Summary of key points: -

- Marginal change by the Fed sends the US dollar soaring

- USD side of NZD/USD equation continues to dominate

- Forecasts of strong NZ economic growth appear misplaced

- Shooting ourselves in the foot – Government pulling the trigger!

- US dual deficits are negative for the US dollar in 2022 and 2023

Marginal change by the Fed sends the US dollar soaring

The central FX market outlook thematic of this column has been that a stronger US dollar against all currencies would emerge in 2021 as the US economy recovered strongly from Covid enforced lockdowns and the US Federal Reserve would be forced to dial-back on its extraordinary monetary stimulus levels.

We have been consistently forecasting a Kiwi dollar pullback from around 0.7300 to the 0.6900/0.6800 region due to this expected USD strength. Following two months in April and May of mixed US economic data results, which resulted in a sideways movement for the USD against the EUR and NZD (0.7150 to 0.7300 trading range), the currency market landscape has dramatically changed over this past week.

The US dollar has certainly struck back with some vengeance in global currency markets since the Federal Reserve FOMC Committee delivered some “ever so subtle” changes to its messaging on Thursday 17th June. The forex markets reacted instantaneously by buying the USD against all currencies when the Fed stated the following: -

- The labour markets is seen as very strong and sizeable increases in new jobs can be expected over coming months.

- The timing of the first interest rate increases from the Fed being brought forward in 2023 compared to the timing in their March statement.

- Individual Fed Governor’s own predictions of the timing and amount of future interest rate increases (the “dot plot”) indicating that more FOMC Committee Members see earlier increases in 2022 and 2023 than previously.

- Risks may have increased that the lift in the annual inflation rate to 5.0% may prove to be more permanent than the previous expectation of only a short-term “transitory” increase.

Over recent months the majority of the investment banks on Wall Street (Goldman Sachs, UBS, Citigroup, Morgan Stanley, JP Morgan Chase etc) have been forecasting a weaker USD against the EUR to above $1.2500 due to the Fed continuing their super-loose monetary policy for most of 2021.

These investment banks would have had short-sold USD positions placed in the FX market to profit from others following their forecasts and selling the USD.

Their strategy has badly backfired on them as the Fed has caused massive USD buying over the last few days.

A significant part of the USD buying that has driven the EUR/USD exchange rate from $1.2200 mid last week to $1.1860 by weeks end was those very same investment banks being “stopped-out” of their short-sold USD positions and being forced to buy the USD’s back. The 2.8% appreciation of the USD against the Euro over two days, has contemporaneously dropped the NZD/USD rate by 3.0% from 0.7150 to 0.6935 at the market close on Friday 18th June.

USD side of NZD/USD equation continues to dominate

Further USD gains over coming weeks seem likely, particularly on the back of large NonFarm Payroll employment increases for the months of June and July. The minimum that could be anticipated is the EUR/USD rate declining from $1.1810 to $1.1700 (which it last traded at on 31 March 2021), which given the close correlation to the NZD/USD rate would have the Kiwi down to 0.6800.

Adding to this NZD depreciation is a sharply weaker and out of favour Australian dollar, both currencies suffering when global investment market risk aversion levels increase i.e. equity markets falling in value. A Chinese Government crackdown on speculation in commodities markets has also weighed on the Aussie dollar.

Forecasts of strong NZ economic growth appear misplaced

A second strong theme of this column over the last 12 months has been that the NZD/USD exchange rate direction would be purely driven by the USD side of the equation.

New Zealand- specific commodity price or economic data was seen as having no direct influence on the NZD/USD rate movement as the international hedge funds (who use to be large players in the speculative Kiwi dollar FX market) were no longer interested to buy or sell the Kiwi on separate NZ news or developments.

Last Thursday’s surprisingly strong NZ GDP growth number of 1.6% for the March quarter only very briefly lifted the Kiwi 40 points from 0.7050 to 0.7090 before the dominating USD forces took over and the Kiwi sunk to 0.6935.

Yet again buoyant retail spending and house construction were the sectors of the economy that caused an expansion considerably above the consensus forecast.

The majority of local economic forecasters (RBNZ, NZIER and all the banks) are predicting a continuation of this stronger GDP growth for the NZ economy over the next 12 months of up to 4.0% and 5.0%.

They seem convinced that strong consumer spending financed by increasing debt on appreciating house prices is a sustainable economic model.

They are all far too optimistic on the economic outlook in this writer’s opinion and are ignoring what is happening at the heartland coalface of the economy. The productive base (agribusiness, primary exports, construction and manufacturing) of the NZ economy is currently facing major growth constraints in the form of severe labour shortages, a broken supply chain and over-the-top Government regulatory change. Remove the GDP growth that comes from foreign tourists and immigrants and the picture is far from rosy.

New Zealand has had to learn some harsh lessons from debt-fuelled spending splurges in the past, it seems the current Government has no institutional memory or understanding of such past policy errors.

Shooting ourselves in the foot – Government pulling the trigger!

Observing New Zealand’s current economic policy direction can only be summed up as - “Why are we continuously shooting ourselves in the foot?"

The Government seems intent on attacking the agricultural productive base with water/carbon costs and now climate change targets that require a 15% reduction in livestock numbers.

Farmers and tradies being required to part finance EV’s owned by the urban elite is arguably the last straw for many. Jacinda and Grant are lucky that the milk price is currently $8/kg milk solids, otherwise we might have tractors being driven down Queen Street in protest. Correction: tractors being driven down Tay Street, Invercargill is more likely as Queen Street in Auckland is largely blocked by obstacles put in place by the Council!

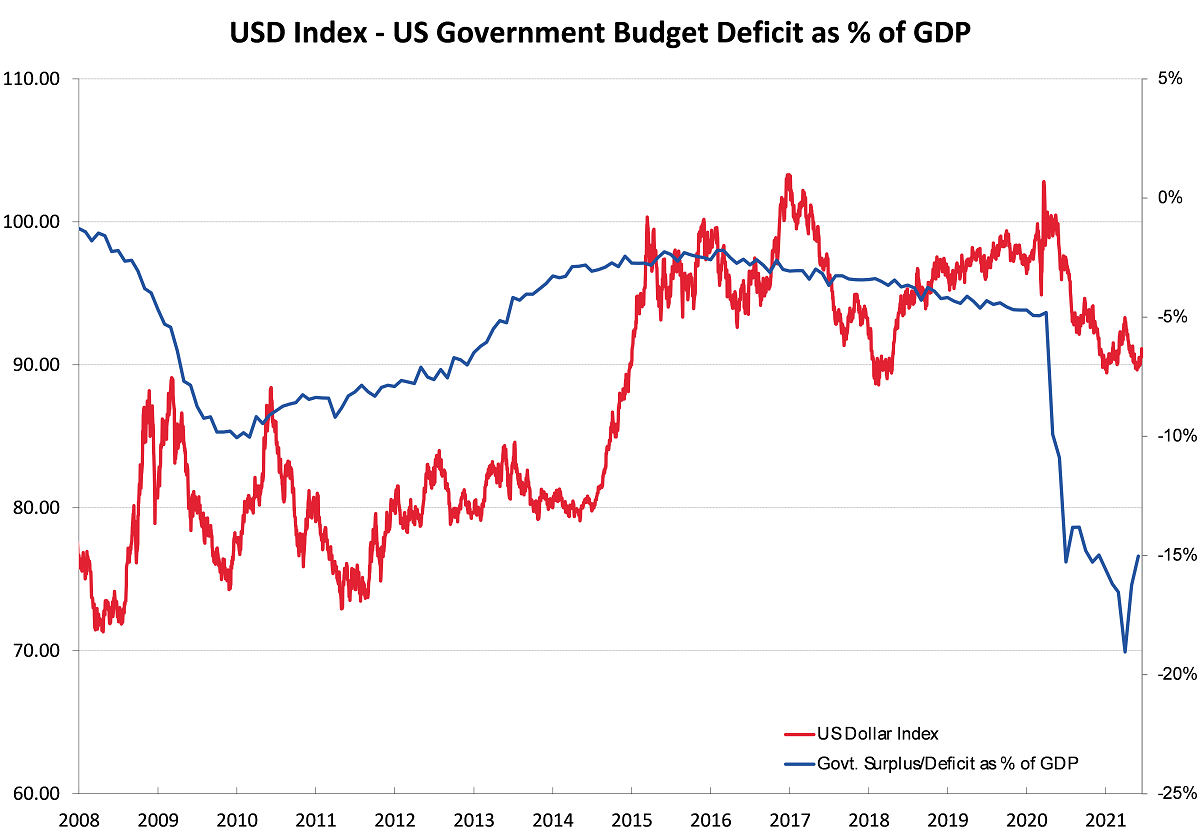

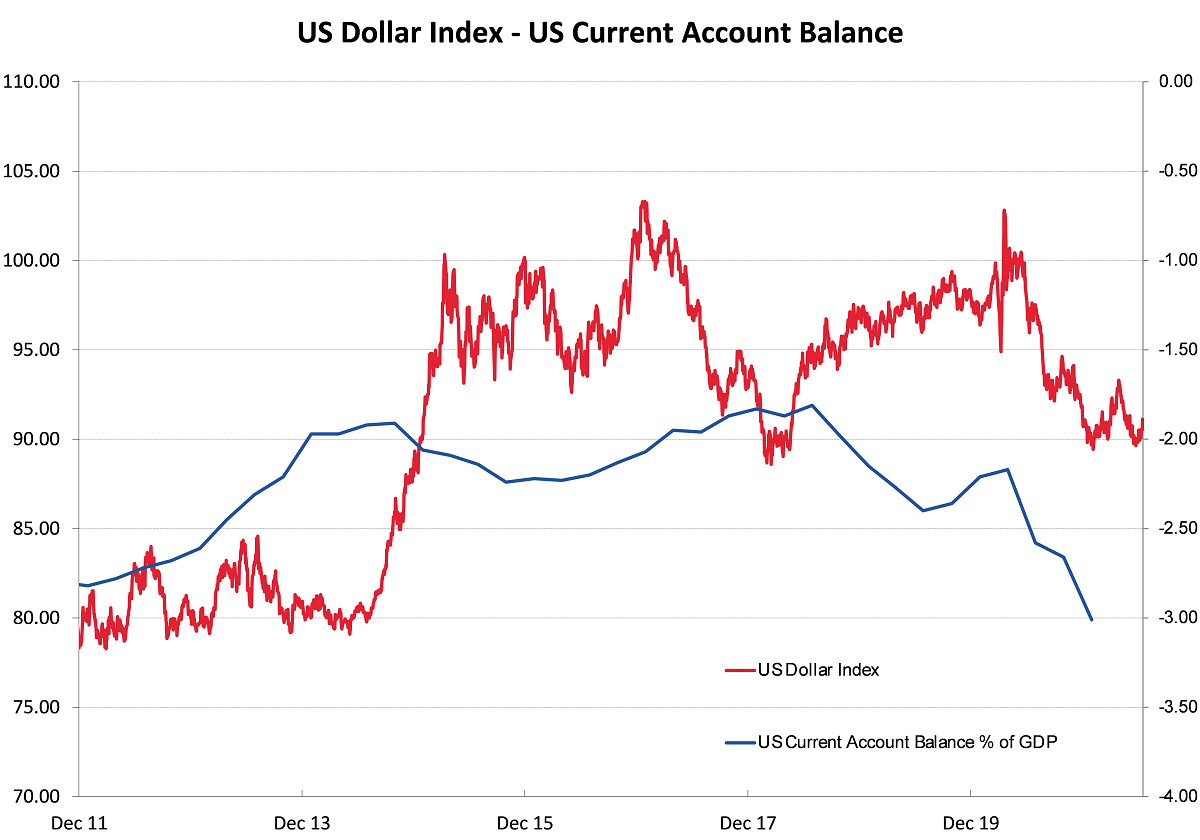

US dual deficits are negative for the US dollar in 2022 and 2023

Whilst the US dollar has room to strengthen further over coming months as the Fed signal a progressive unwinding of their monetary stimulus, the medium to long-term outlook for the USD is much less certain.

The US dual deficit situation is extreme compared to recent history. When both the internal Government budget deficit and external Current A/c deficit blow out the US currency value invariably depreciates. Currently, the Government budget deficit has increased to 15% of GDP and the Current A/c deficit has increased to 3% of GDP.

These very poor economic fundamentals suggest a much weaker US dollar value in 2022 and 2023, and this is the risk that local USD exporters need to hedge against.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

10 Comments

Up goes petrol and all other imported commodities.

Inflation rate going up in the next quarter.

Interest rate increases just around the corner!

Sadly, mortgagee sales will be inevitable

Hold on to your seats!!

RBNZ are looking through inflation don't you recall?

Heard it all before, but you know what they say about broken clocks.

Wait until you see the next CPI rates, it is possible that you could see a number closing on double digit.

I'm seeing steel +20% in 3 months, Milk up 8-10%, food items up 10%+, butter up 50cents a lb (10% already), and a massive Fonterra brands price increase is about to come through with the quarterly price review (driven by global prices). Add scarcity of vehicles, new taxes on housing, rates increases.

Pick the worst number you could think of, can the RBNZ look through that?

The mighty Tane Mahuta can look though anything, especially anything that only make the poors poorer.

Nothing must stand in the way of the "wealth effect" from Yuong Ha's brainchild property bubble.

The government has long ago run out of feet to shoot.

Thanks Roger for the excellent commentary. Much appreciated.

Great article

What I have noted (80% of the time - to provide a sense of prospective) in my almost ten years of following movements between the US$ verses the kiwi, I have found that futures trading on the gold market sets the rate.

"They seem convinced that strong consumer spending financed by increasing debt on appreciating house prices is a sustainable economic model.

They are all far too optimistic on the economic outlook in this writer’s opinion... "

Nail on head.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.