Banks' non-performing loans collectively hit the $3 billion mark for the first time since October 2020 in August, but - perhaps surprisingly - household mortgage stress didn't worsen over the month.

Reserve Bank loans by asset quality figures for August show that total non-performing loans rose by $171 million (6%) in the month to 3.017 billion. The RBNZ said the non-performing loan (NPL) ratio reached its highest level since May-21 at 0.55%.

Yes, 0.55%. It is worth recording that the total loans in the banking system stood $551.368 billion. So it is a small percentage that's not performing - but rising nevertheless. (The highest percentage of system-wide non-performing loans recorded was 2.2% during 2011,)

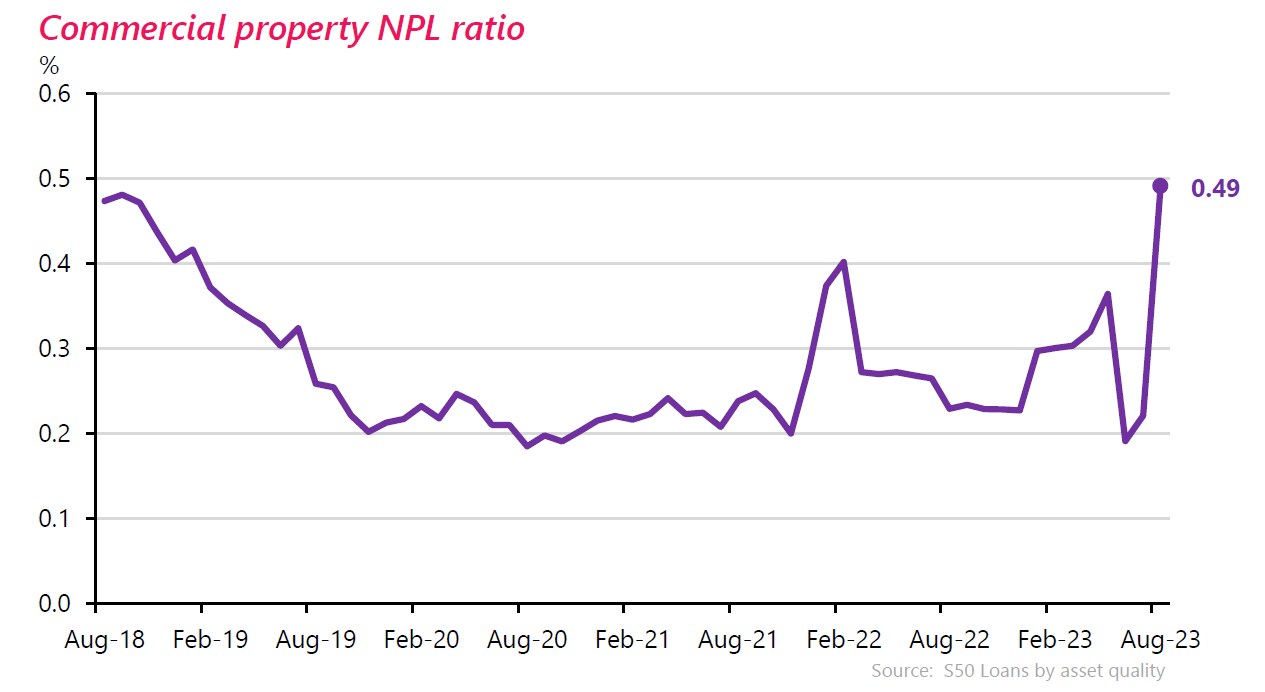

The big mover in terms of non-performing loans in August, was commercial property impairments. These rose by some $122 million, which pushed the commercial property sector's total non-performing loans up to $211 million and the NPL ratio up from 0.22% to 0.49%, levels last seen in 2018.

Total SME impairments rose $123m, which pushed its NPL ratio up to 0.73%, its highest level since June 2018. And agriculture non-performing loans rose by $26 million (3.3%) and have risen $131 million (18.8%) since the beginning of 2023.

The biggest portion of banking loans by a long way is made up by housing loans, which totalled $346.358 billion as at the end of August.

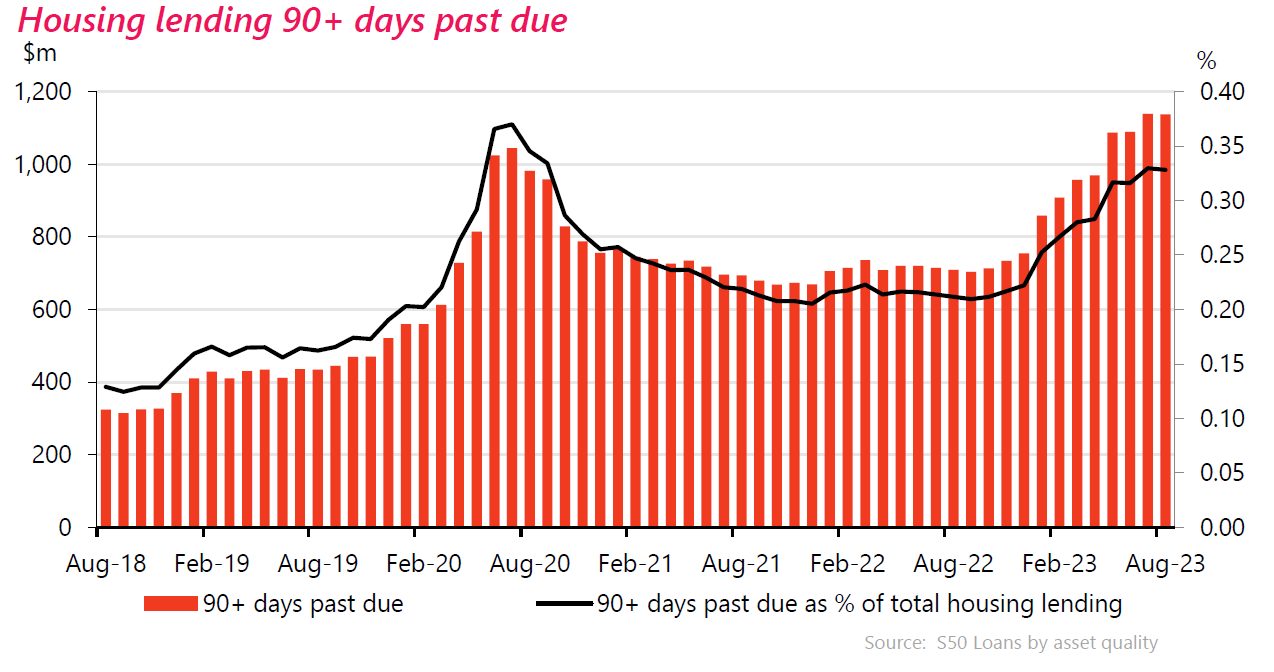

As we reported last month, the specific impairments on mortgages and the past 90 days due figures have been rising notably this year - albeit off a very low base.

Therefore it comes as a genuine surprise (to me at least) to see that there's been very little movement in the figures in the latest (August 2023) month.

Specific impaired housing loans rose to $188 million in August from $185 million the previous month. However, the 90 days due figure actually dropped for the first time since September 2022, falling to $1.137 billion from $1.139 billion. This meant the total of non-performing housing loans edged up to $1.325 billion from $1.324 billion.

In December 2022 the total of non-performing housing loans stood at just $850 million, so, it has been climbing quite markedly this year, although from very low levels.

But do the latest (August 2023) figures suggest we are now seeing a levelling off? It is dangerous to make any assessment based on just one month, but at this stage I certainly might have expected to see the figures keep going up month by month at a noticeable rate.

The ratio of non-performing housing loans to the total remains at a little under 0.4%. And while that's well up on the 0.2% seen less than a year ago, it is still a long way short of the kinds of levels seen after the Global Financial Crisis.

The ratio of non-performing loans at that time rose above 1% for a considerable period of time, hitting 1.2% during the period from 2009 to 2011.

So, at the moment, while with mortgage stress is higher than its been, is not particularly elevated by historical standards.

And yet this is despite the fact we've just moved rapidly from a period where mortgage rates were at historically low levels that encouraged people to take on historically large mortgages. For a while there it required a first home buyer in Auckland attempting to acquire an average sized house (average price at one point $1.3 million) and with a 20% deposit, to take out a million dollar mortgage. And people did.

In terms of popular fixed mortgage rates, in August 2021, according to RBNZ averages, the average one-year fixed rate was 2.49%, while the two year was 2.7%.

As of August 2023, the average one-year rate was 7.1% and the average two year 6.78%.

People have been facing 50%+ rises in the monthly mortgage servicing costs. And yet, for the most part they do seem to be managing. We do know that a lot of people were ahead of their mortgage payments. And a lot of people have been able to secured reasonable pay rises.

Is it possible then that mortgage stress levels won't get that much worse, or will we suddenly see a sharp move upward again in those non-performing loan numbers?

At the time interest rates started heading skywards in mid-2021 (a move which pre-empted the first RBNZ Official Cash Rate hike in October 2021), it was noted that the RBNZ would be able to get substantial 'bang for its buck' in terms of the impact higher rates would have on customers. This was simply because at the time a lot of people had gone 'short' in their fixed rate terms.

A perusal of the RBNZ's mortgage data on times to repricing shows that as of August 2021, owner-occupiers had a collective $203.427 billion of fixed mortgages. At that time $67.712 billion (33.2%) was due to refix within six months, while $141.855 billion - a very considerable 69.7% of the total - was due to refix in up to a year.

The situation now?

Well, a lot of people are still up for refixing, but proportionately quite a few fewer than two years ago. As of August 2023 owner-occupiers had $229.704 million of fixed mortgages. Of this, $66.204 billion (28.8%) was to be refixed within six months. Some $133.97 billion (58.3%) was to be refixed in up to a year.

So the numbers of those that face imminent repricing are still notable, but not AS notable as they were at the start of the rate rises two years ago.

And the other point worth referring to at this stage is what's happened to mortgage rates in that time. The one and two year fixed rates have tended to be the most popular over time, though we can now chart ups and downs in popularity with a new data series that the RBNZ is running on these. But anyway, looking at the two-year rate, if a buyer had taken up a mortgage on this in August 2021 they might, according to RBNZ averages have been paying 2.7%. So, had these people been re-fixing in August 2023, and they went for two years again, it would have definitely been smelling salts time, with the average rate according to the RBNZ being now 6.78%. Ouch.

However, those fixing for one year might have had a mortgage at around 2.49% in August 2021, but would have had to refix in August of last year - 4.91% - and now refix again this year in August at 7.1%.

I guess the point I'm making is that we are now gradually getting through that major 'pain threshold' that we saw when rates first really started to surge. The increases in mortgage rates, and therefore payments, from now will be progressively less onerous. But will the damage to finances be cumulative?

The question is whether people who have moved on to these higher rates had savings up their sleeves that buttressed themselves against the higher payments for a while at least - but maybe the buffers are gradually being used up? Or alternatively are people finding a way to cope better than perhaps the RBNZ might have thought.

The key thing now presumably is whether we see mortgage rates go much higher than they are and for just how long they do stay at or around current levels. Definitely worth keeping an eye on.

48 Comments

Well written and balanced article David.

Is it possible then that mortgage stress levels won't get that much worse, or will we suddenly see a sharp move upward again in those non-performing loan numbers?

Whilst I'm also surprised (like you David) that mortgage stress levels aren't bad at all now, I cannot see any reason why they won't be much worse in 12 months time. I think your paragraph about people having a buffer so far is valid, I also think this buffer is in the process of disappearing quickly.

My view is it will keep grinding higher.

Look at this chart for mortgage stress in Aus:

https://twitter.com/DFA_Analyst/status/1708457301449888232

This growth will be huge over the next 12 month as the greedy bank milk there customers dry so they can keep their greedy profits.

By pooing in their own nest I hope they take a serious bath on some deals but they can never really lose.

Maybe a dumb question but how well do measures like this capture people who aren't behind on their mortgage but who are severely stressed by their mortgage?

My wife was talking to one of the other mums from her antenatal group the other day, who is in this situation - her and her partner basically cannot afford anything else other than the most basic of food, power and commuting to work after paying the mortgage at their new, higher rates. They aren't behind 'per se' but everything else is behind (e.g. buying toddler clothes on Afterpay).

Played a round of golf over the weekend and the two guys I played with are in a similar situation; not technically in arrears on mortgage but very pressured with no wiggle room left.

Having a baby, although a beautiful event, is not going to help the cashflow :-(

You can say that again brother, as I found out the hard way (the couple I'm referring to have a toddler - the antenatal group still catches up every month or so).

Wouldn't change it for anything though ... as mushy and lame as it sounds having a kid has made me completely re-evaluate what is important in terms of work/life balance etc.

But very tough for those on tight household budgets.

That being said (and it's not my place to stick the oar in) this couple is bad with always wanting to buy the 'latest and greatest' for their toddler in terms of clothes, toys etc. Every time 'Jamie Kaye' - one of the more desirable kids clothing brands - drops a new release, they will have hundreds of dollars worth of gear on tick via Afterpay.

Although we would earn far more as a household we buy just about everything 2nd hand apart from safety-related equipment (car seat, cot and pram), as the little tyrant destroys clothes and toys like Godzilla tore up Tokyo. Weirdly enough they also grow like crazy!

Firstly, good on you for becoming a parent DT, the way you post, I think you 'll be a great dad/mum (trying not to gender assume). I also like the 2nd part of your comment, although there are external circumstances we cannot change (the higher interest rates), we do have some control over our own lives (the responsible spending). Successful people focus on what they can control !

Suggest buying jk on trademe, there’s a whole second market of basically new stuff marked down. Purely because people buy the “drop” and don’t use it. Kids wreck clothes. If they aren’t wrecking clothes they aren’t being kids. Patches holes and stitches, they don’t really care until they’re 10-12 so no point spending thousands on clothes they won’t wear. Always buy good shoes though, with plenty of support and space to grow, that’s the budget that won’t budge.

But yea kids are very expensive. One whole income expensive if you think about it. Best to start when you’re young and broke, then they’re cheaper, being mid 30s and having a massive income hit probably isn’t so much fun. Being 20 and being broke as all hell is pretty common regardless!

(speaking from experience so only half serious)

They definitely change you, especially the work life balance. Been quite the focal point for my financial decisions, providing a stable roof in a good area very close to schools. We could've leveraged quite comfortably into a rental property, something I may have done without a child, but that would sacrifice what we have now. Simply crossing the road and walking through a sports field to school is much better than "beating the traffic and finding somewhere to park".

We don't live frivolously, although our daughter now has the "latest and greatest", a Barbie Dream house, camper & holiday home. Since she was 5 we paid a generous $10 pw pocket money for chores. Tidying her room, collecting her washing, reading 1 book per night etc. She wanted a Dream House, showed her how much money she had ($350 at the time). Then it was on sale 25% off, she had about $300 in the bank so bought it with her money. Since then she accumulated enough to buy the camper, and just recently the vacation house.

You’re right that is generous, but no matter the number, it is good she is learning the value of money and delayed gratification at such a young age 🙂

"......delayed gratification at such a young age."

One of the secrets to success. Never buy depreciating assets with credit. Delay buying the new car....delay...delay. Then look and ask if you really need it.

Surprised one of the commentators' described friends under 'financial stress' whilst playing golf. Probably still have SKY, alcohol, takeaways and clothes bought from stores other than K-Mart or trademe. Irony, go figure.

Golf is free if you paid for a annual membership many moons ago.

(And find as many ball as you lose.)

It's pretty punishing alright. Baby paraphernalia, childcare costs, buying new clothes every few months as they grow etc. And that's just the cost side - time off work and reduced working hours mean income drops too.

For many it will be the most financially challenging period of their lives, and does get better/easier. Well that's what my wife and I tell each other anyway.

I’m seeing this with a significant amount of my friends, especially those with kids.

Pre 2022 everything looked easy, now the price of that debt isn’t looking so great and a sense of regret is taking hold.

These are high income owners living a Pak n Save lifestyle….

Which is how people should operate.

Instead, most people elevate their lifestyles in line with (or exceeding) their income. That's a good way to stay poor, but with nicer stuff.

My peers laugh when I turn up to a meeting in a 15 year old banger car, while they're rocking the latest Raptor or Euro. And then proceed to complain about how close to the wire they are at the moment financially. No kidding.

Wow so now only a 15 year old car is now a "Banger" ? I think everyone has moved up the scale without even realising it. Still did speak to someone the other day who's 5 year "Old" car obviously needs replacing now.

I upgraded from my 40+ year old banger to a newer model when petrol hit $2.50 a litre.

The 15 year old one wasn't flash even when it was new.

Smart move. I've only ever bought a new car once. All the others have been at least 7 years old and all have engines less than 1.3l.

(The new car? A kit set Caterham 7 paid for by a compulsory car allowance. Why a Caterham 7? Zero depreciation!)

Facebook marketplace is a goldmine currently. People leaving the country and selling off goods, clearing out elderly homes when they downsize, the list goes on. So much savings to be had so we can afford to spend our money on things we want and have a rainy day fund.

Ditto. And I get the funny looks parking the 2002 Honda next to the Audi and Tesla in the staff carpark. The laughs when I buy 2nd hand clothes and refuse to buy alcohol unless it's a family celebration.

It's nice however knowing that if interest rates go to 8, 9 or 10% I sleep well at night. Redundancy, who cares. Retirment next year has never smelt so good. Play the long game, have a plan.

You sound like me! Except for the bike...and now the wfh :).

Hedonic adaption is worth understanding.

When you understand the impact of compounding interest it changes your life. Not providing a description or reproducing the equation but being able to determine "if I forgo that trip to Fiji and pay $2000 off my mortgage, this is the financial gain in 25years." Continually blown away that supposedly smart people are make such poor financial decisions.

Delayed gratification is a spectrum I guess. Some refrain from spending on many things then decide to splash on others after a period of saving hard. This may or may not cost them over 20-30 years or so depending on their position financially. That's why it is so important to find joy in the small things. I love my 21yr old station wagon, as the wife and I can go away and throw a mattress in the back and some blankets for some weekends away, take some homebrew and enjoy nature.

That is what I call 'winning.' Good stuff!

In the same vein reading a book on your deck mid-week when every other bugger is working or running mid-morning along deserted bush paths. Nominal cost, immense mental and physical benefits

Enjoy nature

😉

"if I forgo that trip to Fiji and pay $2000 off my mortgage, this is the financial gain in 25years."

Except in 25 years, when you want to take your lady to Fiji, you can't go anymore because of the climate, and your willy doesn't work anymore and you can't even be arsed standing in the queue at the airport to fly out.

We actually agree on something, I have an 8 month old baby, while I drive something I enjoy, we don’t splurge and are generally pretty responsible.

As DT said, kids change you, for the better IMO.

You can enjoy things in moderation, just don’t live beyond your means, that includes buying a rot box for a million dollars.

I found some wiggle room..cut out the golf

What you say is typical of the early days of high interest periods. I.e. there is a well known cycle that plays out.

We are currently just over a year from when i-rates past the "recent normal" of about 4.5%. About this time (usually earlier), people's buffers have run out and short term consumer debt (cc's, pay later, loans from the boss, overdrafts, etc.) is rising. At this point, a small financial setback (e.g. the car needing a major repair, one client stops buying or goes bust, not meeting a sales target, sickness, injury, etc.) becomes a tipping point. While many will be able to ride it out, an increasing number won't. Then we see businesses failing, marriages failing, etc, etc. and the situation starts to snowball.

It's no different this time. The fact it's taking longer than normal is due to covid which allowed people to build bigger buffers (both through savings and absurdly low interest rates). Normal service will be resumed shortly.

The RBNZ could drop i-rates early next year and the damage would be minimised. Alas, they probably won't because inflation won't be under control by then. Why? Because the OCR is a useless weapon when those doing the spending (or setting prices) are largely unaffected by interest rates.

One thing we're going to see - and most will be surprised by - is banks maintaining healthy profits. Why? When banks come to the 'rescue' they increase loan terms to reduce repayments and/or give 'holidays' and/or allow interest only repayments. All of these 'rescues' result in the banks booking more interest revenue while maintaining the level of debt. Its good to be a bank in NZ.

Outstanding post Chris! IMO you have an excellent understanding of the situation were in.

I see stuff have put these figures into number of loans - currently 18000. With the estimate being that NZ currently holds 1.2M Mortgages- that means 1.5% of mortgages are in trouble - and this is before the unemployment rate starts to rise.

What happens when employers start laying off staff - construction, retail and the public service are all in a world of pain and you cant imagine it will be too much longer before companies need to cut heads in order to keep their head above water. The effect on mortgages could end up being ugly.

The same Stuff article had this quote from a mortgage broker.

“The number of request to switch to interest-only has increased exponentially. With most of these requests we have to complete a new application to ensure that they can still afford the lending that they have in place. My first appointment this morning was exactly this type of inquiry. There is also a large number of requests to move providers looking for a lower interest rate."

Don't worry. The National Party and ACT have a plan to keep everyone employed .... No. Wait ....

Sadly, you're right.

Once a few layoffs start the situation will snowball quickly. (Actually, they have started already in construction. Retail will follow after Christmas.)

Kiwis are as dumb as dirt.

Will only get worse with rising yields..

The Rentier Economy is a Free Lunch

You’ve had, for the last – really since the 1980s, but even since World War 1 – this movement to prevent industrial economies from being low cost. But the objective of finance capitalism, contrary to what’s taught in the textbooks, is to make economies high cost, to raise the cost every year.

That actually is the explicit policy of the Federal Reserve in the United States. Turn over the central planning to the banking system to essentially inflate the price of housing, with government guaranteed mortgages, up to the point where buying a home is federally guaranteed up to absorbing 43% of the borrower’s income.

Well, you take that 43%, you take the wage withholding for social security and healthcare, you take the taxes; the domestic market shrinks and shrinks. And the finance capital strategy is exactly what it is in the United States today, in Europe. Shift all of the money away from the profits of industrial capital that are reinvested in making new means of production. To expand capital into a shrinking economy where the financial sector intrudes more and more into the economy of production and consumption and shrinks the economy.

One wonders how many under performing commercial loans are being masked by new bridging loans? Particularly among property developers. The real question is how long must we kick the can and will it be too long to stop the balloon going up?

So, the Banks dodged a bullet ? And with rates stablising with a outlook for decrease, may be the Bank Owners can sleep better ? Not so the borrowers, who have to pay higher than before interest.

Banks have been able keep the mortgage stress under wraps by being proactive - and having falling property prices work in their favor. (Sounds odd, but bear with me.)

The banks contacted people in the most dire straights when a re-fix was coming and pointed out to them just how bad it would be. The people listened. And when they realised the bank was right and property prices were falling, the people were quick to agree with the banks that they should cut their loses and sell quickly. But now that both banks and other R.E. spruikers are saying the R.E. market has turned, people in the same position now want to hang in there for a better price. Thus the low rates of mortgage stress was a temporary thing.

Normal service will resume shortly. And with some vengence.

It's interesting the commercial property loan stress. I'll draw a long bow and reckons and say, lack of tenants, business failures or downsizing, potential job losses and finally mortgage stress, particularly if the business is backed by the house.

Might take a while.

Many residential property investors moved into investing in commercial property when LVR's were raised, and interest deductibility was being phased out. Some commercial property was purchased at rental yields of 5-6% or less.

Is anyone seeing more mortgagee sales in commercial property? Can anyone shed any observations into commercial property market?

Commercial/industrial is still fairly strong, despite those low yields. No distressed sellers, anyway.

No idea about retail/office though.

No idea . Full stop . Commercial values are tanking.

Though you can always get yourself a tame valuer to tell you something else 😊

Still being priced at 5 - 6%. Im picking a massive overshoot on warehousing as inventories drop. Im a small sample, but from March this year to March next, our goal is a 50% inventory reduction. From what my 3Pl is telling me we are not alone in this goal.

Retail is dying, Office space is a dead duck.

You can price at whatever you like . Pointless if not in tune with market and that isn’t 5-6% anymore.

Seismically compliant premium office space isn’t a dead duck. Far from it .

Painter - Check out commercial property defaults in La and SF were forced sales at 70-80% discount are common. One Roof and other property spruikers will claim its different in NZ - until it isn't in 2024!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.