Summary of key points: -

- Are we there yet? Likely market reactions to the end of the Iran war

- New era of transparency and accountability at the RBNZ

The global financial and investment markets ended last week laying bets that President Trump will largely accept the latest proposals from the Iranians and signal and end to the conflict and an eventual reopening of the Strait of Hormuz. We are not there yet, as Trump will want to typically play games and screw the scrum to attract attention to himself and what he has achieved. The changing market positioning is predominantly seen in the oil futures market. The West Texas Crude Oil (“WTI”) futures index has progressively declined over this last week, as the speculative element in the market unwind their previous “long oil” positions entered over the last three months. We have always expected that oil prices would drop sharply on the confirmation that the war is over and the tankers would soon be transporting crude cargoes through the Strait to the refineries in Asia again. It does not require the physical supply of oil to return to normal levels for the market oil price to drop. There was always a very large amount of financial speculation in the pushing up of oil prices in early March, those punters (e.g. hedge funds) are still taking their profits and have to sell the oil futures to do so. The financial players are far more influential over short-term market pricing than the producers and end users hedging their price risk.

Over this last week the WTI oil price has decreased 8.00% from US$94.60/barrel to US$87.60 at the Friday close. Expect a continuation of the daily volatile movements at the Trumpmeister makes up his mind on the deal. It is likely that the Americans will compromise on certain aspects just to get a deal across the line as the political runway from Trump runs out. As anticipated, the US dollar value has followed the oil price downwards and will have further to go well below 98.00 on the Dixy Index when the deal is consummated. When the peace deal is reached, oil prices will likely decrease to well below US$80/barrel and maybe even below US$70/barrel. The markets are selling the USD in tandem with oil and as the oil shock becomes confirmed as relatively short term, the Fed can look through the adverse impact on US inflation and therefore return to interest rate cuts later in the year (USD negative).

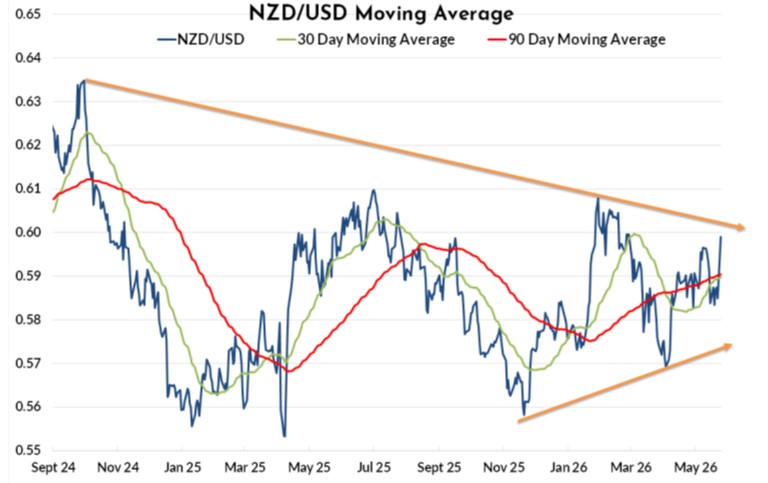

The strong movement higher in the NZD/USD exchange rate over the last week is instructive for the likely FX market environment for the Kiwi dollar over coming months. Further appreciation to well above 0.6000 is a growing probability due to: -

- Weaker USD on the global stage as oil prices fall further.

- The sea change in the RBNZ’s outlook on monetary policy (six months behind the Aussies).

- Investment/capital inflows into the NZ economy and the Kiwi dollar continuing to ramp up due to the Advanced Investor visa inflows, Invest New Zealand landing some foreign investor deals and more Kauri NZD-dominated bonds issues in the pipeline.

- Trans-Tasman currency traders unwinding their “short sold NZD/long AUD” speculative positions put on several months ago on the NZD/AUD cross-rate i.e. buying NZD, selling AUD to unwind, therefore sending the NZD/USD exchange rate higher on its own accord.

All strongly held views have risks associated with them. The largest risk to the stronger NZD outlook in this column is that Trump prolongs the war as he wants to be able to say that he extracted all the enriched uranium and ended Iran’s nuclear arms capability, to be awarded the Nobel Peace prize he so crazily desires. It is all about self-indulgent vanity and self-aggrandisement with the Donald!

The NZD/USD exchange rate has been trading within a “converging wedge” chart formation over the last three months, with the lows becoming higher and the highs moving lower. The pattern always leads to an inevitable break out. It looks like the Kiwi dollar is just about to break out the top side of the converging wedge and therefor that is a chartist signal for further gains. The 30-day and 90-day moving average lines have crossed into an uptrend as well (refer chart below).

New era of transparency and accountability at the RBNZ

All the double guessing and egoistic attempts to catch the financial markets off guard/wrong footed under the previous leadership regime at the RBNZ have suddenly disappeared in a new wave of transparency and accountability. The markets have Governor Anna Breman to thank for the reforms at the RBNZ, to move on from the unnecessary cloak and dagger stuff to a refreshing openness. There was considerable intrigue to see the disclosure of how each individual monetary policy committee member voted on the adjustment to the OCR interest rate last week. It was a close-run vote, indicating that the three external members of the committee subscribe to the strategy that if you pre-empt with early interest rate increases you cut off inflationary pressures early and inflation does not go as high in the cycle, as compared to delaying hikes. The Aussie economy is paying the price today with tight monetary policy because they did not tighten hard enough in 2022 (preferring to keep unemployment low) and allowed inflationary pressures to stay higher, for longer. The individual committee members responsibility for their respective views/stance, and their reasons behind those cited, is really good to see. The markets will hold each of them to account in respect to their ongoing performance, which is a paradigm shift from the previous way the RBNZ did things. It is true that the only real difference between the three external members who voted for an immediate OCR increase and the three RBNZ staffers who voted to wait, was one of timing. At the end of the day, it will not make a great deal of difference, as the OCR will be increased in July anyway and the interest rate markets are already pricing-in many more hikes in 2026 and 2027.

The more hawkish than generally expected statement was unequivocally positive for the Kiwi dollar and we saw buying of the currency on its own account over the subsequent 24-hour period. The NZD/USD exchange rate lifting from 0.5840 to over 0.5900. The NZD/AUD cross-rate jumping up from 0.8150 to a high of 0.8280. By week’s end, the weaker USD from falling oil prices had propelled the Kiwi dollar higher again to 0.5990 and 0.8340 respectively. The sterner and more stringent monetary policy signal from the RBNZ effectively marking the “start of the end” of the two-and-a-half-year period where New Zealand interest rates have traded well below those of the US, weighing the Kiwi dollar down in the 0.5600 to 0.6000 bottom of cycle range. The NZ/US two-year interest rate differential has closed up a long way already and looks set to close to zero as US two-year market interest rates decline further on the expected ending of the war.

As covered in the RBNZ’s statement, there are endless permutations and scenarios of how the Iran war, and the related oil shock, plays out in terms of higher inflation and lower GDP growth in the NZ economy. What we do know today is that President Donald Trump’s political runway has all but run out (despite what he says), resulting in the probability increasing of oil prices decreasing and the US dollar value following them down, as we are now witnessing.

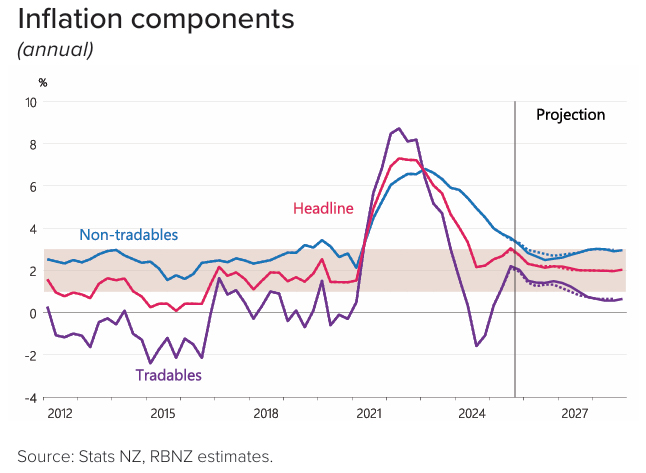

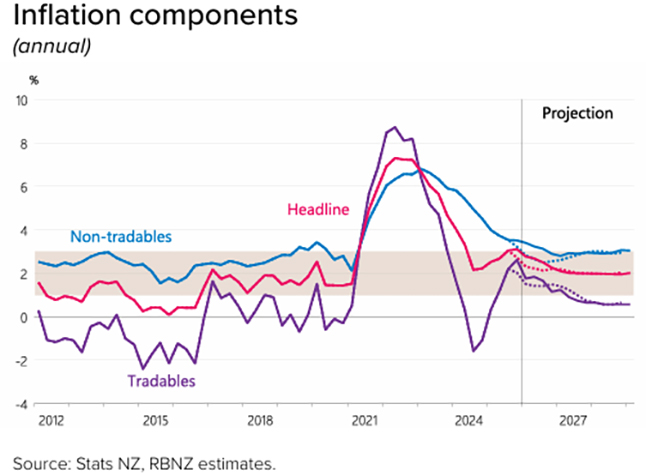

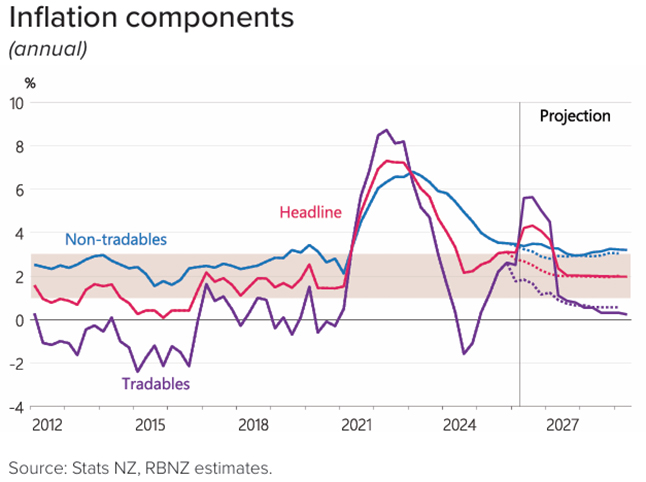

A disconcerting feature of the updated RBNZ inflation forecast published last week was that they are no longer forecasting non-tradable/domestic inflation to reduce in 2026 due to excess spare capacity in the economy. If you dismiss the impact of the Iran war/oil shock entirely and examine the RBNZ’s forecasts for non-tradable inflation on 26 November 2025 through to 27 May 2026, they have abruptly U-turned from forecasting a decrease to 2.50% (blue line in the three charts below) to now forecasting an increase to 3.50%. The cutting of the OCR to 2.25% last November was based on the excess capacity in the economy driving non-tradable/domestic inflation much lower. It never happened and will not happen in the future. New Zealand’s perpetual “administered” price increases are immune to general economic conditions. The RBNZ should have worked that out by know!

We always viewed the RBNZ’s assessment of considerable excess capacity in the economy driving non-tradable/domestic inflation lower as being based on flimsy data and “hope”, rather than a good understanding of how the public sector and the cloistered parts of the private sector set their prices in our economy. As this column has repeatedly highlighted over many years, inflation control is just so much harder in New Zealand due to the lack of true market competition in so many of our industries (domestic airlines, banks, electricity, insurance and building products).

It is becoming apparent that the new RBNZ Governor is already receiving a sharp lesson in some of the challenges with maintaining our inflation rates close to 2.00% without causing a recession. The previous Governor was quite happy to be the cause of both the booms and busts in our economy.

Follow the shift in the blue line in the three charts below to visualise the RBNZ’s U-turn on non-tradable inflation forecasts. What is also now very apparent is that the slashing of the OCR to 2.25% last November was a policy error, even before the war/oil price factors came along in March.

RBNZ MPS, 26 November 2025

RBNZ MPS. 18 February 2026

RBNZ MPS. 27 May 2026

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.