quickly, while home owners will stay the course and end up in deep negative equity. Ironically the governments actions could have the opposite of the intended effect.

KW - Lawyers and Real Estate agents will join the dole queue and the current collection of clowns in the Beehive should be looking at relocation to Auckland Island.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.