Summary of key points: -

- Debt funded lolly-scramble coming to an end

- Kiwi dollar under-performance abruptly reverses

- NZX cyber-attack ignored by the FX market

- Export-led economic recovery still has some challenges

Debt funded lolly-scramble coming to an end

"Living in a fool’s paradise” is a well-used term in New Zealand’s economic history to describe periods when we over-extend financial risks, but no-one really cares as the party blasts on.

The current Covid-ravaged economic environment is starting to feel this way as the debt-funded lolly-money from the Government inevitably runs out and investment asset bubbles inevitably implode on themselves.

“But this time it is different” is often the answer to such sceptical expectations about the future.

The only real difference today to previous periods of irrational exuberance is that the cost of debt is near to zero and investment in traditional alternatives to equities (cash and bonds) do not make any sense as there is no return yield.

We know for sure that mortgaging the future to have a consumer spending party today has to come to an end very soon. However, we do not know when the equities investment bubble (comprising the mega-capped US tech stocks) will deflate/burst as unrealised paper-profits are inevitably converted into realised cash in the bank.

When that time does eventually arrive, the NZ dollar exchange rate will again move out of favour for international investors/traders as the “risk-off” mode pervades through the financial and investment markets.

The upcoming general election in New Zealand and Presidential election in the US may act as catalysts for some investors to take profits, or it may be another “event risk” or shock we do not know about.

Picking the timing of a sizeable market correction is impossible, however history tells us that it always happens.

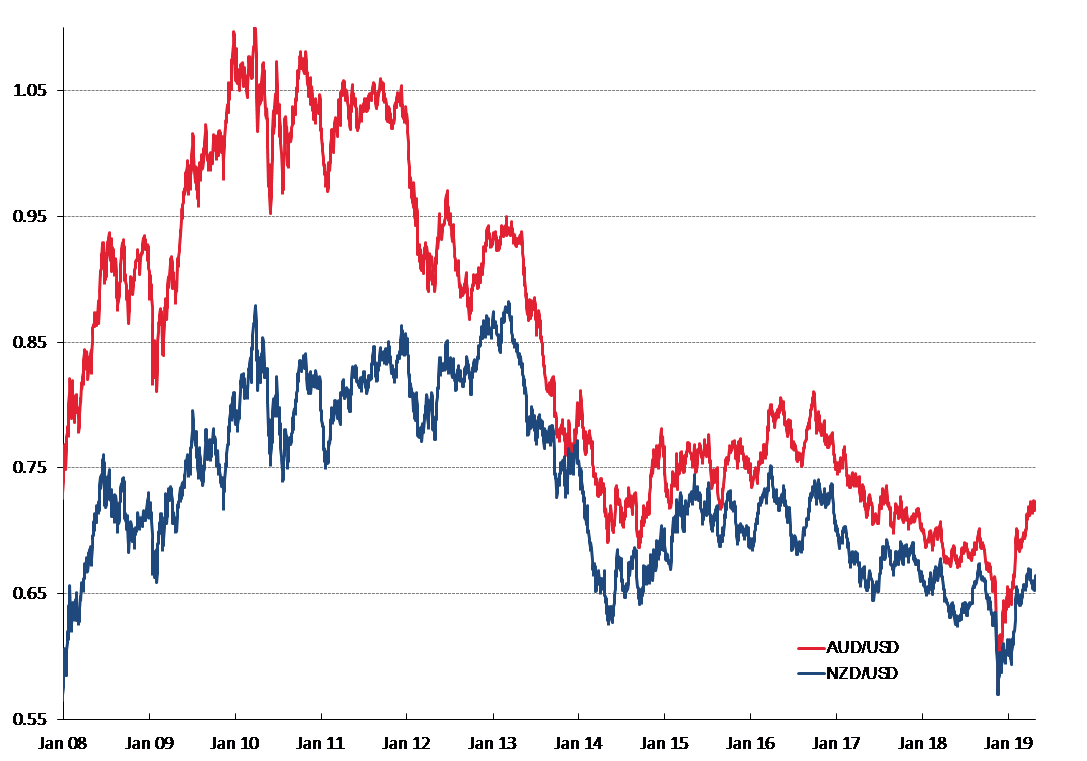

Kiwi dollar under-performance abruptly reverses

Through July and early-August the Kiwi dollar under-performed the appreciating Australian dollar against the USD and rising equity markets, due to the RBNZ jawboning it lower as part of their looser monetary policy settings via increasing the QE amount.

As commented on at the time, the RBNZ might like to think they have a command over the value and direction of the NZD/USD exchange rate, however in the end they do not as far greater global forces take over.

The spectacular jump up in the Kiwi dollar over recent days from 0.6500 to 0.6740 has been a sudden and largely unexpected catch-up to the recent disconnect to the AUD and equities markets.

It looks like offshore currency traders quickly recognised the short-term Kiwi dollar misalignment and have increased speculative bets on the NZD, driving it up sharply to 0.6740.

The probability of the anticipated short-term downward correction in the NZD/USD rate to the 0.6400/0.6300 region does appear to be further away today.

However, there must be some serious profit-taking not very far away from market participants who have been long AUD against the USD, short USD against the EUR and long equities. All these traders/investors have enjoyed significant unrealised gains from the rapid favourable market movements of late.

NZX cyber-attack ignored by the FX market

The Kiwi dollar has encountered immediate resistance at rates above 0.6700 previously this year, in the first few days of January and again in late July. On both occasions it promptly retreated to lower levels.

Our economic news and recovery from Covid shutdowns is not that different to other economies to differentiate the Kiwi dollar out for any special treatment at this time.

What is really surprising is the dramatic NZD gains to above 0.6700 occurred over a few days last week when the on-line NZ stock exchange was closed due to cyber-attacks.

Our reputation and credibility as a safe/secure investment destination has taken a massive hit through this event, however to date that has not reduced any enthusiasm to buy the Kiwi dollar.

The total disconnect between the NZ share market and the NZ dollar FX market does not add up, however the fact that our major stocks are also listed and traded on the Aussie stock exchange is a partial explanation.

Implications for New Zealand’s reputation will not be positive if and when it is revealed that NZX’s cyber defensive standards were not sufficiently robust to prevent such an attack.

Export-led economic recovery still has some challenges

The risks described above that could send the Kiwi dollar lower from current levels are all likely to play out over coming months. Beyond that period, the medium to longer-term outlook for the Kiwi remains positive with a weaker USD globally and comparatively stronger NZ economic fundamentals such as increasing overseas trade surpluses and high terms of trade index.

However, there are prerequisites to our economy being superior to others through a strong export performance in 2021 and beyond: -

- The Government recognising that there will not be sufficient local workers to pick the apples, milk the cows, operate sophisticated agricultural machinery and harvest the grapes and thus a way has to be found to allow in seasonal workers from the Pacific Islands and elsewhere under the RSE schemes. Otherwise, export production will be compromised.

- The Government also backing down on draconian and ideologically driven environmental policies on water run-off from farms, when it is a tiny minority at fault. Right now, Government leadership needs to be nurturing rural confidence as our economic saviour, not destroying it through sledgehammer regulation.

Unfortunately, through these challenging economic conditions and times we seem to be bombarded with “unintended consequences” from decisions made by authorities. Some examples to contemplate: -

- Zero interest rates designed to stimulate economic activity, but actually causing excessive investment risk-taking and thus property and equities speculative bubbles.

- The Auckland/Waikato border controls restricting healthcare and food manufacturing as workers could not get to their workplaces (under level 4 they were essential workers, under Auckland’s level 3 they required bureaucratic exemptions).

- The Government’s Covid elimination strategy based on an early health solution being the best outcome for the economy, now in tatters as businesspeople lose confidence about the future as every Covid outbreak will lead to continuing shutdowns. Business folk are still awaiting the Government’s long-term term plan as to how we live with Covid, so they can also plan and get on with investing and employing people.

- The US Federal Reserve changing to an “average” inflation target from the current “single point” target of 2%. The problem being that actual higher inflation influences all price-setting behaviour and rising inflation feeds on itself. Delayed monetary responses normally have to be much more severe and therefore impart greater economic damage. For the moment, the Fed are happy to accept this risk.

The rollercoaster ride that is the Kiwi dollar movements seems likely to continue over coming months, and it will not all be in one direction. The AUD/USD rate movements also continue to be the dominant influence over NZD/USD rate movements.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

17 Comments

Mortgaging the future is the only play the RBNZ has. Just a little bit more...

DTM,

But it's not just our Reserve Bank stuck in this hamster on a wheel mindset. Here is a quote from Mervyn King's(former head of the BoE) The End of Alchemy; Central banks are trapped into a policy of low interest rates because of the continuing belief that the solution to weak demand is further monetary stimulus". That was written in 2016 and we are much further down that path now. The result? little stimulus to the productive economy, but lots of stimulus to the stock and housing markets. As a beneficiary of this, perhaps I should just sit back and be grateful, but I have grandchildren and I worry about their prospects.

I agree, they've painted themselves into a corner, and the solution so far has always been to double down. Has to end at some point, but nobody wins when that happens.

Just imagine if the government got organised and built affordable housing en masse. Like it did in the 1950s, but this time in the form of centrally located apartments.

They could sell 3 bedroom apartments 'at cost', freehold, for circa 550K.

Or they could sell some as leasehold for circa 400K.

They wouldn't have to cut interest rates anymore, because housing would be truly affordable. And because the housing would be much more affordable, the middle income households living in them would have more disposable income to spend in the economy...

We would also have sustained economic and employment growth from counter-cyclical development activity.

People would invest in business. People would be encouraged by the affordability to take risks elsewhere, having a go at creating a real, productive enterprise.

Would be a pretty different environment.

They could sell 3 bedroom apartments 'at cost', freehold, for circa 550K.

Actually they could sell them much cheaper than $550K. They don't even have to sell them. Just let them as a proportion of h'hold income. No different to Austria, Japan, and S'pore.

The more that housing costs are reduced, the more spent into the consumer economy or invested in other sectors of the economy. At present, property services is the biggest driver in the NZ economy. Is that a problem? Not necessarily. Just depends on what kind of economy you want.

And at present instead of working for affordable rents we subsidise them to raise the rental floor and yields for investment property. Bizarre welfare.

Looks like Roger has bought into the bubble thesis. Not sure if this is a recent realization or not. It shouldn't be.

It’s interesting he mentions the stock market bubbles and not the other ones

Hey folks! Serious question , you might see it as trolling ,but unfortunately no jokes.

I have a little kid (2 y.o.). I myself was always taught to always work hard and try to save as much as I can, don't engage with suspicious investments, cannabis is bad etc. etc. etc.

Given that this govt (I mean not only the current one) and RBNZ broke all my understanding of how things should work in this world and really letting me down day after day, shall I just start the polemic in my family , e.g. stop saving , throw as much money as you can in as riskiest "Investments" as possible (e.g. Cannabis ETFs etc , maybe even "heroin" ETFs soon if suddenly it becomes legal), you should not worry about house price, just buy!!! because by the time you are at my age the OCR will reach -20% .

Seriously, I'm a bit lost in how to talk to my kid .

Teach your child above all else to treat people well no matter who they are and where they come from, have a decent work ethic to be self sufficient no matter what way the world turns. To be open minded, curious, and believe in themselves. Teach them that others don't define the limits to what they can achieve, they do. Save for a future but don't forget to live. Debt is giving someone else control over your future, so be selective and not dependent.

Thanks , those things in the beginning of your comment are just great ,but I was really asking about "saving habits". So regarding "Save for a future but don't forget to live. Debt is giving someone else control over your future, so be selective and not dependent". I'll tell you what, it all sounds like if you are not collecting debt massively you become a looser , and the further things go the more you loose. So "Save for a future" might probably save someone else's future and not yours . And regarding " Debt is giving someone else control over your future" - It also sounds wrong suggestion in the current environment - rephrase it to " Debt is giving you (as a landlord) control over someone else's future" . So thanks, appreciate you comment but one of us is living in some different New Zealand apparently

It's not the here and now we are talking about Andreas. Your kids are only two years old, so it is the future we talk about. I don't know about you but the current place the world is in is so far off any maps no one can know where we will be in five, 10 or 20 years. Sure interest rates are low now and property is high, but where will they be in five years? You can bet on where you think they will be, but that will be just that - a bet, where if you are loaded with a lot of debt and inflation comes back you can lose everything. Do you want to set your kids up for that?

Teach them to be suspicious of RBNZ e.g. jaw-boning exchange rate = signal to banksters to take other side of trade

https://www.theguardian.com/world/2020/aug/31/new-zealands-astounding-w…

"The extent of wealth inequality in supposedly egalitarian New Zealand has been laid bare by figures showing the wealthiest individuals have over NZ$140bn (US$93bn) stashed away in trusts – and overall have nearly 70 times more assets than the typical Kiwi."

"While some rich listers are entrepreneurs, developing useful new products, fortunes made in finance, insurance and real estate are predominant. Conversely, the country’s essential workers – including health staff on the front line of the coronavirus pandemic – earn so little that they are often unable to save for a house deposit."

Among those in the poorest half of the country, meanwhile, the average person owns assets worth just $46,000 and has debts of $33,000, leaving them with a net worth of $12,000. They have negligible wealth in trusts and on average just $4,000 in the bank, leaving them vulnerable to sudden financial shocks.

This is the crux. People are living paycheck to paycheck. I have quoted the profile of those below the median. The cash at hand is the issue. This has the potential to rip the guts out of the economy. It's all about consumer spending and there are simply crumbs for the rainy day.

It's raining now.

No capital gains tax policy favors the 1% fat cats. Income tax is for the working class to serve the fat cats.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.