By David Hargreaves

It is always incredibly difficult to know how seriously to take surveys of expectations.

Economists tend to take them very seriously, hence in the case of the ANZ's Business Outlook Survey we get the interesting situation where a survey written up by economists is then reviewed and commented on by OTHER economists.

The Reserve Bank takes its own Survey of Expectations, a quarterly survey of business managers and professionals pretty seriously and has been known to be very strongly influenced in terms of its decision making by sudden swings in inflation expectations in this survey.

I'm not sure if the RBNZ's Household Survey of Expectations is quite as influential within the bank, but for sure the RBNZ will have noted the collapse in house price expectations in the latest survey out last week.

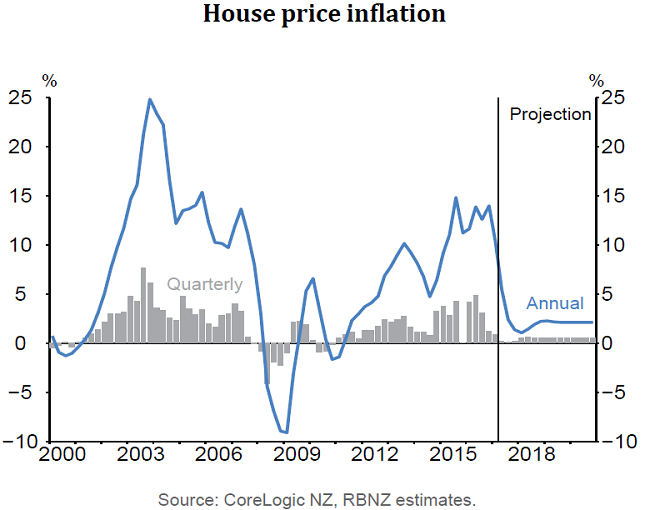

Clearly the RBNZ's household survey (which takes in a sample of 750 views) has not proven that accurate in the past (since 2011) at predicting what house prices would actually do.

So, probably it's biggest value - and it's not alone in this in terms of expectations surveys - is gauging the temperature of people; how they are feeling about things and how they might react in future.

What therefore do we make of a finding that for the first time in the six years the question has been asked that the respondents see essentially no house price growth in the next year?

And is the logical next step that we'll see respondents in this survey next time around (the surveys are quarterly, so it will be into next year) predicting actual falls in prices of houses? Certainly a fair few of our readers - based on the comments stream here - would concur with such a view if it emerges.

The big question then would be how homeowners might react to sitting on a property that might begin falling in value. And while that's still a very big if in my view, look, it's possible isn't it?

(I would stress I think the longer term outlook for house prices in New Zealand and particularly Auckland is very good - particularly given the shortages. But that wouldn't necessarily stop short-term volatility.)

Coincidentally, and the timing possibly isn't great, we've had the new Auckland valuations come out, amid huge interest. And sure enough of course these reflect the massive gains in Auckland property values in recent years.

From a pure investment perspective, it's generally wise if one has had a good 'run' with an investment - but then sees flat times ahead - to 'cash in' and bank some profits.

Houses of course are quite a bit different. Everybody would like to live somewhere and in New Zealand the preference is very much to own your own home. So, the idea of taking profits now, putting them in the bank and say renting while seeing if the house market does indeed fall probably wouldn't hold too much appeal for many.

What though of people who have bought investment properties? This could be more interesting, particularly in the case of people who might have bought properties that don't have great rental yields because they believed they would get capital gains on the properties.

Might the combination of the strong recent gains in house prices and the fact that prices are expected to be flat at best from here prompt a fair few investors to seek to cash in?

The RBNZ itself is not forecasting house price falls, but is picking house price inflation of only something like 2% a year over the next three years.

The RBNZ has also signalled it will have something to say about its limits on high loan to value lending in its latest Financial Stability Report being released on Wednesday, November 29.

This would suggest that the central bank is at the very least going to give some indication as to when the limits may start to be relaxed. The RBNZ has clearly indicated on several occasions that it would not lift the measures all in one go.

With the way the housing market is now looking, I would suggest the most urgent priority is easing the 40% deposit limit for investors.

As indicated earlier in this article, I would see owner occupiers as more impervious to possible short term adverse movements in house prices than those holding investment properties - particularly ones that don't have a great rental yield.

Keeping the market as tight as it now is for housing investors then actually runs the risk of the very thing the RBNZ had wanted to avoid - which is a lot of houses coming on to the market at the same time, putting downward pressure on the market and prices, and therefore putting pressure on the banks and ultimately the supply of credit.

A somewhat complicated emerging situation is further complicated by the fact that the RBNZ is still looking for a new Governor. Acting Governor Grant Spencer reiterated recently that it is still his intention to be out of the door of the RBNZ when his official term as Acting Governor ends on March 26.

It falls to the RBNZ board therefore to recommend a new Governor to Minister of Finance Grant Robertson, with him then officially making the appointment.

At the moment the process is in the RBNZ board's hands. The official word from the RBNZ as of this week is: "The Board is working to enable an appointment to be made so that the new Governor can take up the role when Grant Spencer’s term ends on 26 March 2018. Any announcement is for the Minister to make, after he has agreed to a recommendation from the Board. The Board won’t be giving out possible timing of any steps along the way."

Well, they had better get on with it. The problem for the board of course is that we've had a change of Finance Minister and with that a proposal for some changes in how things work at the RBNZ.

The question is whether these changes make a difference in terms of who the RBNZ board feels is the best candidate to recommend (because it's to be presumed the board absolutely would not want a situation in which the Finance Minister rejected their pick). Then there's the matter of whether the preferred candidate still wants the job given the looming changes.

With the housing market moving into an interesting phase (not to mention a lot of other issues up in the air too) it would certainly help to get a new Governor on deck as soon as practicable.

I think the house market is going to need watching closely next year. Any sign that particularly investors have 'tipped' in favour of selling would need reacting to.

The summer housing market is always intriguing anyway. This one promises to be particularly so.

A few nerves may already be jangling out there. Further signs of softness in the market as we get into the New Year may just make that worse.

29 Comments

Relaxing the LVR limits on investors would be very unwise.

The Bank of England’s working paper SWP619 dated October 2016 examined the issue, their model found that: “The increased demand from BTL investors also drives up the level of house prices by around 59 percentage points. This higher price reduces the number of owner-occupiers that can afford to buy a house, reducing their market share by about 25 percent. They turn into tenants, renting from the BTL investors that bought the houses.” .

If NZ wants to throw FHBers under the bus once again, then relaxing LVRs on investors is a good way to do it.

Well said Peri. Prices are the problem, not access to credit

Yes totally agree with you. With the newly released rates valuation it just goes to show how crazy the whole Auckland property situation has become.

Allowing property speculators to pile back in to this market would be like, pouring money in to a giant bottomless hole.

There was a problem with the policy that Banks implemented in Regards to the 40 per cent deposit required for investors.

The Banks made the 40 per cent retrospective in that the previous loans they approved were also brought into the 40 per cent, which made it very difficult for most to get another cent from them.

Many aren’t able to get anymore to do renovations and maintenance and therefore this impacts on both Banks security and the tenants enjoyment.

Haven’t got a problem with the 40 per cent on newly purchased property but ridiculous to have been lumbered on property that had been bought 10 years ago even though prices were obviously much lower.

Hasn’t impacted on us personally but from other investors it has killed their prospects of buying another property and therefore providing shelter to others.

Don’t beleive this Government has any idea whatsoever on how to handle the housing issue.

Building more houses in Auckland will not solve their issues as there are so many that will never be able to save a deposit and afford to service the debt, and the return on newly built state house will be poor!

Unfortunately the banks make the rules, but to blame the bank is being a bit rich. If people need to use negative gearing for an investment - it is not an investment - it speculating.

Why would people be borrowing more money to do maintenance? That should come out of the operating expenses not capital (which is what you are effectively doing by borrowing - capitalizing an expense).

To use the argument that your are being benevolent is most touching but I think most disingenuous. While some may wish to rent many may want to want their own home.

Re the current Government - perhaps you should first be looking at the previous Government. The current Government inherited the problem after National did nothing.

No, a negatively geared investment is still an investment. A definition of a speculator is 'someone who takes large risks, especially with regard to anticipating future price movements, in the hope of making quick large gains'. Negative gearing can be used as a successful long term investment strategy even when capital gains are quite modest e.g. averaging a few percentage points per year. I find the current focus on using the word 'speculator' to label anyone who uses negative gearing as an investment strategy to be inflammatory and misleading. Negative gearing is commonly used in Australia by so called 'Mum and Dad investors' with just one investment property and is considered normal and acceptable investment practice.

But you are taking a risk - at some point it has to turn positive (and that is not guaranteed) otherwise you are just speculating. I think you are treating negative gearing a legitimate investment strategy just because tax law allows negative gearing. Any business that continually loses money would not stay in business.

The RBNZ set those rules, not the Banks. They were largely only allowed to lend 40% on investment properties and 80% on O/O. It's blended for a mixed one.

If you bought a house 10 years ago with a 20% deposit, shouldn’t you have like 60% equity due to principle repayments and capital gains? It seems to me the real problem is an addiction to debt. Why is leverage so important property investment? I understand debt funding the first, second, third properties, but why does the 40th property have to be leveraged up to the hilt?

Leveraged return on investment. Of course it comes with the risk of leveraged losses too but everyone seems to ignore that.

For example look at this mortgagee sale in Auckland for an example of addiction to debt.

https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

The trademe data estimates that the house is worth $870k on the mid-range figure. The house was purchased in 2012 for $515k. Their financial position should be good if they have been sensible with expenses, however it's likely that the new VW parked out front is financed either through a loan or via the mortgage.

Did the minimum payments finally exceed what they could actually pay?

"it comes with the risk of leveraged losses too but everyone seems to ignore that."

Nope. Since 08 the central banks have had your back ... when they abandoned free markets & capitalism . Prior to that all govts had yr back through tax incentives & chasing easy capital gains GDP growth.

Dp

What a naive graph - a beautiful soft landing (which is utopia) and then a flat curve which has not been seen in the ALL the years prior, for not even a couple of months...

I think it may have a margin of error of 15-20%

What would you do, add some spikes to make it look more realistic? How would you decide the magnitude and direction of the noise? Of course the future won't look like that, and they're not so naive as to think it would - predicting the future is hard.

So it's okay for houses to rise 10 or 20 or more percent a year but the RBNZ "must" step in at the slightest whiff of them falling?

That dear sirs, is a rigged market.

It's completely daft, more magical thinking where somehow everything will work out without anyone having to pay a price. It's not an investment if there isn't risk, so time to pay the piper, sideline investors out of the market and let said market adjust accordingly. If relaxing LVRs is really a RBNZ policy then no one has to wonder who their real constituency is.

any move to try and stimulate investors would have to reinforce capital gains as the yeild in Auckland is so low that Capital gains are necessary to make money on the investment.

So if house prices were to still surge ahead then that would blow the loan to income ratios even more out of whack for owner occupiers. The problem with that is that banks have tightened and are not going to lend 10x income.

Given the way Labour have been talking up getting normal kiwis into houses I think it is more probable that the LVRs would be eased for FHBs

The LVRs might be eased for FHBs at some stage but that doesn't mean the banks have to take notice. Their economists can see what a state our housing is in just as well as the RBNZ and will be requiring high deposits from Fhbs.

What people do seem to forget is that things like this go in cycles. The big problem is that wages are now so out of whack with house prices, and wages just can’t increase, because who is paying for that increase?

Unless they are really good negotiators, I imagine that there will only be 'profits' if they

1) exit the market (move to a cheaper town or rent) or

2) downgrade

... because they'll be buying and selling in the same market.

The valuation is just a modelled number on a piece of paper and doesn't reflect the market price necessarily as markets are driven by sentiment, the state of the house and the relative volumes of supply and demand.

I say let the investors exit the market, they can invest in NZ businesses and let people who need homes buy them to live in them. The sooner we kiwis get over our obsession with property the better for everyone

I would prefer that the term investors was a term referring to people who invested 100% of their own money, rather than punters who speculate with other people's money.

I started off negative gearing but soon saw the down side in that strategy, but kept buying positive cash properties. No sensible investor will exit the market. The sensible ones have too much equity and are waiting for prices to go down slightly to buy again. That is the reality of it.

Rents are providing cash to sensible investors to pay for the mortgage and have something over

for themselves. I can understand people getting pissed off but if there wasn't the demand for rentals then we would be out of business because the return wouldn't be there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.