You put your money in the bank, the bank goes bust, the Government possibly steps in so that you get a slither of your savings back. Depending on how diversified your assets are, you’re left financially crippled.

How’s that for a bleak, yet plausible scenario?

New Zealand is an outlier among its OECD counterparts that largely protect depositors through insurance schemes. While different countries have different set-ups, the idea is that for every X amount you put in the bank, a portion is paid to a fund that can be used to compensate you if your bank runs into trouble.

The International Monetary Fund (IMF) in May said introducing deposit insurance would strengthen New Zealand’s financial safety net and complement the Reserve Bank's Open Bank Resolution framework, which potentially protects taxpayers from having to bail out a bank if it goes under.

Yet the Reserve Bank isn’t keen on introducing a deposit insurance scheme, largely due to its concerns around it creating a moral hazard.

The former National-led Government wasn’t keen on a deposit insurance scheme either.

And while both New Zealand First and the Green Party have within the past year spoken out in favour of a deposit insurance scheme, it isn't in the new Government's Coalition or Confidence and Supply agreements. This is despite the Labour Party supporting such a scheme in 2013.

However documents released by the State Services Commission reveal the Green Party asked Treasury to do some analysis of deposit insurance during coalition negotiations in October.

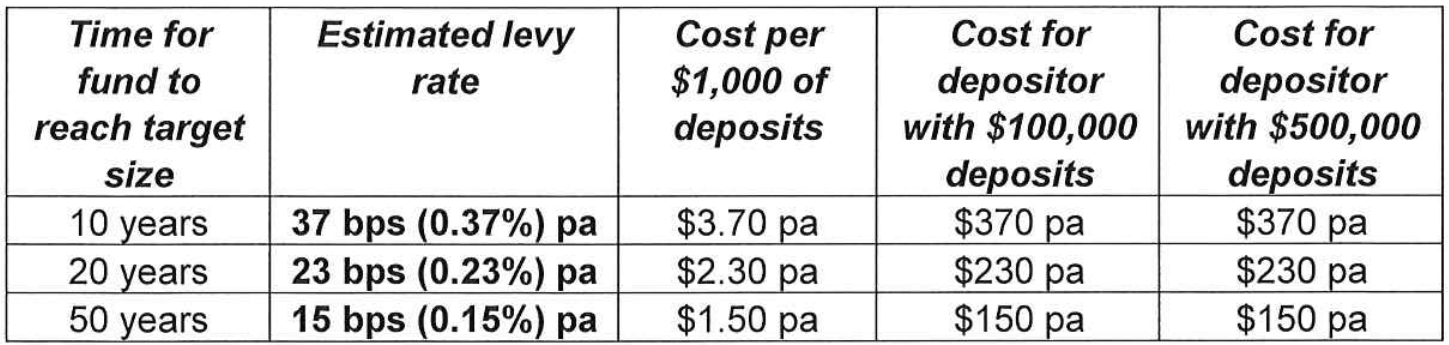

It asked how much deposit insurance of up to $100,000 would cost the average saver.

Treasury responded saying the cost per $1000 of deposits would be between $1.50 and $3.70 per year, depending on how quickly authorities would want to see the fund reach its target size.

So if the time for the fund to reach its target size was 20 years, someone with a $40,000 deposit would pay a levy of $92 a year.

Among its assumptions around how the scheme would work, Treasury’s costings are based on rates only being charged on deposit balances up to the coverage level of $100,000. So if you deposited $200,000, you would only be charged on, and insured for, half that amount.

Its other assumptions include:

- Banks would pass on the entire cost of insurance to depositors.

- The fund would be big enough to cover the cost of one average sized bank failing, despite it being liable for a failure of multiple banks. Given New Zealand’s concentrated banking system, Treasury says an argument could be made for a scheme to be based on covering multiple bank failures, but this would see its cost projections multiple accordingly.

It recognises that as with the Earthquake Commission (EQC), the Crown may have to lend the fund money to cover a shortfall in the event of a systemic failure, or if a failure happens before the fund gains scale.

- The portion of deposits lost in a bank failure would be 15%. Treasury says this is a conservative estimate, as it is unlikely depositors will face a total loss, as banks will have assets they could sell.

- The levy wouldn’t be risk-based, but would be applied at the same rate across all institutions.

- Insured deposits would grow at the historic average rate for household deposits of around 9% per year, but the portion of deposits covered would remain constant at around 64%.

- The scheme would be operated by staff at a pre-existing agency such as the Reserve Bank. Its funds would be invested/managed through pre-existing infrastructure such as a Superannuation Fund. It would cost $1 million p.a. to administer and returns would be 5% p.a.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

63 Comments

Deposit Insurance, one of those things we should implement yesterday to fully protect depositors on Monday if a bank fails on Friday so that they will be happy to keep spending on Tuesday.

Some wrong assumptions or clarifications here,

a) however it depends on how the insurer is. Private insurer, yes, if its joe public, no. So I am perfectly happy for the Government to legislate that deposits up to say $250K NZ where owned by a NZ citizen is privately guaranteed.

However why is it that a bank deposit needs to be guaranteed? the money is privately held why is it the owner of the capital cannot or refuses to look after their own money? What about moral hazard here? ie if the depositor feels safe they will demand a bigger return (yes OK fat chance) and then bank can do it as someone else picks up the tab if it goes wrong (the bank employees still get their bonus if it goes wrong) .

b) By and large the "saved" are not big spenders so in terms of "keep spending" you seem to be (potentially) ignoring the impact on those having to pay for the loss which is generally the younger ppl who actually spend more in terms of economic activity.

Steven, if depositors are protected then deposits won't be pulled from banks and shifted to institutions where deposits are currently guaranteed - like Australia for example. I guess I should have clarified that it also helps maintain stability and confidence in our banking system.

Can you justify / prove your statement please? As frankly I think that is rubbish. Ultimately like your house etc, it is "your" asset you should be looking after it.

If an OBR event is pending or even a bad recession, think Greece there is no confidence when it comes to it, the money will run anyway.

I have no issue with people putting their money elsewhere "safe" in fact its a great idea. If that happens then NZ banks will have to offer a higher return to keep the money, or insurer it to level the playing field.

If such an event happens that the stability of our banking system is really threatened frankly this will be to small a thing to matter as a prop to keep things going as the losses will be staggering.

Steven, I'm not visualizing such an apocalyptic financial event where you suggest bank stability is the least of our worries let alone the need to start doomsday prepping.

Think 2008, bank depositors could easily have placed funds under the pillows. Implementing deposit guarantee prevented this from happening. If the deposit guarantee was not fit for this purpose then why was it implemented in the first place?

I leave it to you to prove otherwise :)

Actually if I recall correctly a lot of $100bills seem to have disappeared from circulation.

I assume that an OBR event is a Great Depression scale event which we have some evidence has happened in the past.

"fit for purpose" lets be clear here the expectation was that [future] tax payers pay the losses even if it took 50 years to pay off and it was a huge gamble it would be OK.

Steven, there is no evidence to suggest there are less $100 bills in circulation - unless you can prove to the contrary?

https://www.stuff.co.nz/business/money/77045766/the-dirty-secret-of-nzs…

not sure what you want me to "prove here" We have had global bank crisis's in the past so they can occur. Futher the protections that were put in place to try and guarantee they would never re-occur have been removed. Since then inequality has built up to a level only seen just before the Great Depression was triggered. We have mad speculation on things like bitcoin, most assets are vastly over priced when the income is considered so all we are looking at is people gambling there is a bigger fool to buy off them.

Steven, I totally agree the risks are very real and lie before us all yet again, part in thanks to QE. A deposit guarantee like in 2008 would help hold the banking system together. It's better than having nothing at all. I think it should at the very least be as equal to the $250K in Australia otherwise any whiff of an OBR event and money could head across the tasman and only serve to deepen any crisis.

If there was no Government guarantee at all post 2008 then it could have been a lot worse. I am fortunate in that a large portion of my cash are with Rabo under a grandparented parental guarantee that was removed for all new deposits in 2015. The Rabo parent (Rabobank Netherlands) guarantees my deposit and the interest earned provided I do not transfer it out. OBR would not greatly affect me as the remainder is spread amongst the rest of the major banks.

1

Money deposited with a bank is considered to be AS SAFE AS HOUSES.

yes when we look at the Great Depression we see clearly it is not. The Q I wonder on is if it was truely safe why is there so much insistence its insured? and why those who insist refuse to pay for that insurance?

Kind of odd really I mean you can drive a car on NZ roads with no insurance or if you are worried about the liability get insurance to cover it, so why is it deposits are different to a car? (or house? etc etc)

because your car is not loaned out without your knowledge or say of who it is loaned too.

No that does not matter. If nothing else you knowingly give the money to a 3rd party to act on your behalf rather than lend directly yourself so you have chosen to abdicate that responsibility and are quite free to take that money back and do it yourself.

what fuzzy logic...bank accounts in reality are often the actual mechanisms for the medium of exchange and not all investment which are usually term deposits invested. RB may want to deem them all investments however if so where is the return on an on call standard operating account...mixing up the debate with comments like " 3rd party to act on your behalf" is making things even more muddle and clearly a misdirect.

Uh no, a misdirect? I think you are being more misdirecting here. A bank account as a medium of exchange, yes sure but this and a deposit are really not the same thing under the OBR from what I can read. In fact I think in the event of an OBR the medium of exchange ie the bank account can re-open immediately or at least far quicker under OBR rules than if the bank closed its doors in the traditional manner.

My point with using an analogy of a car was you insure your asset at your cost.

The reason for using the analogy was an attempt to highlight that it seems strange that people are perfectly happy to self insure some of their assets like cars but are not prepared to pay for insurance of what can be one of their biggest assets, their savings.

The Q remains, why is it people expect others probably with less than them to insure their "wealth"?

In fact I find it really interesting that extreme right wingers / libertarians (such as yourself?) seem unwilling to support most public services but seem perfectly happy that in effect the the tax payer has to pick up the bill to protect their wealth.

Steven,

Since I voted Green,you can't accuse me of being an 'extreme right winger/libertarian',but I would be quite prepared to pay a small premium for a limited deposit protection scheme.

Why are all other countries with such a scheme wrong and NZ right? Just how could the average depositor make an informed decision as to which bank offers the least risk of default?

I would cap the scheme at say,$40,000 per person per bank-that compares with ANS$250,000 in Australia- and that would cover most depositors.

So we will pay directly for the insurance. Can we not just have a simple Govt Guarantee on the first $100k-$250k like the rest of the world.

All that will happen is the Govt will bail out the insurer now rather than the bank. Cut out the middle man and save the average citizen some cash.

Sounds like just another scam by the banks to make even more profit - I can actually envisage a Bank Manager dressed up as Dirty Harry Callaghan Spinning a revolver asking - Do you feel lucky? as you hover over the question - do you want insurance with that.

Why should I guarantee your money? If its your asset why are you so un-willing to insure for the risk?

Why should we pay for your children’s education?

Why should we pay for you and your family’s healthcare in a public hospital?

Why should we pay for yours and your family’s benefit when / if you happen to need it?

This is a different argument. If nothing else you do not pay for my children's education. Their education is for about 15 years, yet I pay tax over 40 years if not longer easily paying back that as a sum. Same with healthcare same for benefits.

Your children's education is not the only benefit of taxes that you receive over the years, obviously. There was an article on Interest a while back pointing out there are likely to be some on average net-negative generations going through NZ now and the next few decades (i.e. receiving more on average than they contribute).

Hmm I cant see how that can make any sense. ie I cant see how in future there can be net-negative generations as that loss has to be paid for somehow which is an underlying call on energy which will be less and less in the future, ergo be able to support less debt than now..

I would also wonder if in effect the present situation, the BBs are indeed actually going to be net negative ie leaving behind a staggering debt future generations cannot pay. and will default on.

Yes, it obviously cannot be an ongoing situation for many generations or you end up with a Greek crisis. The article described it being limited to a few current generations, as you describe.

Cash in a bank is not always a traditional asset though, is it?

Banks are now a required function of society. Try and get a job, a benefit, pay tax, etc... without one.

I therefore don't see the insurance as a means to cover the "investor" but rather the average citizen that has not had a choice in the risk they are exposed to.

Based on most measures. 70-80% of the population live pay to pay - they are unlikely to have tens of thousands saved, in fact most would not even have $100 to their name. So covering $250k is really just pandering to the wealthy - but this is common overseas.

Personally I think a Govt backed $50k cover is reasonable. Anything over can be self funded. It provides a safety net should something go wrong, and allows the individual (and their family) to survive some months (using their own resources - as opposed to Govt benefits) if wider ramifications resulted.

See my post above - but in addition

OBR is fine in theory, but would it stand up to actual use? The govt would be bailing out the bank almost immediately.

So why should I guarantee your money? Because I would rather guarantee yours, than the banks margins.

Hmm but I dont see it being only one bank, if we see an OBR in one the rest with the same risk structure and lending profile will be closely following.

Would the Govn bail out a bank? ie ignore the OBR? that is a very good question. The Q is then if the Govn has to bail why did the RB even bother with an OBR safety valve? indeed if the risk is so small why have a valve?

I dont want you to guarantee my money btw, if you do so then actually in effect you guarantee the no loss of the shareholders and bank's margins. So for me in the first instance its paramount that the shareholders take the first loss until they are wiped out an OBR system makes this more likely.

I agree - shareholders should take the first loss.

Will they? I highly doubt it. It will always be mum and dad taking the loss.

Gareth Vaughan argues Westpac's capital stuff-up demonstrates why the combination of a hands-off bank regulator and the internal models approach to regulatory capital requirements is a bad one

https://www.interest.co.nz/opinion/90935/gareth-vaughan-argues-westpacs…

https://www.rbnz.govt.nz/about-us/statements-of-intent/statement-of-int…

Sorry why is the reference point per $1000 dollars deposited? Maybe it should actually be a levy per $1000 borrowed.

In the end it's a cost that hits banks margins somewhere - the only question is where. Maybe it would be cheaper for all if the banks simply held more capital? (perhaps not cheaper for shareholders...)

I agree. It is the default of the borrowers that presents the risk so the cost of that risk should rest with them. I agree also that the government needs to direct the Reserve Bank to take a far more prescriptive and Hawkish approach to requiring that the banks have a healthy capital base to cope with these risks. The Australians did this last year and cash from their NZ branches was used to prop up the Australian operations accordingly. It is high time that we extended our developing hard nosed attitude to the Australian banks also.

it is the bank that takes the risk as they set the policies for lending to each class of asset or Basel that sets those.

No the bank is the middle man, really it takes no risk ie there is no real risk on the bank or its employees it is all on the depositors. What there is is bonuses so really its in the employees interest to maximise their bonuses by taking undue risks as they lose their job if they dont perform anyway so they have nothing to lose and $s to gain.

--edit-- and shareholders....

So with interest rates on deposits a staggering <4%, minus tax (20%?), minus 10% insurance, your left with a net rate of 3% return and that's heaps better than it was. Here's an idea why don't banks use their record profits to gaureentee the money.

is it not ironic that you put your money in a bank because its supposed to be safe only to find out if you want it to be safe you must pay for insurance on it.

No, there is no such thing as a risk free investment, only people naive or stupid enough to think this is the case.

Personally as a potential guarantor (or more like my children) I really take exception to being forced as such for a certain event for such a piddling amount by those who already posses way more assets as a generation than my children will ever have.

In fact it on the face of it it makes no sense. I mean if the premium is so small then that implies the risk is also equally small, why then the insistence on having someone else pay the insurance premium? why is there so much fear? is it because sub-consciously the "saved" know they really have broken the system and expect it to fail within their lifetime?

Morally for me demanding such an insurance for free from other less well off is in-defensible.

I'm saving to hopefully have a place to call my own one day. As someone that potentially stands to lose the lot (unless the government steps in), a insurance type policy to protect everything I own sounds like a good idea.

Maybe I should take out some savings and go to a financial adviser for investments, however I worry that will take away from my future deposit and cost me more in mortgage interest. I'm a bit green compared to the experts around here.

It's all about your tolerance of risk. I'm in a similar position to you and have a chunk of money in a bank account as I work on the deposit as well. Sure I've missed out on the the gains in various stock markets over the last few years but I could easily have lost the same. Historically the share market (or other investment options) are going to outperform a bank deposit but over the term of saving that is relevant for its purpose of buying a house (3-5 years for me) the risk was too high for the likely gains. In hindsight it's been a mistake, but I think it's not about min maxing so much as ensuring that you reach your goals in a timeframe you are happy with. Good luck with the saving!

Hindsight is 20/20 as they say. And good luck to you too. ;)

It's the going down to one income that makes me nervous. Putting off kids to save for a house is an ugly sign of the times.

Indeed. I will ramble here.

The problem is in the OBR event any other investment carries an even bigger risk and impact than a deposit, ie there is no risk free investment and nothing acts in isolation. This also applies to house values by the way, so in an OBR event the actual OBR event is going to be caused by a massive drop in house prices first (I assume?) ie the banks "assets" are no longer worth anywhere near what they were worth and the bank goes toes up. (or can something else do it?) I have no crystal ball to say when or what goes first I just look at Math, physics and geology to see this game cann continue for ever unlike how most people view it.

Also in my mind I think house prices will drop 75%+ and the stock markets will look like 1929 (only faster), the Q is then will your insurance be able to pay up? or will they have gone bankrupt already?

"- The levy wouldn’t be risk-based, but would be applied at the same rate across all institutions."

The size of the levy has no relation to the size of the risk.

It's a sort of government bizarro insurance world.

You have to wonder why there is no such insurance anywhere in the world provided by a private insurer. Presumably the reason is that the risks can't be justified by the premiums charged. Why is it that only 'taxpayers' will take that risk? Is that because they are the ultimate sucker? Those who want the protection are looking for 'no risk' for 'no cost' and 'no work'. To me that seems a greedy imperative to foist on to the taxpayer.

Public 'deposit insurance' is the ultimate moral hazard; private benefit (loss insulation) at public cost.

Nothing, including bank deposits are risk free. Assuming that you can get others to pick up the risk is to just push risk away from 'you'. Many people think that 'the Government' can insulate them from risk. It can't; it can only impose it on the unsuspecting future taxpayer.

You can be pretty sure it is a 'generation selfishness' - those that have want those that don't have to protect them.

Nonsense. Banks' services are being used by an absolute majority of population, having bank deposits is pretty unavoidable for a person living in a modern society, and it is easy to see why taxpayers in many countries and their Governments decided that people's bank deposits should be protected.

Yes but it linearly (up to the insurance cap) benefits those who have wealth more than those who don't. A young person living paycheck to paycheck couldn't care less about whether they are covered for their first 100k deposit because they don't have that. In the meantime some portion of their tax is still being used to cover the cost to the government.

The risk should lie 100% with the owners of the banks.

If the banks need to offer a lower return on deposits, or make less money, or charge more interest on borrowing to guarantee them, then that is what they need to do.

Deposits are not an investment in a bank. The depositors do not see it this way. It is not marketed this way, and must not be treated this way.

Your asset - your risk.

The deposits are not "protected" from loss someone still loses. What they are ise insured free or charge from loss by having the tax payer cover the loss.

Its easy to see in that its a political cop out.

".. someone still loses."

Yes - but someone ELSE loses.

David on an agenda...clearly there is no private insurance market world wide as it is crowded out by Governments in most western countries...hardly good logic to bring into the debate.

Hmmm, yes and no. With an effective no premium insurance scheme this is probably the case. However a) most Govn schemes only insure for the first 100k or 250k, so above that there is a theoretical space for a private insurer. b) as you say "most" countries so there is a private market potential but its pretty clear that the attitude of the "saved" is they refuse to pay anything for insurance.

Looking at the stat's world wide on liquid investments over and above a home.. that 100k-250k and above deposit is a relatively small market, investments in banks can be spread over several jurisdictions providing cover to a much higher level for the sophisticated and in addition, at the very higher level bank deposits often become a smaller part of a larger portfolio, self insurance in reality for the truly wealthy.

ps Who says the "saved" will refuse to pay..currently there are no alternatives for the open minded person that has to use a bank...

You appear more concerned about not paying, or your children, and ignore there is a public benefit actually having a stable banking system, no alternatives for the little guy that has to use a bank and is looked at sideways in a society that consider holding cash is dodgy!

"refuse to pay" I think enough comments in here today alone point at a refusal to pay.

You only have to use a bank as a transaction medium, you do not have to use it to hold your wealth again this seems to be a mis-direction on your part.

There is no reason I can see that we cannot have a stable system with the OBR. The OBR does not cause nor prevent instability. In fact if it does indeed allow the bank to open its doors almost immediately it arguably improves stability. Stability, historically after the Great Depression it was done with adequate banking regulation that was removed, we are paying for that.

"If there are no consequences, then the world is seriously broken."

Different story, but the sentiment is the same.

http://www.afr.com/opinion/how-banker-fabien-gaglio-ran-his-us100-milli…

The banks should be held accountable for having their own deposit guarantees and it should be legislated and paid into a government held fund

We keep hearing about all these banks taking record profits in the hundreds of millions of dollars all on account of the government licencing them to print money.

This is just another way to punish savers.

I can guarantee you that if the banks start falling over so will the insurance companies and all that money to cover the deposits will have been eaten by fatcat salaries and administration fees. Dont think that re-insurance will necessarily help as if NZ banks are falling over there would have been a lot of other international banks that precede them.

In the case of both the banks and insurers ran into $$$ crisis at the same time, whos gonna payout to the poor depositors?

Best way is to increase the banks reserve ratio so they couldnt lend recklessly.

"whos gonna payout to the poor depositors?"

I love this. The tax payer will guarantee the depositor. It's not like they are one and the same NZ public.

Brilliant.

Its absolutely absurd that deposit insurance is not yet in place.

1) I can insure my house (& the tax system is already biased against savers (taxed) vs property owners (free capital gains in most cases))

2) I can insure my car

3) If I'm large enough I can insure bonds via credit default swaps.

"Its absolutely absurd that deposit insurance is not yet in place."

Minor correction - "Its absolutely absurd that deposit insurance - does not exist." I think to call a government guarantee insurance is an abuse of language.

IMO one reason we have a housing crisis and house prices have gone up so much, is due to NOT having any deposit guarantee scheme. This means cash rich people have been buying houses to diversify their assets, beucase if a bank fails, at least they will still have their asset. Plus they have been getting a better capital gain, than the terrible interest rates banks have been paying. This is not the only reason for the housing crisis, but it is one of the pieces of the jigsaw puzzle. A DGS should never have been removed from banks. The big mistake the government made during the GFC was applying it to those few finance companies that were still in existence. It should only apply to banks that meet strict criteria.

Steven and a few others have appeared to have lost sight of some basic, core facts here. The first question is what is a bank? In the context of this argument, a bank is an institution that accepts depositors funds and puts them to work on behalf of the depositor. This is in line with the original concept of a bank - where individuals with $10 could not do much with it, but $100 or $1000 could achieve much more and generate some income. Here the bank would take a slice to cover their costs and the rest would go to the depositor. What has this become today?

Firstly the banks are opaque. Depositors have little oversight as to how their money is used, and what return the banks get from putting it to work. There is much evidence that the banks are profligate in spending on themselves (CEO wages just one example) while paying depositors sweet FA for the use of their money. Steven argues change banks if you don't like it, but all the banks are the same to the man on the street, so what is gained? Try living today without a bank account. Employers won't pay you cash, the banks have got the system so tied up, our entire society has become highly dependent on them BUT they are PRIVATE business's, not publically owned. Is this situation acceptable that we are dictated to and manipulated by private corporations?

We can debate semantics all day, the experts in risk management and finance splitting hairs over terminology and the rules but it ignores the fundamentals. The banks should be regulated and liable for their practices and the risks they accept on their depositors funds, not the depositor or some already overloaded insurance company.

Conflict statement - I own 80 CBA shares.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.