Summary of key points: -

- The markets interpret the Fed message as hawkish at the start of the Kevin Warsh era

- Kevin Warsh kicks the can down the road on Fed reforms

- NZ economic performance stronger than reported and realised

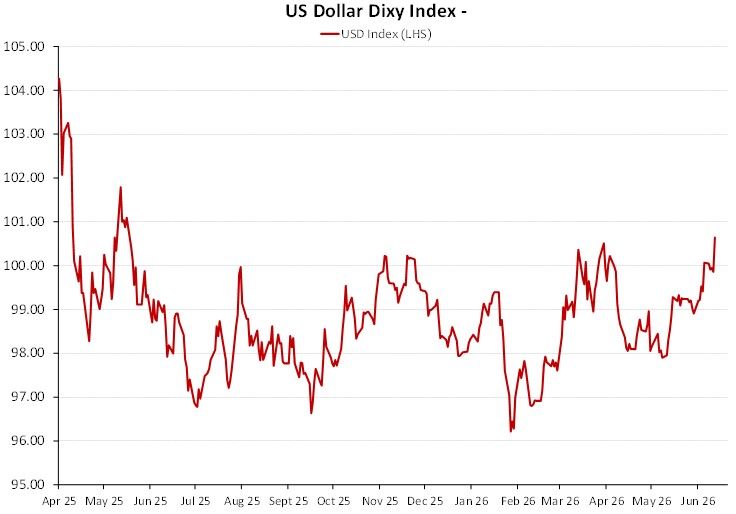

The immediate reaction by the financial and investment markets to Kevin Warsh’s first meeting as the US Federal Reserve Board Chairman was instantaneous and conclusive, sending the US dollar currency value to its highest level since March 2025 (100.60). The markets interpreted the statement and following media conference as a clear pivot by the Fed to a decisively more hawkish monetary policy stance to drive inflation back to the 2.00% target. Without wanting to provide any forward guidance as to likely future Fed actions, Chair Warsh made it very clear that their top priority was to reduce the annual inflation rate to 2.00% and that it was not acceptable that the inflation rate had been consistently above that target over the last five years. US interest rate markets are now pricing-in two 0.25% interest rate hikes by the Fed by the end of the year with the two-year Treasury Bond yield sold higher to 4.18. The US dollar appreciated on the more hawkish than expected Fed message and the prospect of higher US interest rates.

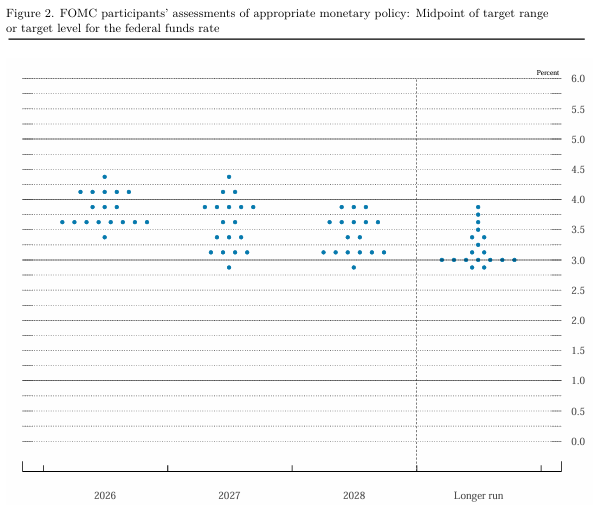

Fed members lifted their 2026 and 2027 inflation forecasts in reaction to the higher energy prices caused by the US/Iran war. The “dot-plot” of where individual Fed Board members forecast the Fed Funds interest rate to track over the balance of 2026 and into 2027 and 2028 was divided as ever (refer to the chart below). Nine of the 18 Board members see the Fed funds interest rate increasing once or twice x 0.25% over the course of 2026 from the current 3.50%/3.75% setting. Nine members see the interest rate being stable or 0.25% lower this year.

What we do know is that the majority of the Fed members would have submitted their inflation and interest rate forecasts before they had the information that the US and Iran had electronically signed a “Memorandum of Understanding” agreement to end the war and recommence shipping of oil through the Strait of Hormuz. As oil prices tumble in response to that news, it could have been expected that a good number of the Fed members may have adjusted their inflation and interest rate forecasts lower than what they submitted.

It is purely coincidental that the timing of Kevin Warsh’s first Fed meeting was at the very time the war has ended and oil prices are plummeting as we expected them to. Our long-held view was that when the war ended, oil prices would plunge back to below US$70/barrel and that the US dollar would follow oil prices down as US inflation would reverse lower as fast as it went up over the last three and half months. The Fed stance being interpreted as more hawkish has usurped our forecast of a lower USD and therefore a higher NZD/USD exchange rate.

The question to ask now is whether the financial and investment markets are correct in their immediate assessment that US interest rates will be increased this year? If they are right, the US dollar will retain its gains to above 100.00 on the Dixy Index. However, if the track of US inflation over coming months does not increase as 50% the Fed members expect, but actually reduces sharply on falling oil prices, the USD will reverse its recent gains and depreciate on the US interest rate markets unwinding their recent increases.

The USD Dixy Index has traded to above 100.00 on four previous occasions over the last 14 months and each time it has not been able to sustain the gains and has fallen back down again. Whilst our view that the US dollar would deprecate on falling oil prices has not played out as anticipated, we do not see the USD continuing this latest bout of strength. It will require clear evidence that US headline and core inflation are reversing sharply downwards for the USD direction to turn around. We believe that the US inflation reversal will come much earlier and in a more dramatic fashion than what most expect at this time. Fed Chair Kevin Warsh is absolutely correct when he states that he wants the financial markets to be solely reacting to economic data as it evolves and not distorting their pricing by factoring in what the Fed might do or might not do. Hence his reluctance to provide forward guidance on likely future Fed actions. We expect the US interest rate markets to reverse their pricing of higher Fed Funds rates this year when the evidence comes through of sharply lower inflation outcomes over coming months.

The foreign exchange and interest rate markets consistently react to the immediate media headlines of Fed statements or economic data releases. However, as with everything, the devil is in the detail. Therefore, it pays to examine the detail of the component parts of US core inflation (food and energy prices excluded) if you wish to formulate an accurate forward view of where the annual inflation rate will travel over the next six months.

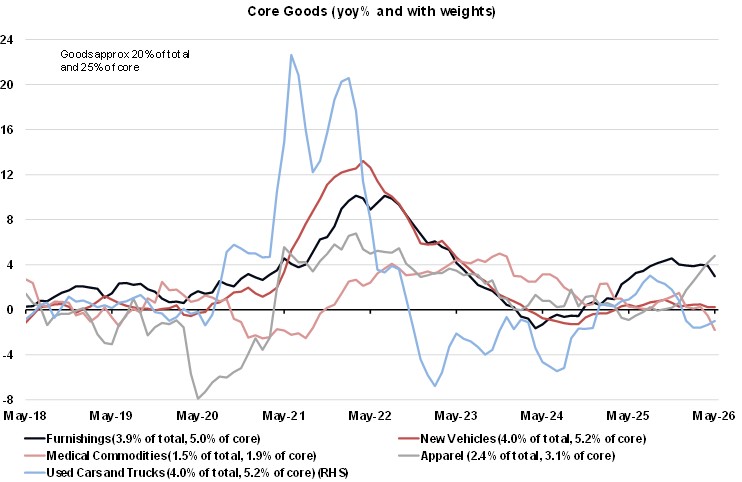

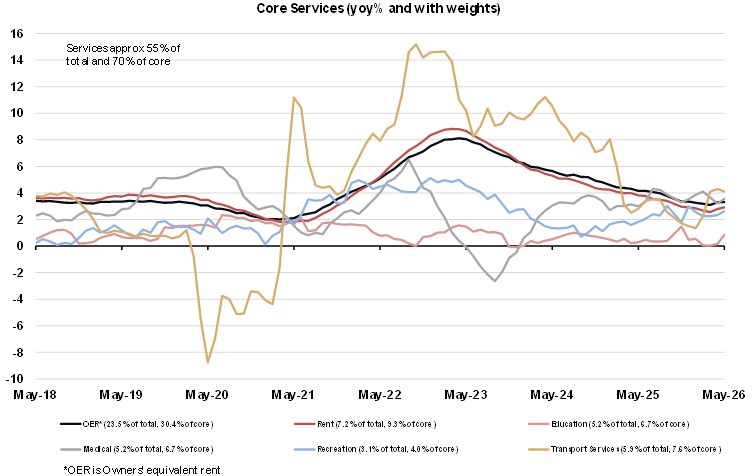

The two charts below of core goods and core services inflation in the US highlight the following trends: -

- With the exception of apparel, the annual price increases of imported goods such as furniture, motor vehicles and medical commodities are all turning down again as the tariff related increases of 12 months ago fall out of the measure.

- Core goods only comprise a weighting of 25% of total core inflation, however these annual price increases are now reducing.

- The transport services prices (largely airfares – gold line in the second core services chart) will now reduce sharply with falling oil prices.

- Rents and Owner’s Equivalent Rent making up a whopping 40% of total core services inflation (black and red lines in the second chart) have levelled off over recent months, however they seem set to reduce further to 2.00% pa over coming months as actual market rents have continued to decline over the last 12 months. The official “shelter” CPI (rents) data is inexplicably delayed by 12 to 18 months.

- History tells us that US business firms typically increase their prices over the first three months of the year and keep prices relatively stable over the remainder of the year.

The Fed preferred measure of US inflation, the PCE Price Index for the month of May is due for release this Thursday 25th June. Core PCE prices are forecast to increase by only 0.20% in May, with the headline increase estimated at +0.40%. There will be renewed market focus on the inflation results over coming months as evidence is sought on how quickly the tariff and oil related increases are unwinding. Wage increases in the US remain on a downward path from above 4.00% pa 12 months ago to 3.40% currently.

Inflationary pressures are not coming from wages, oil and tariff forces are reversing, so just where are the inflation increases that some Fed members are now forecasting coming from?

Kevin Warsh kicks the can down the road on Fed reforms

New Fed Chair, Kevin Warsh had previously stated that he would implement radical reforms at the US Federal Reserve to change its focus, operating processes and modernise the institution. At the media conference following the Fed’s meeting last week he outlined the setting up of five task forces with outside subject experts appointed to review and recommend on the following areas. The task forces will report by year end. In essence, Mr Warsh has kicked the can down the road on important issues that the markets were expecting some immediate changes to be announced. The more likely probability now is that Warsh will attempt to keep the Fed “on hold” with any interest rate changes until he has the recommendations back from the task forces.

- Review of the Fed’s framework for communication. Do they still hold the media conference where the Chair represents the Fed meeting discussions to the world? Do they provide any forward guidance with the SEP economic and interest rate forecasts? Do Fed members still make speeches with their own views expressed?

- Balance Sheet policy. How and when does the Fed sell Treasury Bonds it holds to reduce the size of its balance sheet? Would they sell bonds, which would push long-term interest rates higher, at a time when inflation is falling, and they may be contemplating cutting short-term interest rates?

- Sources of economic data. We have highlighted the poor quality of US employment and housing cost data previously, with large historical revisions and long lags. Mr Warsh rightly points out that “live-real time” data on the economy is now possible. Inflation in the US would be much lower today if they used current market house rental data.

- The impact of AI on productivity and jobs. The theory is that AI processing will reduce business costs and therefore reduce prices. Good for the Fed’s inflation mandate, however as AI replaces jobs, bad for the Fed’s full employment mandate.

- The inflation target framework. Is the 2.00% target still appropriate, given that they US inflation has been above that level for the last five years and below the 2.00% level for the five years prior to 2020?

The objective to reduce the size of the Fed’s balance sheet is having the largest impact on current interest rate market pricing. The chart below suggests that US two-year Treasury Bond yields should be decreasing as inflation expectations reduce, however they remain elevated at 4.18% as the market worries about the Fed selling large volumes of bonds.

NZ economic performance stronger than reported and realised

Even though New Zealand’s GDP growth data is released nearly three months after the end of the quarter, last week’s March 2026 quarter release was very instructive as to the performance of the economy since mid-2025. Since July 2025 the economy has expanded by +0.90%, +0.50% and +0.80% respectively over the three quarters to 31 March. A strong and sustainable economic recovery, not the “fledgling”, “fragile”, “gradual” and “uneven” labels attached to the recovery by the RBNZ and local bank economists at the time. Because the return to strong economic growth was not powered by rising house prices and immigration, most did not recognise it or understand it. If the RBNZ had recognised the strength of the export-led recovery they would not have slashed the OCR to 2.25% in November last year.

Off course, the US/Iran war that started in March and the related energy crisis has delayed New Zealand’s growth momentum, however not derailed it (as Finance Minister Nicola Willis correctly points out). The business and consumer confidence surveys have plummeted over the last three months. However, that does not mean the economy falls back into another mini recession. We would expect a rapid bounce back in the sentiment surveys over coming months.

We are already witnessing a stronger economic impulse coming though some of the high-frequency data of late: -

- Job adverts through Seek are at three-year highs.

- Electronic card spending was up 1.70% in the month of May, well above prior forecasts of +0.40%.

- Building permits increased 10.90% in April, against a forecast for a 3.60% contraction! Building permits are up 16.00% over the full 12 months period.

The RBNZ’s GDP growth nowcast indicator for the June quarter has improved from a -0.30% a few weeks back when the surveys were so negative, to now record a +0.10% growth indication as the actual consumer, export and labour data comes in stronger. Housing and construction remain a detraction from overall GDP growth. The nowcast forward indicator for the September quarter is a return to a robust 0.80% expansion.

We await retail sales and employment data to confirm that the geo-political risk impact on the NZ economy this year was relatively minor and fleeting. The US dollar side of the NZD/USD exchange rate will continue to dominate the short-term direction, however our improving economic fundamentals will eventually be recognised and reflected in the NZ dollar exchange rate value. NZ interest rates rising to above US interest rates over the next six months would help!

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

1 Comments

I'm amazed at how little coverage the weakness of the NZD is getting - particularly against the AUD, where we are at 15-year lows. That's a 15%+ tax on every item imported, every holiday to Sydney or the Gold Coast.. or on buying a house there, if you want to follow the herds making that move. The quiet devaluation...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.