By David Hargreaves

A high-powered report outlining global agricultural prospects for the next 10 years sees only slow improvement in global dairy prices over that period - and no return to the highs of the recent past.

Labour's finance spokesperson Grant Robertson says the report suggests dairy farmers here won't reach breakeven till 2019 at the earliest and says there are serious implications for the dairy sector and economy.

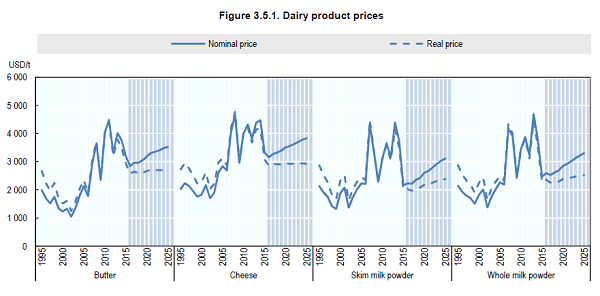

The OECD-FAO Agricultural Outlook 2016-2025 and the accompanying more detailed break-out section on dairy predict that over the next 10 years, it is expected that real dairy product prices "will increase slightly".

"Nevertheless, real prices will remain below average prices of recent years, but substantially higher than in the period before 2007," the report says.

Recent global dairy prices have remained flat at low levels, with the key Wholemilk powder price most recently averaging US$2079 a metric tonne.

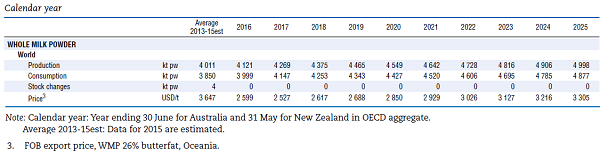

According to the OECD-FAO report, WMP prices averaged US$3647/t through 2013-15 - but the report doesn't see prices getting anywhere near that again in the next 10 years.

The report forecasts the price to hang around in the region of US$2600 till 2019, and gradually moving up to break the US$3000 mark by 2022, as shown in the below graph and abridged table underneath. Bigger versions are available here.

Robertson said that for dairy farmers to break even they need a whole milk powder price of "at least US$2650 a metric tonne" at current exchange rates.

"The OECD’s forecasts push that break-even point back until 2019 at the earliest.

“This has serious implications for the dairy sector and the wider New Zealand economy - dairy’s total direct and indirect contribution to the economy is at about 5 – 6 per cent according to Treasury analysis. Dairy farm debt has risen to close to $40 billion, and represents 10 per cent of bank’s loan books.

“In this scenario farmers will not be in a position to reduce debt anytime soon. In fact they will require significantly more borrowing for a sustained period, which banks may well have concerns about."

Lower for longer

The 'lower for longer' scenario portrayed by the OECD-FAO report squares with some research and projections that have been made in New Zealand too. ANZ economists warned just on a year ago that dairy farmers will get prices for their milk that are 5%-8% lower on an ongoing basis than they have been in the past.

The OECD-FAO report says that world milk production is projected to increase by 177 Mt (23%) by 2025 compared to the base years (2013-15), corresponding to an average grow rate of 1.8% p.a. which is below the 2.0% p.a. witnessed in the last decade.

"The majority of this growth (73%) is anticipated to come from developing countries, in particular India and Pakistan. This expansion of production is largely in fresh dairy products, which will grow at 2.9% p.a. in developing countries, and predominantly supply domestic markets. At the world level, production of the main dairy products (butter, cheese, SMP and WMP) is increasing at similar pace to milk production, albeit more slowly than that of fresh dairy products."

But in contrast, milk output growth is expected to be constrained in New Zealand, the largest milk exporter, compared to the previous decade, with growth slowing from 5.1% p.a. to 2.1% p.a, the report says.

NZ 'influenced by China'

"As the majority exporter of WMP, New Zealand was particularly influenced by China’s sharp decrease in WMP imports leading to decreased producer prices. This, combined with adverse weather conditions and environmental constraints, has led to a reduced production potential. Most of the growth will come from a further increase in the dairy herd (1.6% p.a.) as the mainly pasture-based, extensive milk production system implies a continuation of low yield per dairy cow. Furthermore, due to rising prices for beef meat, non-dairy cattle will compete for land-use in the future."

Per capita demand for dairy products in developing countries is expected to grow consistently over the medium-term, supported by rising incomes and lower dairy prices relative to their 2013 peak.

"As seen in previous years there is a continued shift in dietary patterns away from staples and towards animal products, due to changes in diets. Strong consumption growth is expected across several markets in the Middle East and Asia, including Saudi Arabia, Egypt, Iran and Indonesia, with the per capita consumption of dairy products in developing countries growing between 0.8% and 1.7% p.a., the lowest growth being for cheese and the highest for fresh dairy products. In addition, per capita consumption in the developed world is expected to grow between 0.5% for fresh dairy products and 1.1% p.a. for SMP."

A key uncertainty

In terms of some of the uncertainties, the report says China’s role as a key importer of many traded dairy products is a "key uncertainty" in the future developments of world dairy markets.

"China’s domestic milk production has continued to increase, along with investments in processing capabilities. If China resumes imports at 2014 levels, this would have a significant impact on the markets for milk powders.

"On the other hand, China could become further self-sufficient, supplying much of its demand for dairy products domestically, although current low prices do reduce the attractiveness of investments in dairy processing."

Dairy prices

Select chart tabs

18 Comments

Well there you go, you can't take it with you.

http://i.stuff.co.nz/business/farming/dairy/82319997/Kiwi-farmers-face-…

And see some robust comments at the foot of the item.

Imagine the business of loans are a one (or few) to many structure.

Say 5 loan makers and 3,000 to 8,000 borrowers of varying keen-ness/motivation.

Where, is there, demonstrated artfulness in lending management (and estimating future commodity prices).

We must be of the very few where scale resources/primary debt funding need not have committed price and volume off-take.

Everyone knows the psychology of the cashstrapped borrower (take what they give you).

Mind games indeed.

You have to wonder if conditions in the dairy sector could fall off a cliff sometime in the next 12 months. If so far farmers have gone through a cost cutting phase and then borrowed against their (shrinking) equity, there has to come a time when the banks start to blink, turn the tap off and start selling farms.

It's all very well to have a gentlemen's agreement between banks but once one bank starts selling farms in earnest surely all banks will be forced to do the same.

Would be interesting to hear some anecdotes from farmers.

I believe some of this hoo haa over the residential sector from the rbnz is fear of what is happening in the dairy sector. The only thing they can do to help is drop the OCR. They must get the dollar down. In doing so igniting, no they are in full ignition already...stoking the speculators in property. I dont see getting the dollar down helping that much if this is ongoing for 3 or 4 more years though. I dont have any interesting anecdotes Zombie, but you can see trade is getting hard looking at some of the advertising. Buy a tractor, get a free frontend loader. Cheap motorcycle servicing. RD1 is doing some amazing deals on calfeterias. I noticed an electric fence tester way under $200....usually they sting you for around $220. Sharpened pencils everywhere. I never saw how fieldays did this year. Usually it is paraded through all the news media.

I also dont get this bullshit about getting costs down to $4.00/kg ms.....or whatever $/kg.....first you have to spend the money. Then comes production. Which can be awfully dependent on a few things...weather, fert, luck, good management. Its a pie in the sky figure. Something you can do a cashflow forecast with. But as we all know a forecast is your best guess and is generally quite wrong.

It is only a matter of time before this is front page news again. Somehow this ticking time bomb has been swept under an increasingly bulging carpet by all things Auckland Housing Ponzi.

If this plays out it is a massive failure of forecasting from all manner of" experts", who farmer thought they could believe. Remember Theo calling a bounce to $3500/t by early last year, breathless statements from MPI, John Key, Nathan Guy re "export double" on the back of endless Chinese demand, especially infront of( a grinning) President Xi, any bank economist(take a bow Nathan Penny for award for most wreckless) etc etc. They will all keep their high paying jobs while the people they were guiding will face the consequences.

Haven't been totally convinced about Grant Robertson to date but to his credit he is on record during the last election campaign, at the height of the boom, warning of the pending price collapse. Seems he was one of the few that read the tea leaves. Farmers walking off their farms will not be much of a backdrop for the next election.

Winnie called it first. I remember him talking below $4.00...I thought he was being a bit over the top. I would love to know who was in his ear. He was very vocal that this was gona be really really bad, while the preacher Tim from Rabo was saying it would drop to $7 at worst. Hosking took the cake. His dismissive manor in the face of some pretty dire circumstance. I notice he zipped it when the number of suicides escalated. Actually Key and his Ag minister were probably worse. Theirboundless bullshit new no bounds. All history now. Lets see how and what these people do from here.

JK really starting to piss people off, today he said Auckland house prices reflect how successful NZ has been led under his govt.......LOL

Nathan Penny full of hot air.......hyped up from a seminar with JK

SS - was talking to Rural Support Trust representative recently and they said they are rather busy - with sheep farmers, not dairy farmers. Bankers have also said they are by and large more concerned with sheep farmers than dairy. What are you hearing? The media is all over dairy, but is the non dairy sector in worse shape?

Sheep farmers...or those sheep farmers that also relied on dairy grazing? Unsold winter grazing crops? Or possibly worse...ex dairy grazer borrows expensive money from the likes of Farmlands or wrighties and buys overpriced cattle on a falling market. Loses the monthly cheque and gains a huge OD. Plus a tax problem likely.

A lot of property was bought on the back of that monthly cheque from grazing.

More likely drought. The local scanner has seen a 10% drop in scanning rates in our area, and back in the summer there were a lot of store lambs sold cheap. A dry Spring and Autumn meant lamb growth rates were always going to be crap. Drought tends to eat away at you slowly, and for us down here, it's our second dry year in a row.

The dairy farmers don't have the exposure to climate risk as sheep & beef, so have always taken on more debt. It's just that they can't figure out if it is light at the end of the tunnel, or a ruddy big train coming at them. My money is on the choo choo

Sorry to hear that Bruadar. I was thinking CO was talking bout Southland. Howsit looking now? On our side of the country its starting to look like too much rain.

Much better thanks Belle. We have had a couple of winter rains which has helped to guarantee some spring growth. The effect of the last 2 seasons has been very variable, not in terms of rainfall, but how different farmers have responded. Those who take action early are normally fine, both financially and mentally. Those who try to do the same thing and hope for a different result.... well Einstein called it insanity.

"Strong consumption growth is expected across several markets in the Middle East and Asia, including Saudi Arabia"

But Saudi is making noises about "getting out " (excuse the mad coughing fit) of Oil in the next 10 years ... they are now plundering their foreign reserves to keep the show ticking. They will be broke well before 2025.

My grandfather rode a camel, my father drove a Toyota, I drive a Merc, my son will drive a Toyota and my grandson will ride a camel.

their big problem is that back when your grandfather was on the camel, their population was somewhere in the region of 2mill ... today knocking on 30 mill , all dependent on Oil to buy their imported Food ... it wont end well.

My father drove a Toyota, I drive a Merc, my son will be dragged through the streets by a Toyota.

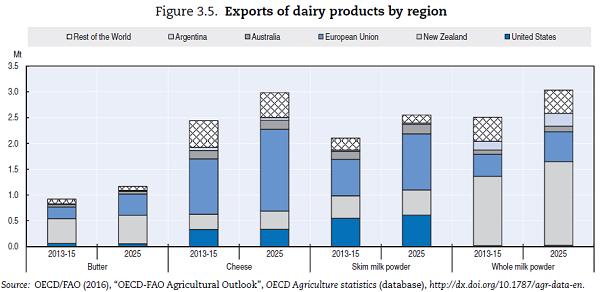

Cool graph. Looks like we are going to DOMINATE on the WMP front by 2025.

All going according to the master plan.

This show Fonterra directors out of touch with reality and living in la la land

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.