Economists see the Reserve Bank still having much more work to do with its stimulatory quantitative easing programme in future after inflation dropped by 0.5% in the June quarter.

The fall, as measured by the Consumers Price Index (CPI) was the first quarterly decline since 2015, according to Statistics New Zealand.

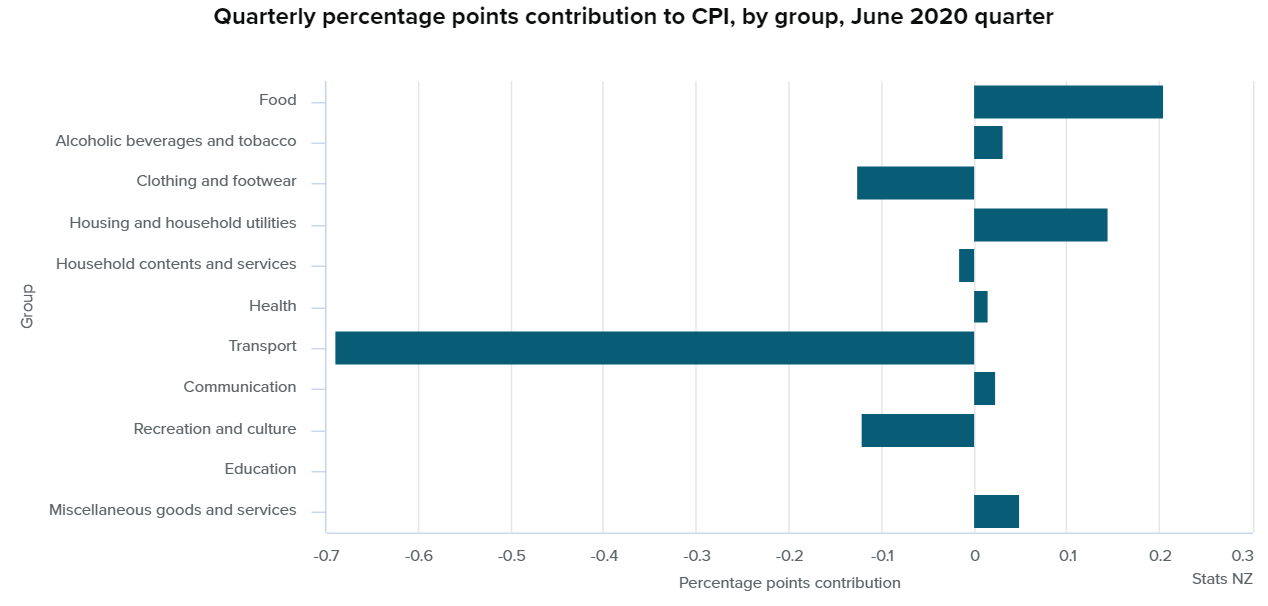

The drop, largely driven by lower fuel prices, was at the smaller end of economists' estimates. The Reserve Bank (RBNZ) had picked a 0.7% drop.

The quarterly decline in inflation brought the annual rate of inflation down to 1.5% from the eight-year-high of 2.5% that was hit in March.

Economists' reaction

Westpac senior economist Michael Gordon said he expected overall inflation to slow further, bottoming at around zero by early next year.

"More importantly, we think that inflation will be slower to return to target than the RBNZ is forecasting. It’s likely that the economy will be running below its full potential for several years to come (largely due to the loss of international tourism), and employment will remain well short of its maximum sustainable level. With both of the RBNZ’s mandates arguing for more action, the path ahead is clear."

Gordon said with the outlook for weak inflation and higher unemployment, there is nothing to stand in the way of further easing measures by the RBNZ.

"We expect an expansion of the RBNZ’s bond purchase programme in the coming months, and a move to a negative OCR [Official Cash Rate] next year."

ASB chief economist Nick Tuffley and senior economist Jane Turner said while they currently expect inflation to remain positive over 2021, "we can’t rule out the risk of deflation and the RBNZ must remain vigilant".

"In saying this, the RBNZ (along with most economic forecasters) will be pleased by economic developments to date.

"We expect GDP to be 5% below year-ago levels by December 2020, which is in line with the RBNZ’s May [Monetary Policy Statement] forecasts. However, if the economy proves weaker than expected heading into 2021, and more policy stimulus is required, we believe the RBNZ will opt to increase its Large Scale Asset Purchase programme [quantitative easing, or QE] or lean on other policy measures and leave the option of a negative OCR as a last resort."

ANZ senior economist Miles Workman said the medium-term outlook for inflation (and employment) will be making the RBNZ very concerned.

Inflation to run below target

"We expect headline CPI will be running below the 1-3% target band by year end," he said.

The NZ dollar's value is elevated, world prices are seeing deflationary pressure, inflation expectations are at record lows, and labour market capacity is set to increase markedly, he said.

"The RBNZ has a momentous battle on its hands. Without further action or a significant change in the economic outlook, the risk of a persistent undershoot [in the inflation target] is likely to materialise.

"Overall, despite the CPI coming in a touch stronger than we forecast [ANZ forecast was -0.6%], we got what we expected: A volatile read on quarterly inflation with evidence that there’s more volatility to come.

"Looking through the noise, there’s also confirmation here that the underlying inflation pulse is as weak as a kitten."

Capital Economics Australia and New Zealand economist Ben Udy said non-tradeable prices were flat in the June quarter "and we think they will struggle to gain much momentum in the coming months as spare capacity in the labour market weighs on wage growth".

"The upshot is that both headline and underlying inflation are set to fall below the 1% lower bound of the RBNZ’s target in the coming months. And we think sustained weakness in inflation will force the RBNZ to cut [interest] rates into negative territory next year."

'QE programme to increase in size'

Kiwibank economist Mary Jo Vergara said a return to the RBNZ’s 2% inflation target 'mid-point' is a long way away.

"Based on our forecasts, it will take at least two years to return to full employment (around 4%) and stable inflation (around 2%). And that’s without further shocks.

"With both mandates unlikely to be met in the next two years, the RBNZ has more work to do to ensure the recovery is sustained. We expect the RBNZ to expand the LSAP [Large Scale Asset Purchase] programme into 2022 (from May 2021) in August, and take the total amount towards $100 billion ($90 billion on NZ Government Bonds, $10 billion on council debt)."

At the moment the LSAP programme is set at $60 billion.

"The programme is likely to hit $120 billion into 2023. But that’s not all they can do. The next best policy tool would be a term funding facility for banks. Cheap term funding will lower all bank rates (deposit and lending) immediately. Indeed, deflationary pressure demands monetary policy to remain expansionary for the foreseeable future," Vergara said.

The RBNZ "are far from finished," she said.

Stats NZ said the Covid-19 global pandemic saw cheaper petrol and falling hotel and motel prices.

Overall annual inflation was affected by Increased prices for rent, and cigarettes and tobacco, partly offset by lower petrol prices.

It was the first fall in quarterly inflation since the December 2015 quarter when there was also a drop of 0.5%.

“The Covid-19 pandemic has created a lot of volatility and uncertainty,” prices senior manager Aaron Beck said.

“These have resulted in some large price fluctuations as well as several measurement challenges.”

Out of gas

Petrol prices fell 12% over the quarter. This is the biggest quarterly fall in petrol prices since the December 2008 quarter.

“Global crude oil prices fell sharply over the first four months of 2020 reaching a low point in April,” Beck said.

“International lockdown restrictions and global economic uncertainty have greatly reduced international demand for crude oil, driving prices down at the pump.”

The average price of 91 octane petrol was $1.83 a litre this quarter, down from $2.09 last quarter. The June 2020 quarter price is the lowest quarterly price since the September 2017 quarter.

Petrol excise duty and increases in road user charges were implemented on 1 July 2020 and will be reflected in the September 2020 quarter data.

Domestic or non-tradable inflation increased 3.1% in the year to June 2020. It is the fourth consecutive quarter where it was above 3% on an annual basis.

The latest annual increase was influenced by higher prices for rent, cigarettes and tobacco, restaurant meals and ready-to-eat food, and property rates.

Non-tradable inflation measures goods and services that do not face foreign competition. It includes housing-related costs such as rent, construction, property rates, and many domestic services.

Consumer prices index

Select chart tabs

25 Comments

So non-tradables inflation hasn't budged - running at 3% still. Stagflation anyone?

don't worry, councils can save from a deflationary fate.

Agreed, a collapse in business investment sentiments could make the stagflation worse from here on, unless the government stimulates capital investment in housing construction, power & transport infrastructure, etc.

Stagflation has been predicted by quite a number of people (following a period of deflation - I guess we're seeing disinflation in some areas now).

Inflation had its first quarterly drop since 2015, dropping 0.5% in the June quarter, according to Statistics New Zealand.

So, $18.347 billion of RBNZ QE "money printing", over the same quarter, produced nothing but deflation. Time to call it quits and really find out why monetary conditions are tight when interest rates are at record low levels.

Japanification?

Possibly - I watched Princes of the Yen again a few weeks back. The whole story around vested interest that pushed debt and asset prices so high just rings so true across many countries today, including NZ. And the same entities are in on it, for their own vested interests, be it central banks, retail banks, governments and some groups of individuals/businesses. It really could be bad for the country long term.

Yip makes you think that what we're doing isn't working - but I'm guessing that central banks are just going to keep doubling down further on this failing strategy. Its a pretty risky game as well in my view, as the economy keeps getting weaker but asset prices stay sky high. It really could turn into a complete wreck.

Michael Reddell observed that in previous crises to OCR has been cut by around 500 basis points. Compared with the 75 points we got, who can blame people for not spending more - as a proportion of the OCR the cut was large, but not enough in real terms to make much of a difference anywhere. Orr himself said less than a year ago that bond buying etc wasn't a particularly effective tool, but that's what they've gone with.

I think central banks have got to the point where they realise no matter what they do its likely going be bad - even if they aren't publicly saying that.

If they do nothing - we have deflation and debt defaults.

If they keep doing what they are doing we may have rising inflation and high unemployment - stagflation. Which again may result in debt defaults if/when interest rates rise.

Time for the Politicians to front up with workable policies not just hot air and hope this works

MMT suggests that too low inflation means not enough money in circulation. If this is true where is all the money going? Are the banks vacuuming it up through their housing ponzi?

Look at the correlation between money supply and share/property prices. So basically the inflation has gone into capital prices not consumption prices - yet we measure inflation in CPI via consumption - then wonder where inflation has gone and keep dropping interest rates further to try and find some inflation - then share/property prices go higher, and the issues get worse and worse...until it all folds in on top of itself (possibly somewhere near you soon!)

Land is excluded from the CPI - only new home build costs is included. Yet its land values that have had massive inflation! If land was included in our inflation measurements, interest rates would have been rising not falling and we wouldn't have a property/debt bubble now. But we haven't....so now we're really at risk of it all collapsing.

My view is that CPI targeting at the 1-3%, using the current inputs, isn't going to work long term. It will cause bubble/busts like what we've just witnessed.

Your thinking is good. The CPI construct has been very destructive as an instrument for deciding policy.

...for example I believe that free public transport during the lockdown is included in the CPI figure. When almost nobody was taking public transport. How stupid is this!

100% correct thinking.

I think that the "powers to be" know very well what you are talking about - they are just ignoring it because of vested interests.

Well they can't publicly say it because then it would mean admitting that the current economic system isn't sustainable.

"Westpac senior economist Michael Gordon said the inflation result "does not alter our view that the Reserve Bank will need to keep monetary settings loose for a long period".

Low Interest rates aren't 'loose' Monetary Policy! They are tight policy.

The lower interest rates go, the LESS banks will lend to FEWER creditworthy customers. And the more people will SAVE and REDUCE spending.

Hasn't that sunk in yet!?

Yip so many things are the opposite of what people have been lead to believe they are.

if you want inflation, pump cash rather than credit. QE through institutions creates credit/debt/inflated asset price, which suffocates CPI inflation and widens wealth gap. It's been this way since GFC. Time for UBI.

Please wake up: QE does not raise inflation. Look at USA. QE keeps interest low on gov debt

How do you know QE didn't prevent deflation though? We will never know the counter-factual, creating inflation is the easiest financial outcome there is, just ask Zimbabwe or Venezuela. QE is much more about funding, liquidity and keeping the credit premium contained than directly creating inflation. I recall one of the classical economists saying inflation happens very slowly at first, and then very quickly.

I note no reading for education on the graph? Has it stopped?

The great capitalist age is almost over. The game has been played hard & the winners are the bankers & the 1%. There's another 10% doing okay while the rest of us have slipped or stayed where we were. Remember its a global game, we're not the only ones to be fooled. The question is, what are the alternatives? Crash & do it again? That's been the plan for the last 40 years. Maybe not. Crash & reset? What does reset mean exactly?Forgive all debts in a once in a jubilee lifetime (70 years)? Hang on a sec, I'll just take out another mortgage. Bust open all the trusts & tax them? That'll be popular. Not. Declare war on the tax havens? Mmmm! This one has possibilities. Probably better fighting them that fighting China. Would we be wiser to wait for the second coming? Sigh! Have you read Revelation?

" Westpac senior economist Michael Gordon said he expected overall inflation to slow further, bottoming at around zero by early next year."

So this is exactly the same as saying there is zero deflation , but no one dare use the D word , I have news for them :-

ZERO INFLATION IS THE SAME NUMBER AS ZERO DEFLATION .

My bet is that is going to be at least 1 % deflation soon enough

Here's a thought - since they've already tried this in Japan and it didn't work, how about we stop QE and see if inflation becomes worse. I'd bet the answer to that is it makes no difference.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.