By Gareth Vaughan

The decisions by the Australian parents of New Zealand's big four banks to retain between 11 and 15 basis points of this week's Reserve Bank of Australia (RBA) cash rate cut will boost their margins by between 3 and 5 basis points, and their earnings by between 2% and 3%, according to analysts at Macquarie Securities.

After the RBA cut the cash rate by 25 basis points to a fresh record low of 1.50% on Tuesday, ASB's parent Commonwealth Bank of Australia, ANZ, BNZ's parent National Australia Bank and Westpac cut their standard variable, or floating, mortgage rates by between 10 and 14 basis points. As Macquarie puts it, this means the four "announced 11-15 basis points [of] repricing."

"We see this as a positive earnings catalyst for the sector and estimate that it provides 3-5 basis points to banks' margins and 2-3% to their earnings," says Macquarie.

Or as The Australian Financial Review's Chanticleer column noted; "Australia's big four banks have shown their determination to hang on to their high return on equity for as long as possible with their half-hearted pass through to mortgage borrowers of the Reserve Bank of Australia's 25 basis point rate cut. As interest rates fall the banks will continue to hold back as much as possible of the lower official rates from mortgage borrowers in order to protect their net interest margins."

Although the big four banks were much more friendly towards savers, with term deposit increases for terms ranging from eight months to three years of between 45 and 85 basis points, expectations are much of this will be clawed back, as happened earlier this year after similar moves following the RBA's May cash rate cut. Indeed the Macquarie analysts note the deposit rate increases are "likely to be unwound over time with limited impact on profitability." Competition among Australia banks for deposits is, however, expected to be strong in the lead up to the implementation of the Net Stable Funding Ratio, which is similar to NZ banks' Core Funding Ratio requirements, in 2018.

So what will NZ banks do next week?

With the Reserve Bank of New Zealand widely expected to cut the Official Cash Rate by 25 basis points next Thursday, August 11 to 2%, this begs the question as to how much local banks will pass on to borrowers, and what changes will there be for savers?

As we reported earlier this week, ANZ's economists are suggesting borrowers should not expect to see their mortgage rates drop 25 basis points. This argument was made in ANZ's weekly Market Focus report. It was also set out in ANZ's NZ Property Focus report last week as below;

"While the RBNZ is set to cut the OCR again, we doubt the full 25bps will be passed on. Credit growth is outpacing deposit growth, a partial by-product of lower interest rates. Any shortfall needs to either be funded offshore (which is more expensive) or by shifting relative pricing, which means competing more aggressively for deposits and slowing credit growth. Banks’ cost of funds continues to rise. Deposit rates are now into the territory where further reductions would negatively impact already falling deposit growth rates. For money to be going out the door (lending), it needs to be coming in as well, and continued falls in deposit rates is incongruous with that. So we appear to be approaching a point where borrowers will not get the full benefit of OCR cuts, but depositors will not receive the full pain either, and in fact may benefit if competition heats up."

ANZ likely to set the tone

ANZ, comfortably NZ's biggest bank, is generally the first major bank - if not the first bank fullstop - to react to Reserve Bank OCR changes. ANZ thus often sets the tone for those who follow. This is what happened in March when the Reserve Bank last cut the OCR. Then ANZ cut its floating mortgage rate by just 10 basis points. BNZ and Westpac also subsequently cut by just 10 basis points, while ASB and Kiwibank cut by 20 basis points.

The miserly cuts came even though Reserve Bank Governor Graeme Wheeler said he expected the full 25 basis points cut to be passed on to floating mortgage rates. The only bank in March to cut its floating mortgage rate by 25 basis points was the 100% retail funded The Co-operative Bank. Its CEO Bruce McLachlan said at the time there was no case to not pass on the full 25 basis points OCR cut to floating mortgage rate customers, and those borrowers shouldn't have to pay for pressure on bank margins elsewhere.

In March banks cut savings rates, with greater purpose than mortgage rates in some cases, whilst some dragged their heels in terms of passing on lower mortgage rates to hard pressed farmers.

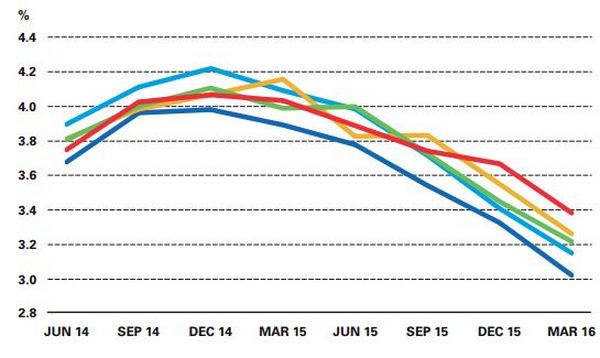

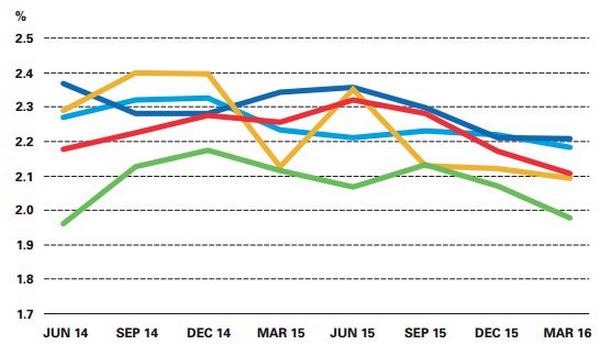

Meanwhile, the latest quarterly KPMG Financial Institutions Performance Survey, out last week, shows - in the charts below - that whilst the major banks' net interest margins have been slipping, their funding costs have been falling faster.

Major banks' average cost of funding

Major banks' interest margin

*This is an abridged version of a longer article that ran in our email for paying subscribers. See here for more details and how to subscribe.

30 Comments

The .25% is being seen as a done deal. As I have previously stated I am going with the idea that we will see a .5% cut.

Not a chance. Wheeler just doesn't operate like that. It will be 0.25%% and it will do little or nothing to lower the dollar. The RBA and the BOE have just cut rates by that amount,so the RBNZ will just be playing catch up,again. There should be a marginal fall in the rate against the US$, but no more.

dp

Why ?

"While the RBNZ is set to cut the OCR again, we doubt the full 25bps will be passed on. Credit growth is outpacing deposit growth, a partial by-product of lower interest rates. Any shortfall needs to either be funded offshore (which is more expensive) or by shifting relative pricing, which means competing more aggressively for deposits and slowing credit growth. Banks’ cost of funds continues to rise. Deposit rates are now into the territory where further reductions would negatively impact already falling deposit growth rates. For money to be going out the door (lending), it needs to be coming in as well, and continued falls in deposit rates is incongruous with that. So we appear to be approaching a point where borrowers will not get the full benefit of OCR cuts, but depositors will not receive the full pain either, and in fact may benefit if competition heats up."

Please point to evidence beyond RBNZ tables S6(bank funding) and S7(bank claims), after mutliplying claims by 21% (foreign funding) and adding this back to S6, where there is substantive evidence of a claims/ funding mismatch.

I think that's the authors point - the 21% foreign funding share is needing to increase at higher proportions. RBNZ table shows funding up $20.5b YoY while claims up $29b. Includes housing +$18b while household funding up less than $13b. That's a decent sized gap because people chasing yield or capital gains aren't depositing funds.

So you're saying the figures point to an on-shore shortfall in funding by the banks. That is, mums and dads are not putting enough deposits with the banks to cover lending growth. Therefore the requirements of offshore funding are growing.

If that's the case, then shouldn't banks be keen to attract more on-shore deposits which must be cheaper than going offshore. Continuing to lower NZ savings rates certainly won't be helping this position.

Not to mention that NZ domestic depositors are the ones most at risk from any future bank stability issues - with the unique approach by the RBNZ with their OBR which will directly penalize NZ depositors rather than the overseas parent banks. This risk is not covered at all with current deposit rates - much less with future lowered deposit interest.

I suspect it’s correct that yield chasers are increasingly moving away from bank deposits. And interesting that Westpacs latest cash raising wasn’t swamped with interest, although risk no doubt a factor for many on that one. In many years of investing my portfolio fixed interest ratio has never been so low. The many doomsters on this site will point out the blood red sky portending my coming doom but lots of people who depend on interest income are being squeezed by falling rates. I think bank deposits will become increasingly less popular with potentially interesting implications for bank funding costs.

Remember also not only do we have the OBR here (which is not in Australia), but Australian depositors also have deposit insurance cover for deposits up to $250,000. Does that mean then that if an Australian bank fails in NZ, the NZ depositors will be propping up the Aussie depositors? Looks like a win win situation for Australian depositors if this is the case. Banks are definitely not paying enough interest to depositors in this country to cater for the risks they are exposed to.

Just like fuel companies quick to up price,slow to cut.

Its the free market Capitalist system , and unless a better system comes along, we should just tolerate it .

Said like a true boomer

Sigh... Yawn...

there is no free market - otherwise why do we need (& now depend on) stimulus packages & money printing? The central banks abandoned free market long ago to prop up shares and asset values in an effort to keep commodity producers afloat.... But its not going to hold indefinitely. At this point we will be back to a free market and it will look really ugly.

Nothing is going to just "come along" we actually make stuff like this happen, there are grass roots movements all round the world. We have it here, just not organised enough.

Come on Boatman, you surprise me!

Tolerate bad weather, tolerate bad neighbours, tolerate beating up-wind, but tolerate getting ripped off?

Might as well roll over the barrel, voluntarily!

ham n eggs,

You are right that there is no free market and indeed,there never has been. All markets need rules to operate efficiently and for the benefit of all parties. Unfortunately, powerful vested interests have been increasingly successful in having the rules shaped to benefit only the few at the expense of the many.

A few figures can help illustrate this. In 2013, Apple spent US$3.40m on lobbyists, Amazon $3.50m, Facebook $6.40m Microsoft $10.50m and Google $15.80m. Source: Center for Responsive Politics.

Wall st. firms make very large payments to political parties, as do the drug and seed companies. They are in effect, rigging the market in their favour, but of course, they want there to be rules to stop others from undermining them. I could go on at length on this, with many more examples of corporate greed and outright malfeasance.

I suggest you look up the meaning of capitalist and facist. I think you will find elements of facism exist in this "system".

Wouldn't banks not passing on cuts be a good thing? Less bubble inflation and getting the NZ dollar down for exporters?

The banks are bastards - they are so far up each other it's unbelievable:

http://blog.creditcardcompare.com.au/big-four-ownership.php

Now, now... Big Blue, you're being unkind to the poor bastards of the world.

Bankers, RE Agents, Politicians, - same animal, just different suits, all lower than whale manure.

They make car salesmen look good.

It means the fat Bankers will get fatter - end of. The full reduction will never be passed on to the consumer. They actually salivate each time the OCR is cut, because ultimately each time this happens their profit margins increase.

End of.

If dividend levels are the definitive indicator, bank profit margins are not hugely different to other corporate sectors. The graphs show that interest margin varies across banks, indicating competition exists (assuming efficiency is similar).

Unfortunately the less astute mortgage borrowers (for which it would apply to the significant majority) become complacent and "comfortable" once they have had their mortgage approved, and dont regularly review or manage their mortgage position as effectively as they could be. People need to be more proactive with their mortgages and to look at the alternative options available to them, and if necessary walk if they can get a better deal, but hey its human nature to take the easy way out.

It would be great of all savers of a single bank removed all their savings from it, due to the low interest rates. That would cause them to panic, and there may then be some competition in the savings market. currently people are moving their money out of the bank and putting it into shares, causing huge increase in share prices. But that bubble could burst. So this decrease in interest rates by the reserve bank are potentially going to cause a lot of people to lose money, as they are forced to seek higher returns elsewhere. It is a repeating cycle, as it happened during the last financial crisis with the finance companies.

If they are still having to reduce interest rates, doesn't this just prove that NZs economy is doing very poorly, and it is being artificially pumped up by the huge immigration flows into NZ. As a result NZers are suffering by not being able to buy lower priced housing. Instead they are able to get cheaper money, in order to pay more for higher priced houses, which may come back and bite them in the future if interest rates go back up. If they reduce immigration numbers, then the numbers are going to look worse, which is why they are not wanting to do this. It all just sees like a house of cards. Also why is housing omitted from inflation numbers, when it is housing that currently has huge inflation. If it was included in the inflation figures, they probably wouldn't be able to reduce interest rates as inflation will be outside the range.

.

Meanwhile over the ditch: Why would banks raise their deposit rates as the central bank cuts its rates? In other words, why would banks raise their cost of funds (deposit rates) while lowering their revenues (lending rates), thus crushing their spreads – and thus their profit margins? Among the big four banks, the movements were nearly panicky:

Maybe they're trying to suck in cash for a bail in?

CBA will raise its one-year term deposit rate by 0.55 percentage points to 3% and its two-year and three-year deposit rates by 0.50 percentage points to 3.1% and 3.2% respectively, effective August 19.

NAB will raise its eight-month term deposit rate by 0.85 percentage points to 2.9%!

ANZ will raise its one-year advanced notice term deposit rate by 0.60 percentage points to 3% and its two-year advanced notice term deposit rate by 0.75 percentage points to 3.2%.

Westpac will raise its one-year term deposit rates by 0.55 percentage points to 3%, its two-year deposit rate by 0.45 percentage points to 3.1%, and three-year deposit rate by 0.55 percentage points to 3.2%.

http://wolfstreet.com/2016/08/04/australia-big-four-banks-housing-bubbl…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.