By Gareth Vaughan

The Third Coming of Reserve Bank restrictions on banks' high loan-to-value ratio (LVR) residential mortgage lending is predicted to shave up to 5% off house price inflation within a year.

This guesstimate, from the Reserve Bank itself, says the plan detailed yesterday to tighten credit availability, primarily to residential property investors, will dampen house price inflation by between 2% and 5% in the first year of implementation. This means the Reserve Bank expects a bigger impact than it did from either the high-LVR restrictions' first or second iterations.

The Reserve Bank predicted its initial crackdown from October 2013, that restricted new residential mortgage lending at LVRs of over 80% to no more than 10% of the dollar value of banks' new housing lending flows, would reduce house price inflation by 1% to 4% over the first year that policy was in place.

Then last November when the Reserve Bank tweaked the LVR restrictions, to ensure borrowers would generally need a deposit of at least 30% for a bank loan secured against an Auckland rental property, it predicted the move would reduce Auckland house price growth by 2% to 4% over the first 12 months.

Whether the up to 5% dampening effect actually happens, or whether the up to 4% reductions for either round one or round two of the LVR restrictions occurred, is certainly debatable. But what's not debatable is the fact that house prices, in Auckland and more recently around New Zealand, have continued rising strongly despite the Reserve Bank's moves - so far - to restrict the flow of bank credit.

Real Estate Institute of New Zealand figures show that from September 2013, the eve of the initial LVR restrictions, to June this year, the Auckland median house price surged $251,000, or 44%, to $821,000. And the New Zealand national median house price jumped $100,000, or 25%, to $500,000.

'Billions of dollars of high-LVR lending hasn't happened'

In the consultation paper issued with its new LVR restriction proposals the Reserve Bank acknowledges that risks associated with the housing market have "increased for a much longer period than expected at the time that the LVR policy was introduced in 2013." It also argues that the LVR restrictions are improving financial system resilience by increasing households' equity buffers.

The Reserve Bank claims about $20 billion of lending at an LVR above 80% has not happened because of its initial high-LVR restrictions. And, it says, about $3 billion of investor lending at an LVR of above 70% has not happened due to last year's changes.

And the central bank, which says its LVR restrictions are about improving the stability of the financial system and reducing the impact on the financial system of any severe housing downturn, has previously pointed out the stock of high-LVR lending in banks' mortgage books fell to 13% of total loans in December 2015 from a peak of 21% in 2013.

"The policy appears to have reduced the risk of a [house price] correction, by curbing the rise in house prices and credit growth by approximately 5%," the Reserve Bank suggests.

Action is required on many fronts

Nonetheless, yesterday's Reserve Bank statement quoted Governor Graeme Wheeler saying; "The drivers of the housing market strength are complex and action is required on many fronts that extend well beyond financial policy. Broad initiatives to reduce the underlying housing sector imbalances need to remain a top priority."

This comment could be interpreted as Wheeler returning Prime Minister John Key's "they should get on with it" comment directed at the Reserve Bank earlier this month, and then reiterated. Key's comment came just ahead of a speech by Reserve Bank Deputy Governor Grant Spencer is which Spencer effectively called for action from the Government to tackle runaway house price inflation.

Spencer pointed to three key areas well outside the Reserve Bank's remit, but where government moves could make a difference. These are housing supply, tax, and migration policy.

Of housing supply Spencer noted, "the key challenge in the long run is to expand housing supply to meet the growing demand."

The latest Statistics NZ building consent figures show just 61% of the new homes Auckland needs monthly to keep up with demand were consented in May. And HSBC economists recently estimated Auckland has a shortage of about 30,000 homes, which is equivalent to about 6% of the region's total housing stock, and that the shortfall is increasing by about 7,000 homes a year, as record low interest rates and record levels of net inward migration fuel demand.

Tax and migration policy

Spencer also said it was important to explore policies that "will keep the demand for housing more in line with supply capacity." Two key areas here are tax and migration policy.

"On the tax front, the implementation of the bright line test for housing investors introduced in October last year has helped curb short-term speculative activity in the housing market. Consideration might be given to further reducing the tax advantage of investing in residential housing," he said, pointedly noting we have "a tax system that favours debt funded capital gains."

Or as NZ Herald columnist Brian Fallow recently put it; "The message from the tax system is clear: if you want to provide for your old age, don't save money. Instead, borrow and engage in highly geared plays in the housing market."

On the the controversial issue of foreigners buying New Zealand houses, Spencer suggested the introduction of a requirement for a New Zealand IRD number had probably restrained housing demand for a period late last year and early this year.

And on migration Spencer said; "We cannot ignore that the 160,000 net inflow of permanent and long-term migrants over the last three years has generated an unprecedented increase in the population and a significant boost to housing demand. Given the strong influence of departing and returning New Zealanders in the total numbers, it will never be possible to fine-tune the overall level of migration or smooth out the migration cycle. However, there may be merit in reviewing whether migration policy is securing the number and composition of skills intended. While any adjustments would operate at the margin, they could over time help to moderate the housing market imbalance."

Key, however, was quick to respond, ruling out changing his government's immigration policy to help tackle housing problems.

The housing affordability challenge

In the latest iteration of its high LVR restrictions, the Reserve Bank is proposing that, from September 1, no more than 5% of bank lending to residential property investors across New Zealand would be permitted with an LVR of greater than 60% (i.e. a deposit of less than 40%), and no more than 10% of lending to owner-occupiers across New Zealand would be permitted with an LVR of greater than 80% (i.e. a deposit of less than 20%).

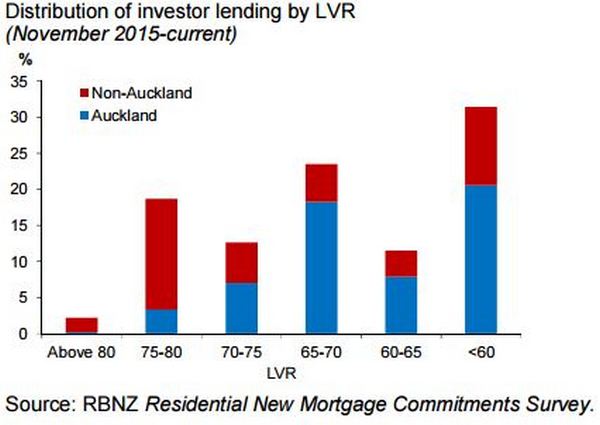

Based on the current LVR distribution, the Reserve Bank says its proposed nationwide investor speed limit would potentially impact 70% of investor lending, split roughly evenly between Auckland investors, primarily at an LVR of 60% to 70%, and non-Auckland investors primarily at an LVR of 70% to 80%.

We can debate whether the Reserve Bank has, in high-LVR restrictions, chosen the right tool to tackle the housing bubble. Certainly many would-be first home buyers, finding themselves requiring bigger and bigger deposits, haven't been thrilled. But the Reserve Bank is doing something.

And the Reserve Bank is now lining up two potential additional tools. Also within the scope of its so-called macro-prudential tools, it is looking at both potential limits to high debt-to-income ratio lending, and the possibility of making banks hold more capital against housing loans (a counter-cyclical capital buffer or capital overlay). (I've previously argued for higher bank housing capital requirements here).

The other step the Reserve Bank could make to try and take heat out of the housing market is, of course, to increase the Official Cash Rate that's currently at 2.25%. But with annual inflation having now been below the 1% to 3% band targeted by the Reserve Bank for seven consecutive quarters, that's off the table.

Against this backdrop the ratio of Auckland house prices to average income has reached 9 or 10, and the house price-to-income ratio outside Auckland has got back to its pre-Global Financial Crisis peak of 5.3. Internationally a multiple of no more than 3 is generally regarded as a good marker for housing affordability.

Former Reserve Bank Governor and ex-National Party leader Don Brash recently suggested Auckland house prices need to fall 60% to achieve affordability, given waiting for income growth to catch up with flat prices would take 50 years to restore house price to income multiples to around 3.

Meanwhile, investor lending has risen to 36% from 28% of overall mortgage lending over the past 18 months, and to 46% in Auckland. The Reserve Bank says about 30% of mortgage lending is now done at a ratio exceeding 6 times the borrower's income. Although record low interest rates are supporting loan serviceability for now, if interest rates and/or unemployment rise significantly, this picture could change dramatically.

Where the buck stops

The key point is that the time for Reserve Bank-style fiddling around the fringes is well and truly over. If we're to rein in Auckland's housing bubble and genuinely tackle housing affordability issues, the Government, not the Reserve Bank, needs to take the lead. Big decisions need to be made. Local government also has a role, notably around consenting and land allocation and pricing. Thus Auckland Council's impending Unitary Plan offers a key test on the local government front.

But ultimately central government can override both local government and the Reserve Bank. This, along with the various levers his government could pull, means the Prime Minister's office on the ninth floor of the Beehive is where the buck stops.The question is whether the government is merely governing for existing property owners or the greater good.

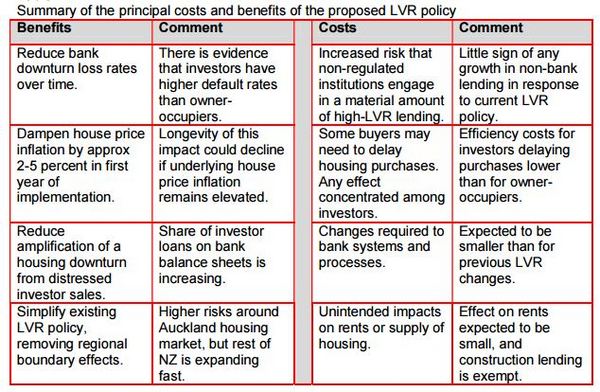

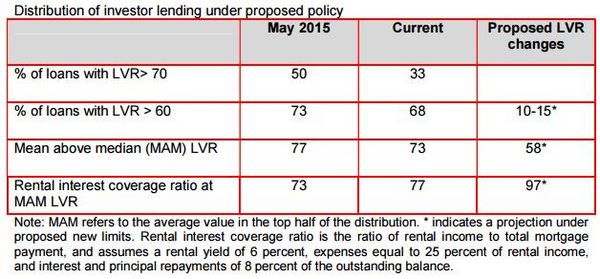

*The tables and chart below come from the Reserve Bank's consultation paper on its planned changes to restrictions on high-LVR residential mortgage lending. It wants the changes to take effect from September 1, and has called for submissions by August 10, which is less than a month away. Bank lobby group the New Zealand Bankers' Association said yesterday it was too soon to comment on the Reserve Bank's new high-LVR proposals.

*This article first appeared in our email for paying subscribers. See here for more details and how to subscribe.

58 Comments

There is no silver bullet but its the elephant in the room that no one wants to accept. CGT, Stamp Duty & enforcement by IRD of the 2yr buying and selling rule. The "tinkering" with loan ratio's, urban boundary's and city intensification is a fools game which achieves very little but is an expensive bureaucratic exercise for rate payers. The National party are ideologically opposed to Market Intervention.A change of Government is the only way to break this deadlocked death spiral.

Did you see the above graph? Less than 35% of new investor lending since last November was at an LVR of < 60%. Based on that, how do you figure that a 60% limit would do 'very little'? Sure, it may not have much of an effect on price growth, but by definition it will shore up bank balance sheets and increase financial system stability, which is the aim of the game.

The only fair way to control house prices is to stop investors claiming tax against the interest on their mortgages and to bring in a capital gains tax.

What they have done is exclude first home buyers out of the market and first time investors Overseas investors and "well healed" local investors will not be touched by the RB measures.

John Key will not touch the tax system when it comes to property investment because his wealthy backers may have to pay their share of tax.

More taxes won't build houses.

Reduce immigration and the supply will eventually catch up. Prices will stabilize.

Stop the rest of the world being allowed to purchase any NZ property under 5ha.

Working class NZ'ers can't compete with the other 6 billion humans on the planet. NZ for NZ'ers!! Why should we compete with the rest of the world to buy a house in NZ?

The buck stops with JK. Can anyone tell me if he is actually still alive?

There also used to be a guy called Smitty who ran round in circles making all sorts of proclamations and noise on housing that never came to anything also. In the oil industry they would call him a "seagull", fly in, wing clapping, squarking and s??ting on everything and then fly off, forgetting whatever went down.

The Unitary Plan is out in a few weeks.... they better let people build up and out, the Nimby's can get stuffed if they don't like it, especially the Kohi crowd, Kohi is going to look like the gold coast in 20 years.... so is Takapuna Milford etc

The UP will definitely have more up and out in it, surely no independent panel could decide otherwise. The question is whether the council will accept the plan.

Exactly. Unfortunately the NIMBY contingent aren't exactly going to shrug in resignation and let everyone get on with it.

I expect many more 'consultations', 'reviews', 'challenges' and 'discussions' until, at some point in 2032, the Council agrees to consider implementing a review of a course of action that may, or may not, result in the densification of central suburbs.

Yep, the only way that the council, NIMBYs, and grey rinse brigade can be removed is if we have a NZ version of the Khmer Rouge. Mind you, I wouldn't particularly mind seeing Len Brown walking around a Northland farm followed by thousands of council workers in black pajamas carrying buckets of water for irrigation. The old folk can be set aside to cook the rice and boiled tripe for their daily meal.

Let's put the pyramid of skulls in Paratai Drive, as a warning to others.

No point. Most of the houses will be empty. Some can be used for re-education facilities.

Westfield Mall, then. In the space they use for Santa's Grotto.

One NIMBY is equal to a hundred non NIMBYs. There will be quite a battle.

There are enough plastic bags at the landfills....

We are going to need really strong leadership then, someone in the mould of Churchill to steer us unwavering towards a fairer future for all. A brilliant take charge energetic kaiser that will overcome entrenched resistance and boldy go with no fear or rearward looking.

Let's face it - we are stuffed.

In Ancient Rome there was a system where if something had turned into a terrible insoluble fustercluck, somebody suitable would be called out of retirement (one of the most famous was described as leaving his plough) to take charge as all-powerful emperor of that one thing, with a free rein to do whatever necessary to fix it. Then when it was fixed, powers were removed and he'd go back to his farm in the Campagna.

And wasn't that position called "dictator". And wasn't there one person who was stabbed to death after granting himself those powers for life? And I think the fusterclucks that the Romans needed to resolve were armed hordes at their city's gates, not poor urban planning and finger pointing politicians.

Not to say that the mess does not need to be resolved, and that someone has to take charge, but all that is required now is action by those that can take action (i.e. parliament).

Or we could try; not filling our country up with people, Oh gosh! that would be to simple, problem solved.

Yes - the debate on demand has never been completed.

Also - Never been contemplated by the Nationals as it would upset their artificial GDP growth figures

Also for big projects. Those aqueducts weren't going to build themselves.

Political lesson in there for our leaders. Remove enough checks and balances on power, and the only recourse left is for somebody to jam a knife in the emperor's guts and watch him wriggle.

Isn't that CERA?

It only works if you have a competent person to begin with.

churchill was a nut...

We can keep the cost down by using some of that excess Chinese cement production.

For a very loose definition of 'cement'.

Why not higher density in Otahuhu, Panmure and those close in suburbs where prices are lower, sections larger and have not been re developed into very high value properties on very small sections. I can not see anything that is affordable to FHB coming out of the Eastern Bays, Just very high value, high spec apartments for foreign buyers and investors. I see the FHB as just a stalking horse for parties that have their greedy eyes on a totally different market that will do nothing for average Kiwis.

Building high rises in Kohi, Takapuna and Milford is not going to provide affordable homes for anyone. I don't understand this urge to suggest this unless it's just to spite the people living there currently.

While I agree with this change and like the simplicity of one limit for all investors, I can see it accelerating house price inflation outside of Auckland, perhaps in some of the areas that have been relatively unaffected at this point, such as New Plymouth, Palmy and Dunedin. I don't think the leveling of LVR limits between Auckland and other areas will be enough to offset the increased capital requirement, which is likely to see investors seeking better bang-for-buck, as they have already started to do.

One of the points that doesn't seem to be getting much discussion is the fact that this is good for first home buyers (notwithstanding the reduction in ex-Auckland speed limit) as it makes them relatively more competitive in the market. It's not within the RBNZ's mandate, but it could be useful from an equality perspective to offset a lowering in general LVR limits with an increase in investor limits, or to lower general limits prior to lowering the investor limits, when the time comes.

Nothing by itself will help as long as the Government does not take the initiative. RBNZ can and will do its part but what about the government. Buck has to stop with them.

National Party can only delay the inevitable and Question that should be asked is whom is the government trying to protect. Why are they not acting on foreign Buyer, specially Asian.

It is no hidden secret, you go to any auction in Auckland and can check who the buyers are and fail to understand why is government so obliged and under pressure from them that fails to take any action.

Things have started to move now and whether or not National Party likes it or not will not be able to deny and ignore for long as slowly we are moving towards election. The main reason of their denial is to protect their Non Resident Asian friends and many being Non Resident will not vote though will get total support of Asian but are limited (using the word Asian instead of country as otherwise many feel it as racist). Next election will be Asian + Rich benefiting VS Rest of New Zealand. Has really Divided the society like no other has done before.

No it does not, as an investor can still leverage against new builds.... it makes the investor more focused now on them at the fFTB demise..... Developers like investors as they can sign land/build packages,,,,

One reason for the high level of investors in the Auckland property market is down to the densification that is going on. I see old houses all over the place being subdivided and then 4 new properties being built so the high investor level is not entirely bad news. They are increasing the housing supply and density both of which we need.

Is buying a house, subdividing, and building another considered a new build for LVR purposes?

If you are a property developer then its different lending criteria..... there is more risk to the bank as a half built house is worth almost only the land at mortgagee auction (a few went through after GFC you need to be a builder to touch them) ....

As the developer you could presell the subdivided new builds as land/build packages to investors and not be captured inside the regulations..... as the RBNZ want more houses in the system.... with good lawyer you could structure the lending to sub divide something you own and build on the back with high leverage....

Dont hate the developers, if enough are built rents will fall, and prices will come dowm, clearly AKL needs more houses, funny enough it looks like the lending required to build a large number of new homes is getting more difficult to get just as the cycle turns, normal behaviour from banks to limit supply so that prices dont fall too far....

The National party should come out of denial and take on their responsibilty.

Thus is petfect time for government to put some measure on non resident buyer like Sydney along with measure by RBNZ like LVR and loan to Income restriction ( which too should be announcrd on 11 Aug together with LVR insteaed of waiting to have more impact instead doing in piecemeal).

Any measure by national beside supply along with RBNZ measure is the need of the hour.

Will they stand up or still run away from their responsibilty to act is to be seen.

The Heading Should Not be where the buck stops in housing BUT how to make the national government realize that the buck stops with them - The Government and it is they, only them, who can take measures to control, unfortunately being in power. Wish people had more option than to wait till next year election.

If helpless and not able to understand that what is required today is to curb speculation, non resident buyers (except crying supply ...supply- which is important but even if released today will take couple of years to have any effect. Supply process has started and will take it own time).

Please resign and let their be fresh election as nation needs answere and not excuses and lie.

“Limitations can only be undone by the mind that created them.”

― Erin Fall Haskell

No point in discussing where the buck stops BUT Do Know Who Who Has Blocked The Buck AND Solution #Jkexit

Sadly, the Government won't act, because anything they’ll do may crash house prices and put the blame on them which in turns will hurt them more in the polls and instead of being strong opposition, National will become worthless opposition with much less MP’s. Politics is the game here.

They already down on polls and are probably already worried about fourth term.

So I suspect no decisions will be made until election time, while the latest restrictions put in place by the RBNZ will not hurt investors as most of them got enough equity anyway.

If National will win Forth term then I believe more measures will be put in place.

Dreaming, 3 years ago " If National will win 3rd term then more measures will be put in place." Then you can compare the price to 3 years ago.

If JK willing to put any measures to house price, he should have done this years ago, now it just get to big to fall.

Here is one of the professional views on this matter, i am sure that some will enjoy it !!

http://www.nzherald.co.nz/opinion/news/article.cfm?c_id=466&objectid=11…

the above information is 100% true and the people who are in the business of property development and investment know this only soooo well. ACC have been snoring on the wheel for more than a decade and they wont wake up until they get a kick in the guts.

What we see today is partly the result if mismanagement and complacency... FHBs were not born 5 years ago, they were there and were buying until 2013 when the masses of returning people and immigrants swapped what ever was available in the housing stock, they pushed up the more modern and expensive ones first and the rest is history.... in the last 3 years the ACC was fiddling around making plans and withdrawing them .. building cycle lanes and complicating traffic while pushing the huge housing issues under the carpet ... their collective planning and management skills are very questionable, and the proof is in the pudding!

While repeating old news helps making a long comprehensive article Mr. Gareth Vaughan, it also keeps inflating and distorting a real comprehensive and fair debate on the issue . We do that for the well being of the Nation, not of the few!!

After all, everyone is dependent on the others and need each other to survive and prosper.

I say that caution is now required to prevent agitating some mislead and financially illiterates people to distort the entire issue.

It is not a challenge and it will not be won by loud noises, its a problem that needs to be calmly and wisely discussed and solved .

Inflaming articles won't help, neither will daily hammering of the same events and news albeit almost selectively.

Anyone who wants to create ciaos and start a political campaign, it is too early for that, save your breath until next year .. and get out there and Vote!!

Someone told me today of a property in Scott Point that has changed hands six times in a year. Yes that's right, six times! All Chinese interests.

I want to know whether each transaction has been subject to the Brightline test. Presumably that applies to foreign nationals who transact in NZ as well as kiwis?

I will be writing to my MP on this matter.

There was a report in the Herald a few weeks ago where people had sold their mother's house after she died, and in the six months or so following, it was re-sold four or five times, putting on about $600,000 in the process. Several owners on from the original sale, some of the deceased lady's stuff was still lying on the floor. Nobody ever moved in.

This is all completely unshackled from real demand for houses as dwellings.

Oh I nearly forgot foreign property speculators are not contributing to the housing crisis!

It's just garden variety money laundering. The Switzerland of the south pacific has a locust problem.

Yep. And the thing about money laundering is that eventually you want it back as a liquid asset, not a pile of mouldy gib board in Avondale where the ownership can be easily traced by any person or investigator who cares to create a login account.

We're more the Swaziland of the Pacific than the Switzerland. Perhaps our leaders failed geography. And spelling.

Frtiz, if you have an address for this Scott Point house I'd be interested in checking it out - gareth.vaughan@interest.co.nz

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

Well,well

Who would have thought the head of ANZ Bank would see it this way

Next we will be hearing super property spruiker Tony Alexander saying there is a crisis!

Tony A says it's all good for another two years.

Guess who pays Tony Alexander?

You all miss one critical issue, leverage. In an era where leveraging is like building a bomb, the answer isn't simply less leverage. Even and LVR of 60% will blow apart at the seams when leverage goes in reverse.

I'm a young couple living in Auckland looking to buy my first home. I take John Key's advice and buy a home as he repeatably told us there is no housing crisis and it's just a sign of success that houses cost this much these days. Nothing to see here. And John Key, being the Prime Minister is full of integrity, trust and leadership so of course I should take on-board his advice - heck he's worth $50 million so he knows what he's talking about right when it comes to markets and good investment policy right?

Then two years down track, the housing market goes bust and I've lost 50% of my equity in my $900,000 home in Auckland. I've also just lost my job because of the recession. I am bankrupt. Am I in a position to sue John Key for damages? He's the Prime Minister who is sworn under oath to serve the country - (which my understand of this would include the people that reside here). He knew the risky position his leadership and policy setting had caused, but continued to lie/deceive/deny about the state of the issue misleading me into making a poor decision. I pay the guys wages (via taxes) so expect reliable advice - like I do a financial advisor. Is he liable?

No, there is no duty of care owed by the Prime Minister to individual citizens in respect of investment choices they make. Furthermore, Crown immunity will apply.

If your old enough to buy a house your old enough to think for yourself. Many of the problems with the "have nots" in NZ is that the expect to suckle on the Government teat forever... Here's a thought, get up off your knees and start working for once.

The only way to cure the housing crisis is to make every Landlord a dinosaur.

Then there will be plenty of houses available at a price tenants can afford,

Landlords are just parasites taking advantage of the vulnerable in 90% of cases

The only way to cure the housing crisis is to make every Landlord a dinosaur.

Then there will be plenty of houses available at a price tenants can afford,

Landlords are just parasites taking advantage of the vulnerable in 90% of cases

What's the point HeavyG? With individuals like you it doesn't matter how hard I work right now - given the rules/regulations I'll never get any closer to the desired goal. And if I choose to, which believe me I have, I'm just feeding greedy monsters like yourself via rental income and taxes.

I think I'll stay at home, watch skytv, go for two coffee's - one in the morning and one in the afternoon, plan my next holiday through Europe, update my instagram and wait for my parents to die then take their inheritance...

I think I'll have a mental breakdown otherwise if I try and play the game by the rules that are currently being enforced. Which I can do - but then you'll need to start paying for me to be in mental rehab getting a pay out from the government. Not sure which you prefer?

You seem to want some form of Communism where everyone else works for your pleasure. Those days a slowly going and as resources become limited people will be less likely to fund the lifestyle choices of others.

You cannot have a society where the unemployed expect the same entitlements as a worker e.g. home, car, sky TV, smokes, kids... There are plenty of migrants more than happy to come to NZ and work hard and not whine about why the cannot buy a home when they are working part time, swilling lattes and laying on their parent's couch (sound familiar?..).

National is making moves to reduce housing NZ stock and to replace detached homes with smaller units (and hopefully in the future hostels) for those unwilling to earn a home. Try selling crazy but it looks like life in the institutions isn't that hot if the patients are being restrained and locked in rooms for weeks on end (more efficient resource wise).

You should set up the NZ Communist party but you won't as even that would require too much effort. So that leaves you with whining on these websites with your "woe is me" attitude.

Fair enough Heavy G but I am a bit confused as to what the government's role is..

I really think they should at least be doing something more than speeches and shaking hands with dignitaries here and on "Fact Finding" tours overseas. This mob take laissez-faire to a new level with their do nothing approach. I only wish they had this as an event at Rio - JK would be a shew in for the gold.

FYI, we have the David Hisco article up here now - http://www.interest.co.nz/opinion/82697/anz-ceo-david-hisco-argues-several-levers-must-be-pulled-take-heat-out-property-market

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.