BNZ economists have changed their call and are now picking an official interest rate hike as soon as early next year.

And the economists say in the latest BNZ Markets Outlook publication that the Reserve Bank will be "negligent" if it does not express "an explicit expression of rate increase(s)" in its projected forward track of the Official Cash Rate when it reviews the OCR this week in its latest Monetary Policy Statement.

BNZ head of research Stephen Toplis says there is "no excuse" for the OCR to be at "just" the 1.75% level it is currently on - "but odds are the Reserve Bank will find one when it delivers its May 11, Monetary Policy Statement".

"As we see it: inflation expectations are elevated and rising; growth is at or above trend; capacity constraints are intensifying; headline and core inflation are around the mid-point of the Reserve Bank’s target band; the currency is proving to be weaker than anticipated; and commodity prices are pushing New Zealand’s Terms of Trade to near record levels. All of this argues for the cash rate to be a lot closer to neutral than where it currently is."

Toplis points out that the last time inflation expectations were at their current level the OCR was actually at 3.5%.

"Of course, one of the main reasons that inflation expectations are rising is because headline inflation has pushed significantly higher. Having been near zero for quite some time, headline inflation has now jumped to 2.2% on an annual basis. The rise to (and through) the mid-point of the RBNZ’s target band has occurred two years earlier than the RBNZ had expected.

"Sure, there are a few one-offs driving the jump last quarter but we still believe inflation has not yet peaked and that it won’t drop below 2.0% until 2019 (and that only with the help of higher interest rates)," Toplis says.

He believes that taking various factors into consideration, "we not only believe the RBNZ will have to formally move to a tightening bias but we also believe that it will, eventually, be forced into moving rates even earlier than we have previously hypothesised".

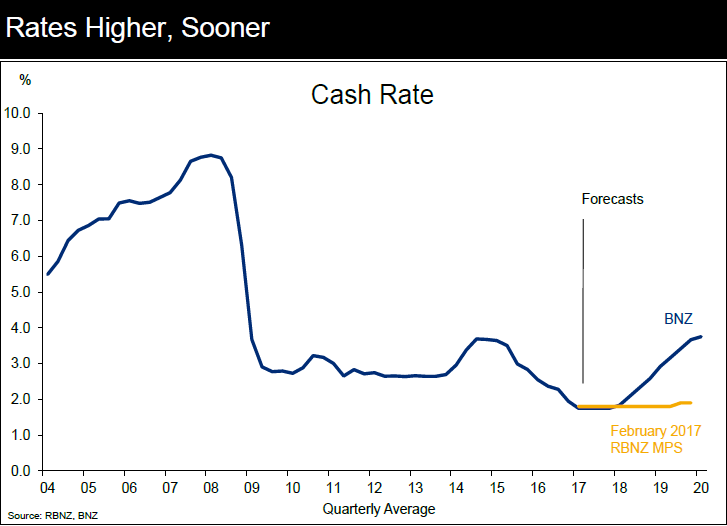

"Accordingly, we are taking this opportunity to move our own projected first tightening from May 2018 to February 2018 even though we doubt the RBNZ will say anything of the sort this time around."

Toplis says that realistically the BNZ economists have "no idea how" the RBNZ will weight its desire to be consistent with its previous statements versus the increasing evidence of rising inflation in the data.

"With no great conviction, we think the Bank will print a track which shows the first rate hike in H2 2018 rising at around 10 basis points a quarter thereafter. And given that the neutral interest rate is likely to be significantly above current levels, even this track would allow the RBNZ to reiterate that 'monetary policy will (still) remain accommodative for a considerable period'."

Toplis says that, Importantly, not only has headline inflation moved to the middle of the RBNZ's 1%-3% target band but core inflation is there too. "Our derived measure, based on the six “core” readings that the RBNZ follows, sits at an annual 1.9%."

And Meanwhile, Toplis says, the pressure on future inflation keeps rising.

"To start with, the NZD Trade Weighted Index (TWI) is currently almost 5.0% below the level the RBNZ assumed it would settle at through the current quarter. Was it to stay here that would add around 0.5% to the RBNZ’s year ahead inflation forecast by itself.

"And elsewhere the pressures continue to rise. Capacity utilisation indicators keep going from strength to strength, the unemployment rate (at 4.9%) is now at or below levels previously considered as inflation-generating, dairy prices are rising and will push the terms of trade back towards record highs and it is highly likely that the upcoming Budget will deliver an easier fiscal policy track than that currently built into RBNZ forecasts."

Toplis concedes that lending rates are already rising as bank funding costs increase and credit growth is also being restricted thanks to a combination of the liability growth difficulties faced by banks, tighter RBNZ controls and the increased cost of capital. And, consequently, the housing market does appear to be softening (at least in Auckland and Christchurch).

"From the RBNZ’s perspective they will also point to ongoing low wage inflation, further uncertainty in the global economy and the transitory nature of some of the recent price “shocks”. This is fair enough [but] we still believe that the potential deflationary impacts that persist seem to be well and truly overshadowed by the inflationary pulses elsewhere.

"Moreover, our general premise is that as all else starts to return to “normal” so too should interest rates."

15 Comments

Opening line:

"BNZ economists have changed their call..."

and they will have to change today's call later on as well

Early next year LOL.

BNZ head of research Stephen Toplis says there is "no excuse" for the OCR to be at "just" the 1.75% level it is currently on - "but odds are the Reserve Bank will find one when it delivers its May 11, Monetary Policy Statement".

"As we see it: inflation expectations are elevated and rising; growth is at or above trend; capacity constraints are intensifying; headline and core inflation are around the mid-point of the Reserve Bank’s target band; the currency is proving to be weaker than anticipated; and commodity prices are pushing New Zealand’s Terms of Trade to near record levels. All of this argues for the cash rate to be a lot closer to neutral than where it currently is."

Hmmmmmmm...

This is, of course, the Phillips Curve where today economists believe in a short run tradeoff between unemployment and consumer price inflation. The theory suggests that as more people go back to work there will be fewer left unemployed on the sidelines, so at some magical point the level of remaining “slack” will diminish such that employers will begin competing for employees. Rising demand against lower supply leads to a rise in the price for labor, or wages. As wages rise, spending power does, too, thus consumer prices are set off.

The central bank must therefore decide, if you believe all this, to get ahead of demand so that when that magical point is reached it doesn’t spiral out of control; in the view of orthodox dogma rapidly rising wages are somehow a bad thing. It places a good deal of importance on figuring out ahead of time the level where recovery stops and slack ends. Since monetary policy “tightening” takes time to work, the FOMC must vote in advance of actually seeing that magic point. [my emphasis] Read more

Irrelevant

The big wide world will place its own pressures on the bureaucratic RB

Their guesses are usually too little or too late or both of these

NZ like everywhere else is deeply in debt & OCR is cosmetic

GFC2 is on the way unless Trump starts WW3 in which case even more debt will be created

You are right. Debt everywhere except for the very wealthy. At least national debt to GDP is low in NZ. Property globally has peaked. I see UK post brexit party is coming to an end. There is a serious imbalance in top end properties in London right now.Teresa May has scared off the non doms with the new inheritance tax rules.

"......And the economists say in the latest BNZ Markets Outlook publication that the Reserve Bank will be "negligent" if it does not express "an explicit expression of rate increase(s)" .....

WOW. Lucky BNZ is not the RBNZ Governor.

If RBNZ raises rates by 10bp BNZ will raise their rates by 25bp within hours sighting some other bs reason. Never pass on the full cut, but always pass on the full increase plus cream.

Head down - I think you'll find that the BNZ were talking about the RBNZ publishing a forecast track in their MPS on Thursday that shows a 10bps move higher each quarter, It's not an explicit forecast as central banks tend to only work in 25bps (occasionally 50bps) lots, but the forecast track is designed to show direction and magnitude.

No doubt there will be some bad loans in the books of banks who have lent to get market share, like maybe ANZ & BNZ (the only 2 I hear wishing for higher rates), and how else to cover the losses than to rely on higher rates / better margins on existing good loans.

Excellent comment! Never looked at it that way.

Uneducated comment really. The economists are independant of the banks interests and are employed to provide information/education and forecasts. If you are too cycnical to believe that, then they should be telling everyone interest rates are going lower.. and to float. Floating margins are massive and where the banks make most of there money on the residential book.. so telling people rates are going higher and to fix in lower margin loans doesnt really make too much sense.

On top of that, while many of the loans made recently may turn out to be bad, the performance of the loan book at the moment across the banks locally is actually very good with very little in the way of imparements (even agri provisions made last year have now been written back).

DP

Why on earth would anyone think that the RB must do something, when the market is already doing it? Deposit rates are increasing, ergo, why increase the OCR?

Dave2

"Why on earth would RB do something"

To appear to be relevant is why

What the RBNZ actually does is slightly irrelevant at the moment as the retail banks are doing the job for them though the rising cost of finance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.