By Gareth Vaughan

Last week something happened that might have caused me to fall out of my chair a few years ago.

In an unsolicited move, our bank offered my wife and I a series of mortgage rates below its advertised rates. Apparently this was because our bank wants to look after its existing customers.

Although I'm sceptical about how widespread this type of bank behaviour is, it does feel like the worm has turned in recent years with many customers now less prepared to just accept the interest rates banks offer them, and some banks realising they should make more effort to retain their good customers.

Way back in August 2011, in what feels like a life time ago, I wrote an article suggesting it was time for borrowers to haggle with their banks over the interest rates they were being offered. The international economy was in a Global Financial Crisis induced funk, and the Auckland housing market was having a quiet period after the Champagne Charlie days of the mid-noughties. Despite all this, New Zealand banks were in clover, posting record profits.

...it's time more borrowers started to question the rates their banks are offering. Next time you're talking mortgage rates with your banker, pretend you're shopping somewhere in the third world and haggle over price. You never know, it could be your lucky day.

Just three months later, in November 2011, I felt compelled to reiterate the message, and extend it to include savers.

So if you're looking to take out a loan, renew one, or invest some savings with one of the big banks, don't be afraid to haggle. There is room for them to move. And if your existing bank won't offer you a better deal, one of the other banks might.

So almost seven years on, it's heartening to see at least some of the banks are taking the initiative with at least some of their borrower customers and offering discounts to their advertised rates straight off the bat.

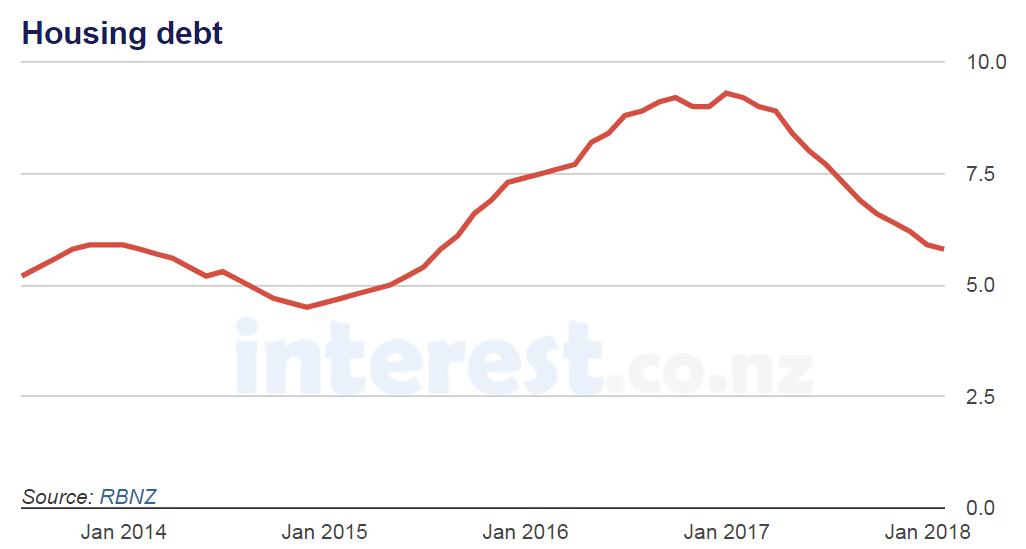

This of course does come against the backdrop of an Auckland housing market that's once again subdued, as highlighted by ANZ's economists last week, and the latest Reserve Bank data (at the time of writing) showing annual housing debt growth of 5.8%, the lowest it has been since mid-2015.

What should borrowers do?

So for borrowers with mortgages up for renewal, or those taking out a new mortgage, what should they do in the current environment?

The newbies should definitely shop around, trading off banks for the best deal. And those refixing should certainly see how their bank's offers compare to those from rival banks.

Meanwhile, is it best to fix or float? Fix some and float some? Fix for one-year, two-years, go out longer term, or split between two or more fixed terms? These are, of course, among the perennial questions for borrowers.

As ever the advice out there differs.

John Bolton of mortgage broker Squirrel reckons fixing for three years is attractive. Here's what he wrote after the Reserve Bank left the Official Cash Rate at its record low of 1.75% last week;

With credit growth and the housing market somewhat tamed, competition between banks will keep housing rates in check.

We’ve seen banks offering cash incentives again as they cut each other’s lunch. It seems there’s still a decent financial incentive to refinance if you can put up with the hassle of shifting.

After briefly increasing last year, mortgage rates have fallen back to their historic lows with rates in the low 4’s. For my money I think the three year fixed rate is looking attractive.

ANZ's economists have a different view. They reckon one-year rates currently offer the most value, or alternatively suggest borrowers spread risk by borrowing over a number of fixed terms. Here's what they say;

With average mortgage rates unchanged over the past month, our favoured views on where to fix remains unchanged. The 1-year rate remains the low point on the mortgage curve and offers the most value in our eyes. We are watching the recent lift in bank funding costs, but don’t believe pressures will escalate and affect mortgage rates significantly. But borrowers concerned by that possibility, or the possibility of the OCR moving up within the next year (which is not our expectation), may wish to spread risk by borrowing over a number of fixed terms. This strategy always makes sense from a risk-management perspective.

Ultimately every borrower has to choose what suits their own circumstances best, taking into consideration what they could afford to pay if interest rates rise significantly. Building a buffer into your plans to see how your finances would be affected if your interest rates went up by, say 200 basis points or to 7.50% for example, is always advisable.

Below is the full snapshot of the current advertised fixed-term rates on offer from banks. You can see our fixed versus floating calculator here, our mortgage calculator here, and our break fees calculator here.

| below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at February 16, 2018 | % | % | % | % | % | % | % |

| 4.99 | 4.35 | 5.15 | 4.65 | 4.99 | 5.89 | 6.09 | |

| 4.95 | 4.30 | 4.39 | 4.65 | 4.89 | 5.39 | 5.59 | |

| 5.35 | 4.39 | 5.05 | 4.65 | 4.99 | 5.89 | 6.09 | |

| 4.99 | 4.29 | 4.65 | 4.99 | 5.65 | 5.69 | ||

| 5.25 | 4.39 | 5.15 | 4.65 | 4.94 | 5.89 | 5.59 | |

| 4.80 | 4.39 | 4.69 | 4.69 | 4.99 | 5.39 | 5.59 | |

| 4.85 | 4.19 | 4.19 | 3.95 | 4.89 | 5.29 | 5.59 | |

|

4.99 | 4.35 | 4.59 | 4.64 | 4.99 | 5.49 | 5.55 |

| 4.85 | 4.49 | 4.65 | 4.39 | 4.89 | 5.55 | 5.69 |

In addition to the above table, BNZ has a fixed seven year rate of 6.15%. And TSB has a 10-year fixed rate of 6.20%. See all banks' carded, or advertised, home loan interest rates here.

What's happening with banks' funding costs & profitability?

The basic theory of banking is that banks are middlemen. They borrow money and then on-lend this asking their customers to pay higher interest than they themselves pay to borrow.

With the US Federal Reserve now increasing its Official Cash Rate equivalent, and expected to continue doing so through until 2020, some pundits believe NZ banks' funding costs will rise, with NZ mortgage rates following suit. (The Reserve Bank recently issued an analytical note on banks' funding costs pass through to mortgage rates).

When local banks increase mortgage rates their executives often cite their own rising funding costs as a key reason. Interestingly, whenever you talk to a senior bank executive, it seems that their funding costs are always rising or about to rise...Across the range of funding deals banks do, from term deposits to covered bond issues, the pricing of individual deals differs significantly and bank funding costs are thus a constantly moving feast.

But what we can do is average them out over time. What this shows is that by historical standards NZ banks' funding costs are currently low. If you are a depositor you'll already know this. Bank profits, as ever, are strong. My headline on a February story about KPMG's annual Financial Institutions Performance Survey (FIPS) encapsulated this nicely; Annual FIPS shows highest profit & lowest funding costs in survey's 31-year history.

The FIPS showed NZ banks delivering record combined annual profit with a 7.35% increase in net profit after tax to $5.19 billion. Annual funding costs, meanwhile, fell 40 basis points to 2.82%. And every quarter I number crunch key figures from the bank's disclosure statements. This shows that, for the December quarter, the big five banks - ANZ, ASB, BNZ, Kiwibank and Westpac - had an average cost of funds of 2.8%. Smaller NZ owned banks and active mortgage market participants SBS, TSB and The Co-operative Bank, had a slightly higher combined average cost of funds of 3.19%.

In more grist for the funding costs mill, last week Westpac issued a five-year bond, paying 3.720% pa for NZ$550 million. That compares favourably to the bank's five-year term deposit rate of 4.10%.

In terms of their Reserve Bank enforced funding requirements, the banks are sitting pretty. NZ banks must meet Core Funding Ratio (CFR) requirements. The Reserve Bank introduced the CFR in 2010 to reduce NZ banks' reliance on short-term offshore funding. The CFR requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. The minimum CFR for each bank is 75%. As of January, the industry-wide CFR was at 88% with core funding of $357.738 billion against total loans of $406.651 billion.

Interest.co.nz annually adds NZ's big four banks to a Bank for International Settlements measure of profitability across the major banks from both developed and emerging international economies. Profitabilty at the NZ banks, across a series of measures, continues to rank near the top.

Thus the message for borrowers in 2018 remains haggle with your bank. Given their profitability, there is room for our banks to move in a competitive market. And you never know what you might get if you ask.

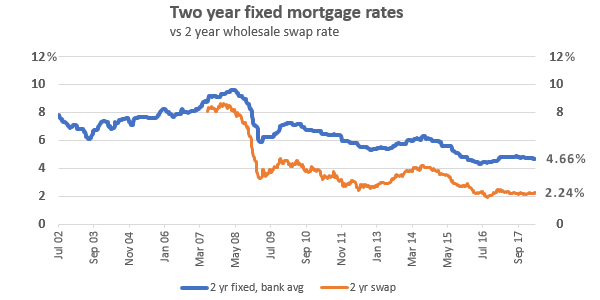

The chart below shows two year fixed mortgage rates against the two year wholesale swap rate, as a proxy for bank funding costs.

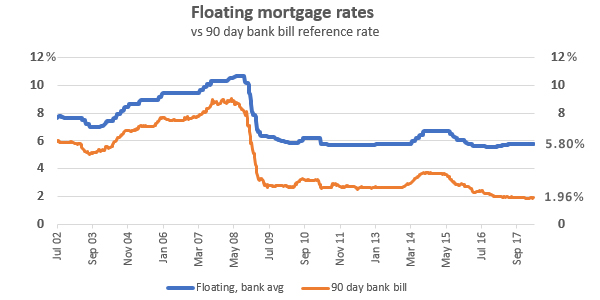

The chart below shows floating mortgage rates against the 90 day bank bill rate, again as a proxy for bank funding costs.

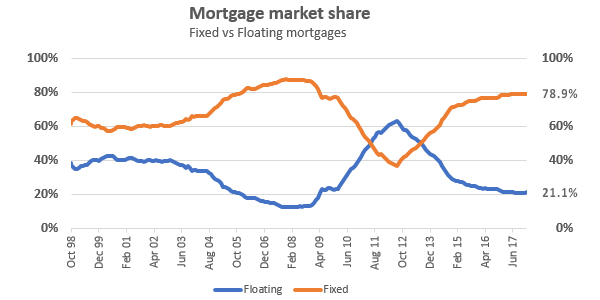

The chart below shows fixed versus floating mortgage market share.

35 Comments

I already had a below carded rate and they offered another 7bps reduction on top of that. I'm guessing we have another year of current rates before the pressure goes on RBNZ to increase. We'll still be likely to have sub 5% rates available for some time.

I've just refixed in the last week. I made a low offer to my bank - well below carded special, and below my previous rate - that I fully expected to be rejected and negotiate to a mid ground rate. But they sat on it for 24 hours hours and then accepted. Go lower than you'd think.

What was the rate and for what term ?

Interest rates are going to be under 6% indefinitely.

Doubt whether the one and two year rates will be over 5% in the long term, when you can get lifelong interest rates of around 3.5% in the U.S.

The 5 year rates that our Banks are offering are far too high and for you to be better off, the rates would have to go well over 6 % which is not going to happen.

Banks are keen to retain their good customers with good security and easy servicing and are prepared to move on their rates.

I note that the borrowing from first home buyers has increased marketedly so I am wondering why so many are saying that houses are out of their reach.

Now would be a great time to be buying if you think there is value in the property

Real interest rates could be quite high. I just got nearly 3.8% for one year deposit.

The argument that first home buyers have suddenly surged onto the market ,and hence affordability has improved is somewhat flakey .

4.1% fixed for 1 yr and 4.35% fixed for 2 yrs.

with what bank please?

One of the challengers is to find someone at the bank with the authority to make a better offer.

After the long wait on the Call centre.

Why would you do anything over the phone these days?

the alternative?

Visit the branch?

Online? Mobile app? Any decent bank should have some form of secure messaging that you can use.

why not a broker?

5.5% @ 2 years on our mortgage as we had to go through a credit union as a first home buyer last year. Fortunately our mortgage is only 3x my salary.

Dont ever be intimidated by banks, they are a a business just like the fruit and veg shop on Dominion Road ........... they need to make a profit and make sure their customers stay with them .

As a Baby -Boomer , I took out my first mortgage in 1981 at a rate I cannot even remember ............. but it was expensive , and there was NO NEGOTIATION whatsoever .

I was called in to sign the docs , and this old bugger who had me signed up had an office with dark wood panels with bookshelves . I wondered why a banker would need all those books , it looked to me like it was for show

He had a secretary scuttling around , calling him "Sir " and he used a heated stamp to put that red wax stuff on the loan documents , and it was all a little intimidating, and then he proceeded to sign the documents for the Bank with this huge over- the -top pompous signature .

The Bank simply told the instalment amount ( you dare not ask the rate ) and created the impression they were doing you a huge favour by even giving you the time of day

Bastards !

I subsequently qualified as an accountant , and then joined a London -based multi-national Bank , and it was then that I realized how it all works.

Banks NEED your business , and sure they will stuff around with the approval process , and that's just part of the game they play to ensure assymetry and having the upper hand in the whole process , they are masters at it .

Things have become far more difficult for them with the internet .

Customers are way better informed ........... information assymetry is largely gone , and customers who do their homework and ask for a better deal with get a better deal .

Are cashbacks still common?

The other day I was paying my rates bills at KiwiBank (old fashioned i know) and the lady there was trying to convince me to change my mortgages to them and offering me cash.

Zachary, at the very least I hope you took the cash!

very common cashback on new lending and refinance, we see it all the time, banks fight hard for new business

First home buyers may well be entering the market again in increased numbers. There could be some good buys around. I see this place in the auction results page:

https://www.barfoot.co.nz/752046

Sold for 640k but with an RV of 720K. Affordable? Nicely presented place however the old RV was 450k meaning it sold for 42% above that. This would appear to be a win for both seller and buyer.

Zachary, your spruiking aside, patience is key here. Significant outperforming of house prices over many years now means significant underperforming (stagnant) house prices is the best possible outcome medium to long term (barring a crash of course). A strict savings regime while renting will gain the FHB much needed traction over the coming years. If you don't buy into this scenario then your implying house prices are about to take off again!

FHB, there is no hurry. There is a surplus of unaffordable houses out there and there is a myriad of well documented reasons why many investors are right now wishing to exit. Valuations are highly stretch by historic measures such as price to income and rental yield. Don't waste your hard earned savings making some greedy speculator rich. You could potentially pay interest on any profits the vendor banks. All you are doing is contributing to this ridiculous ponzi. It's just not worth it.

In case you missed it, the Australian interbank credit spread is widening faster than the Libor-OIS rate. This is due to the Royal Commission into Australian banks that is exposing the deep rooted mortgage fraud that has been occurring. As Australian banks are New Zealand's banks I dont see mortgage rates going down any time soon - in fact, watch the banks desperately try to maintain those profits by putting interest rates up. Bank CEO's get paid by protecting profits, not customers. Although once the criminal justice system gets done with them maybe they will at least contemplate the effect of their actions on their customers.

K.W., what was it, $500 Billion in liar loans? This has the potential to tighten lending criteria considerably on both sides of the Tasman in the years ahead; https://www.smh.com.au/business/banking-and-finance/500-billion-pool-of…

Canada has a similar issue here; https://wolfstreet.com/2015/07/30/canadas-highly-touted-conservative-mo…

Yes, $500B or around a third of all mortgages. And people thought that the US subprime problem couldnt happen anywhere else. More worryingly, those subprime IO loans that have been reset to P&I loans are now starting to show up in rising mortgage default rates. Tick tock, tick tock .....

Latest update, Australian Banking Royal Commission of Inquiry into banking practices could trigger credit crunch, see here; https://www.domain.com.au/money-markets/banking-royal-commission-could-…

I should imagine financial institutions are well aware, according to the FBI 80% of mortgage fraud is committed by the lender.

Banks have always offered cash but it comes with a condition you have to stay with them for a number of years so it’s worth reading the fine print. It’s also better to get an equivalent interest saving than take the cash incentive. In a very real way people who don’t negotiate a rate are subsidising bank profits.

It’s always puzzled me that banks charge the same rate to everyone. You would have thought a doctor would get a lower rate than an Uber driver because the former is far less likely to default. No?

Yes! And that's what you should negotiate on - credit risk and collateral quality. I would expect lower rates on the exact same loan than someone who had a lower income/less secure job/higher debt-to-equity ratio. If the bank doesn't immediately recognise that I stop dealing with them very quickly.

Advise always seems to be split your mortgage into several parts with some floating (to allow faster payments when have some spare cash), some fixed for say 2yrs and some fixed for say 3yrs. Seems good, but when one of those fixed portions nears end of term you've got little ability to shop around for better rates due to the other fixed portion. Maybe splitting mortgage over different fixed terms isn't such a good idea?

While I cannot speak for all banks, the people I know working for a few of the big five currently have informed me that a large part of their performance rating is around customer experience now, versus around sales and bank profit as it was a few years ago. A banker offering a reduced interest rate is probably not a widespread decision from the bank to do this, but more the individual banker in question knowing what rates they can offer and being willing to give those rates to hopefully get better customer surveys and responses.

Basic questions..

Why mortgage rate compared to swap rate?

Swap rate means, swap against what?

Sorry. These r newbie questions

.

@Greg Hamilton .......... its complicated but , in simple terms Banks lend money long term ( between 5 and 30 years ) but most of their deposits are short term ( on call like a savings account or or 30/60/90 day call accounts AND term deposits )

This mismatch can cause liquidity problems if people demand their cash so the Bank has a committee often called an ALCO or assets and liabilities committee . It manages the RISK a and the big banks committee sit almost every day

Now because of this mismatch there is a risk that if interest rates moved suddenly or unexpectedly that there will be a crisis , so the bank enters a hedging arrangement ( gets someone else to bear some of the risk ) and this is done by a swop contract with another or other banks .

During the GFC some banks refused to enter these contacts with other banks because they were afraid of contagion , and this made the GFC worse

Thanks Boatman and Pragm*

I read somestuffs online.. can understand the scheme when read on the fly ; but dont get to understand how exactly it affects :-P

so u said

if interest rates moved suddenly or unexpectedly that there will be a crisis , so the bank enters a hedging arrangement

So in our case or in the graph in the page, whats the 2yr swap rate hedged against ?i.e who is the risk-sharer here ?

thanks

Just got 4.09 for 1 year plus $7500 cash on $1m from ANZ. You'd be mad to do anything over the phone these days. I do all my negotiating by email so I can play banks off against each other and against a good broker. In this case, broker got the best rate.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.