By Bernard Hickey

Finally, Auckland's Generation Rent have found someone who is actually talking about the elephant in the room of New Zealand's political economy - rampant speculative demand for housing by landlords.

Reserve Bank Deputy Governor Grant Spencer gave a speech in Rotorua this week that everyone who has ever worried or debated the thorny issue of Auckland's astonishing house prices should read.

He spelt out in the plainest language yet that rental property investors were taking advantage of the tax incentives available to leverage up with cheap debt to buy as many houses as they can get their hands on.

These investors can see that the powers-that-be have allowed or created an opportunity for extraordinary leveraged tax-free gains.

Every grown-up in town -- the banks, almost all the politicians, the land bankers and reality television show producers - are telling them to borrow against the pumped up equity in their homes to buy more rental property.

They can see net migration at record highs, strong economic growth and a shortage of 25,000 dwellings that is not being whittled away.

They can see that voters, for whatever reason, decided against a capital gains tax and limits on foreign buyers at last year's election. They can even see the Labour Opposition leader Andrew Little is going soft on the idea of taxing their capital gains and New Zealand First Leader Winston Peters has never been keen on the idea.

They've seen the median house price in Auckland rise 20.1% in the year to March, once adjusted for the skewing effects of all the million dollar-plus house sales.

They can see the Reserve Bank's hands are tied by inflation being below its 1-3% target and therefore can't put up interest rates.

They can see banks continually passing on record low interest rates in Europe and the United States to them in the form of falling fixed mortgage rates.

They can see banks ramping up competition for their business through mortgage brokers, now that BNZ has rejoined the market after a decade-long hiatus.

They know they are on the biggest investment free kick in New Zealand history. And even better, they know no one is going to stop them.

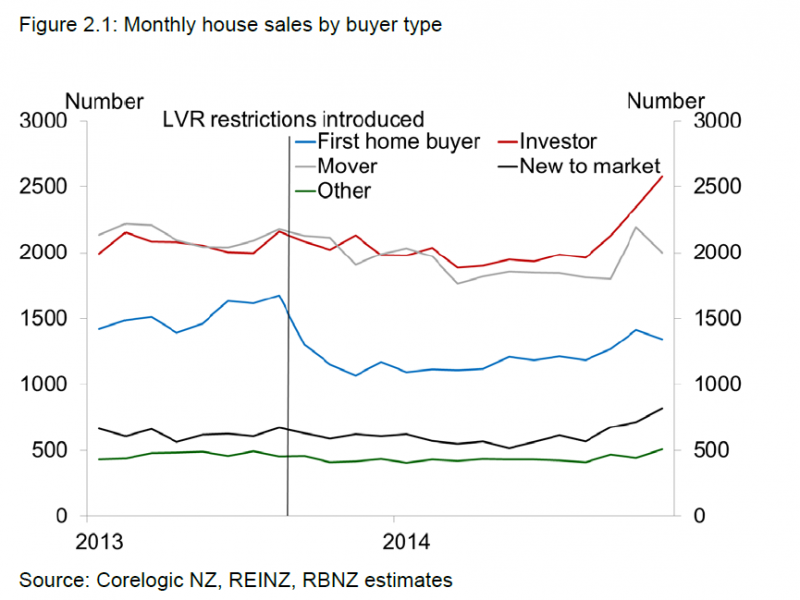

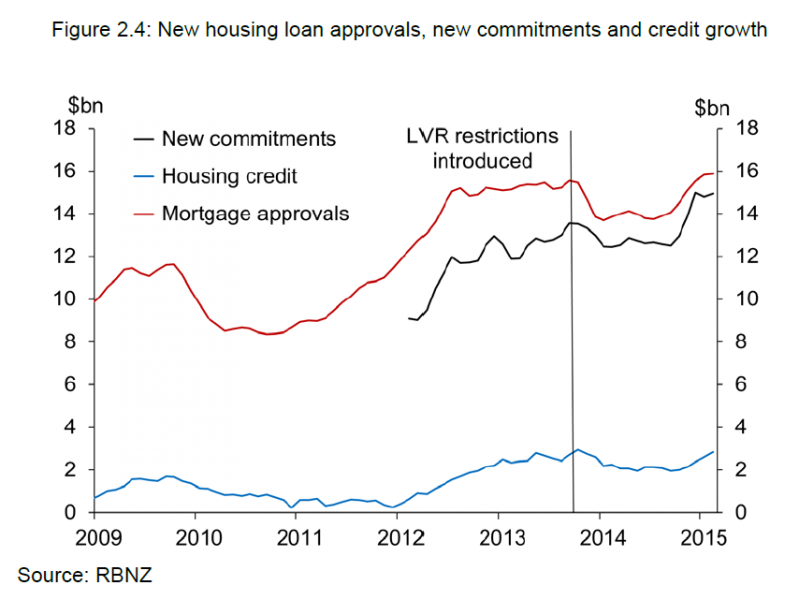

Mr Spencer pointed out in his speech that new mortgage lending was growing at an annual rate of 20%, with borrowing by landlords in Auckland the biggest and fastest contributor.

Over the last three months, more than NZ$15 billion of new mortgages were pumped into the market, with more than half of that going into Auckland.

More than 2,500 houses a month are now being bought by landlords, more than any other category of buyer, including first home buyers and owner-occupiers moving from one home to the next. That's up 25% in less than a year.

The Reserve Bank has exhausted its toolkit, having put up interest rates and introduced limits on high Loan to Value Ratio (LVR) lending. It is also looking to increase capital requirements for mortgages to landlords, but it knows it's not enough.

Exasperated by yet another explosion in Auckland house prices, the Reserve Bank has asked for some 'mates' to help it control the risks to New Zealand's banking system, which relies on house values to back 60% of its loans.

Mr Spencer called for the Government to revisit the tax incentives for landlords.

"Housing is the most tax preferred form of investment, particularly when it is highly leveraged," he spelt out.

"Indicators point to an increasing presence of investors in the Auckland market and this trend is no doubt being reinforced by the expectation of high rates of return based on untaxed capital gains."

He also suggested new tax measures to encourage land bankers to put houses on undeveloped land.

The Government's response was to essentially say: 'Talk to the hand."

Housing and Construction Minister Nick Smith described the Deputy Governor's comments as vague, and repeated the Government's opposition to a Capital Gains Tax, saying other officials at the Productivity Commission were not in favour and it had not worked in Sydney and Melbourne.

"He (Spencer) has been non-specific about his tax proposals and we are not satisfied that the tax system is at the core of the problem," Mr Smith said.

The Government is now ignoring the crisis of demand and supply in Auckland by refusing to consider taxing landlords' property, refusing to slow inward migration, refusing to limit foreign buyers, refusing to build large numbers of new affordable houses itself and refusing to fund the infrastructure needed to underpin those new houses.

Generation Rent can now see the issue clearly. The Government's top economic advisor has said the tax incentives for landlords should be reduced and apartments in central Auckland should be built in defiance of the NIMBYs controlling Auckland politics.

The politicians in the Government and the Council are refusing to take that advice. Landlords are celebrating because nothing will change.

At what point does Generation Rent start using their votes to change those politicians?

----------------

A version of this article was also published in the Herald on Sunday. It is here with permission.

53 Comments

Unfortunately getting Genrent to block vote will be like herding cats most of which are blind.

When the LTVR regime was first mooted I said it would have no effect whatsoever . Just read my comments on this site at the time.

This is a supply side problem , there is simply not enough land on the market , its tightly held by land-bankers , developers and speculators and the city has too many restraints on growth with its arbitrary ring around the city

You say it has had no effect what so ever- its blocked lots of people out of buying a home by not being able to get a loan.

I agree more land needs to be released, its quite sad what this is doing to the place that Auckland once was

'At what point does Generation Rent start using their votes to change those politicians?' Because of post '60's "family planning" their parents will always out vote them.

Becoming single and retired I chose to downsize from a four bedroom to a two bedroom home away from Auckland but I have more land. I felt it was abhorrent to be living in so much wasted living space when so many are struggling to own a home. I wonder how many singles in a similar situation feel any responsibility.

Incidentally, I do not miss Auckland at all, especially its horrendous traffic problems. And I am near Thames hospital that has already proven to be a life saver.

Very admirable Didge. I trust your "abhorrent" feelings inspired you to also sell your house at a cheaper-than-market amount to someone "struggling to own a home."

That would be foolish and would not have helped my grand children whom incidentally, are NO longer assisting those in society that are primarily greedy unproductive parasites.

In my wider family there is a growing movement toward consolidation of living arrangements and we have opportunities to influence others in this regard. Grey Power may also become a useful tool. Certainly more practical uses of living space must have an impact upon Auckland house prices. WE oldies are a growing power.

So Didge, despite your initially fine words, you DO put your self-interest ahead of those "struggling to own a home."

Do your issues about people "struggling to own a home" have to be fixed by other people's money?

Whom do you believe are the greedy unproductive parasites?

Hey me too, i hate what auckland has become, i can only go back there for a day or two at the time. 40% of the population is forecast to be asian soon, i guess they are use to what that place is turning into

Would mates for the Reserve Bank and generation rent look like this?

http://mp.natlib.govt.nz/detail/?f=subarea%24Drawings+and+Prints+Collec…

No problem we just need to find some century old voters and politicians.

Note: I cannot seem to do links from Chrome with the new changes, I am missing those icons.

Bernard, my friend is an ordinary NZ bloke with an ordinary NZ family all doing ordinary NZ jobs.

This bloke has 3 siblings. Between these 3 siblings and himself they have 10 children

Those 10 children range in age from 28 to 48

7 of the 10 own their own homes, 3 are renting

One owns 2 houses (one being a rental in Auckland)

Another owns 3 houses

3 of the children are more wealthy than their Baby Boomer parents

2 are equally as wealthy as their Baby Boomer parents

And this is just an ordinary NZ family with ordinary NZ children with ordinary NZ jobs

As far as i can tell most vote for National because they feel they have done well under JK

I would never vote National so i am not making it up.

I work with a lot of new graduate nurses (nurses with 0 to 5 years experience) in Christchurch. None of them own a home, none of them are saving to buy a home. If you ask them about home ownership -you get a wistful look. Most of them don't understand how they are being screwed. But for a whole generation the ordinary dreams of previous generations are not for them.

Brendon - About 3 years ago, i wrote in here that my daughter, a solo mum with no help from the father, bought a flat in Christchurch.

I got howls of disbelief, but it is true.

She got 100% mortgage from SBS

Now she pays less on her mortgage than people pay in rent.

On top of that she has made about $80k capital gain

I was garantor for her mortgage but she is now free ond stands on her own two feet.

Excellent Mike, if you had another younger daughter (or a grand daughter) could she buy her sisters (mums, aunts) flat off her as easily? Given she would have to pay an extra $80K.

Of course it is possible to buy some property in Christchurch. But that 'something' is getting worse and worse.

The expectation of the powers that be is each new generation will lower its standards to get on the property ladder.

Previous generations as far back as the 1890s did not accept a poor status quo system, they demanded the system works for them. At some point Generation Rent will demand the same too.

Your daughter hasn't "made" any capital gain. She won't make that unless/until she sells.

.

What she's 'made' in the meantime is an increase in rates, which is cost, not a gain.

Back in about the 70's people had to get 2nd mortgages at higher interest rates (unsecured rates) in order to buy a house. This is good because if a person defaults then the banks are covered by the house while 2nd mortgage lenders loose out.

"He spelt out in the plainest language yet that rental property investors were taking advantage of the tax incentives available to leverage up with cheap debt to buy as many houses as they can get their hands on."

Get some quotes hickey, because him or you are telling lies.

there are NO tax incentives or tax free gains.

Demonstrate how it works VS a small business startup of similar size.

AND STOP BLOODY LYING.

How many small businesses can fund themselves making losses for 10+ years? What do you mean by similar size - $30k turnover or $400k capital?

Could it be that the Reserve bank governor is creating a crisis, then claiming he needs more tools (fools). Meaning he needs more power and a fat pay rise?

his tool, the OCR worked 30-50 years ago during the development phase, while there weren't many cashed up businesses and few foreign firms in Nz. (and banks were NZ companies)

Push the interest rate around, everyones buying patterns changed,

But now many people are up to eyeballs in debt OR have no NZ debt. Changing the OCR makes little to no difference to them.

The OCR itself only came into existence in 1999.

Generation Rent being the likes of financial commentators who sold their Auckland house convinced prices were going to drop?

Or Generation Rent being an economist who is frequently quoted in the media and has always said renting is a much more sensible financial option than owning?

What has predicting all the twists and turns of a complex market based system got to do with advocating for a better, more stable and fairer regulation of the property market?

fairer and more stable for whom? Foreign investors are doing very well, thank you.

Bernard, our family all voted against national this last election. We all voted for different parties for different reasons. None voted labour. Each of us in our own way without much discussion on the subjects were disgusted with much of Nationals behaviour and policies. Perhaps most was foreign investers allowed easy access to our homes and farms. I have heard from a good source the chinese deal with Lochinvar will go ahead, along with 3 other big farms in the area. Plus they are on the cusp of buying many more. My children want to farm. They dont want to work for chinese masters. Or swedish or Australian or yankees. Or for that matter the 1%ers of kiwis. They want to own a farm themselves. With John Key at the helm there is little hope. Those printing fiat in far off lands need somewhere to put it. And Key n co are offering up our kids houses and farms gleefully. I remember the guy that sold his farm a few years ago, kept the house and a few acres. Sadly looking around. The value of his money was negligable. The value of the land had risen 10 fold.

Because nz is a paradise compared to the rest of this crazy world, our land is extraordinarily valuable. Key and his cronies arent valuing it as such. They are flogging it for a few pieces of fools gold.

There was a time when New Zealand governments broke up a few large estates so they could be sold for many family owner occupier farms. Back then, 125 years ago, New Zealand voted for progressive liberal parties. Is that the sort of 'mates' that the Reserve Bank needs?

http://www.nzhistory.net.nz/cheviot-estate-taken-over-by-government

sums it up nicely

Once upon a time ....

NZ used to be the land of milk and honey where every-one had a fair go

Now, today, competing against foreign nationals to whom, whatever price New Zealand puts on its assets, is mere pocket-fluff ...

The hope and expectation of a fair go is gone

We have already had the discussion about "Once upon a time" and it was concluded that it was a time of rampant drunkenness, wife beating and racism among other evils and something we would never want to go back to. We have no choice but to roll on toward Elysium with its super-rich Asian girls.

How true Belle.

Maybe the Deputy Reserve Bank governor should have mentioned land value taxes instead of capital gains taxes to find more mates. There certainly seemed to be lots of 'mates' for LVT here at interest.co.nz that think this sort of tax change will help achieve the sort of outcomes Grant Spencer is hoping for.

http://www.interest.co.nz/opinion/75040/bernard-hickey-looks-grant-spen…

If the Reserve Bank wants to target property investors why don't they limit banks lending to investors (non-owner occupiers) where income in the form of rent does not cover interest + principle payments?

because they don't actually want to target _property_investors_. They want to target those pesky NZ citizens who buy houses and won't pay rent to their masters.

I think investors here and overseas are suddenly realising the massive tax incentives they get from house investments in NZ and no capital gains tax. More tax incentives than most other countries. Things like stopping the claiming of tax from interest on mortgages is one that would correct the housing market tomorrow. There are numerous legal tax dodgers for landlords if he has a good accountant !!

What is the exact definition of "investor" vs. "owner occupier"? Example: a friend of mine bought a place few years back and moved to AUS about 2 years ago. The place is rented out now.

Did he become an investor 2 years ago? Should he evict his tenants to remain defined as owner occupier? Should his interest rate be manipulated upwards by government to punish him for renting out?

The world of 2015 is globalized. People switch countries, jobs, private circumstances like never before. And you want to fix problems by bringing in laws fit for the 1950s?

PeterPen the Reserve Bank could have the same rule as the LVR being that it should apply to 90% of loans, so there is some leeway for the sort of situation you outline.

Oh dear

Over on NBR, UK blow-in, Treasury boss Gabriel Makhlouf espouses the supply-sider argument and rubbishes Grant Spencer

He spouts forth a lot of words, more-or-less saying the solution is, more of the same, without explaining where, when, how, or by whom. Genius at work

http://www.nbr.co.nz/article/treasury-odds-reserve-bank-over-cgt-171606

Interesting comparison between Spencer's and Makhlouf's views

Who do you believe?

Neither of them and I'm just a pleb ;)

A CGT will raise tax but have limited effect on demand.

Building more houses would help but that isn't going to ramp up quickly and how many would actually need to be built to satisfy demand...?

With demand high, the solution is to force the real 'investors' (foreign cash) to build new.

I'm with Mr Makhlouf on this ... if your wish is to discourage house construction and refurbishment , then charge ahead and introduce a CGT ... a CGT will suppress improvement and innovation , and will slow down the turn-over of assets ... BUT ....

... if your wish is to have " affordable housing " , then identify the key problem : Which is the price of land !

Then take measures to address that .

Generation Rent already had someone talking about the housing crisis. I'm also a Generation Renter.

None of the extra regulatory proposals will make one positive difference.

The housing crisis is the result of market distortion caused by excessive regulation.

The high price of land is the result of an artificial shortage caused by the Metropolitan Urban Limit.

As regulatory bodies get further involved, the price of that land becomes more unaffordable.

A cumbersome consents process has ensured it costs an average of $33,000 for permission to build each house.

The Reserve Bank's LVR did nothing to arrest the growth of house prices, it just made home ownership even less attainable for young families and the poor.

The National government's increased grant for first home buyers will only further fuel inflation, increasing the demand in an undersupplied market.

A capital gains tax will just add an extra cost which speculators will factor in to their activities; it will be passed on to the next person who purchases a property from them.

Every new regulation will result in a new cost which will be passed on to the purchaser.

The solution is to abolish the Metropolitan Urban Limit, streamline the consents process and respect private property rights so the Council gets involved less often.

LOL. Sure, sure...

Are you sure "market distortion" is the cause? I would blame economic dogma and human greed as the cause.

This is not a generational problem.

The problem started around 2008/09 (when a lot of "investors" in Auckland were sweating the natural and overdue fall in real estate prices) when instead of letting market forces sort out the global debt crisis, quasi-Socialist governments in the US, UK etc and their central bank cronies decided to switch to central planning economy by manipulating the supply (= money printing) and cost (= zero interest) of money so that they could stay in office for a bit longer.

A lot of people could have gotten a reasonable deal even in AKL until about 2011. That is NOT a generation ago.

Another issue is the widespread absence of highly paying jobs in NZ. Scarcity of land and rip-off Council fees do not help it, but are imho not the main aspect. NZ over decades has not developed any modern high paying industries, but is continuing with the same old stuff (Australia the same, paying the price for it already). The world around us has not stood still, however.

This is not just about house prices, it is about the failure of the Socialist economic model of the "West". Good luck to all of us, but it will end where Socialism has always ended.

Now, now Peter, steady on. Next you will be saying that socialists eventually run out of other people's money.

So lets be clear here "market forces" / free markets have caused the crisis, but that's OK lets let the same sharks fix it. Plus in terms of low interest rate btw it was Greenspan who took us down this path, a libertarian and free marketeer. http://www.urbandictionary.com/define.php?term=Greenspan+put so it was no switch but a long held and used policy.

it seems yourself and a few in here do not recall or understand that the entire global financial system was about to freeze up with the resulting mayhem that would have caused globally if the US Govn had not acted.

This isnt caused by socialism, its caused by free markets and how they do not work, Keynesian policies are if anything being used to stop this happening with some success.

Bullshit steven. How exactly are Keynesian policies having any success - by blowing asset bubbles and perpetuating failed economic theory?

Socialism certainly didn't cause the problem, capitalism did - the capitalists always want others to pay.

The Keynesian easing is being applied but it's not working as there's no stability occuring and the globalisation is not providing overall market success through specialisation; so when the Keynesian bill falls due the cupboard will still be bare. All that's really happening is the expansion of private credit resulting in a one trip to the big banks.

My Iron Law of property markets is that the more Bernard Hickey complains about property the better investment returns must be.

For a while now Bernard's has been on fire ... raging ... about people involved in the voluntary exchange of money and property. The markets must be booming.

I don't need to do any more research. Life's great in landlord land.

The 'Auckland' problem is common to many other cities worldwide, giving a lie to the supposed supply crisis. Overseas money and investors are fuelling the crisis with cheap cash - we all know this. CGT will not work as here because it hasn't dampened prices elsewhere. I suggest targeting land bankers who tie up usable space rather than developing it. Tax all subdividable land at 1 per cent of its value pa. People sitting on a large section (owner occupiers) could defer the tax to when they subdivide or sell.

Commercial investors would pay each tax year. This would discourage land speculation and free up land for development. Existing rules around cgt should be implemented, say the profit investment property held for less than 10 years should be taxed at the owners marginal rate as it is income, after all. Losses too should be tax deductible after 10 years. The lvr has played into investors hands and is a farce.

A whole generation of young people are being forced to buy crap homes at staggering prices and any action should not force THEM into negative equity.

The CGT has worked elsewhere, see its effect on the UK, seems to have worked very well actually.

is that why prices are so reasonable and housing so widespread in the lower socioeconomic groups in the UK?

5% on non owner occupied land might do it.

CGT gives an impression of fairness but does not address the problem

It is clear to see Spencer is not a tax accountant. There are no tax advantages being a mum and pop property residential investor. If there was CGT then the traders would have a drop in tax from 33% to the 15% proposed by the failed Labour scheme. The single biggest tax saving in our society is being a non resident tax payer. Non resident Foreigners only pay 10% on their interest earning on the Billions they have on on term deposits in New Zealand. Why not start talking about their favoured tax position.

Meanwhile changes to the depreciation and LAQC rules for property investors means an extra One Billion NZ$ per year extra tax. This has stopped new rental construction in its tracks and forced investors to snap up existing homes which were previously owner occupied.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.