The momentum under house prices is "finally peaking", ASB economists say - but rental prices are now running hot too.

In the latest issue of ASB's monthly Home Economics publication, ASB senior economist Mike Jones says after "dining out" on 2020’s stimulus, the housing market is adjusting to reduced fiscal support and the fact mortgage rates are "about as low as they will go".

"Credit conditions are also tightening, particularly for investors, as LVR [loan to value ratio] restrictions return. Housing market activity and the pace of price gains will thus likely slow in coming months."

But this doesn't mean the housing upturn is over, Jones says. He expects house price inflation "to hold a double-digit pace" over the remainder of the year, with 15% price inflation for the year to December. By June 2022, however he is predicting 8% price inflation.

"The outlook for 2022 is really about how quickly the residential construction boom can restore some balance to the market. Our view is that rising supply and eventual modest increases in mortgage rates will pull annual house price inflation back down to single-digit levels. At this stage we don’t expect outright declines in prices."

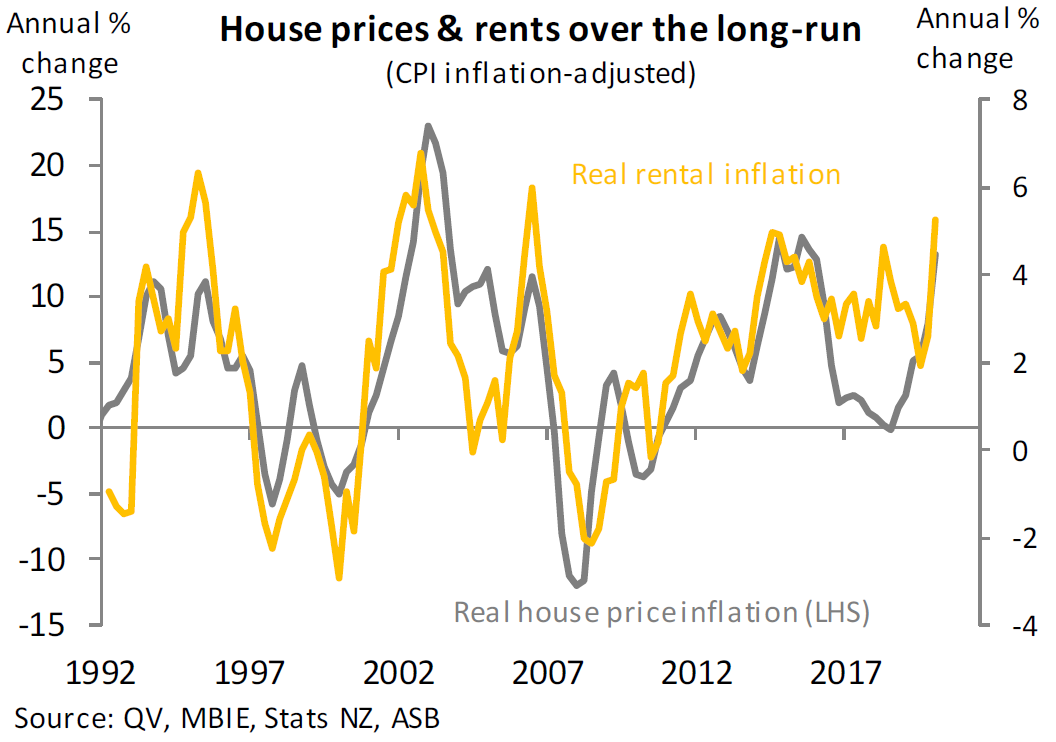

Jones says its "notable" that now alongside rapidly rising house prices, rents are now also lifting fast.

"Our smoothed measure of such, based on MBIE [Ministry of Business, Innovation & Employment] bond data shows annual rental inflation running at almost 7%.

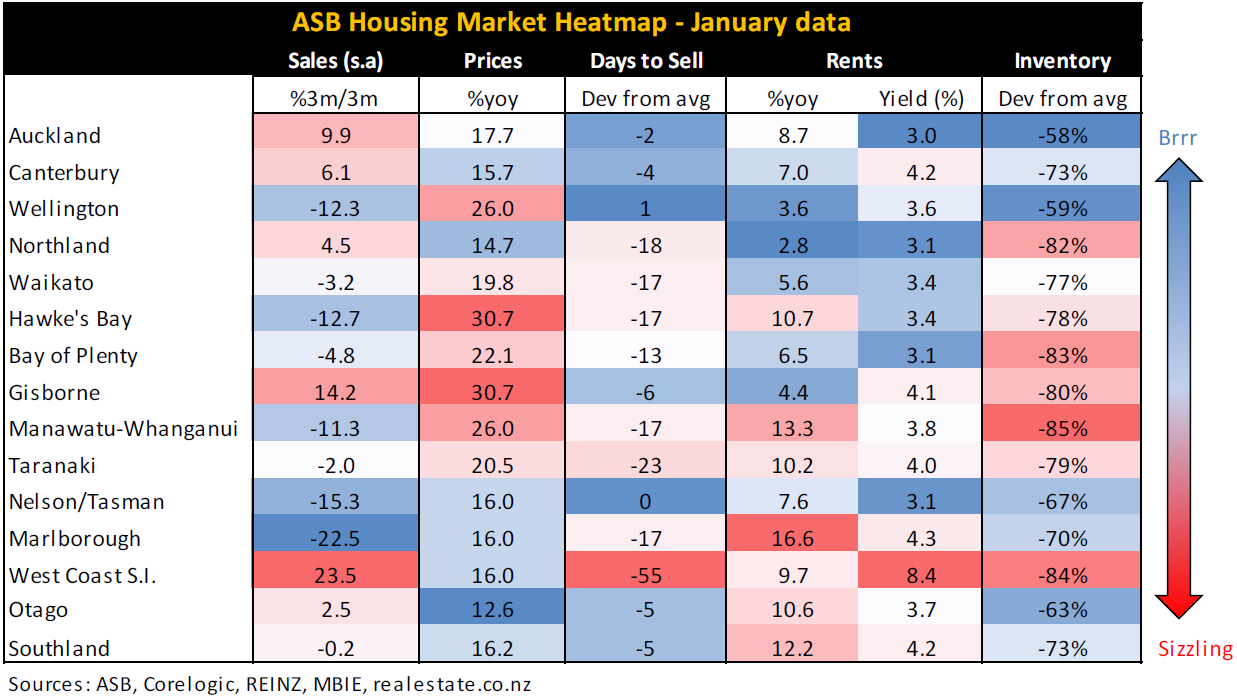

"There’s massive variability across regions – as shown in our Regional Heatmap [see below] – but six of the 15 regions we monitor are currently experiencing double-digit annual increases in rents."

He says the factor common to both soaring rental and house price inflation is a housing stock that is still running short of demand.

"We think it will be late 2021 before the supply response underway starts to restore some balance to the housing market. This is implicit in our forecasts for house price inflation to cool back to single-digit levels over 2022. Will we see house price declines? At this stage we don’t think so. In our view it would take a much more aggressive either supply response or interest rate shock relative to our what we are forecasting for house prices to start falling in the next couple of years. Valuation metrics are very stretched though, so the risk has risen."

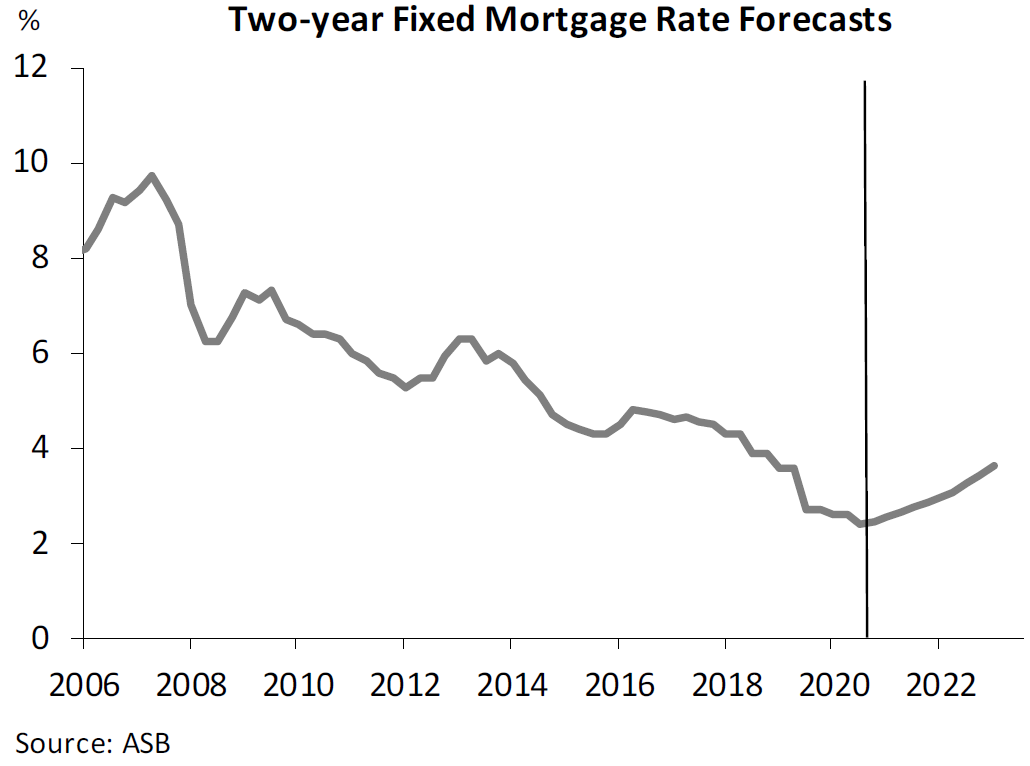

Jones says developments in interest rate markets in 2021 have seen the ASB economists "grow more confident" that the NZ house price impulse is peaking.

"There’s not a lot more juice left in the mortgage rate pipe in our view.

"We find changes in mortgage rates tend to flow through to house prices with around a two-quarter lag. Our simple mortgage rate model has actually done a good job of predicting short-term house price movements lately."

He says the big fall in mortgage rates in the June 2020 (lockdown) quarter went on to produce "a large house price impulse" two quarters later in December. More recent, smaller, mortgage rate falls are expected to proffer some support for house prices over the coming three to six months.

"But that might be about it. Wholesale interest rates are now soaring as financial markets factor in a brighter 2022 with vaccines, above-trend global growth, and less working-from-home-while-trying-to-get-kids-to-do-schoolwork. We think this trend for higher wholesale rates is here to stay. This being the case, the days of ever-lower mortgage rates are numbered. Our forecasts have fixed mortgage rates starting to turn gently higher from late 2021 (see below), removing what has been a key source of support for the housing market over the past 12 months."

79 Comments

The small 8% increases are exactly what we need. Thanks Jacinda.

By June 2022, however he is predicting 8% price inflation.

This still seems a very large figure when you consider it is 8% of a very high value.

For simplicity's sake let's consider a house worth one million. That is $80,000 over 12 months.

Someone who owns four such properties is looking at $320,000 appreciation

That's quite a lot especially considering the prices of other things like cars and appliances haven't gone up much. So percentage value increases distract observers from considering the actual dollar term increases. This is concerning. The implications for rising inequality are obvious.

Question become would it be sustainable for housing to appreciate (in real terms) from this point going forward.

If wages increase at CPI and the average wage is say $70,000 and inflation is 2% - then that is a $1,400 increase in wages (or ability to pay mortgage debt).

If houses increase at CPI (and nothing more) and the average house in NZ is $750,000 and inflation is 2% - then that is a $15,000 increase in capital value (and therefore deposit to be earned and debt to be paid).

High housing growth has only been sustainable because we've pushed interest rates to zero. Now that we're here - how does housing continue to grow at a dollar value 10x faster than wages ($1,500 vs $15,000) even if they both simply appreciate at CPI - or flat line in real terms?

And the short answer is ...it dosnt.

Theres only one direction from here.

Exactly. It doesn't. I have said this so many times before but I like the sound of my own voice (words). House prices have only gone up because some sucker is willing to pay more than you did for your house. Kiwis love to borrow to the hilt. So how do we keep getting house price appreciation (more suckers)? We give them the ability to borrow more via lower interest rates (serviceability). We're now at the point where interest rates have bottomed and wage inflation is non existent. Despite the best efforts of the 'next sucker' to borrow more they can't. What's going to happen?

"Kiwis love to borrow to the hilt." Very few people my age who have found themselves having to sign up to 30 year mortgages for a stable family home enjoyed the idea of "borrowing to the hilt". You might be more correct to say "older Kiwis expect other people to take on far more debt than they ever had to for the privilege of having a roof over their head that they wouldn't get turfed out of at short-notice".

I would say Kiwis don't like "borrowing to the hilt" and this is a recent development. Our changing demographics have made borrowing to the hilt more acceptable when once it was terrifying.

Exactly. I think we have only been conditioned to get these huge mortgages for the last 20 or so years since they have gone until 10%. Infact I remember when my parents got a mortgage and were paying in the teens, they said that the first thing they needed to do was to pay it off as quickly as possible. That was back when the bank manager used to have to come to the house and see it before approving it, and mortgage approvals were no where near as easy either.

We would probably be in a disinflationary environment if Reserve Banks weren't yeeting up asset prices. In that sense a single digit house price growth rate may not be sufficient to support Reserve Bank CPI targets without a hike in per capita income. However it's unlikely we will get a hike in per capita earnings in the next few years.

GV 27 there are also young investors that borrow to the hilt with the aim of accelerating equity gains. Risk tolerance is generally higher when young.

Ah yes. Apologies. "Love to" is probably not the right phrase as many currently borrowing to the hilt are doing so out of necessity to get into housing. If FHB were the only ones in the market outbidding each other we wouldn't be at these levels for sure. Having to outbid mom and pop who are using their new found $300k-$400k of equity in their existing house (which is now 10yrs older) plus you know they're older and likely to have more savings to add to this and voila we have a problem. Boomer: "I know they just want to have the same opportunity we had and that I'm making that harder for them but what about my returns? With TD rates so low and tax-free gains in housing what am I to do to get a decent return? Who's thinking about me and my retirement?"

Should just push interest rates back to 8% - give the boomers with cash a return to live from and push them/incentive out of the property market as investors. While reducing the value of houses and improving FHBs ability to save a deposit. But hey... that might require a 50% fall in asset prices but everyone is too selfish to experience short term pain for longer term stability.

So boomers/specuvestors who cause the problems cash out en-masse to become the beneficiaries of higher interest rates on savings, while owner-occupiers and FHBs who spent years getting a deposit together face being wiped out? I can't see it being hugely popular as a proposal, unless there was a Freddie Mac-style crown refinancing option for existing mortgage owners on their family home to help ease the pain.

And NZD to the moon, decimating our exports, with mass layoffs affecting those same recent FHB. It's not going to happen.

Who says the Fed don't beat us to the punch and we simply have our hands forced to follow their lead - I mean, we've followed them down and we'll follow them back up again. They don't care that the average NZ house is twice as expensive as the average US house and that we've mortgaged ourselves through the roof with private debt.

Oh for sure, external shocks don't care about our lazy domestic political operators - I would prefer a structured, supported paring back of house prices on our terms as opposed to something we don't have any say over that happens overnight.

As Jacinda Adern has said - the people have spoken and they don't want prices to fall. We've wanted this mess. Now we have it. Now we live with it. National told us it was a sign of success.

They may not have a choice. It depends on how big they want the pain to be. The probe is they don't have a plan. eg What population do they want NZ to be. They are just pumping up the population which is going to have major cost implications in the future. I would have thought the current population of NZ is about right.

The boomers and specuvestors can't all cash out en-masse because they only have paper wealth at present - that paper wealth could evaporate if there are no buyers at the current market values. So despite what you say above, only the boomers/specuvestors who cash out immediatly would be the beneficiaries if the markets were to fall, the remainder would, like you, take a significant hit (so you wouldn't be the one and only victim in this nasty game the central banks are playing).

Indeed the smart money are cashing out now, including selling off quake damaged EQC claimed property without declaring it to agent, but caught out - 30a Euston Road Wilton

"Not being the only victim but still being financially ruined" isn't still the huge draw I think you think it is.

And you're missing the most basic part: If only the people who get out first get to keep paper wealth, then what is going to happen? Everyone will try to get out at once, which will just absolutely smash prices through the floor. Even if houses dropped by 50%, there will still be some out there who will make a realised gain on properties in their portfolios given how long this rort has been going on. But a 50% drop would wipe out anyone who has bought a family home in the last five years. That may be acceptable collateral damage to you, but after years of property investors milking bouyant values tax-free and continuing the accommodation supplement even though we know it causes huge distortions, there's a moral obligation on the state to help owner-occupiers stay afloat.

"If only the people who get out first get to keep paper wealth, then what is going to happen? Everyone will try to get out at once, which will just absolutely smash prices through the floor."

Yes that is what happened during the GFC in America and that is what I witnessed in their housing market there. And our bubble is twice the size of theirs now. So if we see a change in sentiment - you're right. It really could gain momentum on the downside. But that is how bubble psychology works and how Shiller describes it in his work on asset bubbles.

"there's a moral obligation on the state to help owner-occupiers stay afloat"

No there isn't. I thought you were a National supporter? This comment sounds like something a socialist would say? You might be surprised how little the rbnz and government do if the market does start tanking. They've already fired all their ammunition at this to keep it afloat. At some point in time, the state will need to cut its loses in order to keep itself solvent. Thinking it will bailout every person that has purchased their home in the last 5-10 years will be wishful thinking - perhaps we should have taxed the gains property investors made the last 20 years we could have created a fund to bail out FHB if this house of cards falls over - because of the greed of property investors? Other tax payers who only own one or no houses should not be wearing that tax bill.

I understand your position - but this whole situation is morally corrupt. Blame the politicians, blame the central banks, blame the retail banks and blame the property investors who have been buying a 3, 4, 5, 10, 20, 50 properties, paying no tax and gloating about how wonderful everything is.

"All get out at once" and live where ? Houses are not like Bitcoin. Houses are a long transaction process when it comes to selling. People are still piling in to the housing market so I think any pouring out is a long way off.

If people don't pay the asking prices, then prices will have to fall. But because supply is so limited,and demand is so high, there are some people who are paying these crazy prices, and if it is more than expected, it just pushes up all of the other prices in the area.

Longer repayment terms to 'increase affordability' (read satisfy the rent seekers) and/or unsustainably high levels of immigration.

Increase serviceability. Increase affordability.

Same same

But different.

"Question becomes: would it be sustainable for housing to appreciate (in real terms) from this point going forward."

There is quite a bit more room for prices to rise in the future:

1. with the increase of NZ's desirability as a place to live, the government can (and will) turn the immigration tap back on.

2. inflation: as rents rise due to inflation, the yield on investment properties will increase attracting further investors

3. there is yet room for interest rates to go down - should another shock hit the world/NZ

4. there is a LOT of money sloshing about the world economy due to governments' money printing - some of that will make its way into NZ property

5..

If you think we've reached the top - think again - look at places like Canada where in Vancouver the average price of a standalone house has reached more than 1.8million CAD this year.. (and they have a capital gains tax, empty homes taxes, property transfer tax)

https://www.cbc.ca/news/canada/british-columbia/pandemic-real-estate-va…

Yes and Vancouver is as screwed as NZ is. Will immigrants just show up and pay cash for the house? If rents rise, then wages must rise, but that means other costs also rise, including debt servicing costs = zero sum game. Sure if interests rates go down, but its only making the situation worse.

Yes, things like capital gains tax, empty home tax, etc. are only treating the symptoms, not the cause. But councils like it because it's a revenue grab.

They are hardly inclined to solve a problem that makes them revenue.

Interesting comments, not much weight given to border reopening? ImmigrationNZ appear to still be processing visa and residence permit applications.

We might be having a massive wave of emigration too so immigration numbers might not make up for that.

b21...if we really do see a massive (and sustained) wave of emigration we can then start thinking about factoring that into our immigration settings once it happens. Until then it just sounds like a dubious prediction made mainly to support the continued flow of "net negative migrants".

Sure, why didn't you reply to the message I replied to with the same argument?

because sooner or later it is 100% certain that the border is reopening and very likely we return to mass immigration soon after whereas masses of people emigrating is far less likely.

Not really, I am aware of a number of both kiwis but mostly immigrants with resident visas currently thinking about the option of returning home where they have better economic and family support. Ignoring this would be a mistake.

I believe they have taken border reopening into consideration. You need to remember it's two ways, there are people coming in, but there are also people going out too. Even if there are lots of people are coming in New Zealand after border reopened, I don't think it will do much impact on housing price. Remember Auckland now is the fourth least affordable city for housing in the world, not even mentioned about its crappy quality of housing.

Some of the Kiwibuild houses don't look badly priced. But few available, and many seem to be a substantial distance away. Apartments are where much of Auckland is heading, and I can't see huge price growth in many of them.

Bank economists' predictions. The guys who predicted a 20 % Decrease in house prices last year. Then quickly changed tack to a 20% increase!!! Typo error perhaps???? I may be better off reading used tea leaves!!

Starting to see a lot of these "house market will cool" articles coming from banks and real estate. A tactic to stop the government acting?

Exactly. Give them the perfect excuse to do nothing... ‘just listening to the experts’

In New Zealand you don't need to stop government acting, they do it themselves. It's keeping the bayonet to their backs that's a challenge.

There comes a time when the public get annoyed enough that they have to act to some degree (Nick Smith got a clipboard out for example).

Now they can instead say that the experts think it is going to cool so no need.

Cunning buggers.

Looking at their forecasts , Auckland median should rise to $1,153,000 by June 2022 up 153000 . Bbrrrr

"Wholesale interest rates are now soaring ... Our forecasts have fixed mortgage rates starting to turn gently higher "

There's only one way that happens - more market 'stabilising' interference from our good friends at the RBNZ.

And who picks up the tab for that? You and me.....

People should just do what ASB's whimsical marketing suggests, and deprive themselves of nutrition to the point of hallucination to save up a deposit. I mean, you have to make *some* sacrifices if you want to own a villa as your first home!

I find that ad very insulting.

Mostly because it suggests that buying a lovely villa is possible for a young couple if simply *grow some veg*. Wow!

It's like suggesting disabled people could leave their wheelchairs and walk if only they did some more exercise.

I've seen other people express similar comments; if you are lucky enough to have a rental with a garden, and lucky enough to be in it long enough to cultivate a massive crop of vegetables, and you were eating 45+ meals or so a day, then sure, I guess replacing every single one of those meals with your home-grown crop could save you money fast enough to put together a deposit in an LVR world. Although why you'd go through the effort of growing veges when you could just offer to supply you local gang pad with wacky tobacky at a fixed price and plant that instead, I have no idea. It would certainly be less morally offensive if they'd done this in the ad instead.

Well the guy did think his wife's face was a tomato, so maybe that is exactly what they are doing.

Yep no more smashed Avo and flat whites out at the Cafe for you its home grown tomatoes on toast if you want that deposit. But seriously thoughj probably not even worth growing your own, was able to buy nice tomatoes for $1Kg the other week, very nice on toast.

Is this Ad on YouTube? Can you link it for me? I don’t watch terrestrial TV anymore (too many Ads for my liking) but I’d be interested to see what sort of brainwashing the population is being exposed to.

The comment section appears to be moderated, unfortunately.

I miss ASB's Goldstein ads

It's perilous to comment on certain groups within NZ society and my observations are anecdotal but I have noticed that many immigrant families within my social circle own multiple properties. When I was younger landlords were rather rare but are now commonplace.

It was the smart thing to do, increase property holdings, as it was also an obvious thing to do when looking at NZ and historical property values and future trends. An outsider could probably see it in a clearer way while New Zealand born people tended to disparage their own country and were happy with the traditional life not realizing that things were changing radically. Increasing immigrant flows, a passive and complacent local population in a world of rising wealth made the property value increases in NZ inevitable.

Certainly many Kiwis born here have indulged too but it would be interesting to see an actual breakdown of landlords by New Zealand born and not New Zealand born. It is a skill having the ability to take advantage of a good thing when one presents itself. A phenomenon no doubt common in all the English speaking countries and a phenomenon that many didn't consider when being told that immigrants bring ready packaged "skills" to the country.

Zach...had you considered that a number of these "new NZer" immigrant families own multiple properties because a fair proportion of them are purchasing them on behalf of non NZ family, relatives and even paying customers. And I believe that to say it is particularly prevalent amongst a couple of specific races is a cultural observation rather than a racist statement.

what you say agrees with my experience years ago, when working for a carpet retailer and the number of installations and properties in the database under certain family names, 100+ houses

And across the pond Governor Lowe has reiterated that the RBA is unlikely to increase the OCR until 2024. Why there is this sudden belief that the RBNZ will raise the OCR earlier and have its own party is perplexing

Cowpat...RBA is posturing. They know that they (just like the RBNZ) do not have real control over the OCR. They may set the rate and announce it but...

That's why Australia has the OCR currently at 0.1 percent or a lofty 0.25 percent in New Zealand . They have absolute control of the OCR.

With what unintended consequences?

Cowpat..we will have to agree to disagree as I feel the RBNZ and RBA could have their hands forced by a number of factors including (but not limited to) inflation, currency rates, unemployment rates or interest rates in other countries.

Agreed, their appears a myriad of factors that could upset the cart (and more so than usual) and make well reasoned forecasts or strategies look stupid in a day week let alone a year. For New Zealand its a minnow, it could blow up tomorrow , and it would not matter globally ( other than China sourcing WPC and Australia lending a hand to its banks). Everything is relative of course , if the NZD were to suddenly decline then I would reconsider our outlook.. Our investment strategy for the first time is considering a substantial and prolonged decline in the JPY and its impacts .

After 20% and 15% if have 9% rise even that is too much.

Million dollar house was selling 1.2 million than now at apps 1.38 million and next year at 1.5 million plus ........

Crazy. Why should anyone do any business if can earn $100000 to $200000 plus per year.

In NZ house market wither goes up (mostly as promoted and supported by RBNZ and government) or fall - never plateaus.

If expecting to keep on rising forever after such magnificent jump of 30% to 50% is going with belief that house price never falls and will never fall in NZ - to be honest partly correct as is the only economy and have support of all.

Money talks :

Any other country would be boycotted but hard as money talks :

https://www.newshub.co.nz/home/world/2021/03/xinjiang-landmark-report-f…

Typical economist: a bob each way.

And they don't take into account that even leaky homes which in the past haven't sold are now selling. One in a terraced block of 4 just up the road in a leafy suburb has just sold; didn't sell at last two attempts a year or so ago. A brick and tile 2bdrm unit next to where I bought a place for my disabled sister in the early .2000s has stormwater drainage problems causing the garage to flood just sold for well over $1,000,000. I can tell leaky homes a mile off because I did work as an assistant to a building surveyor back in the early 2000s.

This phenomenon speaks to the fact that a large proportion of houses now coming on to the market are rubbish but still selling. So any estimate of houses listed and sold must take this factor into account: i e good listings are down and selling and bad listings are up and selling.

I expect some journalist from Interset.co can explain this better than I can, so could one of you please give it a go

Half of the good listings are being bulldozed anyway, the actual house is normally a tiny fraction of the purchase price.

Jimbo

That's a separate issue. You can't demolish a whole block of terraces or apartments if only one in 4 sells..or one in 6 sells...all 4 terraces or 6 home units would have had to sell to the developer/demolisher more or less at the same time to free up the whole site for redevelopment. This is certainly happening with the developer purchasing adjoining houses on their own freehold sites.

I guess the fix costs have become less significant now too. $300k to fix a place that will be worth $1500k after doesn’t seem so bad.

Yes, alot of mono homes on the market here in Welly, and earthquake damaged sh*t by supposedly reputable people

Ridiculous.

Everyone knows you can't lose with houses.

Mate.

We all recall the various banks predictions on house price falls at early Covid ? How accurate are their current predictions/guesses?

I think those forecasts weren't factoring in the massive amount of stimulus via fiscal and monetary policy. Take those out and let the market do it's thing then they likely would have been right. RBNZ and govt had ammo then...do they now?

Finally peaking..? the grabbing headline, inside it's just another OZ banks scare mongering forecast, knowing what lies ahead. Nope, be sure this transformational govt & RBNZ - really keep march on forward. What they're aiming, actually not many knew in public. They're gunning the OZ banks! - so march on Mr. Orr, buy more of those bonds, keep OCR low (we still expect you to put into negative), Play your short term mandated 'independent' action, more QE stimulus plenty reasons are open to choose; 'housing supply'/new govt PR-hence it's not legally binding, coastal erosion/Insurance bail out, Carbon Neutral/Climate emergency, Gender pay parity, overall more $ subsidy to be administer by govt to manifold increase wages/salary, in order to keep up with the raising rental and housing cost. They all will end up with OZ Banks.. just unsure how all those 'unlimited numbers of $ recent creation' considered profit.. are 'worth what they are' by International trader.

.. 'how long that past romantic notion of NZ as a wealthy country'.. it's all in the current market/traders perception, the future will be based on 'real confidence'.. when about dealing with NZ economic parameters.

This property in Tauranga sold for $1.1 million today. RV of $635,000. Nearly doubled in sale price in just over five years.

https://www.trademe.co.nz/a/property/residential/sale/listing/299270755…

interesting about the rent front - seeing the opposite in Wellington (specifically the hutt valley) . I've been watching the rentals in Lower Hutt since Jan and about 1 in 3 are having to discount their listing price rent (with the average discount been $48) before been able to lease the property.

Rents had started to average $650 a week in Lower hutt but this week - just 8 of the 27 properties this week had listed rents greater than $650.

I should hope so, $650 seems like a lot for the hutt

Short term momentum behaviour means little to long term investment horizon.

No one questions Usain Bolt for taking his time mid race with his competitors seemingly catching up as long as he keeps running and finishes the race. The same should be thought of housing inflation, interest rates and investment tenure.

I wouldn't be surprised if there has been a bit of a pull back from buyers in March. I think FOMO may have worn off a bit. At some stage more houses will come on the market. I guess if houses do start to decrease, they can open up the flood gates on migration again. But the downside of this is all the extra costs we will face in the future with the need to increase infrastructure, health costs etc with having a larger population.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.