As Reserve Bank Governor Graeme Wheeler and his team get ready for this week's Official Cash Rate (OCR) review and prepare their Monetary Policy Statement (MPS), they're dealing with two issues the central bank hasn't faced for some time.

The first one, as Westpac's acting chief economist Michael Gordon puts it, is not how to return inflation to the 1% to 3% target, but how to keep it there. And the second one is mounting evidence a housing market slowdown is more than temporary, and the potential impact this could have on consumer spending.

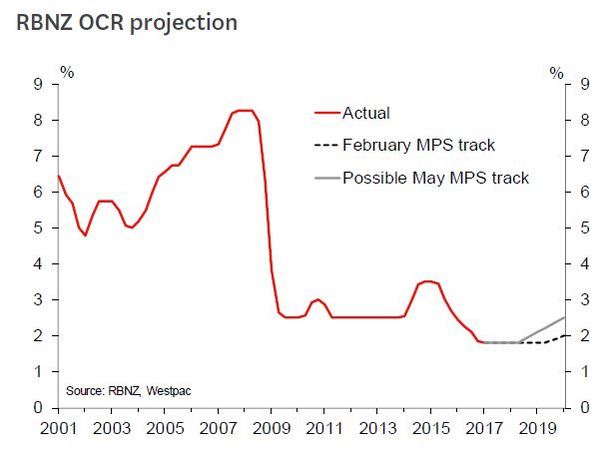

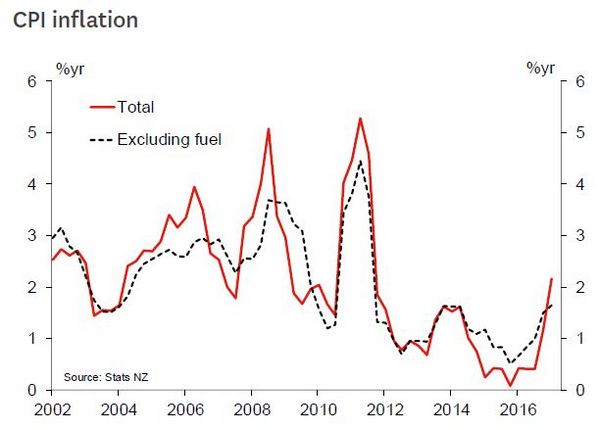

The Reserve Bank is expected to leave the OCR unchanged at its record low of 1.75% on Thursday morning, where it has been since November last year. But with the latest inflation data showing inflation rising to 2.2%, economists are picking the central bank will bring forward its previous forecasts for future OCR increases from late 2019.

Here's a look at what some of the major bank economists are saying in their OCR and MPS previews.

Here's what ASB's economists say.

We expect another on-hold decision from the RBNZ, with the OCR unchanged at 1.75% for the third meeting in a row. Inflation has continued to firm since the February MPS, which will comfort the RBNZ, both in terms of mitigating the risks of low inflation and also in terms of aiding an increase in inflation expectations. There are, however, a number of risks to the outlook, including the potential for US President Donald Trump’s policies to adversely impact NZ growth and inflation.

We expect the RBNZ’s OCR track to show a slightly earlier start to future OCR increases compared to the February MPS. This after the Q1 CPI firmed to 2.2% yoy from 1.3%, with non-tradable inflation also stronger than the RBNZ had anticipated. However, we continue to expect the track to show that any change in the OCR is still a long way off.

Once again, the RBNZ needs to walk the tightrope of being encouraged by recent developments in inflation, but not so enthusiastic the market brings forward even further its expectations of an OCR hike. To this end, the RBNZ will again be looking to strike a neutral tone in its statement. There is also likely to be a slight tweaking of the language around the NZD, considering its recent depreciation.

ASB's economists predict the Reserve Bank will drag forward its forecast for increasing the OCR by six months to mid-2019.

We look for the RBNZ to lift its inflation outlook, particularly for the year ahead. The medium-term track is likely to be a bit closer to 2% than was published at the February MPS. The RBNZ’s published OCR track will be much watched. In the February MPS this was lifted to 1.8% for the near term, rising to 1.9% in late 2019 and hitting 2% in early 2020. We do not expect to see any change in the near term.

Further out, we look for the first signs of tightening to be pulled forward at least 6 months, to mid-2019. Should the track be pulled forward into late 2018, the market is likely to read this as a hawkish signal, prompting a market reaction. The language the RBNZ chooses to employ is likely to have a significant impact. We expect no change to the ending of the statement: “Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain, particularly in respect of the international outlook, and policy may need to adjust accordingly.”

Any adjustment here could bring forward market pricing for the timing of the next interest rate hike. The language around the NZD is likely to be tweaked, given the NZD’s continued under-performance in relation to the RBNZ’s forecasts. At the March OCR Review the RBNZ said the NZD’s depreciation was “an encouraging move, but further depreciation is needed to achieve more balanced growth.”

Given the NZD has softened further since that statement, we could see a tweak towards “The further depreciation in the NZD since March is encouraging, but further depreciation is desirable to achieve more balanced growth.”

In their latest Strategist report BNZ's economists suggest the Reserve Bank may choose to "look through" much of the recent data if it still views the world as uncertain as it did in March.

There is next to zero chance of the RBNZ moving the OCR at this meeting. All the interest will be in how the Bank accommodates the unexpected economic information such as much higher CPI inflation and a meaningfully lower NZD. The latter, importantly, occurring in spite of general improvement in NZ’s major export commodity prices and thus adding to the inflation outlook.

We think those developments outweigh the likes of slower economic growth and higher retail interest rates on the inflation outlook. It all should be enough to lessen the chance of a cut in the Bank’s mind and bring forward the projected tightening from the very late 2019 zone that the RBNZ previously projected. Look for the former in the Bank’s language and the latter in the new set of forecasts.

However, the Bank is unlikely to move as far as what the market currently has priced. The Bank may well choose to look through a lot of the recent data if it still considers the world to be as uncertain as it did in March.

In their preview Kiwibank's economists say they now expect the Reserve Bank to start increasing the OCR at the end of 2018 instead of mid-2019. However, they argue Overnight Indexed Swap (OIS) market pricing, with a 25 basis points hike priced in by March next year, is too aggressive. The Kiwibank economists also argue that financial markets are under pricing the risk of political disruption, with the Reserve Bank expected to remain cautious about global risk events.

In terms of the global economic outlook, the Bank noted in the March OCR Review that it was encouraged by recent positive economic data coming out of developed economies. But once again, the RBNZ expressed concern that “…major challenges remain with on-going surplus capacity in the global economy and extensive geo-political uncertainty.” Since March these concerns have remained in play despite some risk factors moving closer to resolution.

In France, polls suggest that pro-EU centrist French presidential candidate Emmanuel Macron is the favourite to win in the final voting round on May 7, reducing the risk of a victory from populist candidate Marine Le Pen. However, other risks factors have arisen, such as geopolitical tensions on the Korean peninsula. Moreover, uncertainties surrounding US fiscal and trade policy are still no closer to being resolved.

The Trump administration recently released a one-page outline of their proposed tax package, which included a substantial cut to the corporate tax rate from 35% to 15% and streamlining of personal income tax brackets from seven to three. While the current outline is bold and has the potential to lift global growth and inflation, markets are no clearer on some of the key features of Trump’s fiscal policy. Markets remain in the dark about how the administration intends to pay for these cuts.

A key outstanding concern for the global economy and NZ is the possibility that the US administration looks to offset lower tax revenue by increasing import tariffs. Financial markets appear to be under-pricing the risk of political disruption, with the VIX index (a proxy for investor risk aversion) at the lowest levels since the GFC. Credit spreads are also nearing pre-GFC levels in many regions. Given the numerous global events on the horizon, this pricing seems too low in our view. We believe that the RBNZ will maintain a cautious stance to global risk events in the May MPS.

In Westpac's preview acting chief economist Michael Gordon says although the OCR is expected to be unchanged, there should be a stronger signal that the next move will be up. Gordon argues the conclusion from both the February MPS and the March OCR review that “monetary policy will remain accommodative for a considerable period”, with the Reserve Bank suggesting the OCR could remain on hold until late 2019, is no longer tenable.

We expect the bottom line in next week’s statement to be more along the lines of: “Monetary policy will continue to be accommodative, to ensure that medium-term inflation remains near the 2 percent midpoint of the Reserve Bank's target range.” We expect the RBNZ’s interest rate projections to be more consistent with an OCR hike by late 2018. This would probably be neutral for financial markets on the day: an earlier start than previously signalled, but stopping short of endorsing market pricing for a hike by March next year.

In a speech in March, RBNZ Governor Wheeler concluded that the risks around the OCR were evenly balanced, with downside risks from the global environment but upside risks from the domestic economy. In particular, the Governor emphasised the uncertainty around the Trump administration’s policies, and the risk of a marked rise in trade protectionism. The RBNZ’s concerns about the global backdrop will probably remain. Forecasts of world growth have generally been revised up in recent months, but inflation (setting aside the rebound in oil prices over the last year) remains subdued. Moreover, US government policy is perhaps even more worrying now – the odds of a large fiscal stimulus in the near term are growing dimmer, while the risk of a wave of trade protectionism is very much at the forefront.

On the domestic front, the biggest development for the RBNZ is that inflation has risen much quicker than the RBNZ expected. After lingering at near-zero levels for much of the last two years, annual inflation rose to 2.2% in the March quarter – well ahead of the RBNZ’s forecast of 1.5%, and a level that it hadn’t expected to see for several more years.

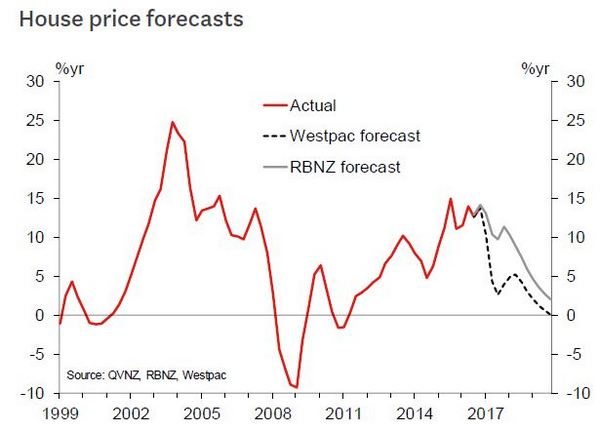

Gordon also points out that house price growth has slowed sharply since August, and flattened out completely in previous hotspots like Auckland and Tauranga. This was highlighted both in the latest QV data and Barfoot & Thompson sales figures, out last week. He attributes this to loan-to-value ratio restrictions the Reserve Bank introduced for property investors last July, and mortgage rate rises. And Gordon suggests, this is already hitting consumer spending.

To date the RBNZ has treated the housing slowdown as temporary, “given the continued imbalance between supply and demand”. But the evidence is now too strong to dismiss.

While the RBNZ may be pleased to see a cooling in the housing market from a financial stability perspective, it presents a real challenge on the monetary policy side.

The RBNZ’s forecasts have relied on strong household spending, supported by rising house prices, to drive economic growth and a lift in domestic inflation. In February the RBNZ forecast an 11% rise in house prices this year; so far it’s tracking in the low single digits. And that already seems to be having an impact on consumer spending – for instance, card spending on durable goods has fallen in five of the last six months.

With inflation back on track earlier than expected, the RBNZ will no doubt be weighing up when it can start ‘normalising’ interest rate settings. But we’re wary that signalling too much in the way of rate hikes at this stage could push retail interest rates and the exchange rate higher, undermining the growth that the RBNZ is relying on to meet its inflation target.

4 Comments

The first one, as Westpac's acting chief economist Michael Gordon puts it, is not how to return inflation to the 1% to 3% target, but how to keep it there.

It's not within the RBNZ's range of capacities to determine the rate of CPI inflation. Banks create credit and society decides how the consequent GDP returns are divided up between citizen cohort groups.

Note Westpac's self-interested house price forecast doesn't drop below zero. It's not good for business to do so.

Whilst I tend to agree that the bottom could fall out quickly... in fairness...

Note: Westpac are still forecasting house prices to fall faster than the RBNZ's forecasts, and the RBNZ is an independent entity with no commercial imperative.

So there goes your argument really.

I still maintain that a monkey has the same odds predicting the OCR correctly 2 years in advance

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.