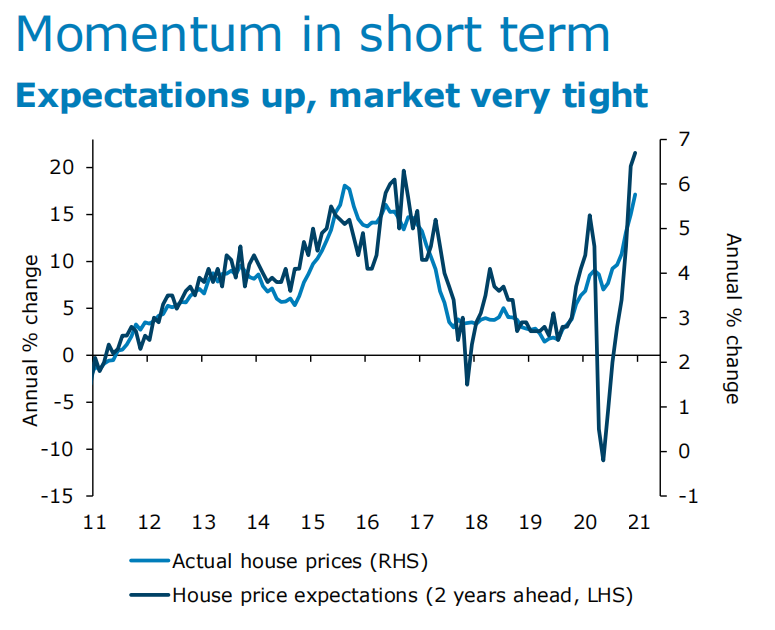

The New Zealand housing market has experienced a "perfect storm" and "unprecedented" price gains, according to ANZ economists. They say the market will cool "in time".

In the bank's latest Property Focus publication, ANZ senior economist Liz Kendall, senior strategist David Croy and chief economist Sharon Zollner say the perfect storm we've seen in the housing market has combined: A fear of missing out (FOMO), scarcity of properties and expectations that house prices will get further out of reach - all at a time when interest rates have been falling and bank funding has been readily available.

"This dynamic is expected to contribute to further price gains in the short term at least. We expect the housing market will cool in time, but exactly when is highly uncertain, given that momentum in the market can be slow to moderate, she says.

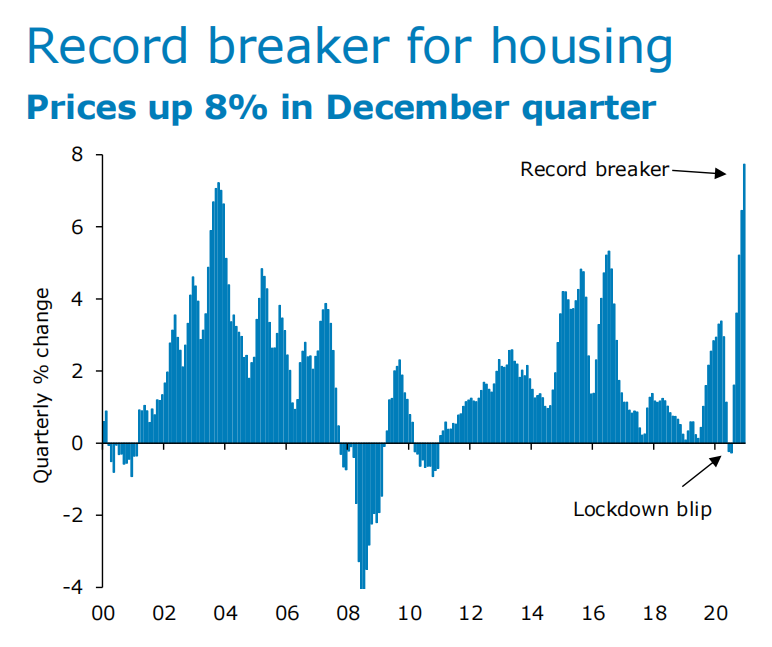

Strength in the housing market through the second half of 2020 was "unprecedented", the economists say, with prices rising 16% since May.

"Increases like that are unsustainable in the context of incomes that have been stable at best."

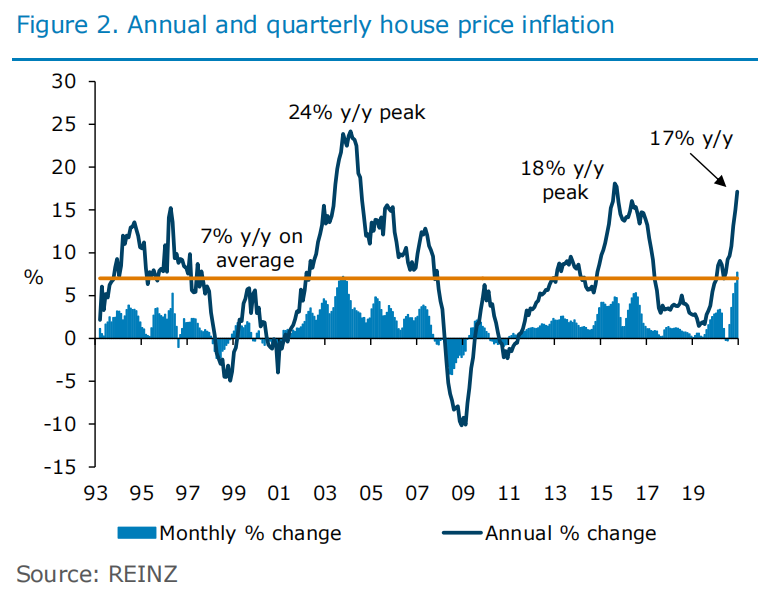

Annual house price inflation is still below the peak seen in February 2004 (24% y/y), which followed a year of solid monthly gains (1.8% m/m on average), the economists say.

"The upturn this time has been shorter but sharper, with price rises of 2.1% m/m on average since May.

"It is possible that continued momentum could see the 2004 peak in annual house price inflation surpassed.

"But there are reasons to think that the upturn might not have the same persistence this time around. A key difference is that the economy was very buoyant in the early 2000s, with incomes growing strongly. This time income growth is fairly stagnant and house prices are already very unaffordable relative to incomes – making continued house price inflation at the current pace unsustainable."

Kendall, Croy and Zollner note that reports of rampant house price inflation "have inflamed FOMO" in a tight, supply-constrained market.

And they say while some heat will come out of the market at some stage "in the meantime, New Zealand’s issues with acute housing unaffordability continue to worsen".

"To reverse the tide, big, bold action is needed urgently."

Eventually, the ANZ economists say they expects that an easing in acute market tightness will occur and fundamental factors will return to the fore, including income considerations, weak population growth (with building strong), affordability limits and credit constraints

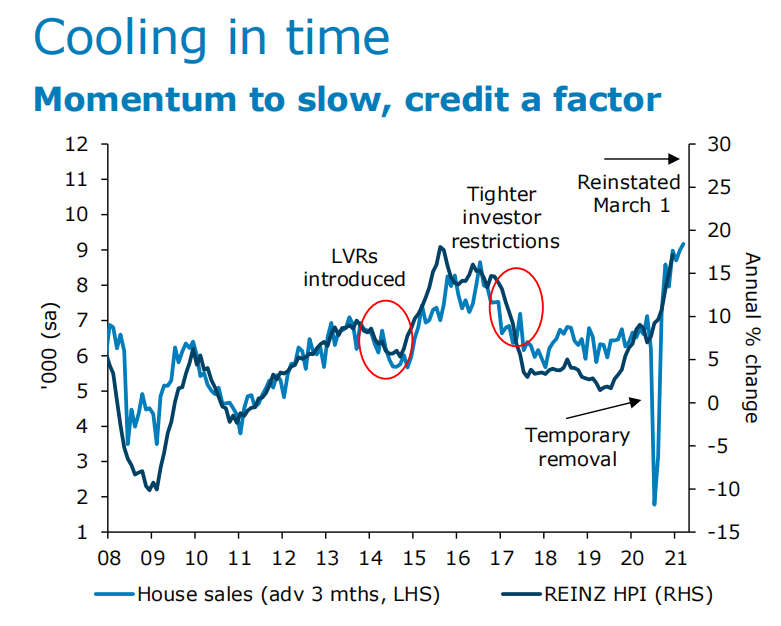

The Reserve Bank has moved to curb high loan-to-value ratio lending to investors, effective from 1 March, they note, with some banks acting pre-emptively to rein in lending to this segment.

"This will have some effect in dampening house price inflation (say 1-2 percentage points, according to the RBNZ), though only temporarily, as with previous imposition of such restrictions. Nonetheless, these may play a role in curbing (in the RBNZ’s words) 'irrational exuberance', thereby contributing to a slowing in momentum."

"Overall, we expect house price inflation to moderate, with solid gains in the next few months, followed by a more marked cooling," the economists say.

"House price declines can’t be ruled out, but for now that is not our expectation and sits squarely in the ‘risks’ basket."

ANZ is currently forecasting house price growth of 3.5% for the March 2021 quarter, followed by gains of 2% in June, and 1% in the September quarter. The next three quarters after that (up to June 2022) are also each forecast as 1% rises.

What this would mean for annual house price inflation, according to ANZ, is that it would be 15.3% at the end of March, rising to 17.8% by the end of June this year, but then falling to 7.7% by the end of the year and 4.1% by the middle of 2022.

118 Comments

Political parties in opposition ALWAYS criticize the one in office that house price being unaffordable, immigration level being high, rivers being dirty, productivity being low.

But interestingly, once the opposition ones sit in the office, they will suddenly mute on all these issues and do nothing to improve.

haha .

I find it not only interesting but extremely disappointed to this political system.

Welcome to a democracy my friend.

Ironically, nobody seems to exercise their democratic right to criticise the government than this mouthpiece for the CCP!

More precisely. Welcome to the world of populist politics.

Highlights the sad fact that people love power, and when they get power they don't want to lose it.

They're just keeping their powder dry...forever

So the better alternative to 'this system' in your opinion is there be no political parties in opposition to criticise the one in office?

Go back to China if you don't like our country and democracy.

Problem solved!

Fritz , go back to your boring life , there was no need for such racist comment you old fool

Ha ha nice one !

Bit shocking seeing such comment. But what’s really funny is that about over half commenters on here are Asians...

I see your new here. You will learn that old Xing is a CCP mouth piece that does nothing but shill CCP propaganda. So when it comes to Xing, Fritz's comment is actually justifiable lol

What is forcing you to stay here?

But Cindy’s Sandringham house price has risen more than her govt salary. Socialists turn to Capitalists pretty quickly when they finally have capital.

The housing bubble is making a great many New Zealanders feel 'wealthy' and supporting spending. In a real way housing is now our economy, the consequences of a fall in real (inflation adjusted) terms for any duration would be devastating for homeowners. Consequently I do not expect to see much easing, in fact I wouldn't be suprised if RBNZ intervene again to make sure that scenario doesn't play out.

Totally agree with your sentiments. The housing bubble is way too big for any government to let it burst. NZ in general and NZ businesses just wouldn't be able to cope with a material drop in prices.

Yes, it's not going to be allowed to fall. All the spin off industries, including tradies, etc etc would be out of work. Until Tourism can get back up to speed, they'll let the property economy run hot and take up the slack.

The two things I can see changing housing would either be an increase in productivity measures (which would raise wages/CPI/interest rates) or extreme liberalisation of housebuilding (think of Houston, Texas.) However I consider these probabilities moonshots in the current political environment.

In addition to RBNZ support New Zealand could feasibly reopen its borders in the second half of this year (Vaccine delivery due in Q3, as the Israelis are showing if you hit the ground running it doesn't take long) which may well offer a nice little tailwind to house prices.

For anyone who thinks that the NZ government have ultimate control over the housing market, and not international interest rates - I have a lovely set of robes to sell you, finest fabric, latest fashion, invisible to idiots who can't see how wonderful our government is. If you know what's going to happen as a result of QE/MMT to those aforementioned rates, I've got a whole wardrobe to sell you.

MMT is a description of how our monetary system operates and it has nothing to do with any policy choices that our politicians make. If you wish to blame anything then blame neo-liberalism as that promotes the creation of money by the banks over that of the government and in fact it promotes governments to run surpluses which can be very damaging for the private sector.

QE is just an asset swap, bonds are exchanged for bank reserves and it makes no difference to the ability of the banks to lend. The Bank Of England explains here how the banks create money. https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

QE - printers go brrrrrrrrrrr

QE is just an asset swap, bonds are exchanged for bank reserves and it makes no difference to the ability of the banks to lend

Yes it does because it impacts the feeling of security.

Who's feelings of security are you referring to? it doesn't make me feel any more secure and it would make no difference to the banks as it doesn't change their liquidity. Reserves and bonds both rank equally as primary liquid assets.

OK. Let me ask you a question. What is the objective of quantitative easing if it is not to enable greater money supply?

If I swap my 2.1 million dollars for your 1995 plaster rendered, kiln dried timber leaky building then that's just a simple asset swap too. If I was the central bank then that's kind of how it works. Good collateral is swapped for garbage assets, and bad decisions are wiped away. The original asset owners are made whole again, and they can play the roulette wheel of speculation again and again.

Yeah.

As someone said the other day, many small business owners need to borrow against their homes.

It shows how dependent our ponzi economy has become on housing.

Totally. The problem with every other housing bubble in the world, ever, is that their governments just let them burst. What they should have done is just not let them burst. Good thing we're smarter than that.

"The housing bubble is making a great many New Zealanders feel 'wealthy'..."

Which is illogical (unless you happen to be a slumlorder with multiple houses who cashes in) - collectively we cant all win

The extra "wealth" just buys exactly the same house in the new market

The real story is that all wealth = DEBT

We are just indebting our future selves

Which reflects no real growth and a need to up the leverage until it breaks

Plenty of New Zealanders feeling wealthy with their newly purchased SUV's & boats from borrowing against the house.

Its not illogical. Mortgage interest rates have dropped from 4.5% to 2.5%. That is a lot of extra money in people's pockets as they refinance their mortgages, which makes them feel flush, and they will go out and borrow to buy a new car or a boat because they can afford the loan repayments, or will spend it on discretionary items like furniture, house renovations, or holidays. Others will decide they can now afford to buy a bigger and better house as the larger mortgage will still be the same repayments as what they were paying a couple of years ago, so they will trade up to a nicer house in a better suburb and feel wealthier as a result. Yet others will take the equity in their current home that's accrued over the last few years, and go buy an investment property since the extra cashflow now means they meet servicing requirements. The fact is that nobody is just swapping house for house in the same market, they are awash in cash and are using that cash in different ways.

The government could have done much the same thing using fiscal policy and it wouldn't have inflated house prices, but neo-liberal economics has dominance in this country and it all flows from our treasury department, all ex bank economists no doubt.

Yes, we could have the same house and the same feeling for half the debt, if only they implemented the right policies.

And housing is the way plenty of Kiwis are "saving" for retirement. If not for property, at 65 there'd probably still be many years of work ahead of them.

Yeah, and too bad about those you've leeched off for your retirement, they can go sleep under a bridge in their dotage

Well no, if the official cash rate were at say 10% then a) house prices would be much more affordable/not a viable way to save for retirement and b) term deposits should generate a sufficient income stream for retirees.

The difference is a) whose money is involved and b) leverage.

In a new world of market intervention there is no such word as unsustainable.

All depends on whose eyes you're looking through. For ex, the ruling elite and general population think 'free money' can solve these issues, but when they see what's happening with a 'sound money' such as Bitcoin, they think differently.

dp

In Canterbury, the housing market appears to be very active with buoyant auctions and listings selling very quickly across the region, builders are very busy and with reports of there being shortages of available land. Speculators appear to very active a recent story doing the rounds sights the case of a Christchurch city residential housing development in an average location. Builders were selling houses off the plans, these were snapped up by speculators, some buying 8-10 houses with an expectation of reselling them upon completion for a profit $80k - $100k each, mind boggling considering the developers and building already will have a margin in the deal. Whilst they have yet to realise this profit it clearly indicates a very high level of confidence in the market. Just where the buyers are coming from begs a question or is this just a flash in the pan.

Is the location referred to Phillipstown?

Bromley, or Linwood, I think

So many indications of a very broken market.

I'm still not sure where all these people are coming from to buy all these built houses either. Auckland refugees maybe?

From what I've seen its first time investors from outside of Christchurch, who believe that Christchurch's affordability is simply an aberration and that prices are about to sky rocket and catch up with the prices in Wellington and Auckland. They don't realise that there is no shortage of housing, that building is going on not just in Christchurch but in Selwyn and Waimak, and without any population growth there will soon be a major over supply of rental housing. Fletchers is sitting on dozens of unsold properties in the city, locals don't want to buy them, so off the plan buyers will need to find some other Auckland mug to take them off their hands once they are built. The good news for local people is that they finally are getting the opportunity to offload a ton of badly repaired earthquake damaged homes to buyers who know nothing about earthquake damage, and arent even bothering to get building inspections done LOL.

A bit like leaky homes in Auckland then.

Auckland uni economist Susan St John said on RNZ recently that research shows more than 90% of investors in rental property are either making very little or incurring losses on an ongoing basis.

Jooolz... maybe on a cashflow month to month basis but who cares about paying a few dollars a month to bridge the shortfall when the average house is increasing over $300 a day, tax free.

And with every $300 day of tax free capital gain, I'm sure the pool of buyers is shrinking at pace.

Again, likely a load of crock. It all depends on whether you calculate the yield for a particular property based on the assets present value - or whether you calculate it based on the assets original purchase price.

True, but the yield is worked out on market value, just like capital gain is worked out on the gain, not what you paid for it.

What you need to really look at is the cash on cash or an annualized rate of return over time, after-tax.

Also what it doesn't show (which I'm no way saying is any justification if they are crying poor me) is they could have withdrawn cash or loaded up the property with 'other debt,' to buy another property, for a holiday, our using as cross security for a business or the bank of Mum and Dad.

Yes I believe the buyers referred to above are from outside CHCH.

Sounds like 2006. Wonder what happened next?

Well things took a slightly bad turn, the RBNZ jumped in and dropped the OCR from 8.75% to 2.5% and voila things took off again.

So basically the same as what just happened in 2020.

"the consequences of a fall in real (inflation adjusted) terms for any duration would be devastating for homeowners"

So i'm wondering homeowners or investors or speculators? I would have thought homeowners could ride it out, cause they are living in their home. Does the 35% of non home owners have to suffer longer because of the irrational behavior or greed of the investors or speculators?

Well we can clearly now see where Labour has nailed it's colours.

1 They will totally underwrite the gains of property speculators unlike those who invest in the productive economy to create employment and real wealth for the whole country.

2 They will sacrifice the hopes and dreams of young families to protect property speculators.

3 They will force tax payers to underwrite speculative property gains by subsidizing families, so that they can pay the rents that are a consequence of these totally outrageous house prices.

4 They will undermine our productive economy because housing costs must ultimately be paid for by employers through wages, taxes and commercial rents. I.e. huge amounts of money are bleeding out of the productive economy into the pockets of property speculators.

5 They prefer to largely hide behind the Reserve Bank and it's very limited range of options to stimulate the so called depressed economy, (is it really? where are the measurements that support this?) rather than take direct responsibility and instigate meaningful initiatives that will add to and improve the economy. (subsidies to private green schools and the various make work schemes don't come close to doing this.) The net effect is that the RB's lowering of interest rates is forcing billions of dollars into the property market, enriching and encouraging property speculators to make housing even less affordable. Labour seem passive and content in the face of this.

Labour are no better if not worse than the John Key Government. The thing that they have in common is an extremely charismatic leader who says one thing and does completely the opposite.

I would say they are worse. At least Key didn't pretend that he was the saviour of the downtrodden.

It is hard to see her sickly sweet ambulance chasing as anything more than a cynical act to try and mask their true behavior.

It would be hard for me to have any more contempt for her hypocrisy.

God they are funny.

It's a wonder they didn't use the term, 'Black Swan event.'

'the housing market has combined:

Fear of missing out (FOMO), - Didn't see that coming

scarcity of properties - Didn't see that coming

expectations that house prices will get further out of reach - Didn't see that coming

all at a time when interest rates have been falling and bank funding has been readily available - Didn't see that coming.'

Plus Removal of LVR's - Didn't see that coming.

Oh' we are on track for another record profit - .........

It's a wonder they didn't use the term, 'Black Swan event.'

The observation below might as well be that, when the masses eventually hit the streets with pitchforks in-hand, since banks are not about to stop excessive residential property lending to the already wealthy minority.

This time income growth is fairly stagnant and house prices are already very unaffordable relative to incomes – making continued house price inflation at the current pace unsustainable."

I like their line, "To reverse the tide, big, bold action is needed urgently."

And of course they, the banks and the Government, all know that any such urgent, big, bold action won't happen.

#rentcontrolnow

I've got my pitch fork ready - just need to finish collecting the data :-).

Isn't funny how they seem so concerned when they are a huge part of the problem.

Don't know how they can look themselves in the mirror each morning

You would be better off lobbying for the Labour Govt to adopt the "Christchurch Model" as per the National Party policy. Go on Facebook buy sell groups in Christchurch and they literally laugh at anyone posting a for rent ad for a property that is $450--$550 a week, and call the advertiser out for trying to rip off people. Not that the advertiser is ripping anyone off, as for that price the house is usually an immaculate 3-4 bedroom home in a decile 9/10 school area.

I just don't see where/how one can compare the Canterbury geography with its flat land for miles, with a place like Wellington. Some have suggested, for example, opening up intensive residential development in Ohariu/Makara but without the road widening and tunneling needs (even before thinking about reticulated services) I suspect, would make that unrealistic. Engineering build costs on our hills is so very different to CHCH - and existing underground services are a mess in the city and suburbs, as it is.

Maybe NZ should move its capital from Wellington? Surely there is a more suitable location? As a Cantabrian I would be willing to sacrifice Christchurch for this duty... (said with tongue-in-cheek).

Hamilton or Palmerston North would be better options from a geographic and demographic perspective, and from a resilience point of view.

It's easy to weigh the various variables that make up the value of a property.

As an example, two identical sections, flat, with no views are $100,000 each. And then you changed one of the variables to steep hillside, then the cost of the extra earthworks might devalue that section by $30,000, but if steepness also meant it had a sea view then that variable might be worth $80,000, so the new price for that section would be $100,000 - $30,000 + $80,000 = $150,000.

Of course, there are dozens of variables that you can factor in. But the basic variable under right, and the first input, is the availability of supply for the land. The original price of the land might only be $100,000 in a balanced market where supply equals demand but might have to be put into the starting equation at $200,000 if supply is constrained.

The variables themselves have different supply and demand contraints, sea views, close to a certain amenity many people find desirable etc.

And there are two main constraints, 1) geography and 2) Regulatory. It's the regulatory constraints that add the most cost by far, and most of them could be removed without lessening the amenity value of the property.

And if you think Cantebury land can be easily developed, even when flat, some TC3 land in Christchurch can have up to $140,000 of land remedial cost just to get to 'good ground' to start foundations.

I think people desperately need to take a chill-pill and stop watching the 'news' and listening to shock jocks.

Jacinda this, Orr that, Megan Woods is, Grant thinks.. Before commenting on this post, walk round your neighborhood for 45mins.. yes you can listen to music, but try to say hello to a couple of people.

Try deleting Facebook and YouTube off your phone for a few days. These house price increases are causing people anxiety, short of giving spiritual council; single-mindedness might help - stop adding news and social media garbage to your mind every time you're bored and see your phone.

interest.co.nz is innocuous enough, but I can tell commenters are getting too caught up and it's clouding reality [probably having been revved-up by other outlets first]. The internet is a place you visit, then your back to the material realm - spend some time in the material realm!

Social Media and News addiction is a huge problem and an adult conversation about it is near impossible because ALMOST EVERYBODY is addicted. The world is in a collective fever dream of sorts. To be fair comments on this article have been pretty down-to-earth.

That is a really good comment. I’ve found myself reading WAY too much news this year. Also I think it’s time for us to get off fb once and for all. So creepy and voyeuristic, so addictive plus there is the censorship issue. What are some tips for avoiding news when you’re on smartphone all day for work purposes?

Turn off notifications. Uninstall the Apps.

ZachB and Bill Evans.. not sure what you can do if you have to work but personally I haven't had a phone or even worn a watch for 3 years now. Pure bliss. For many, social media (and some MSM for that matter) is just a new age type of porn addiction.

Check out The Social Dilemma on Netflix need you have any more reason to ditch social media. The algorithms they use to keep people scrolling are disturbing, yet extremely effective, very addictive.

Theoracle... forced the Mrs and kids to watch Social Dilemma. Within a minute of the credits rolling they all had their noses in their devices again and didn.t move for the next several hours. I admitted defeat with only one act of resistance. I moved my 15 year old sons expensive gaming computer (which I stupidly bought for him) from the rumpus room to the lounge table. At least now he is forced to participate in some kind of social, family interaction, even if most of it consists of grunts, moans and the standard "be quiet, I'm concentrating".

I know its early - but this is comment of the year! So true Zack, so very true.

If there is one thing worse than a housing bubble its a media and social media hype bubble.

Yes and no. Deconstructing and unravelling propaganda like the ANZ media release is a public service. The govt isn't going to do it for you and interest dot co needs to maintain independence.

Property investments in NZ are both risk and tax free with a annual compound growth of the averages at 8% for the last 20 years! To put that in perspective, $1,000 invested in property 20 years ago is worth $4,661 today and that's not including rental yields! Where in the world would anyone find such a great investment but NZ? There's literally no downsides, no volatility and it's tax free. Now couple that with limited supply and valuation increases surpassing interest payments- it's really raining buckets of Gold!

It's really not too hard to become a millionaire. Forget the bears and whinners, they are poor for a reason.

I would add to that the NZ$ has also appreciated against most of the majors over this period. NZ is now a relatively wealthy country and your average Kiwi could sell up here and move to many international cities. This was a fantasy 30 years ago.

Meh. NZD is being severely debased. Its primary use is for the exchange of goods and services in NZ Its relative position in forex markets can turn on a dime.

I give your comment 1 out of 10.

I give your comment 1 out of 10.

Trolling is irrelevant.

Even my daughter stopped using "meh" about a year ago. Yes the NZ$ has been debased, but clearly other currencies have been debased even further - otherwise the NZ$ would not have strengthened against them.

So your comment had zero merit and the 1 was because I'm feeling generous. Less of the flakery and whataboutery,

Meh. NZD has appreciated relative to the USD in lockstep with AUD. JPY has performed much better relatively and its money printing is off the hook.

Wrong again, please try harder.

The NZ Trade weighted index averaged around 60 in the 90's, today it is at 74. What you think is irrelevant, the facts are what matters.

1. The TWI does not measure the expansion of the money supply relative to other countries.

2. An oz of gold today is approx 44% more expensive than 10 years ago (USD approx 43%).

3. NZD strengthened approx 3-4% against JPY and 8% against USD in 2020. But it collapsed in March against both currencies. There is a reason for that.

Arguing against NZD debasement is pointless and futile.

If NZ$ was being debased faster than our trading partners, the FX rate (specifically the TWI) is where you would observe it.

Choosing the Yen is fallacious, Japan is unique.

It was also a fantasy 30yrs ago that you could be earning $60k p/a and have no chance of buying a house in Auckland.

Where in the world would anyone find such a great investment but NZ?

It's really not too hard to become a millionaire. Forget the bears and whinners, they are poor for a reason.

Its really hard to earn a $million salary in New Zealand and yet it takes a one $million bank deposit to save a miserable $10,000 per annum, before tax.

Japanesey is the future perhaps?

At the moment we are on the same central bank monetary policy track.

CWBW... 8% compounding growth (in NZ over the last 20 years) is actually pretty piss poor. I'm guessing the NZX50 returned double that, commercial property a lot more and if returns are compounded even plain old TDs wouldn't have been too far behind till a few years ago. Traditionally most property investments are negatively geared so there is usually no rental yield. Of course property investment is easy to leverage, which, when things are good (which they have been since 1980) increases returns. However, we should all bear in mind when things go badly leverage also increases the losses and they can compound just as powerfully and quickly.

In the last 20 years (or 40 for that matter), the NZ investment landscape has been akin to fishing in a marine reserve and an 8% compounding return almost an illustration of (financial) failure. It would be nice if things really were as simple as you believe.

So called shortage is just in listings. There is a truckload of unoccupied and under occupied housing out there. I pass many empty on my daily work and many with grandma living alone in a three bedder. Throw in the multiple units coming on (6 units one site, but only 2 get listed at a time) and all those airn bnb's chasing virtual tourists.

Hamilton rentals up 200 from a year ago to 635, for sales down over 300 to 427. (trademe0

tik tok.

It got worse over the summer as well. My Christchurch searches are currently returning about a third less the number of listings as late last year (200 instead of 300, which was already down from the usual 500 a few years ago).

Not mentioned as factors:

- inflation rising means it will erode debt leveraged up.

- safe haven orientation

- buying up loads of off plans, number of which we are not told.

- inventory depletion is a factor of factor above, ie stuff that would not sell a year ago is now selling for daft money

If loads of dwellings are being bought off the plans, then the inventory isn't as depleted as it may seem.

Not a "Black Swan" event but maybe a fluffy duckling?

https://www.nzherald.co.nz/business/land-for-giant-350m-426-room-radiss…

Sign of things to come?

Totally out of step now >400 room hotel plus 180 apts ... queenstown area

Not a "Black Swan" event but maybe a fluffy duckling?

Butterfly flaps it wings

Not a "Black Swan" event but maybe a fluffy duckling?

Butterfly flaps it wings

Hotel development in Queenstown falling over cannot be a surprise.

Labour voted in to address this and the inequality it is driving. So far a total fail and they appear to be doing nothing except a total sell out to protect the banks and the risky landlords. Shameful.

The Labour Party has been neo-liberal since 1984, at least National are honest about what they stand for. Jacinda was going to fix child poverty and then she ran up against a brick wall and things only continue to worsen.

I have always detested chardonnay socialists.

Although I like chardonnay. And socialists.

Don't worry about Jessy. The day she declared "Climate emergency" sealed her resume for her next lucrative job in UN. Every policy driven by her were bricks paving towards that. The country can burn all it wants as long as her plans come to fruition. The day she took over labour, we already saw it, and as expected, the dull and naïve fell for it.

Don' get me started. If we now have a climate emergency, why are plastic straws and plastic produce bags not banned? Too much talk and not enough done.

Let's see what they announce over the next few weeks. I predict it will be lame.

Everywhere you look in Auckland there is a wannabe developer putting 4-5 townhouses on an old 1/4 acre that used to have one house. For each of those townhouses they want 900k plus. How much exposure does ANZ have to these developers? The population is not increasing and the number of people who can afford 900k townhouses is definitely not increasing. The market cooling will be predicted by ANZ once any of these developers stop making their payments.

You say that like it’s a bad thing? The fact is we need supply and density of housing. Aiding that is being productive. Would you just rather it be the Mansons who do all the developments in Auckland.

I would rather we cap the Auckland population at what it is now and all the people who want to get rich trading land and houses with each other can get real jobs and businesses instead. Maybe something crazy like making stuff and exporting it.

The number of people that can afford to service the mortgage on a $900k townhouse is increasing. put 15% down, and you'll pay about $730/week in mortgage. Have a look what the rent on a new(ish) build 3 bedroom house/townhouse in West Auckland is.

Yeah just a cool $135k to produce a deposit..by the time a couple on even above average wage manages to achieve that the deposit goalposts have shifted north another $50-75k

Never mind that's committing $38K of after-tax income towards having just having a roof over your head at historic low interest rates to make bare minimum payments. Throw in PAYE, student loan payments, rates, insurances, running costs for a car, food (if you're into that kind of thing), childcare, etc...

The same people you expect to magic 100K plus into existence for a deposit are the same ones paying the exorbitant rents that mean they have shit show of getting a deposit together. Unless it is gifted to them. Do you really think one of these is worth a million dollars.

https://www.trademe.co.nz/a/property/residential/sale/listing/277404507…

Prag.. problem is getting the 15% ($135K?) while paying high rent, unless you have the bank of Mum and Dad.

ANZ just stating the obvious future, anything that running hot eventually will need to cool down.

For now, the clear observations can be made; every support & conditions are still being pumped into the hottie.

That photo.. Dave Moderato having a Thursday flashback!

Interestingly no one in political power is strong enough to tackle housing... they are simply avoiding it

They all know forcing house prices to decline to more affordable level is political suicide so prefer to talk to the issue - but take no action

What we really need is another credit crisis in NZ

Ardern has already stated that NZer's 'expect' house price increases

Wow compare that Covid induced "Blip" compared to the 08 crash and then even worse a record recovery while still in the middle of a pandemic. Stuff like this is enough to make you quit trying to make any predictions for the future. I'm thinking that the housing market has now absorbed so much capital that it cannot be controlled, its now just to big to let it fail and nobody really has the political desire to try and reign it in.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.