By Gareth Vaughan

Doing the same thing over and over again and expecting different results is a famous definition of insanity attributed to Albert Einstein.

This quote came to mind this week when I read a speech from Reserve Bank Assistant Governor John McDermott. He said inflation is expected to rise in the December quarter and be at the bottom of the Reserve Bank's target range. Nonetheless further monetary policy easing will be required to ensure that future inflation settles near the middle of the central bank's target range.

As ANZ's economists noted, McDermott's comments were viewed by financial markets as making "it clear that another OCR cut in November is happening".

The Official Cash Rate is already at a record low of 2.00% having been cut by 150 basis points since June last year.

The Reserve Bank's Policy Targets Agreement (PTA) with Finance Minister Bill English requires it to keep inflation between 1% and 3% on average over the medium term, with a focus on keeping future average inflation near a 2% target midpoint.

In the June 2016 quarter the Consumers Price Index (CPI) rose 0.4% from the March 2016 quarter. And for the year to June 2016 the CPI inflation rate was steady at 0.4%.

In its August Monetary Policy Statement the Reserve Bank forecast annual CPI inflation would rise to 1% in the December quarter, and to 2% in the September quarter next year. It has now been below 1% since the September quarter of 2014, and was last above 2% in the September quarter of 2011.

Going around in circles

We get the September quarter CPI figure next Tuesday, October 18. That may help paint a clearer picture of whether the Reserve Bank's forecast for December quarter inflation will turn out to be correct. However, with inflation there have been a few false dawns. Notably during 2014 when the Reserve Bank hiked the OCR by 100 basis points to 3.50%, saying inflationary pressures were increasing and were expected to continue doing so.

Thus we've been going around in circles with inflation and the OCR for a few years now. And with the OCR set to be cut to 1.75% at the next OCR review on November 10, we in New Zealand are closing in on a tipping point towards the really, really low interest rates that are now a blight in other developed economies.

And to what end?

Will a lower OCR really help magic up the inflation the Reserve Bank craves to meet its target? I'm not convinced.

And will it help our exporters by weakening a New Zealand dollar that has been stubbornly high for so long? Again I'm not convinced.

The Kiwi has weakened against the US dollar over recent weeks. At the time of writing it's at US70.4 cents, down from US74.72c on September 8. (Over the same timeframe the Trade Weighted Index, TWI-5, has dropped 4% to 74.9).

Whilst expectations of a Reserve Bank OCR cut helps, the Kiwi's weakening against its US counterpart is largely because financial markets think the US Federal Reserve may hike interest rates. Whilst the Kiwi may be the world's eleventh most traded currency, the Greenback is number one with 87.6% of the US$5.1 trillion in daily foreign exchange trades done in the US dollar. We're an ant on the back of an elephant.

Deposit rates at breaking point

US economist John Mauldin argued this week that the world's in the middle of a massive monetary policy error. He argues the US Federal Reserve is destroying the retirement hopes and dreams of tens of millions of people with its super low interest rates.

And Mauldin has a point. Two years on from bringing the curtain down on its Quantitative Easing bond buying, or money printing, programme put in place after Lehman Brothers collapsed in 2008, the Federal Funds Rate, the US equivalent of New Zealand's OCR, is still only at 0.25% to 0.50%. Other major central banks, such as the European Central Bank, Bank of Japan and Bank of England, are still printing money.

Here in New Zealand Westpac Group CEO Brian Hartzer made some interesting comments recently. Hartzer estimated people in New Zealand reliant on bank deposits probably need interest rates of around 4% to live off. Westpac NZ's highest carded, or advertised, term deposit rate is currently its 3.50% six-month rate. This with the OCR at 2% and KPMG's latest quarterly Financial Institutions Performance Survey showing funding costs across the nine banks surveyed at 3.03%.

ANZ is the country's biggest bank and usually the one that sets the tone when the OCR is moved. After the last 25 basis points OCR cut in August ANZ took an interesting approach, with most other banks ultimately making similar moves.

ANZ reduced its floating mortgage rate by just five basis points to 5.59%. (Most home loan borrowers are on lower, fixed-term mortgages). The bank was a bit more generous to commercial, agriculture and business customers, cutting their borrowing rates by 15 basis points. And, in an encouraging move, ANZ increased its five-month term deposit rate by 25 basis points to 3.25%, and its 18-month term deposit rate by 30 basis points to 3.60%. (The 18-month rate lasted just five weeks before being cut by 15 basis points to 3.45%).

Fixed mortgage rates

Select chart tabs

Does this economy need a rate cut?

We've got annual Gross Domestic Product growth of 3.6%, low mortgage rates with the two-year average bank mortgage rate currently 4.45%, and stratospheric house prices in Auckland where the house price to average income ratio has reached 9 or 10. House prices are now rising elsewhere in the country. Doesn't really sound like an economy that needs an OCR cut.

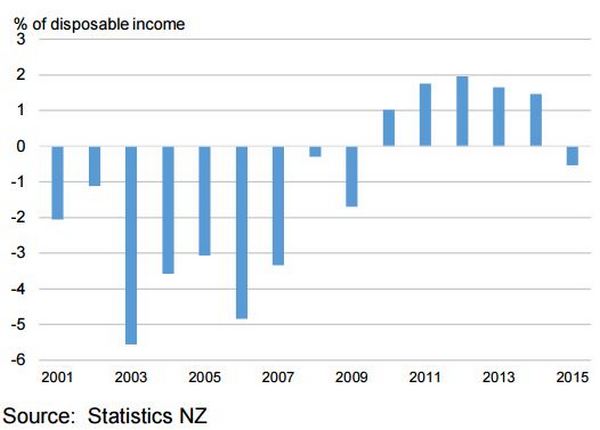

Meanwhile, household saving turned negative in 2015 after a positive run from 2010 to 2014.

And the latest quarterly figures show that household financial liabilities, mostly mortgages, reached nearly $252 billion at the end of June. This number dwarfs the $152.7 billion annual disposable income figure. Thus the debt figure now makes up 165% of the disposable income figure, an all-time high.

Household saving

Update the Policy Targets Agreement

So clearly it's in the national interest to encourage the public to save money rather than borrow it. Thus the time has well and truly come to start turning off the cheap credit tap.

The Reserve Bank could start this process by not cutting the OCR on November 10.

Yes, this will probably mean the central bank continues to be in breach of its Policy Targets Agreement. But this agreement needs to be updated for a changed world. Why not tweak the Policy Targets Agreement so the Reserve Bank is simply tasked with keeping inflation between zero and 3% with no target midpoint?

As Bloomberg notes in this article that highlights difficulties a range of central banks are having with inflation targeting in a world of low inflation and even deflation, there is a precedent for such a move. Citing weaker demand, an ageing population, and intensified price competition in global and local markets, the Bank of Korea has set its inflation target for 2016 to 2018 at 2%, down from 2.5% to 3.5% between 2013 and 2015.

It's time New Zealand took the bulls by the horn and made a similar change.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

35 Comments

Well here's a good reason why the OCR will need to be lowered soon: http://tass.com/economy/904364

Gee thanks John for insulting Putin.

The last six OCR cuts since June 2015 have resulted in the lowest residential mortgage interest rates in 60 years - and have continued to fuel the housing price inflation - and have reduced any incentive for saving other than by investing in property - and have not yet reduced the TWI. A seventh OCR cut will likely fuel more housing price inflation and allow banks to further reduce overall savings deposit interest rates.

The last six OCR cuts since June 2015 have also resulted in an increasingly lower inflation rate so one could claim that the effect of lowering the interest rates is the opposite to what the Reserve Bank is assuming and that there is certainly no sane reason for doing it.

They have resulted in the lowest nominal rates, yes. But real (i.e. inflation adjusted) rates are what matter - and those were consistently negative until the mid 1980s. No doubt Joe Public pays more attention to nominal rather than real interest rates though

Why not target -2% to +2% inflation with the aim of balancing the current account?

It wont work ..... either way you look at it there is a deflationary cycle and Mc Dermot is going to receive a hospital pass if he succeeds Wheeler , because there is nothing we can do about it

The Reserve Bank is required to implement monetary policy in a sustainable manner, having regard to the efficiency and soundness of the financial system.

The RBNZ stated in its latest MPS that monetary stimulus effected by the lowering of interest rates is “expected” to generate stronger consumption by the wealth effect.

In the RBNZ’s model of the economy, NZSIM, there is a component which models how “households select how much to consume and save based on their expectation of the entire path of interest rates”.

However that model does not include consideration of loans, banks, credit, or money! so there is every reason to be skeptical that it is worth anything at all.

It is clear the NZSIM model is failing the RBNZ badly, and as a result failing NZ badly. The RBNZ need to look at the real world to test the basic assumptions of their model: it is apparent by an financial planning model, and now clear by simple observation, that a reduction in interest rates below a normal rate necessitates a disproportionately greater rate of saving, and therefore lower consumption.

Not only is the reduction of interest rates clearly ineffective in increasing inflation in CPI, we are now at the point where lowering interest rates further is not sustainable, not efficient, and with private debt growing 9% is certainly not contributing to the soundness of the financial system.

RBNZ directors should step in to stop the nonsense being perpetrated further.

Janet Yellen's fumbled mumbling only reaffirms that central bankers really don’t know what they are doing, and in 2016 it so much harder to hide.

As MNI notes, regarding Yellen's speech, while a better understanding of exactly how inflation expectations are formed, Federal Reserve Chair Janet Yellen said Friday both actual and expected inflation measures are important for monetary policymaking and are tied to central bankers targets.

"We need to know more about the manner in which inflation expectations are formed and how monetary policy influences them," Yellen said in a speech prepared for the Federal Reserve Bank of Boston's 60th Economic Conference.

"Ultimately, both actual and expected inflation are tied to the central bank's inflation target, whether that target is explicit or implicit."

Yellen did not comment on the current stance of monetary policy accommodation or when the policymaking Federal Open Market Committee might make another move in the fed funds rate.

Instead, she kept focused on the topic of "Macroeconomic Research After the Crisis," which includes the need for a better understanding of inflation expectations.

"With nominal short-term interest rates at or close to their effective lower bound in many countries, the broader question of how expectations are formed has taken on heightened importance," she said.

With many advanced economies struggling with sluggish growth and low inflation, while policy rates are close to their zero lower bound, "many central banks have sought additional ways to stimulate their economies, including adopting policies that are directly aimed at influencing expectations of future interest rates and inflation," Yellen pointed out.

The "unusually explicit and extended guidance" the FOMC used from 2011 to 2014 and the Bank of Japan's upward revision to its official inflation objective in 2013 are such policies, she said.

These and other expectational strategies may be needed again in the future," she said, "given the likelihood that the global economy may continue to experience historically low interest rates, thereby making it unlikely that reductions in short-term interest rates alone would be an adequate response to a future recession."

This echoes her Jackson Hole speech in which she outlined monetary policy tools, including forward guidance, that might needed in addition to traditional tools such as rate cuts if the economy were to take a downturn.

Even as some inflation expectations need to be better understood, Yellen points out the "the standard framework for thinking about inflation dynamics used by central bank economists and others prior to the financial crisis remains conceptually useful today."

She provided a "simple description" of this framework: "Inflation is characterized by an underlying trend that has been essentially constant since the mid-1990s; previously, this trend seemed to drift over time, influenced by actual past inflation or other economic conditions."

Theory and evidence suggest this trend "is strongly influenced by inflation expectations that, in turn, depend on monetary policy," she said.

In particular, "the remarkable stability of various measures of expected inflation in recent years presumably represents the fruits of the Federal Reserve's sustained efforts since the early 1980s to bring down and then stabilize inflation at a low level," Yellen pointed out.

The anchoring of inflation expectations "that has resulted from this policy does not, however, prevent actual inflation from fluctuating from year to year in response to the temporary influence of movements in energy prices and other disturbances," she said.

She asked "how does this anchoring process occur? Does a central bank have to keep actual inflation near the target rate for many years before inflation expectations completely conform?"The influence of labor market conditions on inflation, in part recognized in the Phillips Curve, "seems to be weaker than had been commonly thought prior to the financial crisis," Yellen said, though she has previously said the relationship is somewhat in tact if weaker than previously. Read more

None of the above confirms her right to repeatedly transfer wealth from one cohort of society to benefit another, based upon a blatantly failed pretext.

Perhaps economists have realized the error of their policy decisions and this is a way to justify it to themselves.

Another GFC soon will put paid to all the Central Banks.

The cause of the GFC was mis-allocation of capital by commercial banks.

The solution has been lending to prop up asset markets with low interest rates, creating illusory value, hoping to induce the “wealth effect”.

We have the current spiral:

> Borrowing causes an increase saving as a result of lending (loans create bank deposits! ).

> Saving (rather than consuming) encourages lower interest rates by central banks.

> Lower interest rate encourage more borrowing for buying existing assets;

> Purchase of existing assets with credit increases asset prices;

> Increasing asset prices increases demand for credit (property investors!)

> Demand for credit increases borrowing;

…. And repeat until catastrophe.

We need to break the cycle, the RBNZ should increase rates now.

“To change and to change for the better are two different things."

.

The cause of the GFC was mis-allocation of capital by commercial banks.

The solution has been lending to prop up asset markets with low interest rates, creating illusory value, hoping to induce the “wealth effect”.

And more.

What do you do if you can no longer access primary hedging tools and vehicles? In the search for alternate sources of counter-trend assets, financial firms, even banks themselves, started shorting bank stocks. It’s not as outlandish as it might sound nor even so much ad hoc – there were solid mathematical correlations (inverse, obviously) between bank stock prices and certain financial spreads. Ironically, the SEC and government officials had already started to shift blame to “naked speculation”, even going so far as to ban “naked” short selling on July 15, 2008 – right around the time AIG was starting to get collateral calls and was certainly cutting back its dark leverage “supply” to the rest of the financial system. Read more

What were ANZ short sellers as far back as early 2015 expecting, besides a recent interruption of the downtrend?

Untrue

The cause of the GFC WAS NOT the mis-allocation of capital by the commercial banks

While they may have participated in creating what would become the conditions - they didn't trigger it

The detonator and fuse was something else, unrelated to property, and it got lit

One more reason why the OCR should NOT be lowered is that it will be terribly difficult to raise the rates in the future without killing the economy. NZ is doing reasonably well (compared to most other countries).

LOWERING THE OCR IS A TERRIBLE MISTAKE

Increasing the OCR will mean they must admit they need to update their math to the current modern times. That means dropping the CPI rubbish etc and setting a more realistic inflation monitoring indicator. That being the largest contributor of fiat money devaluing, thus creating huge monetary inflation, namely bank housing loans and borrowing.

But they won't .....because doing this will inevitably highlight that aside from mortgage lending the NZ economy has very little real growth at all. This includes most of the OECD countries

Too lower interest rates for too long created the precursor 2008 global bubbles in the first place. The solution? was .....bailouts!, Now they continue (globally) to try and protect way too much debt via continually lowering the borrowing costs of taking on even MORE debt.... Anyone with even half an economic sense can see this a road to nowhere. They MUST reverse course, change the calculation method and begin raising back up to create again some kind of intrinsic value to currency. The easiest way is to make borrowing and particularly existing loans far more expensive. Many of the weak overburdened ponzi following borrowers out there will lose capital gain which they never deserved in the first place. They produce nothing!

RBNZ Governor Bollard talking to Katherine Ryan of RNZ some years ago said: "sometimes we must pick winners and losers" .

You picked wrong RBNZ!

in Australia, every quarter percent of RBA cut held back by retail banks earns the banks $8million/ day, (on domestic mortgages)

that is a very good incentive to hold back passing on any cuts for as long as possible..

transfer that to NZ, and it would be in the region of $1.5 million/day

so in a a 4-4.5% range mortgage market, holding back 0.25% is almost the same as increasing your profit margin 5% by doing nothing, no wonder they wont pass anything on

So although the RBNZ has the best intention, nothing is going to change in consumer spending without the banks falling into line and letting the cuts through to customers

We've have had a very extreme period of price inflation in fixed assets etc. throughout the developed world which has left us with flat lined consumer purchasing power within our economy. We will have to learn to live with deflation sooner or later if this trend continues. The question is do we go to zero interest rates and quantitative easing with all of the associated difficulties or stop now and get on with learning how to live, invest and operate businesses with deflation?

https://www.theguardian.com/business/economics-blog/2016/oct/12/monetar…

"But more economists are pointing out that monetary policy is in intellectual crisis. Central banks’ tools of low interest rates and QE are clearly failing to boost the economy. Low interest rates have failed to stimulate the economy – we had one of the slowest recoveries from a recession in history – because people and businesses don’t want to take on more debt.

Low interest rates only work by encouraging more private sector borrowing. But levels of private debt are still very high so there isn’t much room to take on even more. And of course, as the IMF recently noted, the best indicator that a financial crisis isn’t far off is a buildup of private debt – so it’s not something central banks should be encouraging lightly."

But what would higher interest rates achieve - trigger GFC2. Surely NZ will then end up following in the footsteps of the rest of the world i.e. Mortgage rates of 2% and term deposit rates of zero.

We also have to consider what higher interest rates might avoid.

Lower the OCR but not for residential lending? only do it for business and farming?

I read on this site about QE (money printing to some), banks laying off staff, money laundering, apple pay, digital currencies, pending financial crisis, financial repression etc. Why does no one mention gold and it's thousands of years of history as a store of value for just such times. For such supposedly well informed people I find it very odd that no one mentions it's qualities, as currencies are debased globally to the extent we now have the formerly unthinkable spectre of negative interest rates.

The argument for lowering the OCR seems to largely centre around inflation or lack thereof. As noted in a recent Bloomberg article China's days of exporting deflation may be over

http://www.bloomberg.com/news/articles/2016-10-14/china-s-days-of-expor…

While the increase is small, the chart of factory gate prices is interesting in that the trend is "upward" and has been since start of the year - does this portend the return of inflation in consumer goods. Only time will tell.

Did anybody hear this interview. Another well informed alternative view that seems very relevant.

http://www.radionz.co.nz/national/programmes/ninetonoon/audio/201816970…'

The main reason house prices have been going up is due to low interest rates (not really a foreign buyer problem in my view)...When our interest rates were an eye watering 10% in the 2007 I also got burned and prices stayed flat for 4-5 years. Local kiwis still drive the market as we mainly buy and sell to each other.

Truth is - the banks wont follow the OCR down. Gouging is the order of the day. We may have NZ's lowest rates in a while, but certainly nowhere near global western rates. Borrow money in the UK - 1.5%. We are still being stung by bank greed.

Banks are a business.

They would not be acting for the best interest of their shareholders if they did not try to maximise profit.

Just doing their job.

Banks are not an ordinary business, they are in an extraordinarily privileged position where their product (credit) can be produced at zero cost, underwritten by the payments system of the RBNZ.

Not to mention when they fail, the RBNZ will arrange for savers pay the cost of their risk-taking via low interests rates and the OBR.

Indeed. That is why they a good investment.

Low yield, but better return than Govt Bonds.

And there is no way they will be allowed to fail.

It's a one way bet.

TBTF is killing the small man while making a killing for the big guys.

Well, sh1t happens.

Don't mortgage up it and expect others to service debts.

Doesn't work that way.

But when Banks load up on bad credit and otherwise screw up they are rescued ?

Yes, banks reward their senior managers with huge salaries to maximise growth.

In practice this means they make riskier loans than their competitors.

When they fail, we can expect the usual rescue practices.

Savers will have their deposits reduced to the extent necessary to keep the bank operational, and will suffer reduced interest rates on their remaining deposits to the extent they are left with any.

We can be sure from overseas examples that despite committing various crimes such as management control fraud (using incentives such as that exemplified recently by Wells Fargo), the managers and directors will go unscathed (because who could have foreseen the result of their incentive schemes and consequent risky lending?).

In short,when bankers screw up they are rescued by savers and taxpayers, protected from any risk to their extraordinary incomes.

The best way to rob a bank is to manage one.

Right about insanity , but there are other ways of curbing lower interest rates feeding into housing prices , which seems to be the primary concern for most of us

We do need to cut the rate , BUT we need to slap a 10% transfer duty on houses bought , and 20% duty for foreigners AND we need to treat anyone with more than 3 negatively geared investment properties as a business and tax the profits on sale as if it were a business

Of course with an election looming , this wont happen

Each time they reduce rates, it just creates another maximum ceiling that housing can rise to, as people can afford to borrow more. At some time they are going to have to go back up, or there is going to have to be hyper inflation, so that wages can catch up with house prices. But I can't see that happening. So at some stage house prices are going to have to drop, to be static for 10-20 years, while inflation catches up.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.