The consistent and central theme of this FX commentary column over recent months is that the NZD/USD exchange rate would recover its losses and return to the 0.6600/0.6700 area on the back of a weaker US dollar as a result of lower US interest rates.

The view was based on the fact that the US would be cutting their interest rates through the second half of 2019, whereas as other economies such as Australia and New Zealand would be holding off to see the impact of their earlier interest rate cuts.

The US Federal Reserve have indeed reduced their interest rates in July and again in this month. However, rather surprisingly this has not resulted in the USD weakening against the major currencies (as yet). Therefore, the NZD/USD rate has not had the opportunity to make gains and seems to be under constant downward pressure from speculative selling, reaching new lows of 0.6260 last week.

The global currency markets seem to be continually disappointed that the Federal Reserve are not providing clear future guidance that they will continue to decease their interest rates going forward.

In July, the Fed’s message to the markets was that the 0.25% reduction in interest rates was a “mid-cycle adjustment”, the markets interpreted that as “one, and done” i.e. no further cuts.

Fast forward to September and the Fed has cut rates again, being exactly what the markets were seeking as guidance in July but did not receive at the time.

There was no clear guidance on future cuts from the Fed last week as the Governors seems split with seven in favour and five against.

The US dollar has not weakened at all from a 0.50% decrease in US interest rates over the last three months.

The Fed are highly likely to cut rates again by another 0.25% when they meet next on 29 and 30 October.

They will need to witness weaker US economic data, particularly employment trends to justify another cut.

My view is that the industrial and manufacturing downturn in the US economy over recent months (due to the China/US trade wars) will now feed into the employment and consumer spending parts of the US economy. The monthly Non-Farm Payroll jobs numbers have been lower than forecast over recent months and that trend looks set to continue.

At some point the FX markets will recognise that the Federal Reserve is delivering lower US interest rates, despite a reluctance to signal in advance any intention to do so.

Look for US housing, consumer confidence and PCE inflation data over this next week to reinforce expectations that the Fed will cut again in late October.

The EUR/USD exchange rate has returned to $1.1000 from $1.1150 as Middle East tensions with Iran flaring up gain and the markets have not been provided the certainty of future US interest rate cuts they have been seeking.

Kiwi dollar depreciates well below RBNZ base case

An aggressive speculative seller of the Kiwi dollar over recent weeks appears to be placing a large bet that the RBNZ will decrease interest rates again when the Monetary Policy Statement is released on 25 September.

There is certainly not any evidence that the New Zealand economy has suddenly deteriorated in performance or outlook since the surprise RBNZ 0.50% cut on 7 August.

What has changed since early August is a significant depreciation of the Kiwi dollar, particularly against the AUD and USD.

As a consequence, the overall Trade Weighted Index value has fallen away from 73.0 in July below 70.0 today (a 4% depreciation).

In their August statement the RBNZ based their GDP growth and inflation forecasts off a TWI value remaining between 72.8 and 73.4 over the next 12 months.

The much lower currency value now prevailing should force the RBNZ to revise both their GDP growth and inflation forecasts for the next 12 months significantly upwards.

It will be interesting to see if their economic model does deliver this upward adjustment.

The FX market response to the RBNZ 0.50% rate cut has been much more negative than the RBNZ anticipated.

The short-sold NZD speculator may be sorely disappointed when the RBNZ fails to deliver a universally bearish outlook with further interest rates cuts signalled this week.

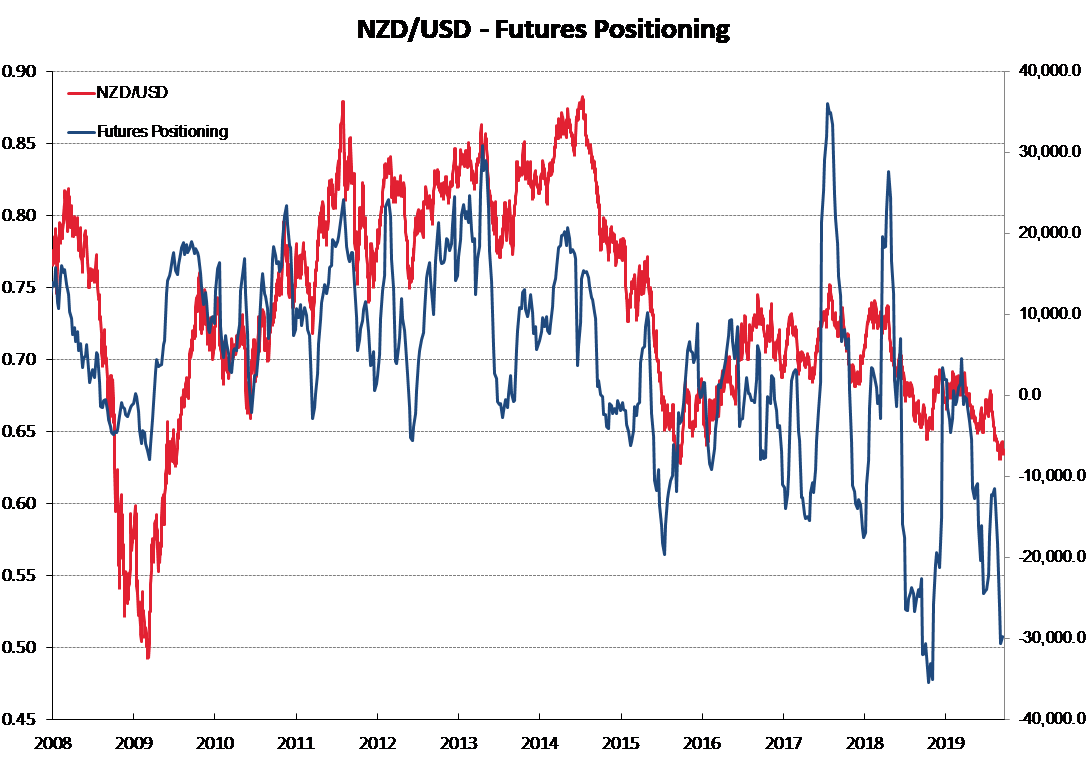

Speculative positioning in the Kiwi dollar has returned to extreme “short-sold” levels again (refer chart below).

History tells us that it is unlikely that the level of short-sold positions will increase any further from here. More probable is a reduction in positions i.e. NZD buying as speculators unwind short-sold positions.

Over the last 12 months, the majority of local economic forecasters have continually predicted “major headwinds” and “challenging trading conditions” ahead for the NZ economy.

There almost seems to be a competition as to who can come up with the most negative outlook of how the economy is faltering and facing a major downturn.

The facts are somewhat different to the picture painted by the doom-merchants, as the economy has held up really well with 2.1% GDP annual growth to 30 June 2019 over a period of extreme global economic uncertainty with the China/US trade wars.

Relative to other economies around the world, the NZ economy has performed admirably through this period.

The only indicator the pessimistic economic commentators have been correct on is the continuing very weak business confidence levels. However, as stated previously, the low business confidence does not reflect weak demand in the economy, it reflects frustration with Government policies on water, carbon emissions, employment and immigration.

Stuttering progress towards a China/US trade agreement

Many observers are concluding that a China/US trade agreement is further away than ever with the Chinese prepared to wait until after the 2020 Presidential election to see whether Trump is still in the White House. The Kiwi dollar was sold down when the Chinese trade delegation cancelled a scheduled visit to US farmers in Nebraska last week. If there is some positive progress coming out of the early October China/US trade negotiations, there may finally be a reason to buy the Kiwi rather than sell it.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

5 Comments

Sorry Roger but FX markets do not agree with your view of China winning trade war, or the fact that in general you are neutral on China's demerits period. Ditto other writers on this site. FX markets value USD higher because it is safe haven and because of US_Euro dominate of trading payments in general. SO, interest rates are not everything. Kiwi dollar is tied in FX minds, to the Yuan and the Yuan value is going down. Also, NZ economic growth prospect has gone from 4.5% in 2017 (according to laughable Treasury) to 2.7% now (for 2020) And the latter has no justification either as trend is plainly down. THIS is why Kiwi continues to weaken. Plus NZ dairy not looking to healthy either and RE market flat as a pancake. Plus RBNZ cut NZ interest rates more than US in last year. SO, big surprise, Kiwi is falling.

Again Roger displays a lack of understanding regarding what is driving USD strength. It's a global shortage of Dollars, why have the Fed had to suddenly inject a tenth of a trillion bucks into the banking system? China is massively short of USD too. Irrespective of US interest rates people need Dollars and when the Eurodollar system seizes up due to counter-party trust issues the value of the dollar is going to rise. Look at what happened to the USD when Americas credit rating was downgraded for the first time in 2011...

Sorry make that more than a quarter of a Trillion bucks.

Roger, I have no idea which stance the RBNZ will take this week, but my opinion is that the trade war itself is flexing the U.S. dollar's muscles. The money printing that starts Monday (U.S.) injecting 75 billion a day for 14 days (1.050 trillion total) should logically have some effect towards diluting the U.S. dollar's strength. But who knows? We don't seem to have "rational" markets anywhere.

The world's economic drivers are constantly changing positions as each global segment tries to re-position itself for the upcoming battles. We've been in an economic war for a long time, probably most of this century, but it's becoming clearer that not everything can be answered with economics. The price of crude oil will skyrocket when the rockets start flying, even though Trump has tried hard not to pull the trigger (or should that be push the button) but it's becoming obvious this strategy has its limitations.

Then, when we're queuing for our allocated 30 litres of petrol at $3.95 per litre & consumer inflation is on the up all of a sudden, only then will central bankers be happy, right? Right!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.