Summary of key points: -

- NZ economy rebounding, however still tough decisions ahead

- Inflation figures next week

- US consumers right to be cautious

- Headwinds for the Euro die away

NZ economy rebounding, however still tough decisions ahead

“Go early and go hard” was the mantra from both the New Zealand Government in respect to measures to control the spread of the Covid-19 pandemic into our country and also from the Reserve Bank of New Zealand to aid the economy out of the negative shock it took on the isolation shutdown.

So far, on any international comparison one chooses to select, we look to have been fairly successful on both counts with the decisions taken and responses since.

However, four months on from the difficult days back in March we still appear to have large decisions on “where to from here” as we debate how our borders are reopened and the markets speculate on whether more monetary stimulation is required to get the economy back on track.

There are implications for the NZ dollar exchange rate on how our economic picture unfolds over coming months. More quantitative easing from the RBNZ would be negative for the Kiwi dollar, as would a prolonged delay in instituting the trans-Tasman travel bubble to throw a lifeline to the beleaguered tourism industry.

Up to the minute, high frequency consumer/retail related data on the NZ economy captured and published by Kiwibank suggests that there is more to the rebound in household spending than just pent-up demand coming through from the lockdown period.

Kathmandu’s spectacular sales growth over recent weeks and other retail sector reports reinforces the view that Kiwis are not being all that cautious with their money due to job insecurity or worries about future house price movements.

Finance Minister Grant Robertson has observed that the economic rebound is occurring at a faster pace than generally expected.

Whilst we may record a technical recession with two quarters’ contraction in GDP, it is not like any other recession in that our major industries (outside hospitality/tourism) have not experienced major downturns in production and sales.

Therefore, the earlier prediction from economic forecasters of a hard, slow recovery for the NZ economy with high unemployment rates is so far not looking to be the case.

Whilst perhaps the economic reality is yet to feed through from some serious job layoff numbers, to date the positives seem to be outweighing the negatives.

A continuation of the stronger economic activity numbers over coming weeks will be reassuring evidence for the RBNZ as they contemplate whether more stimulus is required ahead of their 12th August Monetary Policy Statement.

At this point, with the banks flush with cash and no signs of widespread company failures and financial hardship outside the travel and tourism sectors, the justification for more money printing is just not there.

Certainly, the financial and investment markets in New Zealand are reflecting a decidedly more positive outlook for future economic conditions with the NZ share market (albeit a small number of stellar stocks) and the NZ dollar rising in value.

Should the NZ dollar continue to trade higher into the 0.6600’s against USD and well above 0.9400 against the Aussie dollar, the RBNZ will again express worry about exporter’s profitability and the negative impact of that on the economy.

However, the RBNZ needs to be careful not to “over-cook” the stimulus and create larger asset bubble and inflation issues just to hold the currency within a certain desired range.

With most exporters currently well hedged against future currency risk (in particular, the US dollar weakening substantially in its own right) the RBNZ’s cure (more QE) would seem to be for a problem that does not exist.

Despite all the speculation around what the RBNZ may do or not do on 12th August, my view is that they will continue with a “wait and watch” approach to local economic developments. The impact of the global economic recession on the NZ economy is also panning out to be quite different to the norm, with export commodity prices not falling and inward investment interest into New Zealand anecdotally increasing.

Inflation figures next week

The local forex market will now be focused on the June quarter’s inflation numbers being released on Wednesday 15th July with consensus forecasts for a 0.4% quarterly decrease to drop the annual inflation rate from 2.6% to 1.6%.

Reductions in fuel prices will play a big part in the figures, however most other prices such as food have been increasing over recent months.

Again, the impact of the NZ dollar exchange rate on the inflation rate will be muted as importers (not oil companies) were hedged against the plunge in the Kiwi dollar below 0.6000 in late March.

The RBNZ should not be factoring in a lower currency value to help them keep the inflation rate at around the 2% target level.

US consumers right to be cautious

The disconnect between the rising equities market and economic reality on Main Street is much more pronounced in the US economy.

Zero per cent interest rates do cause unintended consequences with the weight of funds still flooding into shares as there is no yield return with bank deposits and bonds.

For this reason, and as time marches on with the recovery in US share markets proving to be more sustainable than initially expected, the risk of another leg down in equities pulling the Kiwi dollar down in tandem continues to reduce.

Whilst poor leadership and control is now expanding the first Covid-19 virus wave to the southern states in the US, the worries about a second wave have seemingly diminished.

There is no question that the confidence levels of consumers in the US are much lower coming out of the pandemic crunch than confidence levels in Asia, Europe, Australia and New Zealand.

As stated previously, the recovery of the US economy is looking more like a long, hard slog because their leadership was largely ignorant and in denial about the dangerous spread of Covid-19.

Consumer confidence levels about spending and jobs could have been a lot different today had their President donned a mask in February/March and preached personal health responsibility to stop community transmission.

Judging by the political opinion polls in the battleground states, Donald Trump is going to pay the price for his incompetence through the pandemic crisis and a Democratic President will be voted in come November.

The Silicon Valley billionaires are putting their financial clout (which has lifted considerably with their share prices over recent months) behind Joe Biden’s campaign.

What this means for the US dollar currency value is less business-friendly economic policies under a Democratic President, House of Representatives and possibly Senate. The case for a weaker US dollar over coming years has been reinforced over recent weeks.

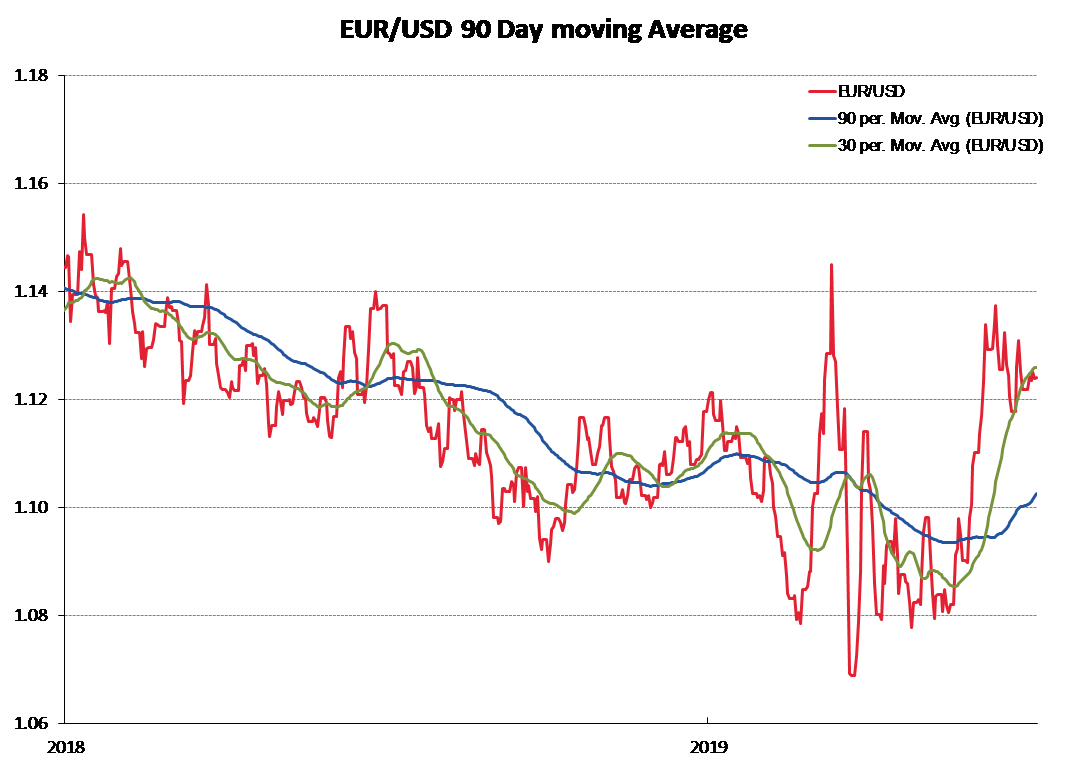

Headwinds for the Euro die away

The Euro has already recorded its largest two-month advance against the US dollar in more than two years to $1.1250 as the Euroland economy returns to some form of normality earlier than the US. Interest rate differentials are no longer a headwind for the Euro against the USD and there are no political risk factors in Europe compared to increasing uncertainties in the US. Therefore, investment capital flows will continue to reverse back in favour of the Euro.

The Australian dollar continues to display strong resilience in holding up near to 0.7000 against the USD, despite Covid-19 community transmission problems in Melbourne. Further increases in the NZD/AUD cross-rate above 0.9400 are not expected as differing monetary policy approaches from the RBA and RBNZ (no negative rates for the RBA, whilst Adrian still has it on the table here) points to the AUD outperforming the NZD against the USD from current levels.

On the technical chart front, the recent Euro gains against the USD have caused the moving-average trend lines to point to a firm uptrend.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

7 Comments

Thankyou Roger another great informative article !

'Whilst we may record a technical recession with two quarters’ contraction in GDP'

Yeah it's a big if. Very unlikely to be honest. Only the biggest economic dislocation in history with new immigration shutdown and international tourism at zero, on top of one of the most over leveraged house hold sectors in the world. Even if we do on the offhand chance have a possible technical recession, will be back to the races after that. Throw in another earthquake and a couple of cyclones and our GDP might overtake the US.

How likely is that? We've ruled out international students returning and the tourism sector will probably never look the same again. Those are big chunks that are missing from our economy for the foreseeable.

That is going to have to be one hell of a cyclone!

SailorRob - I see it as 100% the Sept quarter will be positive growth. It's not at all-bad out there, the recovery is already well under way. This is not a usual recession, our exports are booming, low interest rates, Pandemic under control. Sure there is 5.5% of our GDP gone from international tourist/students but there are positives like $10,500,000,000 dollars not being spent by Kiwi's travelling overseas, $3.5 billion saving in the drop of oil and our economic future not being dominated by a Virus internally. Check the true facts and there are many reasons to be positive !

Hi Roger, I can remember listening to you when you were on ZB with the late Paul Holmes in the mornings...but that is showing my age ! Anyway, what do you think between now and the US election about the NZD/USD rates. I am holding US residential property and want to sell ASAP (already started the process) so to bring the funds back to NZ , as the rate just seems to be creeping up and up ie from 0.57 to 0.61 to 0.64 ....so the higher those numbers go, the less NZD I will receive.

I realise this is not financial advice, but I am quite "weary" about the state of the US economy, as I can't see it getting any better or stronger this year, as having spent a bit of time over there and friends who currently live there, while so many nations are wanting to "step away" from the USD as the global reserve currency.

Any thoughts on this one ? thank you Roger

Roger is likely right , we should not resort to QE or "printing ' until we absolutely need to, the storm is still coming and its going to wreak havoc

The economic fallout from Covid has not even started yet ......not by a long shot , the worst is months if not years away .

The falling into a hard recession is not going to be linear either , its going to take time and be punctuated by what appear to be "lights at the end of the tunnel" and possibly even some 'gains" and good news events , only to be followed by more pain .

Either way the only thing I would recommend to anyone , is to take their time during this Lull-before - the

- storm to SAVE AND PAY DOWN DEBT .

There may have been a reduction in some CPI items (e.g. fuel prices) but, as CPI is based on a weighted basked of goods, it likely has a low impact on CPI overall. Simply stated most people where not purchasing fuel during the lockdown so the price would have carried a very low weight towards CPI.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.