Summary of key points: -

- Stronger US dollar in 2019 – Weaker US dollar in 2020

- Forecast for the US dollar in 2020

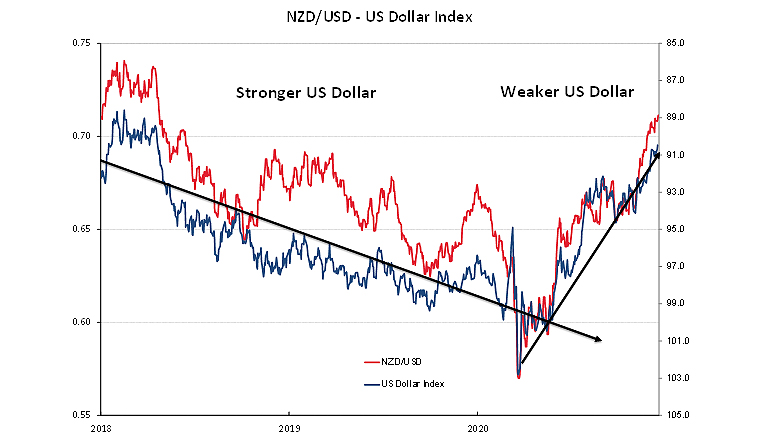

Stronger US dollar in 2019 – Weaker US dollar in 2020

Two gentlemen, residing in Washington DC, have both had a profound impact on the value of the US dollar currency value over the last two years.

Through 2019 the USD strengthened from 90 on the USD Index to near 100 (refer chart below where the USD Index is inverted on the right-hand axis) as President Donald Trump ramped up his trade war against China and currency markets reflected the resulting global trade/economic risks and uncertainties by buying the USD as a safe haven place to be against that environment. Encountering a few bumps along the way, the NZD depreciated against the stronger USD from 0.7400 to lows of 0.6300 in late 2019.

The direction and sentiment towards the US dollar in 2020 was completely the opposite to the previous year.

The initial problem in world currency markets when the Covid-19 pandemic struck in March was a severe shortage of US dollars available in the system. The NZD/USD exchange rate nose-dived to 0.5500 for a very brief period in late March as all countries scrambled to buy the USD’s they required. In stepped the US Federal Reserve, led by Jerome Powell, with provision of immediate currency swap facilities to all and sundry to free-up the USD supply blockage. That Fed rescue action reversed the short-term USD strength in March, and it was followed by a massive monetary stimulus into the US economy. Remember “infinite QE”, meaning that the Fed would keep printing a supply of US dollars to combat the pandemic-induced economic shock. Last week the Fed were still printing more US dollars as Covid miss-management by government authorities (mainly the former President!) still meant that the US economy was struggling to recover from shutdowns and lockdowns. The US dollar’s value has slumped against all currencies throughout 2020 as the supply of US dollars has increased. In addition, substantially weaker US economic fundamentals in the form of the Government budget deficit blowing out to 16% of GDP and US Government debt soaring to unprecedented levels has driven further nails into the US dollar’s coffin.

Zero interest rates and money sloshing around the system has driven spectacular gains in US equity markets (technology stocks in particular) since April. A combination of the Fed’s monetary policy actions debasing the USD value and investor “risk-on” sentiment in equity markets, propelled the NZD/USD rate from below 0.6000 in April to above 0.7100 today.

The Reserve Bank of New Zealand attempted for a period to supress the NZ dollar appreciation through threatening negative interest rates and possibly buying of foreign bonds as part of their QE programme. Their rationale was that a higher NZD/USD exchange rate would hurt exporter profitability and that in turn would inhibit the export-led economic recovery. The rationale was flawed as they ignored currency hedging exporters already had in place to protect their profits. The NZ dollar received another turbo-boost higher from 0.6600 in October when the Labour government was elected in a landslide and to the relief of the business community the Green Party was not holding the balance of power.

In summary, the largest risk facing local New Zealand importers (buying USD’s) and exporters (selling USD’s), over the last two years has been the change in value of the USD side of the currency pair, not the NZD side. As the chart below demonstrates, the NZD/USD rate has followed the USD Index very closely, indicating that specific New Zealand economic or capital flow factors have only been a very minor part of the NZD fall in 2019 and rebound in 2020.

Forecast for the US dollar in 2021

While the majority of global investment banks and fund managers are still forecasting a continuation of the weaker USD trend in 2021, in my view two key and related factors will determine currency market outcomes: -

- Speed of the vaccine-inspired US economic recovery – The American approach to healthcare has always been the ambulance at the bottom of the cliff with the cure, instead of preventative precautions at the top. If consumer spending and jobs recover with the vaccine roll-out across the US, the massive monetary and fiscal stimulus can start to be eased off. The US could be ahead of Europe in this respect; therefore, it would be difficult to justify a stronger Euro above $1.2500 against the USD. The equity markets will not like the Fed removing some of the candy, so watch out for the inevitable correction in the share markets to the jaw-dropping 2020 gains.

- Inflation – not deflation – Both the US Federal Reserve and the RBNZ have indicated that they are not worried about inflation increasing in 2021, they would rather have that problem from over-doing the monetary stimulus, than not doing enough to save the respective economies. However, given the Covid vaccine roll-out and supply disruptions in many industries it is very hard to see a trend to lower inflation (below 1.00%) that the RBNZ have been forecasting. When they are forced to adjust their 2021 inflation forecast higher, the forward looking FX markets will start to price-in future interest rate hikes. Bond market pricing (rising yields) is already starting to reflect rising inflation in 2021, not deflation.

Therefore, my crystal-ball prognosis of the NZD/USD trajectory through 2021 comes in three phases:

- December/January correction back to the 0.6800 region on short-term FX and equity market profit-taking. Against the USD Index, the NZD/USD rate has over-shot to the top-side over recent weeks.

- NZD/USD gains to the 0.7500 area over the first half of 2021 as the USD continues to weaken against all currencies for the 2020 reasons cited above.

- When FX and equity markets receive the first sniff of interest rate increases on the medium term horizon (the first sniff coming sometime in the second half of 2021) the picture changes to a USD recovery as investor sentiment reverses to a “risk-off” mode. Under this scenario, the NZD/USD rate will not reach the 0.8000’s it got to after the GFC a decade ago.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

Should we be concerned ? we have seen the USD as weak as 0.87 in the past and nobody mentioned it. This time however feels different, the USA is reeling under this pandemic and simply cannot control it and over the years China has silently crept up little by little and is poised to take the crown. One feels the USA will not go down without a fight.

Excellent analysis by Roger Kerr, so much more accurate than that of the Bank economists,.

US go just got nod ahead with 900billions pandemic relief fund, after long wrangling. Not bad for population of around 350millions, comparing to NZ 5million team with 100billions knee jerk shot in vein, outdone the rest of those OECD, even in OZ now their reserve bank, considering to go or not for outshine Kiwis to 142b?.. still unsure though,.. pain medication now, for later recovery result? or follow Kiwi way of no bitter pill but straight to 'wow recovery'. The green back fight to retain it's dominant position, will yield collateral damage to some.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.