By David Hargreaves

The annual rate of growth in mortgage borrowing has topped the 8% mark for the first time since June 2008 as the Kiwi appetite for borrowing to buy houses shows no signs of abating.

And while clearly the low interest rates are encouraging the surge in borrowing, the more recent falls in rates and uncertainty about future rate movements seem to be encouraging borrowers into short term fixed mortgages - and even into the recently out-of-vogue floating mortgages.

The latest figures, collected by the Reserve Bank, show that the total amount of borrowed mortgage money in the country stood at $215.687 billion as at March, up from $214.207 billion in February and $199.693 billion as of March 2015.

Separate figures also collected by the RBNZ have shown a sharp spike in the amount of mortgages on floating rates as well as those on fixed terms of less than a year.

In terms of total household claims, which also include consumer credit - but are mainly mortgages; these increased by a seasonally adjusted 0.6% in March. It's the fifth consecutive monthly increase of that magnitude and you have to go back to April last year to find a smaller monthly increase (it was 0.5% that month).

On an annualised basis, the total household claims figure increased 7.7% (also the highest rate of increase since June 2008) to $231.071 billion, up from $229.731 billion in February and $214.629 billion as of March 2015.

These figures come out as concern about the overheating house market, particularly in Auckland, steps up.

The RBNZ had kept fingers crossed that its new borrowing restrictions applying to Auckland investors from November would rein things in. But after a very brief pause the market, as shown by March's sales figures, reignited.

The RBNZ's relatively recently introduced mortgage by borrower type figures for March showed that housing investors, after pulling back at the time the new lending restrictions were introduced, surged again to a new high of over 35% of the more than $6.5 billion borrowed in total during the month.

Unsurprisingly, household debt ratios are rising, which will be concerning the RBNZ. The most recent figures on this showed that the household debt to income ratio has hit a new high of 162%. Westpac economists recently cautioned that the surge in borrowing that's seen levels of household indebtedness hit these new highs could ultimately produce a "drag on economic growth" as the debt is repaid.

ASB economist Kim Mundy, while noting that housing credit remained "very strong", also observed that the rate of household monthly credit growth (seasonally adjusted) had remained steady over the last few months, "but we expect this to slow over the remainder of the year".

"However, while we expect housing credit growth to peak soon, the tentative re-acceleration of Auckland’s housing market could delay the peak and limit the extent of slowing."

She said the "shift in mortgage duration preferences" remained evident.

The latest RBNZ figures show that the amount on floating mortgages spiked up to $51.402 billion in March from $50.631 billion in February in what was the largest monthly rise since 2012 when floating mortgages were the preferred method of borrowing. An even bigger spike was seen in the under 12 months fixed amount, which climbed to $80.316 billion from $76.806 billion in February.

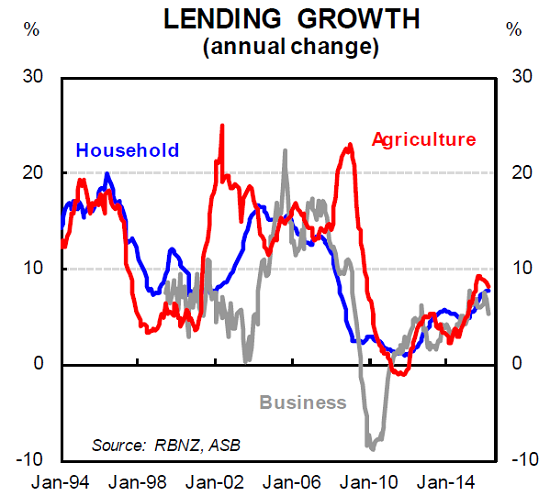

Elsewhere in the latest sector credit figures, business borrowing, which has been really quite volatile in recent months, had another mini-surge in March, rising to $90.695 billion from $90.134 billion in February, though the annual rate of growth slowed to 5.3% from 6.8% as of a month earlier.

Agricultural debt, being closely watched because of the global downturn in dairy prices, again climbed to a new high of $59.372 billion in March from $59.014 billion a month earlier.

However the annual rate in growth is continuing to ease, to 8.2% from 8.6% the previous month and a recent high of 9.3% seen in September 2015.

*This article first appeared in our email for paying subscribers. See here for more details and how to subscribe.

86 Comments

We're breaking all the wrong records these days - first in the world for house price to income ratio and second only to Qatar in terms of real house price growth;

http://www.imf.org/external/research/housing/report/pdf/0416.pdf

Anyone who thinks this isn't going to all go absolutely pear-shaped needs their head read.

are you talking about nick smith or the people that actually listen and believe

http://thespinoff.co.nz/29-04-2016/a-ruling-of-the-spinoff-editorial-bo…

“If you look at the Massey University Housing Affordability Index, independently produced by that university, actually housing affordability in Auckland and every other market in New Zealand is actually more affordable now than when National came to Government.”

I guess the index is weighted towards the cost of debt servicing.

It looks like the gradient blue squiggly line has flat-lined and is about to go negative. The gradients of the gray and red squiggly lines are both already negative.

Luckily we have a compliant media ready to pump the bubble at the drop of a hat (that includes this website).

Don't attack the messenger , ( particularly this website ) . They are not creating this news , they are merely reporting the facts , and yes mortgage borrowing growth has now caught up to the pre-GFC levels .

Its been on an upward trajectory for some time now .

And that's scary , because we are borrowing (sic) ourselves into an ever deeper hole

Reporting "the facts" and avoiding "what if scenarios".

It is apparent that Government is not taking any meaningful measure to dampen the real estate market and has give free go to investors. But measures taken by RBNZ are not effective as well. The simple step of applying differential rate of interest can do the job effectively , which could be cheaper loans for agriculture, manufacturing and first home buyers and higher rate for rental as this in not productive investment , and ring fence loss against investment property

Madan that may help a little however wont change things from their current state. Investors are not buying in Auckland for rental yields at the moment. They are buying in anticipation of further house price growth and capital gains. So if prices are rising 10-15% per year, then an extra 1% interest won't do jack. What is needed is something to make it unprofitable for them to flip homes or to buy to chase capital gains. The best option that will bring things to a halt very quickly is a 10% stamp duty on existing homes. For those investors still willing to buy existing homes great news the govt will get a windfall of 90k stamp duty for every average priced Auckland hold that is sold. Throw that into better transport and other infrastructure and really make Auckland something special.

Capital gains tax, increasing interest rates, increasing LVSs are pretty much just rearranging the chairs on the Titanic. None of these measures will put investors off enough whilst house prices are rising 10%+ a year with a lack of supply and huge demand. Get the investors putting their cash into new homes where it is needed to help balance things out on the supply side.

What surprises me is that the Herald ran their Home Truths articles and I don't think STamp Duty was even considered even though UK, SIngapore and Australia all have it. Surely it was worth considering. I could be wrong however did not see anything on it.

The same could be said about interest.co.nz so perhaps there is something about the Media and not wanting a solution that would rock the sponsors too much.

When you have such a pure speculative market buying a house for both FHB and specufestors alike is akin to playing a high stakes game of chicken.

It will stop eventually, it is a mathematical certainty and it's going to obliterate the last entants and the NZ economy. Why National and their cheerleaders have aided and abetted this situation is beyond reason.

It wont necessarily obliterate the last entrants. What if house prices just stop going up, just go up little or even down a little? It still makes sense to buy rather than rent for a number of reasons even without capital gain especially if you have a good deposit. You are just being hysterical.

So some people may get a haircut. Happens all the time, I lost more than half my wealth in a marriage breakup. You pick yourself up and move on, it's not Armageddon.

I'm sure people wouldn't be too bad if they lost half of their wealth (read: equity).

The problem is that isn't the real risk we are talking about - this is the real risk of negative equity. Losing all, plus more.

I agree with you for moderate deviations in the rent to mortgage cost ratio.

That is not the current situation, it's a speculative frenzy with nobody giving a damn about cashflow or fundementals. It's a really risky situation and the longer it goes on the bigger the risk.

There is nothing to justify the current prices except the hope somebody else will pay more in the future. Sooner or later somebody won't pay more and prices will fall. Why would prices hold steady when there is nobody else to sell to and you are losing a great deal of money on the outgoings?

What is there to backstop a drop once it gets started. How much would prices have to fall from current levels to so that an equilibrium is reached with rental income covering costs? That's easily how much the late entrants could stand to lose.

I agree, the fundamentals people are thinking about are migration, liveability and all the other reasons this time is different. Not actual fundamentals such as cashflow. People are acting as if this is all government guaranteed money, free money, risk free return. The conviction that prices will never fall is incredibly strong in most people.

If prices just stop going up, you will be losing money hand over fist, if you own rather than rent in Auckland. Just the interest payments alone on a $600k loan will cost $30k per year, plus rates, insurance, maintainence. Gross yields are 2%, interest rates are double that.

One would assume that you also lost half your debts with a marriage break up, if only the banks would be so kind.

If a couple both work and have a decent income 30k is not too much for your own home. Most people who currently have a home don't have 600k mortgages, that's more like the landlords who then pay it with rent and possibly a little more like $300-500 in each month.

Sure if someone timed it badly it possibly wouldn't be great but the majority of people have been in the game 3-40 years.

For the 20th time, your grunk on with stamp duty is a non starter! No matter how many times you type it.... its never going to happen. What part of it didn't you understand from the last 4 people that told you? Envy tax lover!

Prices stop growing implies supply and demand is more or less equal. If the growth in consents and building activity is anything to go by, I'd suggest an oversupply if demand declines from current levels. Also, as per the IMF graphs, there's nothing underpinning the current prices in Auckland other than speculation. So, when these gamblers start running for the exits, who knows how hard the landing will be

GM you are so right , the market could be stopped in its tracks as soon as the next budget :-

1) If Bill English phases out the generous tax allowances for speculators and investors

2) And Nick Smith restricts non-resident , non Kiwi buyers to new builds only ( Like OZ)

3) If the immigration rules are tweaked to slow down the fake so called investor category scam ( where they come in and "buy" a coffee shop/ hair salon/ nail bar / fish shop with borrowed money and then as soon as the get PR they are tossed out of the shop to make way for for the next candidate) .

National is losing support from younger voters over this issue and they are well aware of it . Winston Peters is putting a cracker up the arses of older voters with anti-Asian migrant fearmongering and growing in the test - polls .

John Key has to act decisively

The problem is only the government can stop the gamblers at the moment and they are unlikely to do so. It is fairly simple. As long as the market doesn't crash under their watch then they are the off the hook and it will be the next government's fault. So keep the party going and try not to rock the boat too much.

Gamblers is right. We know some friends so desperate to not rent they went and got mortgage via KB, borrowed $50thou more than they budgeted for, and after signing the paperwork found that they are paying $70 more a week than they budgeted on also. If interest rates go up, or bills etc they will be in trouble, but desperate people do silly things

They will be the ones laughing in 10 years. Rates are going absolutely nowhere anytime soon. They will look back at the sacrifice they made between 2016 and 2026 while looking at a 1m equity.

Is a million in equity still a good thing if you need somewhere to live?

Yeah it is. They could sell that house and buy something bigger. Using that equity. Or - they could of stayed renting and had nothing.

Lol bingo, obese and others forget that simple reality eh, that capital gain is only relative to where you buy the next house and for how much

Yeah.. and? I haven't forgotten anything. That's how life works. You either start somewhere, suck up some pain, slog and move up. Or rent, moan and spend all day on websites telling people with 7 figure equity how stupid they are.

What is wrong with renting? If you have 7 figures does that include the decimal points, or just your weight, seeing your Obese?

great come back dude, keep em coming.

Yup can't wait to hit 8 figures, now that's a real milestone I will strive for till my final day...stupid thing is I have rented for twenty years, bloody mad to live in your own house as there are no tax benefits ;-)

ceteris paribus

but their expenses , rates, insurance , maintenance will rise faster than wages, so they would be banking on cheaper interest rates to tread water

Yeah I don't think the OCR is going up anytime soon but... How about council rates? Bank fees? Electricity? Car breaks down? Washing machine gives up? Etc etc

Many of the same things affect you whether your paying a mortgage or renting. Some people just don't get the maths involved in renting vs a mortgage, its very straight forward your better off buying a house. The issues are elsewhere like do I want to be stuck in this relationship long term, I'm going to have to lower my sights a little for my first home and just the long term commitment involved. Getting your head around a 25 year mortgage and the fact your going to have to work your ass off is just too much for some people.

Nah, many renters are cash rich these days. Not having enough to join a ponzi scheme does not automatically imply they are cash poor. Maybe they see it for what it is Carlos? A total and complete con

That's right. I have the cash to buy - but not willing to take the risk of buying into such a ridiculously over priced asset class. I'd love to have my own home. But just not stupid enough to be highly leveraged on property in NZ at this point in time. So I rent....for now.

Independent_Observer - Will you buy after prices drop by a certain percentage? If so what percentage? Or if mortgage interest rates drop lower? Or potential rent yield looks better? As you would love to own your own home what will be the trigger for you to enter the market? Serious question.

Don't expect an answer Zack. This is where the "Ponzi" schemers fall down. A 20% drop takes you back to Dec 2015. You'll never see that again. They have been wrong for so long that they need to double down on their bet of a huge correction.

For ZS. 30-40%. If this doesn't happen in the next 5 years I'll either leave Auckland or New Zealand.

And yes you're are so clever OB!

You sound like a stockbroker making a sales pitch in 1929.....Everyone look at how clever and greedy I am. Good for you.

You know how bad the GFC was right? It fell 15% for 18 months! You'll need a fallout shelter to see 30-40% drops.

I've already got one - its the current shoe-box apartment I'm renting...One of your mates probably owns it!

Wishful thinking. The RBG saved the bacon post Lehman Bros. OCR dropped by 5.75 between July 2008 and April 2009. Little pork left in the barrel this time round.

You could easily shave 50% off most of the AKL prices at present. Think fundamentals.

I think Loose lending....... and I just don't see any. I don't see any catastrophic event that takes the world to a place even close the GFC in the next 10 years.

If you ever have the chance to put down the property press, you should consider reading The Black Swan by Nassim Taleb.

...you don't see any coming. Fair enough, my guess is you didn't see any of the previous either. Yes, the Black Swan..worth a read.....

Maybe some people understand the maths involved rather better than this comment implies you do. There's no blanket rule that buying is better than renting or vica versa, it depends on a huge number of factors including current rental yields of property, expected future of interest rates, expected future of house prices and rents, and what alternative investment you would put the excess funds into if you continue renting. Right now in Auckland, looks like renting is a good bet. Where I bought my house, owning was cheaper than renting from day 1 so it clearly made sense.

The big advantages of buying rather than renting are stability (which is a double edged sword if you might be moving around), leverage (also has its downsides) and enforced saving for those who would spend any excess. There seems to be a fear of any investment other than property in New Zealand, and a strange idea that pumping money into houses is the only way to get ahead.

Maybe it is not so much maths as will power or psychology. The inaccessibility of the savings and unrealised gain works for many people.

Let us know how you get on in rented accommodation when you retire.

Nah, they won't. It's a 30 year and selling in 10 won't be enough time to pay all that interest

It seems like no matter how sensible or frugal you are there are plenty of people out there ready and willing to push to the absolute limit. This is why tighter lending requirements are needed.

Speaking of which, check out the latest lending restrictions on BTL in the UK. I think it would be akin to blasphemy in NZ to require the rental income to cover the interest payments, let alone 145% of them.

http://www.telegraph.co.uk/business/2016/04/30/big-lenders-rein-in-buy-…

more expense coming for landlords, is the first of political parties bringing in tenant friendly policies

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11632404

Labour leader Andrew Little will tomorrow make a bid to raise minimum standards of heating and insulation for rental properties.

However, the Government could scuttle his chances by making its own moves to toughen the rules for rental properties to keep its support partners onside

Tighter lender has been introdued. 20% deposits, 30% deposits are all regualtion now. Do you think 40% for FTB will win you any votes? Everyone pushes to the absolute limit when you buy a house! You are constantly broke for a year or 2 when you buy one. Thus as it ever was. My parents told me they couldn't afford carpet for 3 years when they built their first place. Before you see those rules and regs in NZ there needs to be rate cuts to .5%, FTB schemes in place and a lot of other taxes added to slow the market. It will come though, give it 3-4 years.

There should be prudent restrictions on lending to income multiples like in the UK.

Votes have nothing to do with it, the RBNZ isn't an elected body.

When people see things as a cant ever lose situation this is the result. The belief in pyramid schemes is strong in this country

Well to allow the house party to continue, the government and banks will need to drop interest rates.

Otherwise the only people that will be able to afford to purchase Auckland housing will be the Non-Resident Investors and wealthy immigrants who are able to purchase their citizenship rather than earn it on merit of their skills, education background and dedicating five years of their lives to New Zealand.

its all part of the merry go round, young born and bred kiwis are heading across the ditch to try there luck as they are giving up on the NZ dream to be replaced by a wave of immigration.

i expect to see the pace pick up and its not surprising that the aussies are not happy about it, how many do we have other there now about 1 mil

Another example of debts growing at triple the speed of incomes. For those who don't know math, the way this ends is with a mountain of defaulted debts.

Its' always a good time to revisit Michael Hudsons article ..."Road to serfdom"

Written in 2006..

http://michael-hudson.com/wp-content/uploads/2010/03/RoadToSerfdom.pdf

Buying a property in NZ and especially in the main centres has been a game most Kiwis wanted to play. Looking back now it seems crazy that people didn't buy a house and chose to rent. Inflation and steadily rising wages made the game fairly safe and high interest rates kept it governed. Perhaps too there was some Kiwi unwritten code of behaviour, some reluctance to being a landlord.

With the massive rise in immigration something changed. New players entered the game, noticed how good it was and were willing to take bigger risks but lacked the same cultural mores that kept things civilized. They even carried the same game back to their home countries. There was a reason why the Chinese government banned gambling as they can tend to take it too far sometimes.

Buying a property in NZ and especially in the main centres has been a game most Kiwis wanted to play. Looking back now it seems crazy that people didn't buy a house and chose to rent.

No one chooses to rent, they are relegated by financial constraints to do so.

I chose to rent from 1998 to 2002. I thought prices were going down in 1998 which they were but had a bit of trouble buying in 2002 as prices were recovering when my landlord wanted to move back in.

Kim DotCom chose to rent didn't he?

I think it is rather:

No man chooses to buy, they are relegated by wifely constraints to do so.

I chose to rent from 1998 to 2002. I thought prices were going down in 1998 which they were..

As I mentioned in some thread last week, I bought in 1999.

I disagree - many people do choose to rent. It provides a lot of benefits both financially and otherwise.

- Easy to move, not tied down or reliant on the market.

- You can live in a nicer house/location.

- No maintenance costs/insurance/rates/etc....

- Less stress (i.e. need a new roof - that's the landlords problem)

- Social aspect (i.e. flatting with other people).

It will be different for everyone.

Our new found "wealth " is like "Scotch Mist "

Its time to regulate the banks , ( to protect them from themselves) They are lending against the increase in so called "equity" in exiting properties that can evaporate...........just like mist .

Those borrowing to fund more houses or their lifestyles are at huge risk if things turn .

spot on bring on loan to rental income ratios of 4-1 and see how things cool down.

at what interest rate?

There are always a lot of doom and gloom posters on here. I always wonder how many of you predicting a crash are investors and how many of you predicting a crash are just hoping for one so you can afford to buy? In the long term I believe Auckland will always go up apart from the odd dip here and there. Compare Auckland to the rest of the cities in the world and we really do live in a magical place. Our property is cheap in comparison to what you can get in places like London, New York and Hong Kong. As long as you can keep up the repayments, you can't really go too wrong. I predict that prices may drop a bit or flatten out next year as it looks like we may be in for another global recession in 2017. After that there will be another boom.

Have you compared the average income of an Aucklander vs. the people living in the areas of London/New York/Hong Kong that you are comparing to?

The incomes in these areas are much higher than in other cities, thus people are willing to pay more to live in these areas. Auckland does not have the average income to support prices similar to these other cities. In the end, it all comes down to what people living in the area can pay (through mortgage or rent), and at the moment it is quite out of balance.

Yes, but i don't think we can go on that model any more. Things have changed with far more international buyers in the market, new migrants, expats returning, no child professionals purchasing, Baby boomer investors, more group purchasers to get into the market and so forth.

" In the long term I believe Auckland will always go up apart from the odd dip here and there."

I agree in principle, I think a ~4% annual increase is reasonable to assume in the long term, when going off a "normal" house price base. However, the past 4 years of 15-20% increases have thrown this trend out and, in my opinion, will need a correction / long period of flat prices / a combination of the two in order to get this long-term trend back on track.

I am not an investor, so you can argue that I am biased in my thinking. However, I am just looking at the market fundamentals and they all point to the market being grossly overinflated. It is a combination of a flight to yield (lots of cheap credit with not many places to invest it), along with both the wealth effect (my house is worth more and I've gone down to 70% LVR, I'll sell it and upgrade and reset back to 80% LVR) and the fear of missing out.

So you're happy to predict a global recession for 2017 but to infinity and beyond for Auckland housing?

This is why I grow more confident by the month, that we in the midst of a giant property bubble - such over confidence in continued growth in property which is truly unsustainable. I fear that Auckland home owners and investor/landlords are baffling themselves with their own BS.

I'm not happy about predicting a recession but I think there is a high possibility that one is going to happen based on all of the warning signs out there. Things go in cycles and if you look at the past 20 years you will see what has happened so far in the Auckland market. With the rest of the world turning to crap, Auckland will continue to go up. Not sure if you have traveled much but we really have it good down here in comparison to many other international cities.

Why would Auckland be immune to a global recession?

This would impact the bank's access to funding (meaning less credit to fuel growth and a lot higher interest rates), less people purchasing our exports (our biggest GDP driver), job losses as a lot of companies in NZ are global companies (which would also affect a lot of peoples ability to service their mortgages), people will get worried about the future so will spend less (meaning growth will drop). These are just the few I could think off of the top of my head.

And if you think houses will keep increasing beyond 9-1 loan to income ratio, including in a global recession, I am quite worried about who out there is investing and what they are basing their investment decisions on.

I never said Auckland would be immune to a global recession? and I don't think prices will be booming in a recession either. Prices may flatten or dip in a recession but when things recover they may boom again.

Renters are hung up on the whole Ponzi scheme thing. So glad I wasn't reading any of this when I bought a house 10 years ago. Kept all the emotional stuff out of the decision, it was straight math, pay an extra $150 a week and buy a house instead of renting. Never looked back since, best decision I have ever made. House prices may have gone up but interest rates have also halved and it looks like they are going to stay low for a while.

So you bought 3 maybe 4 times. Today at least 10 times in Auckland. That is a lot of principal to find each month. I presume you have no kids or grandkids as you are clearly not thinking about them if you have.

I want Auckland to be expensive so that it can be exclusive. When the people who were once in the poor suburbs realise that their houses are now very valuable they will look after them better. Maybe pick up the rubbish on the street like I do. Keep the front verges nice. This is my vision for the whole of Auckland. I kind of drifted away from it for a while but now I'm back with a vengeance. Gentrify the whole of Auckland. It's going to be a better place for the grandkids.

Are you a street sweeper? Do you vacum up rubbish?

10 years ago? Just before the GFC? wow. I'm in awe.....of your ignorance

How much equity do you have in your place since then? Carlos has made out like a bandit.

Carlos67, apparently these jokers have been on this site for years singing the same old tune. Some people probably did take their advice five years ago.

Something is seriously wacko!

We've got new money (debt) rising at $25,000,000,000 in the past year (around 11% of GDP) from private sector alone plus whatever the government sectors are borrowing. Our economy is showing zero per capita GDP growth and near zero inflation.

How can the RBNZ, Treasury and "our" government or our creditors be happy about this? Haven't we learned our lesson from 8 years ago?

It's great isn't it. I'm just waiting for someone to declare it to be new economics.

http://www.telegraph.co.uk/business/2016/05/02/bank-of-mum-and-dad-is-h…

Solvent. Ma n Pa may not save you...Even in British Pounds.

Cheapskates cannot even meet their kids obligations....and a lot less than ours.

The housing crisis in the U.K. is due to out of control inward migration. It's that simple.

Which is lower per capita than NZ... ?

21st time ... STAMP DUTY on existing home purchases by investors is required. (2nd homes and homes bought via a company/trust).

Only solution that will change the investors current patterns of pushing up the prices and push them towards where they are needed ie New house supply.

80% of homes in some areas being bought by Investors is a tragedy and just shows you what a mess it is in. Make our Houses our Homes again. Houses should not be a commodity for investors to speculate on at the expense of the economy and FHBs.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.