By Gareth Vaughan

Banks have cut the interest rates they use to test mortgage borrowers' ongoing ability to service their loans by a similar amount to what mortgage rates have fallen by over the past year.

ANZ New Zealand, the country's biggest mortgage lender with almost $85 billion worth of loans at September 30, currently uses a servicing sensitivity rate of 6.65% per annum. Testing serviceability is calculating whether a borrower can afford the repayments on a loan after their other expenses and income are taken into account.

Just over a year ago banks were testing borrowers' ability to service their loans at rates around 7.50%. With other banks now at similar levels to ANZ, mortgage brokers say this has boosted borrowing capacity, in some cases potentially by $70,000 to $90,000. The key reasons for the drop this year are changes made by the Australian Prudential Regulation Authority (APRA) and the Reserve Bank of New Zealand (RBNZ).

In July APRA announced changes to its guidance on the serviceability assessments Aussie banks use on residential mortgage applications. No longer does APRA expect them to assess home loan applications using a minimum interest rate of at least 7%, which had established common industry practice at 7.25%. Since July Aussie lenders have been allowed to review and set their own minimum interest rate floor for use in serviceability assessments and utilise a revised interest rate buffer of at least 2.5% over the loan’s interest rate.

APRA's change was attributed to a lower interest rate world and the widespread use of differential pricing for different types of loans challenging the merit of a uniform interest rate floor across all mortgage products. Mortgage brokers say APRA's move flowed through to NZ's Australian owned banks, ANZ, ASB, BNZ and Westpac, this country's four biggest mortgage lenders.

Then in August the RBNZ made a surprise 50 basis points cut to the Official Cash Rate (OCR) dropping it to 1%. In its November Financial Stability Report the RBNZ noted "a loosening of bank lending standards" in NZ over the past few months with "the potential to increase the supply of credit to the housing market."

A Kiwibank spokeswoman confirms Kiwibank reviewed and reduced its test rate after the August OCR cut, without giving a specific level of where it's now set. BNZ has also recently revised its test rate down, and ASB acknowledges revising its test rate down this year "reflecting the lower interest rate environment and other factors."

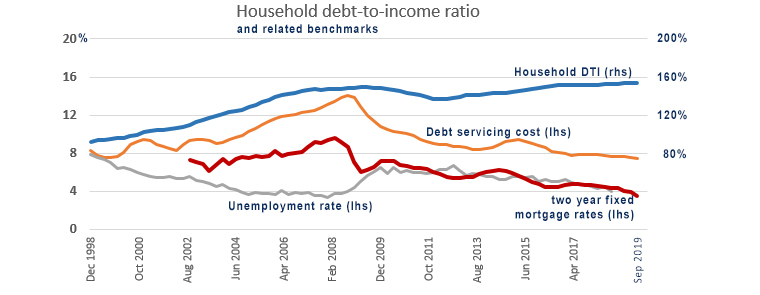

Using ANZ's 6.65% as a proxy for the banking sector, test rates are down about 85 basis points since September last year, when interest.co.nz last looked at banks' serviceability rates. Over the same time period the average of the big five banks' carded, or advertised, two-year mortgage rates for borrowers with a deposit of at least 20% has dropped 80 basis points to 3.53%. And the average two-year mortgage rate across the big five banks for borrowers without a deposit of at least 20% has dropped 66 basis points to 4.17%.

An ANZ spokeswoman says the bank's 6.65% servicing sensitivity, or test rate, applies for all residential mortgage lending including loans to investors. ANZ does now require borrowers paying interest-only to have a higher level of uncommitted monthly income, i.e. more monthly net surplus income, than borrowers paying principal and interest.

"We're working to ensure customers who seek an interest-only period as part of their borrowing arrangements can continue to meet their obligations once the loan moves from interest-only to principal and interest. The change is part of wider improvements to ensure we continue to lend responsibly," the ANZ spokeswoman says.

As of September 30, 19% of ANZ's home loans were paying interest-only.

One mortgage broker suggests borrowing capacity for investors is the highest it has been for three years. Another has a slightly different perspective saying; "In 2013, high loan-to-value ratio (LVR) borrowers had to climb Aoraki. Now they just have to climb Ruapehu. The opposite is true for under 80% LVR borrowers, they need to drive through Auckland traffic and walk up Maungawhau. It’s not hard but you do wonder about getting an e-bike. Investors need to do the Tongariro Crossing."

Borrowers' expenses in focus

Another key area of interest for banks is borrowers', and want-to-be borrowers', expenses. A factor in this is lender responsibility principles. Mortgage brokers say expenses are being scrutinised much more than in the past. Says one broker; "I would be more worried about that if I was a client [borrower] than what the test [interest] rate is." All debt is of particular interest to banks, including interest-free credit card deals and purchases through buy now, pay later service providers.

The move over recent years to comprehensive credit reporting means lenders can see "every credit card, every power and utility bill from the majors and two years of payments history," as one broker puts it. Comprehensive credit reporting enables a "positive" credit reporting system rather than the "negative" credit reporting system of the past that recorded defaults, bankruptcies and court judgments. Under comprehensive credit reporting positive information such as account type, account limit and monthly repayment history is also included in an individual's credit history.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

25 Comments

Great news for First Home Buyers and their vendors!

What's great about blowing the asset price bubble even bigger? Sure, great for vendors with multiple properties...

Pay cash when gambling, buying alcohol, tobacco and adult entertainment. Keep your social credit score high.

They'll notice the cash withdrawals though...on second thoughts just be austere and straight edge.

They will.

I got a call from Rabobank yesterday " Hi, Mr W. We notice that you had a term deposit maturing on the 5th of August (?!) and it was sent to your main bankers. Can you tell us what that money was for please?" I suggested that it had nothing to do with them, and maybe it was just a bad marketing call - but -yes, they noticed!

That sounds just a tiny bit too nosy...

In light of the recent Westpac fiasco it's much better that the banks are taking precautions and asking customers questions. Here's some latest news from The Guardian: Westpac scandal: Apra launches full investigation into bank over child exploitation allegations. "Apra also added $500m capital requirement, bringing total capital penalty imposed on the bank to $1bn". https://www.theguardian.com/australia-news/2019/dec/17/westpac-scandal-…

Ok, so let's assume 'the bottom is in' for interest rates have a look at what the last 6 months shows us for swap rates:

https://www.interest.co.nz/charts/interest-rates/swap-rates

Swaps up half a per cent over that timeframe, and if the trend is to be believed, it's going higher.

So. Do the banks now backtrack on their serviceability ratios; add another 0.5% on to the 6.65% = 7.15% and rising?

Who knows. But if the Australian authorities are serious about reinvestigating past malfeasance by banking hierarchy, then the first time one of them gets financially penalised or sent to prison ( like the NAB forex traders did a few years back), expect serviceability ratios to get really conservative!

Lenders are lowering their standards.

Quality of borrowers, their incomes static.

Per capita GDP weak.

It is bad to have credit grow faster than GDP.

It's worse to have asset prices increasing at a rate substantially higher than productivity growth.

It's a good thing we're doing both!

No doubt this will add to future defaults on mortgage payments. An exciting time for stability of the financial system.

When there is a recession and unemployment rises, that is when you will see the impact on highly leveraged households.

Anything and everything is good to keep up the housing ponzi and support NZ economy.

Housing ponzi should and has to continue............as the moment it stops the result will be a disaster. Pyramid schemes has to continue.

And yet, by its very nature a ponzi scheme can only ever end in complete collapse.

We've potentially still got a long way to go before it collapses.

https://www.harbourasset.co.nz/research-and-commentary/the-changing-fac…

In New Zealand, the Reserve Bank is also working with the banks to create mortgage-backed securities backed by mortgages granted by those banks. Historically, the domestic banks have preferred to keep the mortgages on their own balance sheets. If banks issued MBS, this would reduce their reliance on funding markets and make them more resilient.

https://investmentnews.co.nz/investment-news/rbnz-looks-to-kick-start-2…

Thanks for posting this. The MBS proposal is simply another indication of the extent to which the bubble dominates the economy. Of course, there is nothing in the media release that suggests as such.

MBS (mortgaged back security) brings new different risks to borrowers. Look at the US and robo-signing for foreclosures. Distressed borrowers who have had their mortgage repackaged into an MBS will be unable to ask their lender for forbearance.

Also MBS potentially sets up financial incentives to lower loan underwriting criteria by loan originators as the credit risk is passed on. Look at the US model of banks originating loans to distribute.

Its not a Ponzi mate, its been going for over 50 years with no sign of a collapse to date. Betting on the fact its a ponzi and collapse is inevitable would be at bad odds. You can also buy in and opt out at any time you want, worked very well for me over 15 years and then I opted out. Whats more of a worry is that "As of September 30, 19% of ANZ's home loans were paying interest-only". Thats not going to be great from this point in time onwards.

Long term housing credit bubbles take a very long time to build up depending upon bank loan underwriting policies and asset prices at the start of the period. These things can take 60 - 100 years. Very few people living in the same one country for their entire lives get to experience firsthand 2 housing debt bubbles so very few people learn the lessons.

Just because something hasn't happened in 50 years, doesn't mean it can't happen. That was the belief that led to the US debt bubble. Also the odds of a large house price fall have changed in the last 50 years - the odds are not static over time. The odds have increased due to a combination of the following conditions

1) significantly higher household debt levels,

2) high house price valuations in Auckland,

3) higher proportion of interest only lending

4) higher number of loss making landlords

5) changing residential property ownership laws

6) changing landlord business regulations and taxes

7) changing credit conditions, changing credit criteria, changing credit availability

The tiny proportion of the population that do learn the lessons are those who learn from history.

Well then take your pick and use 1987 or 2008 as a starting point and add 60 to 100 years.

From a NZ banking system perspective, what does the RBNZ see that you don't see?

How low can they go?

The piggy bank and goosing continues

Negative.

For as long as they think they can get away with it. And we've pointed out in the recent past they need to keep the property affordability illusion going and help justify property buying above the $1.5 million mark which is way beyond the means of the majority of NZ's population. We all know that the Foreign Buyers Ban laws can be manipulated when need be.

What a bank will lend you doesnt matter as much as the amount you should borrow.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.