So, what should we invest in at the moment?

The question is not rhetorical. I want to know.

It might seem churlish to fret over declining investment returns at a time when businesses are under stress and people face losing jobs.

HAVING money might seem a nice 'problem' to have versus NOT having money. And yes, I know which camp I would rather be in. And who wouldn't?

But of course, with an aging population, the need for people to provide for their own futures has never been more paramount. And certainly, in terms of what to invest in, and how, I can't think of a more challenging time.

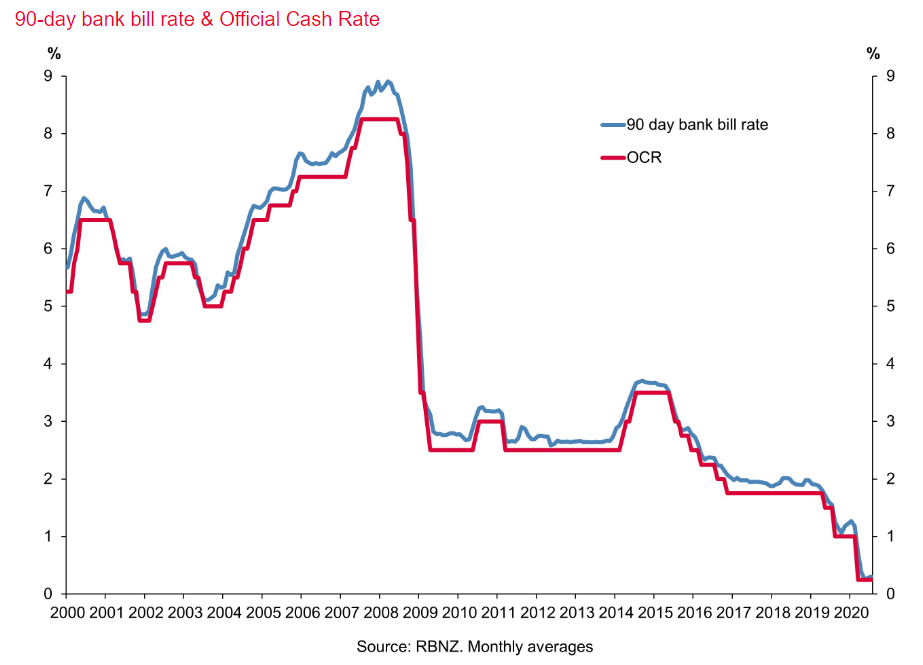

I last visited this topic in depth about a year ago, when I highlighted an interest rate of 2.22%, essentially as an example of how low things had gone. Well, you could only dream of 2.22% now! Look at this lot.

And, remember, the Reserve Bank is sending pretty clear signals it will likely move the Official Cash Rate (currently sitting at 0.25%) below zero early next year.

We are pretty much promised that the interest rates we receive from our banks won't go below zero as well (IE it won't cost US money to have a term deposit), but my goodness nobody's going to be getting rich on the interest rates we will see for the foreseeable future.

If the OCR does go as low as say -0.5% - as a number of economists are suggesting, then its difficult to imagine there will be any bank interest rates above even 1%.

In truth, we've been having to get used to ever decreasing returns from bank deposits for a while now.

If we look at say the average six-month rate offered by the banks, that has now not been above 5% since the end of 2008 - although obviously it's been dropping well below the 5% mark in more recent times. At the moment the going rate is about 1.3%.

If we go back just on 12 years (to mid-2008), six-month TDs were yielding 8%. A deposit of, say, $50,000 would have therefore yielded a pre-tax return of $2000. The same investment now at 1.3% would get $325% pre-tax.

So, the pre-tax return has dived from $333 a month to just $54 a month. You ain't retiring on that. Well, you ain't retiring on that and expecting to eat as well.

I've focused a bit on bank term deposits because they are 'safe'. They are investments that one does not imagine are 'at risk'.

Higher risk

Potentially much higher yielding investments, such as shares, have always been around. But of course they have higher risk.

The point is that for a long time in this country pretty nice returns could be garnered from those 'safe' investments, such as bank term deposits. Park money. Take interest. Live happily ever after.

Now it seems the need to manage risk is much greater.

It has to be appreciated that the range of things that can be invested in has been increasing rapidly in recent years, such as direct investment into things like index-tracking funds. Outfits such as Sharesies and InvestNow weren't around a few years ago and have been very happily embraced by the investor public.

A lot of us of course have KiwiSaver accounts.

There's peer-to-peer lending that enables you to effectively cut out the bank middleperson and lend directly to people, with therefore higher yielding returns, though again potentially somewhat higher risk.

And you can always take a walk on the hair-raising side and try something like cryptocurrencies. Ah, again, not without risk though. Oh, yes.

Saving is a redundant concept

What's happened though is that the old idea of 'saving' is now a pretty much redundant concept. Because you could get some sort of passable return simply by parking money in a bank, then that's what people did. And the idea of 'saving' was a very passive idea. Drop money in bucket and forget about it.

These days we have to think much more in terms not of 'saving' but 'investing'. Okay, you first need something to invest, which means rationing spending, but the point is that with an 'invest' mentality, it's a lot more active and there's rather more work involved.

I would like to think that as a nation New Zealand is improving its level of financial literacy, but goodness me, it needed to. It was a jarring shock to me that still resonates in terms of being a reporter covering the finance company sector meltdown roughly between 2006 and 2010.

The lack of financial literacy that meltdown revealed was frightening and the consequences for some people, reasonably significant numbers of people, were shattering.

What we have now is an environment where - certainly for the foreseeable future - we are all going to need to actively manage our 'savings' more than in the past.

So, financial literacy will be crucial.

Managing risk

The biggest shortcoming that I could see in and around the finance company sector meltdown was a very poor appreciation of the idea of 'risk' - what constituted 'high risk' and what was 'low risk'. And I'm still not sure it's a concept we get our heads around that well now.

With bank deposits having fallen by the wayside as a good income earner, management of 'risk' is now more important than ever, surely.

Okay, you might have noticed something missing from this article so far. Housing.

It's the perennial favourite with the Kiwi investor. Also, arguably, it can more closely resemble the idea of 'saving' or passive investment. Buy house. Sit on it. Watch the capital value grow.

It's hard to avoid the conclusion that the endgame from low interest rates will be even more focus on housing as a key mode of investment.

Indeed, I think we are already seeing the first signs of that.

And of course the risk you have with people flocking to buy assets, such as houses, is that the price of said assets gets squeezed.

Already as we look around us globally there are asset bubbles. Look at some of the share valuations and they certainly in many cases don't represent the current financial of the underlying companies. No they are reflective of demand. And the demand of course comes from plenty of money sloshing around looking for something to invest in.

Which is where we came in.

Testing times

As I said further up the article, having some money is a nice 'problem' to have. But I certainly can't remember a more testing time when it comes to deciding what to invest it in.

We come back to the whole 'risk' idea.

I think there's definitely a risk in us all following each other into bidding up the prices of assets.

Bubbles can keep inflating for a very long time and be remarkably sustainable for a long time. But usually there is some kind of circuit breaker that will pop them.

I do reiterate the concern I expressed in the article I did on this subject a year ago is that there a 'risk' that in search of higher yielding returns Kiwis will over-expose themselves to one of these bubbles.

And that could be bad.

Somehow or other we need to stay 'sensible' even as we are attempting to get investment returns that feel meaningful. Will we all be able to manage that?

79 Comments

Well, while the majority will scoff, Bitcoin has been among the best Covid-19 investments and the best investment over the past 10 years. Very few people will fully grasp and accept why that is. But the irony is that one of its key drivers is that it is positioned as a polar opposite as to how people think investments generate value.

Not saying that BTC will be the best investment going forward, but I'm also not saying that it won't be.

Fixed supply? a world-first if I'm not mistaken. Hedge funds are starting to get in on the action too

It's saying something that the first comment about search for yield is recommending something with no intrinsic yield at all and is simply pure capital speculation.

What’s the difference with a zero interest bearing bond?

It does have yield. There a dozens of lending platforms now offering interest rates and "defi" is becoming a big thing as well.

Hedge funds are starting to get in on the action too

Right. So let's assume that BTC is inherently worthless. Does that mean the hedge funds are taking the public for a ride?

Not at all, the funds are merely farming speculators.. that's what they do.

Aren't they always?

Absolutely.. speculators and sheeple

Just like Tesla etc. Check out the asset valuation versus the stock valuation versus Price/Earnings ratio. Very similar to Bitcoin

Yep, and I challenge any poo-pooers to read The Bitcoin Standard by Saifedean Ammous before commenting further.

You know how many bitcoin existed yesterday, you know how many were created today and you know how many will likely be tomorrow... as strange as it sounds, in time it will become a very safe investment for hedge funds based on actual solid predictable numbers.

With staking around the corner -ETH will outperform BTC in the near term anyway

ETH charging as we speak. Unfortunately only started to stack smallish amounts 18 months ago. Mind you, it's come on leaps and bounds and I'm in before the tourists have shown up.

I’m betting on ETH for this reason.

Imagine if aliens arrived and found us wasting vast amounts electricity to solve pointless maths problems for no other reason than to demonstrate “proof of work”. They’d call us dumb - and that’s even before they see the deluded DGM comments on this site.

No. They would call us irrational. If I thought irrational investment would make me money off dumb people, I would, and have done it.

Any different to the vast amount of energy required to mine gold?

Not much. Physical gold does have some uses.

The only way to make money on crypto is to be first in before the 'tourists'. That's all its good for. Its akin to NZ housing ponzi in that regard.

https://chrisgimmer.com/bitcoin-reserve-asset/?fbclid=IwAR16miwwy58rAcn…

Good starting point, sums up several good articles.

And hey, if you think you know better than the largest independent publicly-traded business intelligence company about Bitcoin, then good for you!

https://ir.microstrategy.com/news-releases/news-release-details/microst…

Well... I'd say Ethereum is doing even better. Like three times better

'share valuations don't represent the current financials of the underlying companies' ... depends what you mean by 'financials'. On historic metrics you'd be right but the plummeting cost of capital has rendered the previous equity 'value' calculations not relevant. Yesterdays sky high valuation has become todays fair value on a yield comparison basis.

Not so. The fundamentals still hold true. P/E, D/E, NTA, EPS, etc. Point in case would be CBD - no current market, increasing losses, leased premises, no licences and no saleable product and yet the share price has >doubled (nearly tripled at one point) since IPO.. pure speculation and FOMO. Same goes for crypto. Recent CBD cap raising was majority from retail - people who aren't looking at said fundamentals imo

Depends what you mean by 'hold true'. As a measure of relative values, yes absolutely. And should always be considered when making investment decisions. But to regard historic ratios such as P/E's that applied in previous different times as remaining fixed under all economic conditions, especially when return expectations have dropped due to cost of capital reductions, results in extended periods of non investment. No bad thing for the risk averse investor but will mean missing the elevator if you want to go higher and it doesn't pass your floor again for a while. CBD style irrational exuberance examples don't make the case either way for conventional ratios being held sacrosanct.

Doesn't it become a question about what *kind* of investment shares actually are?

If the idea is to own a stake in a profitable company and earn dividends, then P/E is as relevant as ever. Bear in mind that this is the theoretical justification for the existence of the sharemarket in the first place.

If shares are only ever held for prospective capital gain on resale, they're a different thing. More like a stamp or a personalised plate or a bitcoin or a beanie baby or a tulip. Then P/E is irrelevant. I think this is the case right now -- shares are traded as blank, fungible abstractions, undifferentiated by anything except their name. There are two sharemarkets, really, with completely different ideals -- there's one where actual companies get traded, which has been very quiet for a long time, not especially profitable -- and another one where tech and cannabis stocks are bought and sold by people who have no interest in whether the company actually makes money, or anything at all.

Yes, agree there are two seperate share markets and that PE's remain instructive if an historic baseline comparison is needed. But for as long as alternative investment returns remain depressed I cannot see that past PE ratios provide a particularly useful guide to future pricing. Also not sure I agree that non fizzy stocks have been 'not particularly profitable'. Defensive NZX stocks have also appreciated sharply over the last decade and I suspect will continue to do so, especially higher div yield ones.

One thing to watch out for are "investments" in finance companies and the like who have lowered the offered returns in order to mask the fact that the investment is extremely high risk. To make it look like your capital is safe......

Registered Securities Limited. Blue Chip Securities. What's in a name? What could possibly go wrong?

Btc is a con. Nothing unique .. just an energy intense way of Selling tulips. Greater fool theory for the con men to exploit the dumber.

Btc is a con. Nothing unique .. just an energy intense way of Selling tulips. Greater fool theory for the con men to exploit the dumber.

I will accept that as a valid opinion. But the question remains: Is what we have been experiencing with financial and asset markets a con?

To answer your question, Yes, they are most definitely a con. But I would argue BTC is a bigger con.

It is basically a collectable, like Art, vintage cars, or old stamps.

I agree. I won’t be too surprised if the value of crypto drops to 0 in the medium or long term. I think it’s more likely than its widespread adoption. But I’ve been wrong before.

Even if there is widespread adoption, it needn't involve any of the current tokens.

Irrational smart people get in, watch the price go up, and then sell to dumb people.

Kiwi Wealth Managed Funds: Conservative Find -

5.4% annualized rate of return on 9k investment, $40 a week for last wee while. Slowly does it. Looking to add to it obviously.

I think you need to recheck your figures pal.. 5.4%pa on 9k is about $500pa so more like $10pw.. just saying. Given that 85% of your money is in NZGovt bonds and 90 day bills, you'll be lucky to make 1% this FY

Next year a dream return wil be 3% if you can find it, or take big risks.

The best way to get money will be to go to work lol

You're talking sense. Even a well researched property play might only yield 20% roi for a trade if lucky, but tally up the hours, time and risk and it's not worth it.

I have done it twice in the last 5 years. the stress, strain, worry are all part of the fun of it actually working in some manner. Makes it awfully interesting just jumping out of bed every morning. Absolutely great fun. Working on the next one now.

I am seeing property advertised with yield of 5% as if that is really good. And maybe it is, relatively speaking.

Is 5% the new 6%?

It is still possible to get 10% net yield on commercial property.

Sure it is. In Rawanda.

Yep that's considered a good return for a hold now.

The diminishing pool of unearned income causing a bit of anxiety out there? Maybe you'll have to something unthinkable to support yourself, work. I mean real work, where you produce something tradeable, not one of those imaginary ones.

Scarfie. But it is real work - in a capitalist system where money should be applied to the best yielding investment proposition someone has to allocate it and the owners are the best incentivised to do this as efficiently as possible. Instead of sneering you ought to be thanking us for our hard work, sweat and the stress involved.

Maybe you'll have to something unthinkable to support yourself, work. I mean real work, where you produce something tradeable, not one of those imaginary ones.

That's what they said about the internet as a commercial opportunity.

Scarfie, how do you think us old gits got all this capital we are so worried about? We all worked heaps back in the day. We took a few risks. Some worked out. Some didn't. Now we don't work so hard, but we are still interested. Installing a new dishwasher in a flat, then golf today. Ringer day. Then putting plywood on top of attic batts for storage. Checking my economics websites at regular intervals.

I think low interest rates will shut our economy down, there won't be high interest rates because the money won't be there to pay it.

Maybe it is time to force a redistribution of wealth in the form of restricting investments to just productive economy by introducing new taxes to shift interest from purely speculative ones such as stock or housing?

I personally think it's difficult to consider any serious improvement in financial literacy until the realities of fiat currencies and their history have been more thoroughly examined across a broad range of society. Yet, considering golds role in the monetary system was wiped out of all financial teachings in 1972, it's hardly a surprise. All fiat currencies today are pegged to the usd, and because of trade, all currencies are on a race to the bottom. Gold is not important? Consider this, 79% of US reserves are in 8131 tonnes of gold. Why does the usa have so much gold, and why is it such a huge proportion of their reserves if it's not important? America's closest allies, that is the 5 eyes nations, have barely any, to absolutely zero gold reserves, and that includes nz. You need to ask why that is.

In countries like Zimbabwe and Venezuela, where they suffer from hyperinflation, the stock market and house prices, have gone through the roof, as people use them as a protection against raging inflation. The Petro-dollar is dead, nearly all fiat currencies are being printed to oblivion. People see these things, yet still feel convinced our political and financial leaders have got everything under control.

Without an understanding of these changes, how can we seriously consider a search for yield? I would venture to suggest that perhaps in another 12 months the question posed could well be not how do we get a return on our investments, rather, how do we get a return OF our investments.

Hear hear Mr or Ms Lark. That kind of conversation would have been considered paranoid and conspiratorial not so long ago. Now people are realizing it's the reality.

Yes, we are in unprecedented times. I find it confounding. Here's another way to make money: In May 1933 President FD Roosevelt ordered the return of all gold coins circulating in the United States and other gold bullion held by U.S. citizens. In exchange the US government paid the then market price of $20.67 an ounce. Eight months later, in January 1934, the US Congress passed the Gold Act that revalued gold at $35 an ounce.

Did anyone at all who had the $35 preknowledge actually hand in their gold? We all know the answer to that one!

So what does that say about the USD at that time? it said that the USD in gold terms is now worth 69% less because they had printed so much money.

https://www.reddit.com/r/conspiracy/comments/31fm32/purchasing_value_of…

Where's the Mary Holms and their 'ETFs all the way', 'don't put more than 10% into gold' speak?

These people are well meaning but their subservience to the financial world is naive and downright dangerous.

Normalcy bias. Empirically grounded, but assumes the next 30 years will be the same as the last 30.

Early in 2019, BlackRock Financial Management had already anticipated a global economic downturn.

That August they made a presentation to central bankers at Jackson Hole & delivered a comprehensive strategy for dealing with this future economic downturn.

Several months later this was adopted by both the US Treasury & Federal Reserve as the basis of the federal response to the much-anticipated economic meltdown.

Fortuitously, a virus appeared at a convenient moment.

By placing responsibility for the economic debacle on pathogens rather than people, Wall Street bankers and federal authorities are off the hook, again.

By my reckoning that's the third time in 20 years!

As per usual, it's the tax payer coughing up for the bailout bill.

The question though remains.

Where to invest one's precious savings?

May I suggest we have passed the point of no return ha ha.

Prudence would dictate that return of capital is paramount in what is irrefutably now the lawless west.

gold then? realestate? I just purchased 11 thousand euros of british american tobacco. People always smoke.

Why does that not surprise me.

Oh please tell me how you disapprove. Just been to the proctologist and I need some cheering up.

Why, property of course (the answer to the question)

I think there are opportunities to invest in Tesla, Apple, Microsoft, Walmart, Google, etc through some online platforms like Hatch, Sharesies, etc. Heard that these shares are defying any Covid related downturn.

There is also Crossgate Capital, a NZ based fund which invests in Bitcoin. There seem to be good ETFs through Smartshares also.

This is not an investment advice, I am not an advisor.

Just noting some avenues out there.

My sarcasm detector is struggling mightily...

Did it let the SmoKey out yet?

"If we go back just on 12 years (to mid-2008), six-month TDs were yielding 8%. A deposit of, say, $50,000 would have therefore yielded a pre-tax return of $2000."

Basically the available Pie shrunk and is still shrinking ...

All returns head to zero as we ran the downslope of leverage

So the good old days of Passive income streams are over ...

All current returns are faked and bound to break

get used to it

You save a dollar today to spend in the future. The problem is those dollars you hold that represent you past efforts can be created (printed) out of thin air. The reality is money is compromised as as a storage of previous effort. I suspect in the next 5 to 10 years this will became a significant problem and monetary inflation is going to rob savers blind like they have never seen before.

If I have a dollar and then print another one, at some stage people will realise they are both worth 50 cents, in spite of what Martin Armstrong says!

This is why you should take into account inflation protection as one of the factors in your investment decisions. Keeping your money as deposits in the bank gives you no protection against inflation.

I can see deflation in the short term, but I also think that increasing inflation is a clear possibility in the longer term.

What we are experiencing is called financial repression. Savers after tax and inflation are earning less than nothing on low risk assets. They are forced to take risk that many should not take to earn something decent and protect themselves (hopefully) from inflation. Who benefits? Over leveraged borrowers and governments. Who loses, savers of course but ultimately everyone since the whole concept of incentivising saving for your future and using those savings to then invest in productive assets is lost. This, I fear, is something also lost on central banks.

ACB - I agree with what you say but maybe we are just facing a change. As humans we are good at assuming how things have been is the best and change that doesn't make sense is rubbished. The drop and dropping interest rates will work themselves through asset classes but there is a limitation once they have hit the bottom. Very tough on savers especially the elderly. House price inflation has had a massive help from falling interest rates for several decades along with immigration of course. In the future when asset appreciation has passed from falling rates innovation/development will be a key source of investment I believe. Wrong or rightly assets especially houses are going to increase so best be part of it. In the new world of MMT no one cares where the money comes from, money created by banks, inflation, money printing, speculative shares Tesla on almost 6000 PE, as long as money comes from somewhere that's what I've come too !

"In the new world of MMT no one cares where the money comes from.."

There is no new MMT world...

Its what DEBT (=money) can physically buy that actually means something .... and thats fast deflating to nothing

And Innovation .... its just a kite in a typhoon ...

Strangely enough the Port of Tauranga share price is at $7.42 today, sagging a bit recently. Like the rest of the real economy.

There are two economies, the real economy which still has to have the demand gap closed and the speculative economy which is being given a boost by increased liquidity.

For the real economy the only game in town is the govt which isn't coming to the party and Aucklanders running around spending money which looks like it may be an on of on off phenomena. So the real economy is set to sag for a while.

Meanwhile the first home buyers are thrilled to be released from their lending ratios but appalled that house prices haven't crashed. Investors are also appalled to find that not only haven't real estate prices crashed but that prices look to be about to spiral upwards in the world of diminishing and unreliable returns. Now the Aucklanders have been released back to generate an even bigger halo effect.

So muttering starts about who is this unelected RBNZ governor who just prints money when he feels like it, sending up asset prices at his whim. What would happen if he didn't? In these days of $US decline would you like to see the $NZ worth $US2? Would you like to see the export sector fall over?

Some people would like this but not me. The RBNZ governor is a cog in the machine, balancing the nation's priorities as best he can. If you want to point the finger of blame at anyone point it at the Minister of Finance, who is starving the real economy of the short term support and credit it needs.

It's a very hard thing for anybody with a mental picture of the economy as a household to get to grips with but understand this - currently any money not spent on the real economy goes into the speculative economy. The govt is the entity that has the power to the support the real economy. The RBNZ has made the money available for the govt to use. If the the govt doesn't use that money then private speculators will eventually be able to use it to bid up the price of assets.

As the govt refuses to spend money in the short term to support the viability of companies and income producing assets through the Covid period there are fewer and fewer real assets to go around and so the prices of the remaining good assets go up. Couple that with unspent funds going to speculators and the prices go up faster.

So you are saying that the Govt should be giving cash out for viaduct coffees and Air NZ twin props joy rides?

Is that correct?

Something I can't quite compute, and maybe you can help me fill in the gaps - The government has the power to support the real economy, but it cannot print real economic output, it cannot print houses (despite some pre-election promises) it can only shift people's focus as we are all watching where the money lands... right?

Sure, a wage subsidy is great as a way to fill liquidity gaps in businesses. But paying for shovel-ready projects doesn't necessarily achieve much, if we are already short of shovels.

So what should the government be doing? Presumably herding the shovels and $ towards tasks that will unblock the kinks in our economy?

Adopt the Swedish model, or similar. Firewall the elderly and vulnerable. Buy more ICU beds. Stop with the crazy unsustainable expensive interventions and allow the economy to heal itself. Do it this summer! Lets get tourism back up and running. Can't be done in winter because of the flu season.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.