Some economists are concerned prudence by the Government could restrict the Reserve Bank (RBNZ) from majorly expanding its quantitative easing (QE) programme.

An indemnity provided by Finance Minister Grant Robertson allows the RBNZ to buy up to 50% of outstanding New Zealand Government Bonds (NZGB) on issue via its $60 billion QE, or Large-Scale Asset Purchase programme.

The thinking is, if the RBNZ buys a higher portion of bonds, this could distort the market.

But what happens if the Government doesn’t commit to spending as much, and thus issuing as many NZGBs as the RBNZ expected it would, and the RBNZ reaches that 50% limit when it still wants to do more bond-buying?

ASB economists Mike Jones and Mark Smith said there was a “near-term risk” that with the economy now doing better than expected a few months ago, the Government wouldn’t issue as much debt.

Westpac economist Dominick Stephens made the same observation, noting that Finance Minister Grant Robertson last month said he was putting away $14b of the $20b allocated in the May Budget towards yet-to-be-determined Covid-related expenditure.

Stephens expected Treasury’s Debt Management Office to reduce its forecast bond issuance programme to $50b (from $60b) this year, and to $35b (from $40b) next year.

Even though the rate at which the RBNZ has been buying NZGBs has slowed, Stephens forecast it owning 54% of the bonds on issue by 2022.

ANZ’s Liz Kendall and David Croy made similar comments, adding it created uncertainty having a cap defined as a value of outstanding bonds on issue, when it wasn’t clear what this was going to be.

“If bond issuance is expected to be lower, then a percentage cap is more likely to become binding, and sooner,” they said.

The limits of buying NZGBs

While all three banks’ economists agreed this was a potential issue, their views differed on how the RBNZ would respond.

Kendall and Croy said the indemnity needed to be made more flexible, or increased to 60%.

This would ensure the QE programme delivered its “maximum stimulus” while dealing with “market perceptions” it could hit its limit.

They maintained it would be more risky and costly for the RBNZ to try to reach its inflation and employment targets using the other monetary policy tools available to it.

However, ASB’s Jones and Smith couldn’t see the RBNZ asking Robertson to lift the indemnity “anytime soon”, saying: “Bank staff have frequently expressed a view that they don’t wish to own more than 50% of the government bond market. To do so would impair market functioning and liquidity and also exceed where some offshore central banks have got to with their QE programmes.”

Meanwhile Westpac’s Stephens believed the RBNZ would turn to cutting the Official Cash Rate (OCR) from 0.25% to -0.5% in April next year.

The RBNZ’s Monetary Policy Committee is on Wednesday expected to expand its QE programme and provide more of a steer on its thinking, when it releases its quarterly Monetary Policy Statement.

The RBNZ has committed to buying up to $60b of mostly NZGBs over a year (by May 2021). In the past four-and-a-half months, it’s bought $23b of NZGBs and $1b of Local Government Funding Agency Bonds.

‘Economic adjustment will be a marathon not a sprint’

While economists’ views differed on how the RBNZ would respond to QE reaching its limits, there was also some disagreement on how bad New Zealand’s economic outlook was.

ANZ’s Kendall and Croy expected the RBNZ to expand the QE programme to $90b over 18 months.

“Even in a best-case scenario, inflation and unemployment look set to be away from the RBNZ’s targets for an extended period, necessitating very expansionary policy to see these return within an acceptable timeframe,” they said.

“The path of least regrets is to err towards doing more, given downside risks and the possibility that inflation expectations settle too low. The chances of doing too much and causing a growth and inflation overshoot look remote in the near term, and worth the risk, given the ability to reverse course if required.”

Furthermore, they said: Shifting the timing of the programme out to 18 months will help with the prospect of a QE ‘cliff’, which is becoming a concern for markets. With purchases due to end in 12 months, the question is: what happens next?”

ASB’s Smith and Jones, and Westpac’s Stephens likewise believed the RBNZ would extend the timeframe.

Stephens saw the cap being extended to $70b over 15 months, while Smith and Jones put it at $80b over an unspecified extended timeframe.

Smith and Jones were more upbeat on the economy than Kendall and Croy, saying, the RBNZ had time on its side, as QE had been successful to date.

“But the economic adjustment will be a marathon not a sprint. NZ’s recent economic performance has certainly been encouraging, but the RBNZ may yet be called upon to do more,” they said.

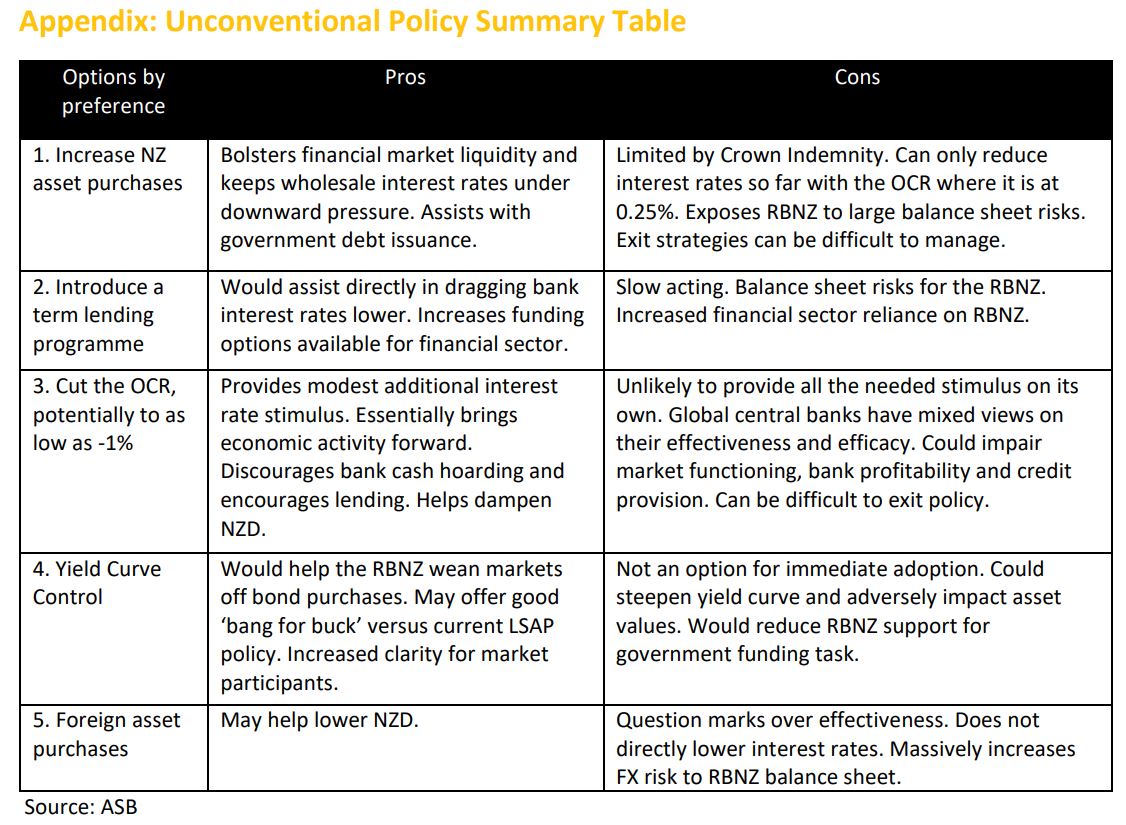

They provided this table detailing the pros and cons of the tools at the RBNZ’s disposal:

25 Comments

The first sentence reads like satire. Monetary policy has become a theatre of the absurd.

Looks like economists have been reading the The Onion a little too often https://www.theonion.com/tag/economy

And then we get comments from Smith and Jones! (That's any number of satire based shows)

Considering that the comments are coming from private bank economists, are these banks expressing concern that the amount of profits they can make might be limited if the government doesn't throw money at the economy willy nilly? These are private interests trying to direct Government policy, and influence RBNZ actions (which I guess they've always done).

In reality the RBNZ and the Government should only be concerned as to the effect of that money they have pumped into the economy. something I am not confident they are able to do effectively as they are pointedly ignoring the out of control inflation in housing that has occurred over the last 15 or so years, and is still continuing, making housing unaffordable for most ordinary Kiwis.

In reality the RBNZ and the Government should only be concerned as to the effect of that money they have pumped into the economy. something I am not confident they are able to do effectively as they are pointedly ignoring the out of control inflation in housing that has occurred over the last 15 or so years, and is still continuing, making housing unaffordable for most ordinary Kiwis.

No. The commercial banks lent money into existence for the housing bubble. Not the RBNZ or the govt. They're kind of an unknown part of the triumvirate. Without them, there's no conduit to the common man, unless we all open a personal account with the central bank.

Indeed, although the RBNZ is the major enabler of the housing price bubble by its misguided interest rate policy over the decades. If the interest rate had been just 0.25% higher over the last thirty years, would house prices be so inflated?

What I don't understand is why employment and interest rates are being portrayed as solely the RBNZ's responsibility; when in fact employment, interest rates and productivity are major responsibilities of the whole jumbled and unaccountable government bureaucracy.

"No. The commercial banks lent money into existence for the housing bubble." my point exactly. The fact that the Government and the RBNZ didn't/couldn't see this and didn't act to control it is also my point. Roger's comment below about how a small interest rate alteration could have delivered a better result is one possible thing that could have happened. it seems we continue to be Governed by people who don't want to do their job properly.

Abolish the bias of the low capital RWA regime that applies to residential property bank assets. Then banks could possibly be deterred from extending ~60% of their lending to this asset class for one third of creditworthy households to favour GDP qualifying endeavours associated with productive enterprise.

{kind=link}

This would ensure the QE programme delivered its “maximum stimulus” while dealing with “market perceptions” it could hit its limit.

"Stimulate" what? - the government has issued ~$30 billion net new debt, over the last four months, which has been monetised by banks and other savers. Deficit spending guarantees it will find it's way into the bank deposit system via transfer payments as and when it's needed. OCR is at 25bps which to me indicates tight monetary conditions. QE will only compound this situation, if it's efficacy is questioned by the constant need to extend and repeat it without the evidence of growth that drives deflation out of the system and delivers the consequent prospect of higher interest rates on the horizon.

{kind=link}

Do you expect central banks to allow "catch up" inflation if and when they manage to create some?

If only and at what price?

Evans introduced symmetry in his remarks, couching it in the context of monetary policy targets. It’s progress only in the sense that after ten years it shows the Fed, or at least certain officials within the institution, are capable of seeing reality (again, which shows just how contaminated the institution has become)

The Chicago Fed President apparently stressed that 2% “is a symmetric goal for inflation, not a ceiling.” That brings his thinking more in line with a price target, or at least a price level target. The difference from an inflation target is that symmetry, or in the context of underperforming for so long making an attempt to reconcile with that past underperformance (instead of running away from it). You can’t just ignore an economy that doesn’t get back up.

As you can see plainly above, if the US economy was to suddenly achieve sustained 2% inflation from this month forward, it would still leave consumer prices with a considerable gap from where they “should” have been had the economy been operating normally in recovery. Time is one factor on both sides; in that it has been more than long enough that if it was going to it would have by now; and on the other side the longer it has been left to decay like this the worse it gets for all involved (and the harder to get out).

We can’t get too hung up on the fact that the central bank wants to harm consumers at the worst possible time, that’s just their methodology of working through money to economy. In this case it’s actually progress because again they are being forced to recognize that inflation is behind, bringing them closer to the realization that it’s not just consumer prices that are desperately lagging (and then the big one, why that is).

Symmetry in the form of a price target would look far different. To close the price gap in two year would require 4.2% annual inflation in both years. The longer the Fed waits to try and force that, the greater the inflation required to bring prices up to where they “should” be. As inflation goes up to that level, so too, theoretically, would economic growth in at least nominal terms – the very thing that is missing. It’s a far different proposition than the current official consensus of “full employment” implying no output gap at all.

{kind=link}

Don't follow. You mean that you don't think they can generate any?

Not at the moment - furthermore, it's not within their capacity to do so under current arrangements.

Weren’t ‘Smith and Jones’ a couple of comedians from the 90’s? As for Stephens well he’s always been a comedian with his constant flip-flopping forecasts!

One giant cauldron of "least regrets", reduce the OCR, throw in a little LSAP , a bit of TAF, mix in a wage subsidy and mortgage deferral, add COMO, a liittle more QE and some BMLS , stir and add TLF , a little MD a bit more mortgage deferral, some SBCFLS.

I note the TWI under the May baseline forecast scenario, and the view of the RBNZ that there would be downward pressure on the NZD, towards a TWI of 66.3 , after introducing the LSAP programme the TWI has actually risen from the most recent MPS, at the expense of exports, which in the view of the RBNZ would have benefited from a lower TWI, and now sits around 72.

Is their any theory out there on a positive stimulative effect form an increase in the central bank QE balance while the bonds available to private holders remains the same? The supplied reason of “market perceptions” meaning the higher the balance, the more perception of stimulus thus more spending must be questionable.

My interpretation of this is, banks (feeling entitled to their own survival at the taxpayers expense) demanding more pubic spending.

Wow. This clearly shows why the tax base need changing. TOPs policy would generate guaranteed govt income, reduce asset prices, disincent never ending debt, and promote productive activity (working - business start up etc) vs idle debt speculation. Everything would be forced to be priced at a reasonable yield to pay it tax vs endless free capital gain chasing. Summary mass wins for almost everyone, except bank profits (to foreign owners), and specuvestors.

Note: investors generating reasonable risk/yield balance will be fine. FHBs new tax would be offset by major drop in income tax so no big change. Long term they will be better off.

Make sure you vote.

I'd argue it's also much better for banks in the long run, as they otherwise will end up overexposed to speculative asset bubbles ad infinitum.

I do not see income tax rates meaningfully changing under any government and any circumstances. So if it is tax on assets, it will be additional to the income tax, not their alternative.

I am also at a puzzle why people are so obsessed with "optimal" use of assets with punishing failure to optimally use it. Under such scenario all assets will end up at the hands of a very very few as the cost of failure is so high for the majority (except for the very wealthy few).

Is 'majorly' a word. I think it's in the same lexicon as 'bigly'.

"Sounds perfectly cromulent to me." Don't forget that expanding ones vocab embiggens one.

These 'economists' are literally employed by banks and just lobby the RBNZ. Sounds objective to me.

I would have thought that the issue is that the banks are currently risk averse and that businesses are having problems accessing credit that would have no problem doing so in normal times.

Expanding the Bank of IRD lending program is what I would do to fix the situation. Covid is back and access to credit will be needed, for a majority of businesses not just the top tier.

Satire meets real life and blurs in with it. The opposite of prudence is stupidity, which a number of these economists are preaching. No surprises there. One would think they could observe what is happening in other parts of the world, and possibly learn from their experiences with QE. Who would have thought Grant Robertson would find so many economists that he is more sensible than?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.