The recent inability of wholesale interest rates to kick on higher as many had expected is opening the door for some settling in home loan rate offers.

The latest to "settle" back is from TSB.

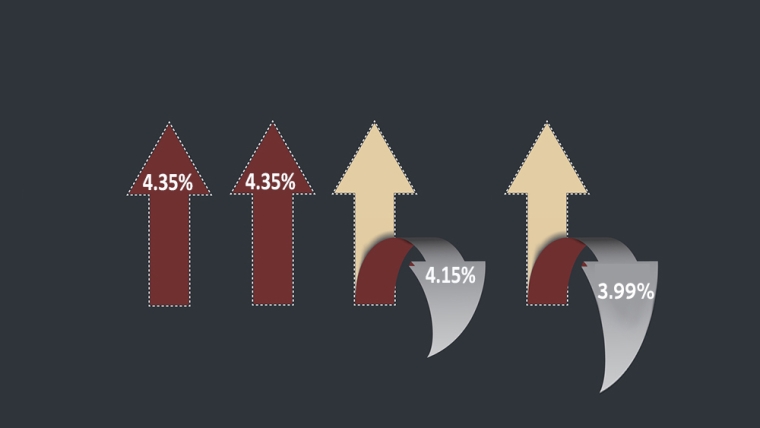

TSB has cut its two year offer to 3.99%, a 31 basis points drop. That matches SBS Bank's two year 'special'.

That takes them below the ASB offer of 4.15% which is the lowest two year rate on offer from a major bank - and which has been in place since December 7.

Recently, ASB was matched by the Cooperative Bank for that rate.

But no bank has a two year fixed rate as low as Heartland Bank's 3.79%.

Rates at these slightly lower levels are possible because the wholesale rates have not yet kick higher. They first reached the current levels in late November and drifted lower over the New Year period. They have risen somewhat since, but only back to those November levels - when the current mortgage rates were settling in to their 'new higher levels'. There has been no kick higher since.

It may only be a matter of time however. A lot will depend on the Reserve Bank's monetary policy review on February 23, and how financial markets price in what they think will happen before that.

The bite Omicron is having, especially on jobs, will come into play. But taming inflation before it becomes unmanageable is top of the policymaker's agenda still.

One useful way to make sense of these changed home loan rates is to use our full-function mortgage calculator which is also below. (Term deposit rates can be assessed using this calculator).

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. But break fees should be minimal in a rising market.

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at February 3, 2022 | % | % | % | % | % | % | % |

| ANZ | 4.00 | 3.65 | 4.15 | 4.35 | 4.75 | 5.65 | 5.85 |

| 4.19 | 3.65 | 4.09 | 4.15 | 4.69 | 4.95 | 5.19 | |

| 3.99 | 3.65 | 4.09 | 4.35 | 4.69 | 4.89 | 4.99 | |

| 4.19 | 3.69 | 4.35 | 4.69 | 4.99 | 5.15 | ||

| 4.19 | 3.69 | 4.09 | 4.35 | 4.69 | 4.79 | 4.95 | |

| Bank of China | 3.49 | 3.49 | 3.69 | 3.99 | 4.45 | 4.65 | 4.85 |

| China Construction Bank | 3.65 | 3.65 | 3.85 | 4.35 | 4.65 | 4.95 | 5.05 |

| Co-operative Bank [*=FHB] | 3.39 | 3.29* | 4.05 | 4.15 | 4.55 | 4.89 | 4.99 |

| Heartland Bank | 3.25 | 3.79 | 4.15 | ||||

| HSBC | 3.94 | 3.49 | 3.94 | 4.15 | 4.54 | 4.74 | 4.99 |

| ICBC | 3.65 | 3.49 | 3.85 | 4.05 | 4.55 | 4.75 | 4.95 |

| |

3.79 | 3.45 | 3.95 | 3.99 | 4.35 | 4.59 | 4.69 |

| |

3.60 | 3.60 | 4.00 | 3.99 -0.31 |

4.64 | 4.74 | 4.90 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

Comprehensive Mortgage Calculator

27 Comments

No customer no new business…

Don’t panic too early about rising interest rates. And don’t fix for too long. Plenty of dips in the economy from various shocks still to come this year.

Exactly. But then I'm a broken record on this.

Yep. Imagine 5-6% home loan rates. Good bye economy.

Yep economy is goneburger at those rates. so it won't happen.

Will you stake your mouse on that?

To be clear are you referring to 2 year fixed rate? I'll take that bet. 2yr fixed rates will cross 5% at some point (not 'never')

No better evidence that we'll sacrifice the lot of the poorer and non-asset-owning New Zealanders to protect our property portfolios. Property has truly become a welfare scheme for the wealthy not a market with risk.

Housing market is poised ready for a soft-landing. Much like in 2016/17/18.

TTP

The world is awaiting direction from the FED. Returning Kiwis late February and the big FED announcement of rising rates in March.

BE QUICK

The reopening announcement made by the PM, along with the NZ will not go back to BAU rather this is a chance for NZ to be better, and focus on overseas trade and promoting NZ Inc. Has this, likely stopped or mitigated the expected decline in house prices in 2022?

Lovely, let's get the housing market back on the boil in time for reopening. Surely this will be the final phase of the bubble.

Hubble bubble toil & trouble

NZ houses always double

I think you mean

Trouble, trouble, boil and bubble

Abrabadabra, monetary viagra. Orr to the rescue, don't step on my fescue. Pigs will fly before the housing market dies.

Another true convert, welcome to the club we are still accepting late arrivals, most Kiwis have already joined.

These banks should be accountable if the market turn south:

banks’ lending behaviour is found to have contributed to NZ’s housing quagmire, banks must be held accountable and share the pain when the bubble inevitably bursts

https://www.interest.co.nz/public-policy/114201/if-banks%E2%80%99-lendi…

LOL, thanks AJ, it was a long day until I saw your comedy gold :).

Too big to fail of course...

"Based on figures from KPMG's annual Financial Institutions Performance Survey, the banking sector's record annual net profit after tax to date was $5.77 billion in the year to September 30, 2018" - https://www.interest.co.nz/banking/113060/anz-nz-asb-bnz-and-westpac-nz…

"At the end of March 2021, New Zealand had:

- 2,750,000 employed people" - https://www.careers.govt.nz/job-hunting/whats-happening-in-the-job-mark…

-----

QED - banks are making $2098 from each working person.

-----

Apologies in advance for saving myself going down many rabbit holes by calling on expertise here, but is there a tool to calculate what salary I definitely need to be on to refinance? Or is it simply a multiplier of (gross? net? remaining after expenses?). I fixed my rate to June 2026 at 2.99, So wondering what wriggle room there is, or, what must I be earning to look after the balance of my mortgage (in the eyes of the lender). Thanks in advance. This is to forecast my options at end of term, of if I wanted to break and move to another region.

A good question and we think brokers would have the right tool for that kind of calculation but you may be able to work it out (in reverse) using our LVR borrowing calculator:

https://www.interest.co.nz/calculators/lvr-borrowing-capacity-calculator

Most banks have mortgage calculators on their websites - eg. 'how much can I borrow' - they will most likely ask for your income & expenses and give you a estimated borrowing figure. This would give you a rough indication if you look at a few banks...

I doubt you'd want to refinance out of a rate of 2.99% for the next 4 1/2 years (nb: not financial advice. But any broker who isn't chasing commission should tell you that) .. so if you moved, you'd want your current bank to substitute your security if you can, and not break the loan.

Things might be very different in 2026, don't think you could forecast out. If you moved to the regions, it would depend on the security and equity you then had.

A good guide for affordability though is a loan <4x your gross income.

Still double of Australia's rates.

Is it?

CBA (biggest AU lender has 2 year fixed rate for Owner Occupied of 2.99% and Investor rate of 3.14%, so doubt that = 5.98%-6.28%??

It is 1-1.5% lower, but note that 2yr TD rate is 0.30%, while ANZ, biggest NZ bank is 2.50%....

You gotta look at more samples mate, and also at variable rates. I won't be listing them out because the various lending institutions update their rates regularly. So many other things cost double or close to double in NZ yet the salary is not quite on par.

'I think the word "double" does not mean what you think it means'

Im not sure if you know the AU market well, but there is a lot of fine print around some of the rates you might see advertised.

But my point was this - the term deposits are also much much higher here. Market funding differs between the two countries. Probably as NZ only borrows, and hardly saves. Vicious cycle.

If people expect inflation to be stuck at around 4% for a while, these rates are an absolute steal!

It's no brainer that real estate is the number one choice when it comes to battling inflation for any households.

I tend to think the couple of recent mortgage rate drops are the opening shots in banks competing for mortgage business (including the volume of refixes), in the peak February-March period. I would expect the big banks to get into it shortly.

I expect the Reserve Bank will increase the OCR by 0.25% at it's February meeting in few weeks. That move (and plenty of subsequent ones) will already be priced into the SWAPS.

The Reserve Bank commentary and singled future OCR path may determine how aggressive or passive the competitive moves are.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.