Floating mortgages are sinking. Fast.

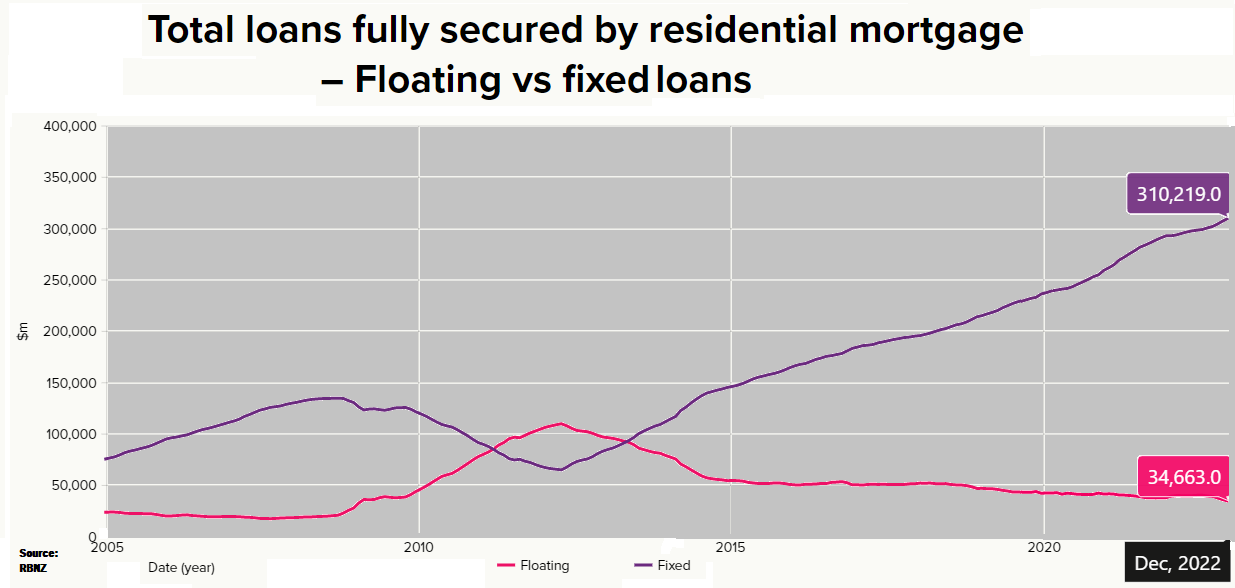

Data from the Reserve Bank shows that in the last six months of 2022, while the overall stock of outstanding mortgages in the country rose by around $6 billion to $344.881 billion, the amount on floating rate mortgages dropped by nearly $5.7 billion to $34.663 billion. That's a 14% drop.

So, that's nearly $1 billion a month worth of mortgages coming off floating rates during the second half of 2022.

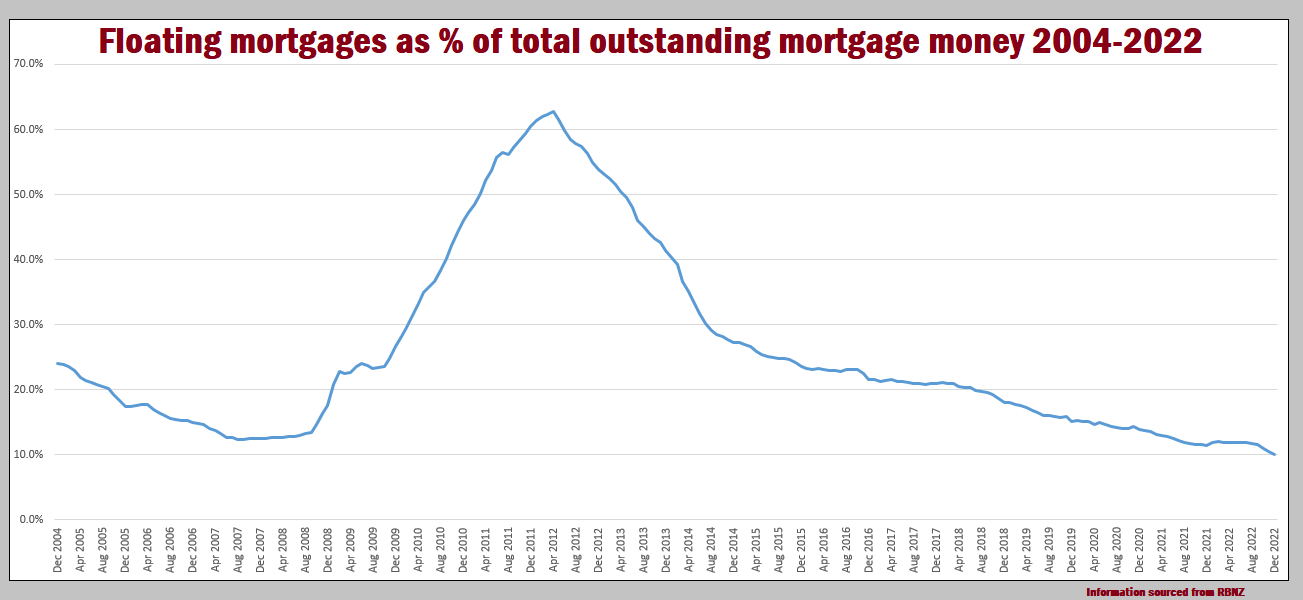

And based on figures in the RBNZ's 'long run' data series going back to 2004, it means that the amount of mortgages on floating - as a percentage of the total mortgage stock - is now at a record low of just over 10%.

In numerical terms, the $34.663 billion floating mortgage stock figure as at December 2022 is the lowest figure since January 2009.

I have been writing this week about how homeowners have been reacting to the higher interest rate environment we now have.

Undoubtedly and understandably the sharp fall in floating mortgages can be seen as a part of all this as homeowners seek to lock in fixed rates, which currently can be anything up to 150 basis points lower than bank floating rates. Indeed, the stock of fixed rate mortgages has increased by nearly $12 billion during that time to over $310 billion.

This is all a far cry from only around a decade ago, when in terms of overall share of the mortgage stock, the share on floating rates exceeded that on fixed. This had followed a remarkable about-turn in pattern following the global financial crisis in 2008.

In the run-up to the GFC, fixed mortgage rates had become more and more popular. The fact that people could access cheap fixed borrowing (often sourced from offshore funding) was something that led the Reserve Bank a merry dance as it was hiking and hiking and hiking the OCR in order to try to rein in inflation. But at that stage it was slow to get traction because of the numbers of people going 'long' with fixed rates.

But after the GFC, and with interest rates tumbling, the situation reversed completely. For long periods the interest rates on floating mortgages were actually lower than those for fixed. Consequentially people migrated their mortgages in big numbers to floating rates.

As of 2007 only about 13% of mortgage monies were on floating rates. By April 2012 this had rocketed up to a peak of nearly 63%. Now it's all the way back down at just over 10% and the question is, how low will it go? Is this the end of the humble floating mortgage?

Well, as we saw post-GFC, things can change quickly. And it will be interesting to see what happens to the composition of the mortgage stock in terms of fixed v floating once interest rates do start to fall here again - whenever that is.

If we do see a return of floating rates that are cheaper than fixed rates then undoubtedly the switching could be back on. But for the moment, floating mortgages are, as they probably don't say, SO 2012.

7 Comments

A decade ago 50% were floating? Floating rates have been much higher than fixed for much longer than that. Weird.

Anyone with their wits about them 18 months/2 years ago would have anticipated where we are at the moment and borrowed/refinanced to the max on a Floating Term and stuck the proceeds into an Offset Account ( net interest payable = $0). Not to get the relatively cheaper Fixed % rate offerings of the time if there was no purpose, but to get their hands on the liquidity whilst (1) Asset prices were still high and (2) banks still wanted to shovel loans out of any door that opened.

Today, anyone who did that, has the luxury of the liquidity that the Floating Rate gave them, that they would find difficult to do now. Perhaps that's part of why Floating is falling in volume?

So, did you do it? or are you just pontificating after the fact?

Anyone with their wits about them would have sold up 18 months ago.

Yeah sell up 18 months ago and live in a van to save money so that when houses prices dropped they could buy back in. Just a shame mortgage rates have gone up.

Mortgage rates rising + house prices falling = perfect opportunity for cashed up buyers who sold mid 2022 and thus will need no mortgage in 2024. With a following wind (courtesy of Mr Orr lol) they might even get 2 houses for the sale price of one.

By mid 2020 it was obvious which way the mortgage interest rates were heading. I fixed for 5 years at 3.39%.

I'll have paid off a large chunk of the mortgage in that time.

Couldn't be happier with the arrangement.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.