The housing investors are in full retreat after their full-on assault of the housing market in the second half of 2020 and into 2021.

According to the latest figures from the Reserve Bank (RBNZ), investors had their lowest share of the total amount of mortgage money advanced last month since the RBNZ began publishing the detailed data on mortgages by buyer types in 2014. The RBNZ provided this summary of the figures.

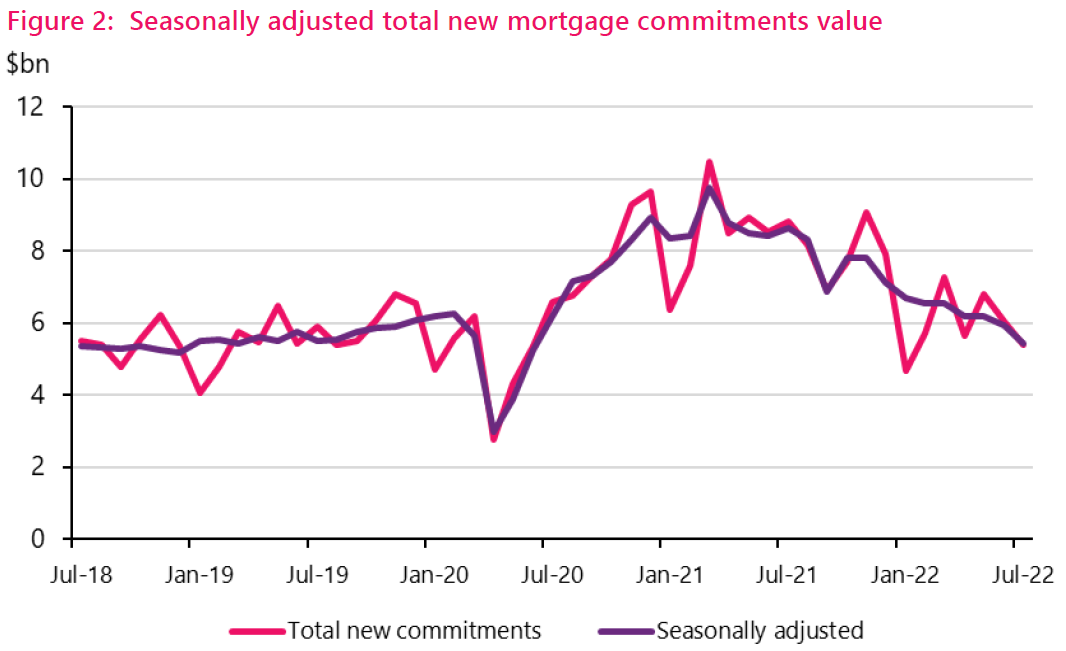

The $852 million advanced to investors in July made up just 15.8% of the $5.4 billion total mortgage money advanced.

This pales next to the figures of 30%+ that this grouping has enjoyed as a share of the mortgage money during housing booms, particularly in the period around the middle of 2016.

In June of 2016 - just before the RBNZ announced stricter lending limits for investors under the loan to value ratio (LVR) rules, this grouping took just under 35% of the total amount of mortgage money that month.

The investors had a big resurgence in 2020 after the RBNZ made the decision (effective May 1, 2020) to remove the LVR restrictions completely.

In December of 2020 - before the RBNZ's LVR limits were officially reinstated - the investors grabbed 25% of the nearly $10 billion advanced that month.

But it is not just a story of investors retreating to the sidelines - the total amount advanced during the month was down 8.5% on the previous month's tally after seasonal adjustment.

And compared with July last year, when the housing market was just starting to cool from melting point, the total amount of mortgage money advanced was down a whopping $3.4 billion.

The RBNZ says the average value of new mortgage commitments across all borrower types fell 6.4% from $405,029 in June to $379,061 in July. This is the largest monthly decrease since June 2020.

It also says there were just 14,251 new mortgage commitments this month, a decrease of 4.7% from last month, and a decrease of 46.4% since July 2021. This is the lowest number of commitments for a July month since data collection began.

First home buyers are still staying quite tough in the market, with just over $1 billion advanced to the FHB grouping in July.

As a share of the total, the FHB grouping saw its percentage increase slightly, from 18.3% in June to 18.9% in July.

73 Comments

Why are investors pulling away?

According to the spruikers you can’t lose with property as an investment.

Are more investors thinking it’s not such a good investment anymore?

or is it the availability and cost of credit?

or a bit of both?

Well if you are a speculator, where is the opportunity? It's not in capital growth. If there is one it will be to keep your cash ready to buy at the bottom.

Plus deliberate Govt. policy of pushing renters into corporate type BTRs for true long-term landlords, and better returns money in the bank.

If you can't lose they should all be piling in as houses are on sale at 20% off

yeah but the boxing day sale isnt too far off

Probably because they can't keep leveraging against the fake value in their existing properties when the market is falling

As far as I can see, the numbers aren't stacking up, rental yields at current pricing is terribad, and there's a wide range of legislation that making landlording fairly unappealing, particularly if the house is pre 1990 or so.

It'll be good in that the standard of rentals will be better overall in the medium term, downside is presumably these older uncompliant rentals will end up in the hands of FHBs and the cost of bringing some of them up to scratch is fairly significant.

I'm guessing many investors will migrate to intensive units being built in the major cities.

The yield on most of those intensive housing developments is pretty average, typically around 3.5-4% gross

Yeah but there's tax and maintenance benefits, and presumably intensification will lower prices and improve yields in some instances.

What's a 2 million dollar plus central Auckland rotbox rent for? 2 percent if you're lucky, can't deduct the finance, must upgrade insulation and heating, ongoing maintenance and upgrades of utilities etc etc.

Only potential upside is if you're sitting on dirt that might have its usage type changed.

I had a look at a couple of marina berths recently, returning an average of 8%. Pile in.

Time to give labour some credit perhaps?

Will certainly reverse if National got back in.

Yeah personally I think longer term things are looking more favourable, the problem is this is something that'll be a decade or more to play out.

No NZ government I can think of has nerfed landlording and property investment more than this one.

No NZ government I can think of has nerfed landlording and property investment more than this one.

Sadly, that's not setting the bar high.

I think a decade is about the right time frame. The recession will arrive 2 qtr next year and it will be a good-un.

People will not be too fussed about buying a new house when they are looking for a job.

In about 10 years time the natural circle will be in effect and the existential climate response will be the next infrastructure boom.

The Charge Of The Property Brigade (not by Tennyson)

Cannon to right of them,

Tax changes to left of them,

Rate rises in front of them

Volleyed and thundered;

Stormed at by ungrateful serfs

Boldly they rode and well,

Into the jaws of Debt,

Into the mouth of diminishing capital gains

Rode the six hundred.

"Never retreat!" yelled Ashley Church, mounted on his majestic white steed. Charging into the guns. "Onward and upward, noble ticket clippers! We will beat these serfs into submission yet".

When can their glory fade?

O the wild mortgages they made!

All the world wondered.

Honour the charge they made!

Honour the Ticket Clippers

Noble six hundred!

Well done that man!

Noice

Boomers are retiring and pulling their money out. It is really simple. The same demographic logic that caused the house building spree in the 70s is now causing the retreat of housing today. Too many boomers want too much money and want to pull it now. Millennials and Zoomers lack the money to buy them at these prices, given existing debt burdens and salaries.

This stuff is simple and boomers need to face the fact they won't be make 10x off their property investments, only 3-5x.

Good summary.

National will remedy that demographic change make no mistake about it. The very reason I remain conflicted as I prefer right wing politics.

Same happening in the labour market, which is exacerbating the labour shortages.

BB's in their early sixties retiring left and right at my work.

it's never really that simple, if it is then shoot the boomers and you would get problem solved, but would you?

investors, be that speculator or long term property investors, are all profit driven, and certainly won't go shopping when no profit out there. all of this is due the the financial market changes, and the general economic environment condition changes. with interest rate increases, interest deductability removed, and no prospect of capital gain, there isn't money in there anymore.

It's too early to comment on the government's policy toughing up on landlords. Rentals are always in demand, and there'll always be people renting, if you beat up the ma-n-pa landlords, the big corps will take over, and they will have a price setting power to rents. some examples are, some 40% rentals are controlled by a few corporates in some US states, which drive people out of affordable rentals into pricier ones.

there will be another issue on the rise, that's the over supply of townhouses and units in big cities. it won't end too well in my opinion, as many developers, investors will get burnt. however, it'll make houses with some land with it more valuable, for long term investors, there will be money to be made.

and last point, every one will get to a point to retire, boomers may seem to be rich, but reality is it's not enough, for most of them. You may be in that position too.

After I expressed the same sentiment yesterday. I was reliably told that

"you only lose if you sell". From someone who doesn't understand opportunity cost probably.

That's the denial phase. The same people were fully convinced that paper gains are real wealth on the way up.

Oh yeah, and the other one is that if property loses value it only matters if it's the banks money. If there is no mortgage, then your money, apparently, is a free good.

If you are forced to sell you loose a lot more.

Opening sentence:

The housing investors are in full retreat after their full-on assault of the housing market in the second half of 2020 and into 2021

Hardly a neutral statement.

Are you disagreeing with the statement of increase and decrease of activity by investors?

Or do you somehow feel this implies judgement of housing investors?

And presumably if you object to "assault", you object to "retreat"?

Wow, you like to complicate things. Note I highlighted in bold "full-on assault", which is very negative, actually assaulting is illegal and people go to jail for it. So yes, that's the word I think is over the top.

a concerted attempt to do something demanding.

"a winter assault on Mt Everest"

Here's a local example from just a few days ago : https://athletics.org.nz/andy-plots-latest-mountain-running-assault/ .

Dictionary

Assault

noun

- A concerted attempt to do something demanding: a winter assault on mount Everest

Here's a message from 2 weeks ago from a close friend who has over 300 tenants in the UK. Note the UK introduced the end of interest deduction from taxable income 2 years prior to NZ:

"It’s become a last man standing market here. Many landlords are exiting and selling up and thus causing a supply shortage. That’s because of the government’s decision to disallow deducting interest rates. So, the upward pressure on rents is enormous over here. Especially rents that include energy bills which of course every tenant wants. But the impact on young peoples budgets is severe. Many talk about having to cut out restaurant meals and holidays completely

A landlord who cares about the impact on young people?

I don't believe it.

I. Don't. Believe. It.

Just sounds like crocodile tears. "Boo hoo hoo, I have 300 tenants and need to raise rents so high that it causes them hardship. Poor, noble, overtaxed me."

this is not what we are seeing here as we are in the middle to end phase of building boom.

supply of unsold townhouses is ever increasing and a number of these have come off the market to be rented (reluctantly)

I believe we are going to see a supply glut that can only be filled with a massive increase in immigration.

IMO interest deductibility was always a stupid idea, pretty much a subsidy for landlords and helped force prices out of reach for a lot of would be owner occupiers.

If the business case doesnt stack up, then the price you are paying is too high! Plain and simple!

50+ new build townhouses in the Wellington region for sale. And of course, in many cases - only one or two of many in the complex might be advertised. Many listings more than 6 months old.

https://www.realestate.co.nz/residential/sale/wellington/townhouse?by=latest&nc=true

Your hate for landlords, Fitzy makes you miss the point. The topic of the article is "the retreat of the landlords" and my post above may give one reason for such retreat.

Hate for landlords + hesitation to buy = beyond help

Or, = instead, invested in productive businesse and continues to enjoy ROI of 100s or 1000s of percent, regardless of the tanking real estate market.

You sound a little bitter.

I always found comments like one from your friend a bit illogical.. If the investor landlord sells:

- Another investor landlord buys. Aggregate rental supply does not change, hence no impact on rents. Perhaps the new investor might even be able to enter at lower cost base, allowing their rental offer to be competitive and put downward pressure on rents.

- An occupier/FHB buys. Aggregate supply decreases, but so does aggregate demand. Perhaps a slight imbalance towards less supply due to smaller household size. But the new owner occupier can always get a flatmate for a few years, in which case the overall demand for housing is unchanged.

So where is the supply shortage coming from?? Immigration? Houses that magically disappear when a speculator sells?

The only thing I can think of is a temporary squeeze in supply when the house sits empty during the selling/settlement process.

Entirely correct.

I also think it's a bit of a stretch to assume that when a FHB purchases a house to live in that somehow half a person (as per the stats) is made homeless. So many people I know that are currently renting and waiting to buy their first home do not have flat mates. I also have a couple of acquaintances that took on flat mates after buying.

These prospective FHB are the "22 year old" home owners of the 70's and 80's. Good wage earners that have unfortunately been displaced from the market by our rentier culture.

It's like the opposite of what happens when investors roll into a regional town in NZ. First house prices go up, then rents go up, and more locals are complaining of inaccessibility of each.

One wonders how robust are these theories of landlords that regulators being mean to them are causing the problem. Common talking points, even here, but...

What is happening in the UK is a delayed response to George Osbournes tax changes on interest deductability (now copied in NZ). Result is landlords sell up to non landlords and there is a rental shortage & rents are very expensive. This is a fact. It is strange though when the local councils are then asking for landlords with houses to contact them to house people instead of them being in hotels.

Thank you Engineer for having the intelligence to understand the point of my post!

Could you please define what a 'non-landlord' is?

Bingo. Sounds like an occupier/FHB, and likely one less person renting. Eventually when there are no more market level occupier/FHB's, prices will have lower to meet the market for other investor landlords or occupier/FHB's.

Most First Home Buyers that i know were living at home with their parents before buying a house, they were never in the rental market at all. So while they take a rental property out of the market by buying it, they do not put another rental back into it. Consequently the pool of rental properties shrinks over time. Around 52% of people under 30 live at home with their parents, and cost of living/inflation is probably going to drive that number even higher.

Fallacy = anecdote & hasty generalisation

https://fallacyinlogic.com/anecdotal-fallacy-definition-and-examples/

https://fallacyinlogic.com/hasty-generalization-fallacy-definition-and-…

interesting topic.

in a general perspective, there'll always be the same house units, as building houses is rather long and complicated process, if landlords sells, it's either to another landlord, or to a home owner who lives in it. this is going to change the rental supply when :

- rental being vacant while selling. for nz it's about 7 weeks from listing to sale, not sure how much longer for settlement, probably another 4 weeks.

- rentals sold to a live-in home owner. because rentals usually houses more people than home owner situation, this is going to create "extra" rental demands. for example, if a rental houses 2 couples in it, when a couple buys that house, then the other couple have to move out and find another place to live in.

- capital is needed to maintain a stable numbers of house units, when capital is leaking out of the property market, this would lead to lower new build units, and when new builds is lower than units demolished, total number of houses will shrink.

Humm, do we actually know this? How many landlords select couples without children in preference to those with as tenants? How many people wait till they own their own home before having children?

Do we really want to look after Mr. Owns-10-houses and has made a lot of money in the last 5 yrs over FHB's and seriously argue that's moral due to reducing rental supply?????Obviously the more we get people into home ownership the less inequality is. Landlords with multiple properties are terrible for equality.

Fellow slum lord!!!

sounds like just your type

Lovely! Envy, bitterness and anger won't make you better off HM.

Yvil, this is interesting. There was a video posted here on this website about the Irish property crash 2007-2014, a few weeks ago. The price crash was severe - then, ironically, there was another shortage of rentals. I did not quite understand why, the video did not explain this. But what your UK friend is saying could be the reason.

In other words, ironically, at the end of the current property crash we could perhaps see another shortage of rentals. I wonder if it would simply be best to hang on now, instead of selling?

Yep I saw that video too, could happen in NZ ! I don't believe there will be a rental shortage in NZ as per "theglc" post above, he makes a good point. BTW I don't own any rental houses (except one for my mother-in-law who lives rent free)

So what happens to the homes that they are selling up?

Debt maxed out, decreasing tax rinse, unfriendly tenancy laws, no immigrants to exploit, and the cost of debt weighing on ones wallet. Who is surprised.

Yet TA is calling loudly for FHBers to jump in now to bail out the speculative.

Almost time to announce a low Dti....

Popcorn.

In a fair world TA would be off to the guillotine.

The TA and AC are asking all who can be easily deceived and money foolish to en-masse pile into the housing market now! "Dont wait" .........go gobble, gobble, gobble up them houses......our reputations as tidily dressed, well spoken rent slavers is on the line!

Save our expert market "Commentaters" weekly gigs, that we have reliably and regularly milked like a pregnant cow......as our well worn(out) "you cannot lose on property" "1001 reasons to just go and buy often and buynow" well and truly wears thin and wears out, as the drip drop of a property correction/crash plays out in real time.

Save us millionaires, poor downtrodden millionaires!!

Go on - don't leave these nice chaps out on a limb......with no desperate buyer to pay them over the odds, for their rental ratboxes.

No one talks about the DTI ratio being implemented... thats got the potential to keep things down longer once it settles.

A DTI would put a massive stop to the debt stacking landlords. Let's say it's a DTI of 6.

- Couple with $100k combined salary can borrow $600k.

- Landlord with $30k rental income can borrow $180k.

Assumes landlord has no other income than the rent on the property.

Fairly rare for a bank to solely lend based on the rental income of a property alone.

They're still subject to the DTI limits on the second rental.

- Primary Income $150k

- Rental Income $30k

- Mortgage on Home $500k

- Mortgage on first rental $580k

- $150k + $30k x 6 = $1080.

Get another rental at $30k per year, total income = $210k x 6 = $1.26m they can borrow. Less the $1080 they already owe = $180k.

That's one of many possible scenarios and configurations, sure.

The housing investors are in full retreat after their full-on assault of the housing market in the second half of 2020 and into 2021.

What about the “full on assault” by all those ‘lifestyle greedy upgraders’ who demand high prices for their existing homes from first home buyers and investors so they can upgrade to a better home?

Upgraders are the guilty culprits who borrow OVER 50% of all mortgages.

Never hear anyone complaining about them pushing up prices.

Well said. We bought our first home in 2017, sold it late 2021 to a FHB for nearly triple what we paid. It gave us a sizeable deposit which put us into our dream home with a very healthy equity buffer.

Looking back on it all, I really do feel remorse for holding a gun to their head.

I wonder about them sometimes also, but not from the 'greedy' perspective. There are more OO with larger debt-to-income ratios than either FHBs or investors, so I wonder how they got there: a large deposit from the sale of their previous house sans existing mortgage.

These people also are losing large amounts of equity as the value of their houses drop, and it would take a significant (but not unforeseeable) drop in house values to put them in negative equity.

But those interest increases on massive DTIs are gonna hurt.

Naivety is not restricted to just FHBs and specuvestors.

It's the targeted change in tax treatment for rental property. Everything else is just noise.

Good thing all those tenants have 20% deposits ready.

No it’s the capitulation of capital gains.

what is a seasonally adjusted month by month statistic?

The pull out method, timing is key.

I've been looking for news on young entrepreneurs with 50+ rentals. Are they doing well or has the tide turned. Can they bank on C Luxon to repeal the tax law?

The reason for this is simple: the numbers don’t stack up for investors at the moment.

Very poor yields, anti landlord labour tenancy and tax legislation, CCCFA limitations. Better to buy overseas.

Ask that great realestate sponsored independent economist

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.