Rising wholesale rates have driven rising fixed home loan rates. They have also brought higher term deposit (TD) rates as well. But mostly only for rates one year and longer. Rates shorter have remained very stable, and quite low.

As the table below shows, a number of banks now offer 4% or higher TD rates for two years and longer. In fact both ANZ and Westpac now offer some of the highest rates for those terms, and it is unusual to find main banks offering market-leading term deposit rates.

We are also seeing the return of finance companies offering even higher rates. They had stepped their offers back as they learned how the fees related to the Depositor Compensation Scheme (DCS) applied to them. And with some signs of improving loan demand, they find they need to offer more to attract the funds they require.

This could well mean that borrowers will be effectively paying for the DCS costs, unexpected because some, including us, thought those costs would likely fall on savers. The early 2026 evidence is that this isn't so.

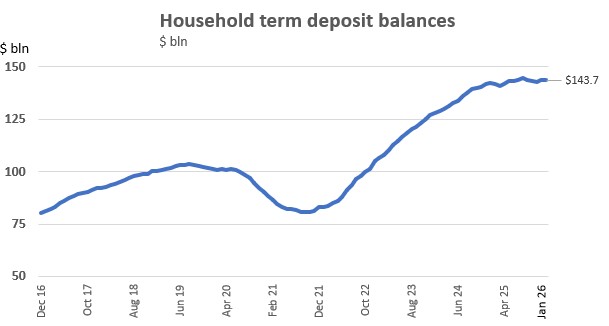

As we are in the middle of rate change activity by institutions, that is, some have moved already, others have yet to move, there remains an open question as to where this will all settle. We will be looking for a bank to adopt a 4% rate for 18 months - or even one year. Savers will start to be motivated by interest rates if, or when, that happens. Savers are reticent to park cash funds for terms longer than one year. Most is parked for less than one year, and with rates in that timeframe being quite low, and seeming to hold low, we have seen funds no longer moving into term deposits.

When you invest, always check how interest is compounded. Depending on how much you are committing, compounding more often is materially better. But some banks advertise their "interest at maturity" rates different to their compounding rates, which for some can be set a little lower. Both Kiwibank and Rabobank do this, although most other main banks don't.

Use the calculator at the foot of this article to see the differences.

We should also point out that after-tax returns can be enhanced for some savers with higher tax rates by the choice of PIE structures. Not all institutions offer these, but most of the main banks do.

Always ask a bank for a better rate. Many bank staff have discretion to offer more than the advertised rate. (And check your bank's app offers as they too are often enhanced to retain you). We have been surprised to hear recently of even big banks agreeing to a small boost, when asked.

Use the term deposit calculator here, or the one below the table, to calculate your expected net after-tax returns.

The latest headline term deposit rate offers are in this table after the recent changes over the past three weeks. The yellow colour code is for those under 4% and has spread comprehensively. Bolded rates are the "best-bank", the highest carded rate from any bank at this time. The blue-coded rates are those under 3%.

This table only lists institutions covered by the Depositor Compensation Scheme.

| for a $25,000 deposit March 19, 2026 |

Rating | 3/4 mths |

5/6/7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 3.10 | 3.45 | 3.40 | 3.70 | 3.80 | 4.10 | 4.40 |

| AA- | 3.00 | 3.45 | 3.55 | 3.50 | 3.65 | 4.00 | 4.15 | |

| AA- | 3.00 | 3.45 | 3.45 | 3.60 | 3.65 | 4.00 | 4.10 | |

| A | 3.10 | 3.55 | 3.40 | 3.55 | 4.00 | 4.10 | ||

| AA- | 3.00 | 3.45 | 3.50 | 3.75 | 3.80 | 4.10 | 4.40 | |

| Kiwi Bonds. 'risk-free' | AA+ | 2.25 | 2.50 | 3.00 | ||||

| Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs | |

| Other banks | ||||||||

| Bank of Baroda | BBB- | 3.35 | 3.65 | 3.60 | 3.60 | 3.60 | 3.65 | 3.85 |

| Bank of China | A | 3.30 | 3.60 | 3.50 | 3.70 | 3.80 | 3.90 | 4.00 |

| Bank of India | BBB- | 3.25 | 3.70 | 3.70 | 3.70 | 3.80 | 3.85 | 3.85 |

| China Constr. Bank | A | 2.70 | 3.20 | 3.20 | 3.20 | 3.25 | 3.25 | 3.45 |

| Co-operative Bank | BBB+ | 2.90 | 3.45 | 3.50 | 3.60 | 3.65 | 3.90 | 4.10 |

| Heartland Bank | BBB | 3.00 | 3.45 | 3.70 | 3.60 | 3.85 | 4.00 | 4.15 |

| ICBC | A | 3.25 | 3.60 | 3.50 | 3.65 | 3.70 | 3.75 | 4.00 |

| A | 3.05 | 3.50 | 3.45 | 3.60 | 3.65 | 3.85 | 4.10 | |

| BBB | 3.00 | 3.45 | 3.55 | 3.55 | 3.75 | 4.00 | 4.15 | |

| BBB+ | 3.00 | 3.45 | 3.50 | 3.55 | 3.60 | 3.85 | 4.00 | |

| Non-Bank Deposit Takers | Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Community institutions with DCS protection | ||||||||

| First Credit Union | BB | 3.40 | 3.80 | 3.80 | 3.80 | 3.70 | 3.70 | |

| Heretaunga Bldg Society | 3.05 | 3.55 | 3.75 | 4.15 | ||||

| Nelson Building Society | BB+ | 2.75 | 3.40 | 3.50 | 3.55 | 3.80 | 4.00 | 4.15 |

| Police Credit Union | BB+ | 3.00 | 3.45 | 3.45 | 3.50 | 3.55 | 3.65 | |

| UnityMoney | BB | 3.00 | 3.45 | 3.40 | 3.35 | 3.50 | 3.55 | 3.55 |

| Wairarapa Bldg Society | BB+ | 3.10 | 3.45 | 3.45 | 3.75 | 3.75 | 3.85 | |

| Finance companies with DCS protection | ||||||||

| Christian Savings | BB+ | 3.00 | 3.50 | 3.55 | 3.60 | 3.75 | 4.10 | 4.15 |

| Finance Direct | 4.10 | 4.25 | 4.35 | 4.50 | 4.60 | |||

| General Finance | BB | 3.40 | 3.65 | 3.85 | 4.15 | 4.35 | 4.45 | 4.65 |

| Gold Band Finance | BB- | 2.75 | 2.75 | 4.10 | 4.30 | 4.40 | 4.60 | |

| Liberty Financial | BBB | 3.10 | 3.80 | 3.80 | 4.00 | 4.10 | 4.20 | 4.30 |

| Mutual Credit Finance | B+ | 4.15 | 4.25 | 4.35 | 4.50 | |||

| Welcome | 4.00 | 4.00 | 4.05 | 4.15 | 4.25 | 4.30 | ||

| Xceda Finance | B+ | 3.70 | 3.90 | 4.10 | 4.30 | 4.40 | 4.45 | |

Term deposit rates

Select chart tabs

Daily swap rates

Select chart tabs

Term deposit calculator

6 Comments

Thanks for writing an article on this area. I find the 'marketing' and 'psychology ' of this area fascinating!

Interesting that Australian banks have quite a different TD/term profile eg 3/6 months at 4.25%pa while 3/4/5 years are at 3.5%. Perhaps reflects the 90+% plus of mges on floating instead of fixed?

Not me (to David's question: will savers jump back in?).

The difference between 6 month TD and 2 yr term deposit is about 0.5%-0.6%.

So, on a $10k TD that's a difference of about $50-$60 minus tax, for the privilege of having your money locked away 4 times as long.

Just ain't happening ...

Interest dot co has a useful article from a few years ago about term deposits based on RBNZ data [https://www.interest.co.nz/personal-finance/125824/new-reserve-bank-dat…] to get a sense of the size of term deposits.

The RBNZ S40 (“Banks: Liabilities – Deposits by sector”) table is publicly available, and if you use R, there is also a package that wraps it [https://www.rbnz.govt.nz/statistics/series/registered-banks/banks-liabi…]

Without delving into the latest data, the average household term‑deposit balance in New Zealand is about NZD 89,000, but this will be massively skewed.

Yup, and I'd say the same thing at $100k.

Would I lock $100k away for 2 years to earn $500-$600 more compared to only 6 months.

As Bro Town said: "Not even-au"

We're on the same page

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.