Economists at the country's largest bank think the Reserve Bank could make a move on debt-to-income ratios within three months in an attempt to dampen the housing market.

In their weekly Market Focus, the ANZ economists say it is "a question of when, not if, the RBNZ will implement additional macro-prudential measures targeting the housing market".

"While we have learned over the past couple of years that these measures are not the most optimal policy outcome – they are distortionary, their effects are often temporary and they are far less powerful than the RBNZ’s traditional interest rate lever – the RBNZ looks set to take another crack via prudential means anyway," they said.

In last week's six-monthly Financial Stability Review, the Reserve Bank stated that risks to financial stability from the housing market had increased, but it stopped short of announcing new measures against the housing market. However, in the press conference following the release of the report both the RBNZ Governor Graeme Wheeler and his deputy Grant Spencer gave very strong indications the central bank was looking at debt-to-income ratios. Such ratios have already been given a strong tick by Treasury as a potential policy response to the house market.

"The rhetoric from the RBNZ appears pretty clear; something is coming at some stage," the ANZ economists said.

"All options appear to be on the table, but the way the RBNZ talked about debt-to-income ratios, a limit of that description looks a likely contender.

"We also don’t think we’ll have to wait too long to find out.

"Something within the next three months wouldn’t surprise us, though it may be a struggle to sell it politically as there will be concern over the impact on first home buyers."

Further action 'inevitable'

ASB economists, however, while seeing further action from the RBNZ as "inevitable - and the next few months of housing market data are likely to confirm this", are looking first at the likelihood of more tightening of loan-to-value ratios in Auckland.

"...What is interesting is that any tightening of loan-to-value ratio (LVR) restrictions is likely to be confined to Auckland, as the RBNZ has a rather sanguine view on the rise in house prices outside of Auckland," ASB senior economist Jane Turner said.

"The RBNZ is confident that a supply response to increased regional demand would not be as hamstrung as we have seen in Auckland. Indeed – the RBNZ cited Tauranga’s per capita consent issuance is twice that of Auckland’s! By implication, nationwide investor LVR measures may not be on the cards.

"The RBNZ will also continue exploring loan-to-income (LTI) ratios, but the time frame for implementing these is much longer," Turner said.

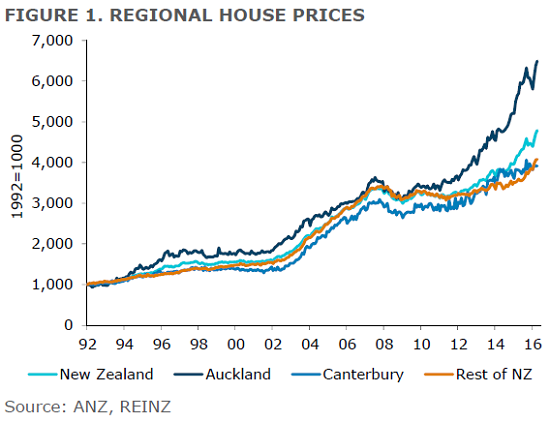

The ANZ economists said the housing market was "once more a run-away train, and strength is now far broader than it has been in the past few years".

"The latest April REINZ data showed annual sales growth running in excess of 20% in nine of 12 regions. While we agree with the RBNZ that regional housing markets don’t present the same financial stability risks that Auckland does, price growth is taking them into that territory. What’s more, Auckland house prices are rising again, with the stratified measure up 6% in the past two months alone, and back to all-time highs."

The ANZ economists said that interest rates were still falling, with the "effective mortgage rate" yet to fully reflect previous monetary policy loosening. "Together with expected further OCR cuts, we estimate there is another circa 35bps of easing still in the pipeline out to the middle of next year."

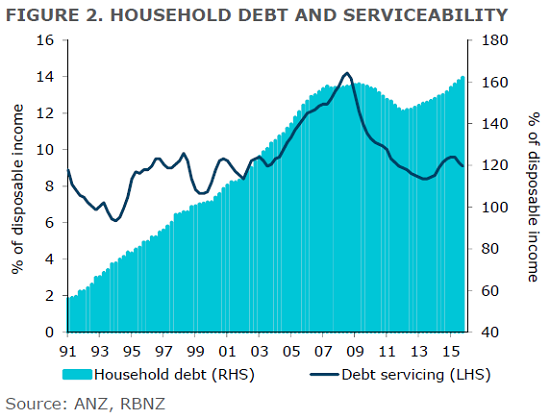

They also said that debt levels were high and speculative behaviour was now clearer to see.

"While household debt-servicing burdens are sitting only slightly above average levels given historically low interest rates, the household debt-to-income ratio (162%) is already at all-time highs and rising.

"Debt servicing only looks okay because interest rates are so low; it wouldn’t take much to change that via even small movements in rates. Investors are accounting for a growing share of both new lending and housing sales turnover. And for the first time that we can recall, the RBNZ is now acknowledging risks stemming from 'the high share of new housing lending being undertaken on interest-only terms or at high debt-to-income multiples'. The share of interest-only lending for new investor and owner-occupied borrowing is over 50% and 30% respectively."

The ANZ economists said that housing supply is responding, "but it is slow going".

'Projects are being canned'

"Most worryingly, escalating capacity constraints and cost inflation mean we are hearing stories that projects are being canned because they are no longer viable."

They have looked at some of the long-run drivers of household debt, and "unsurprisingly", house prices feature heavily.

"Over time, median house prices to income and household debt to income ratios converge to a roughly one-for-one relationship. Other significant drivers include interest rates (negatively of course), the share of the working age population that is employed (as a proxy for income expectations and job security), and the share of the population aged between 34 and 54 (the mortgage-heavy demographic).

"These drivers suggest that the household debt to income ratio will rise further," the economists say.

"It’s a vicious circle where house prices move up requiring more credit to be taken on board, and credit in turn pushes house prices up further. That’s the basic credit-accelerator model that was apparent pre-GFC. But on top of this, interest rates are still falling and the labour market is performing well, providing confidence for households to run with more debt on their balance sheet.

"The main factor working in the opposite direction is demographics, with the share of the population in prime “debt-leveraging age” now falling (it is down from close to 30% of the total in 2007 to 26% now, and it should continue falling as the population ages).

'The rubber band is getting tighter'

"This of course tells us very little to nothing about the sustainable ratio of debt to income. But we suspect that rubber-band is getting tighter by the day, which highlights a growing vulnerability for the economy."

The ANZ economists have already pulled back on their expectations of when the next RBNZ cut to the Official Cash Rate will be. Having earlier expected the next cut at the June 9 OCR review, they've now pushed that expectation back to August (with odds at around 60%). Given global risks they still see the OCR getting to a low of 1.75%, but now not until 2017.

"We still see the OCR heading lower, but further down the track than June; it doesn’t pass the smell test to be upping the ante on housing and pouring petrol on the fire at the same time," they said.

ASB's Turner said a delay in introducing further housing measures may continue to temper the RBNZ’s willingness to cut the OCR much further.

"We still expect the RBNZ to cut the OCR in June and August, but the risk remains that OCR cuts come at a slower pace. The weaker [New Zealand dollar] has, at the margin, also taken away some of the urgency to cut."

Inflation expectations important

Turner said the result of the RBNZ's latest survey of expectations due out on Tuesday this week would be an important decider for the June Monetary Policy Statement. "We expect that inflation expectations will remain steady, at uncomfortably low levels."

She said last week’s retail sales report also highlighted why further rate cuts are needed.

"At face value, 0.8% quarterly growth in volumes may seem pretty robust. However, once accounting for the strong growth in population, strength in tourism and the building boom which is taking place, it’s a moderate lift.

"Furthermore, these are the sectors which are supposed to be driving an increase in the rate of economic growth. However, momentum in retail sales has actually slowed from the growth achieved over mid-2014 to mid-2015. Growth is slowing, and per-capita demand remains weak.

"This will not be sufficient to drive the lift in inflation pressures the RBNZ needs to achieve its target."

62 Comments

Ireland introduced mortgage cap at 3.5 x income in February 2015 in addition to existing LVR. House prices in Dublin were running at 25 percent per annum.. First quarter 2016 Dublin running at 0.9 percent. the reason being financial security , save the banks, but at the end of the day if the housing market is out of sync with incomes and rent the RBNZ should act . Given that Wheelers biggest concern on becoming Governor was housing prices matters have only got significantly worse.

The other thing for the RB to target is lowering demand from Investors - they are driving about 40% of sales.

The other thing to consider is the number of under used houses. In Queenstown 4000 homes were unoccupied at census time vs about 12000 occupied - we don't have a shortage of homes, we have under utilisation with massive capital tied up in vacant buildings.

Vacant homes in QTN of course are holiday homes, who in their right minds would rent one out.

If you rent it out long term you lose the ability to use it yourself. I wonder if a more flexible option could be made available to holiday home owners where they still got to use their homes for certain weeks of the year. Could help solve the some of the rental shortage in QUeenstown

That was called Time Share and lost its reputation many years ago

nowadays its called bookabach

https://www.bookabach.co.nz/baches-and-holiday-homes/search/locale/new-…

Yes,

Im guessing the vacant homes are on the commonage above Queenstown or the edge of Frankton Arm or Lake Hayes Arrowtown

$1 Million may be an estimate each.

The only way I would consider they could be let would be serviced home with a cook/ housekeeper to overseee it.

Rentals are just over 40% of the market, so the number of purchases made by investors is almost bang on. Why would anyone consider this an issue and want to target investors more than the segment that's causing the majority of the problem - people wanting to live in their own house in Auckland.

Apart from jealously and tall poppy syndrome of course...

Not sure that logic follows. Your first stat essentially says that 40% of homes are currently owned by investors. You can't infer that the %age being bought by investors should match, that would depend on how many other investors are selling, how many are new builds and how many resales etc. 40% of purchases by investors doesn't necessarily maintain a steady-state 40% of properties being rented.

That's without getting into the fact that if an investor buys a house, it necessarily prevents a first home buyer from buying that same house and may force them into renting, making this a self-fulfilling prophecy, certainly not an argument that we need 40% of properties to be bought by investors.

But yes, maybe everyone is just out to get you, rather than being genuinely concerned about the current direction of travel.

Loan-to-income good for a start, but won't help much

Have a look at another great story of a Chinese "student" buying $31.1 million property in Vancouver

http://www.theprovince.com/business/million+Point+Grey+mansion+owned+st…

In my opinion you are very very wrong, it will have a huge impact and it will start the property crash

Has anyone thought about the unintended consequences of this ludicrous rule .

How is this going to work without excluding ALL young families with stay-at -home Mums , from home ownership ?

Completely true. Just as the 20% deposit rule it will hurt the poorest the most.

It also cuts down on peoples options. My wife and I bought a house dearer than we could really afford knowing that we could divide off part of the house into a self contained flat and use that income to pay a decent part of the mortgage. With these new rules we may not have been able to do that as the income from the flat hadn't been realized yet.

Boatman, that is true, but they are already excluded.

There isn't really any way to get a family on one lowish income into an $800k+ home - unless that home falls in value - which is very likely what these rules would do.

Loan-to-income rules are the best thing a young family or FHB could wish for, but the scare campaign by the vested interest will of course try to convince people otherwise.

Brilliant.. So you are saying in order to get the low income families into $800k plus home, lets drag the price of the house down by implementing loan to value ratio rule and then get the lower income family to buy it.. Nice... Have you considered the fact that $800k house won't fall alot or at the most $20k.. so if you buy a house for $800k after 6 months this rule comes to fact, you reckon you will be happy to sell it for $600k?? If the house prices do drop that much then Market will crash and if Auckland crashes, whole NZ house market will crash and RBNZ will be in pretty big sht!!!

Why do you think the RBNZ is talking about DTI rules? It's about financial stability not 'dragging down' prices for low income families.

Yes but that will make all those families not being able to afford any house.. Avg income $150k (lets assume).. 150x4.5= $675k.. u can't buy anything decent with that..then we will need to come up with 20%.. if something needs to happen then release the land and kick council to hurry up with consent so more houses go up.. Tauranga city council issues consents at double the speed as per article in herald.. why AK council can't do that..

Many on here are actually hoping and waiting for prices to drop significantly so that they can buy. Nothing wrong with that but the funny bit (at least for me) is that some have been waiting for years for this to happen while they were in position of buying a property for some time now. Rest is history.

I do feel for those who want / ed to buy but can't / couldn't as opposed to those who could have bought but choose not to.

Nothing funny about recognizing a scam when one see's one and staying the hell out of it until logic or atleast some financial madness is brought back from insanity. And that can take years. Do you ever ask yourself why back in the 70's-80's a family of 5 could live off one income and still own their own home?

It's not just about supply and demand anymore like many claim. It's something far more insidious, and I'm not just talking 'inflation' or 'population'.

Some are cautious for good reason because in their gut they know the whole thing stinks of corruption.

It not a "scam", its not a "ponzi" its a functioning market with supply and demand. You have the perfect attitude of a crash troll. Been dead wrong prices will drop while losing $100's and thousands of equity in the process, while paying rent. I used to think just like you. The difference is, most people stop doubling down on being wrong and get involved. Lets say prices did drop 20% (which is more than during the GFC) you are still only back to 18 months ago at the very most. Take that tin foil hat off and chill a bit mate, you're going to blow a gasket.

Fat tutu. It's a scam if you think of how it used to be, and how it is now for middle class families. Once they had money. Now-they spend their lives in penury. Ask - where is all this vast river of cash going. Not to other New Zealanders certainly. Scammed for sure.

OB - if you're willing to name people as 'crash trolls' then I think I'm equally entitled to call you a turkey, you turkey.

This is not supply and demand issue as most like to say it is. Why? Because no matter how many houses we build in Auckland there will never be enough to meet the demands of the greedy investors/speculators/landlords. We could build 50,000 house in the next 6 months to build shelter for all the new arrivals to the city, and they'd all get swooped up by speculators. And at the same time, thousands more people will end up living in tents, garages and cars! We have corrected the supply side of the demand equation by building more houses for them to live in, but they can't afford to live in them because they are priced out by the rich!! So this is not about supply and demand, it's about changing the rules and making it a more equal playing field.

Economics 101 works okay if you have a one house, one family supply and demand equation. But it certainly doesn't work if you talking about some individuals thinking they need 5, 10, 20, 50...1000 houses. While others are simply happy with a tent.

Wake the hell up you gobbling turkey...

OB, if the people first in make money by doing absolutely nothing productive, it is a scam/ponzi whatever.Just because a lot of people are doing it does not give it a moral legitimacy.

Buying houses does not create wealth for society, it does not provide a sevice, make or export anything.

If you do make money by doing nothing, you may well be a winner(as Donald Trump would say), but as no net wealth is created somebody else has to lose(at huge social cost).

"Have you considered the fact that $800k house won't fall alot or at the most $20k.. "

Who says that house IS worth $800k ? How is that determined? It's determined by everyone's available income vs everyones current debt and how much a bank will allow them to borrow. That's it.

How much something is worth based on credit and....(key word here) speculation is relative to many factors

What you are reece is a believer in 'ponzi economics' . As for low income families, no they won't be buying that house or any house at the moment. But they have the right to aspire to and also have the right to have a government that looks after ALL NZder's and not just those who may own a 800k home. Helping people at the bottom , the less fortunate also helps us all in the long run. It's about recognizing we citizens are not all born into favorable financial environments but we ALL have the same needs, some of the same hopes and dreams too. It's whether YOU and others care about that?

At the risk of baiting the social engineers, what about the argument that if you can't afford a reasonable deposit on something - you probably can't afford it? It was good enough for your grand parents.

What are you talking about? I'm the seventh generation of my family in this country and the only one who is formally educated. I have 3 degrees earn alright money and my siblings and I (in our 30's) will be the only generation unable to enter the housing market.

Three degrees? A professional student? It's not our fault if you spent all your time and money studying nonsense.

Well if you must know Zach I studied Nursing because I wanted to help people and quickly realised that if I didn't want to live in poverty on my pittance of a salary I would have to study further. So actually I spent a lot of money making myself a more qualified and experienced health professional so I could help people like you. If that is nonsense then so be it.

Ngrrk - perhaps a bit of a reality check is needed.....you studied nursing because you have a need that you wanted to fulfill i.e. you wanted to help people.......you could of volunteered at something and helped people and got the same need met........

When you worked as a nurse was it in the public or private system?? If it was in the public system maybe give a thought to the businesses who had to generate the income first so the tax could take place....I'm sure many of those businesses would think you are ungrateful of their efforts.

The only reality check that is required is from you I'm afraid, you see the world through blinkers. I'll talk in terms you understand. Having a highly functioning health care service' which myself and my qualifications contribute to, produces healthy citizens. Healthy citizens are productive citizens. I contribute to the overall economy as much if not more than any businessman.

Interest.co.nz where people get attacked for working hard to get qualifications and for trying to earn decent pay.

Not aneconemist... Consult your pharmacist, they may stock "daiastop" or reinsert your head if the problem continues.

That's pretty out of touch Zach. A number of jobs require two degrees and often people have to change to another field due to job instability. Other jobs require on-going education.

Maybe prices will fall and become affordable..

It's all part of the plan, nothing unintended whatsoever.

Elites don't want young families to own their own homes.

They want young people trapped paying high rents, unstable in their living arrangements, and thus easier to control.

Serfdom.

Because investors borrow more relative to their incomes than home owners do. So they are impacted more.

If people choose to have kids and stop working that's their choice. The rest of us already subsidize their kids health and education (which is fine) and give them free money via working for families (which is not fine). Are you seriously suggesting we should ALSO give them an exception so that they can buy a house easier than people like me, who are being responsible about how and when we have children?

Doubt it.

How would you prevent them being excluded without doing things that will lead to house prices leveling or falling? Subsidies will just push prices higher, lower interest rates push prices higher, neither will really help those who need help and both come with unintended consequences of their own.

Low income will still get the 10% deposit rate via welcome home loan. Not quite a ninja loan lol

Great article keep up the good work. Exactly what NZ needs to rein in this credit-accelerator model.as you put it so clearly.

8% p.a credit growth and 216bn of consumer debt (increasing 20bn a year). Time to act.

There is talk of a global recession this year or next. Often 2 months before a presidental election. Put on your crash helmets and seat belts....

I heard a radio add yesterday which infuriated me. Its was for a company that markets your house directly to the Chinese market. Something tells me home ownership rates in Auckland are about to fall off a cliff.

Sorry, but I don't believe they will really do jack other than make it even harder for FHB's. My reasoning is simple and proven by the recent past history of both government and RBNZ.

They know talking about it in public has a kind of 'we do care' effect to quieten the screamers. Don't be fooled, as the election gets closer you will hear more of this spin

Would govt need to approve a DTI or pass it into law or could Reserve Bank just have the power to do it without govt approval

As if the "3 percent" really care about debt servicing ratios... The only people this move would affect were already railroaded by RBNZ last November.

I believe they need govt approval as it is not in their toolbox yet (complete oversight on Wheeler's part)

Overseas countries have brought this in yet little old NZ know better ;)

Who needs all these rules. We can just have more bribery and corruption. Make all foreign investors donate $100k to local community services whenever they buy property. We may not be able to afford houses but we will all have tablets.

http://www.stuff.co.nz/business/industries/80062197/land-sale-approved-…

Won't matter too much.. will just distort the market further as others have already said. Why cant the Govt take a proactive approach rather than hiding behind badly collected data.. https://www.theguardian.com/business/2016/may/16/chinese-pour-110bn-int…

$28.5 billion USD has been invested in residential real estate in 2015 alone.. at an average of $832k USD. We get an allocation that studies have put at about 2-3% of Chinas total overseas property purchases, which puts the number coming into NZ at a significantly worrying level.. but everyone already knew this already

Welcome to the property crash when DTI happens

Debt to income will be an easier sell if house prices drop as Westpac are predicting.

http://www.stuff.co.nz/business/industries/80066702/house-prices-may-fa…

No change then

how strange to come out with this as the RB is putting together its DTI which would clip westpacs ability to lend therefore make money, is this the beginning of a PR campaign by the banks to say the DTI is not needed

I run past Cheltenham Baech in Devonport at the same time each morning. Just after 6.30 every morning lately 5-6 or more work men have been leaving a house on the hill above all getting into the same van/people mover.

At first I thought they were arriving at the house to work as they were dressed a bit like builders/labourers. Now I can tell that they are actually leaving the house at this time every day .

The lights are still on in the house so there are more people living there it seems. The house is an old wooden three bedroom by the looks of it.

I think we are seeing signs of dormitory living in Devonport much like Queenstown where houses are being over crowded and 3- 4 people per room are sleeping in them. If this is happening in rich neighborhoods of Auckland. where will it all end.

High Density Housing (build Up/Down)

Lots of developers in London built up one story and built a basement... and they were then all sold as flats.

Other developers ripped done houses and built blocks of flats.

queenstown is a lot worse most places rent by the night not the week.

i was talking to one guide and they had 15 living in a company owned flat $40 per night, it only worked because most were out on tracks so the most thay had one night was eight. and that was cheap compared to if they tried to rent. they have a real big problem down there with housing the workers needed for the tourist industry

http://www.stuff.co.nz/business/79117488/Greedy-Queenstown-landlord-to-…

Sounds like a backpacker rate and that is reasonable.

It would need to be staffed and there may be a meal provided, think i have heard of such a place.

Anecdotally a place was selling rock bottom priced evening meals.

The problem with Queenstown is the short seasons, compared to for example Bay of Islands and its cruise ships.

Talking to a taxi driver in Dubai recently - He was in a place there 4 to a room, 5 bedroom house - 200 a month, rest gets sent home to Pakistan to his wife children and extended family who see their Father once a year. Works 6 1/2 days a week.

Id suggest move family to provincial NZ, Father/Mother live in the city in these sorts of conditions, and there you go - housing problem solved. Why hasnt Nick Smith come up with this idea ? So short sighted.

The Interest tax offset ponzi is way way in tulip land. Even the guy who barely speaks English and just painted my house has several rentals. Whats the saying - "when the taxi driver is quoting his share portfolio to you its time to hit the ejection seat".

DI Ratio for the win, death to the debt ponzi. Will take a few years as longer loans role through their terms but if you have been losing heaps of cash on your interest offset ponzi, shame on you. Debt leverage is great on the way up, but is a cancer causing bankruptcy machine on the way down. The bank will be stabbing you to protect themselves. Exemption for first home buyer or family home, or those who have just done so as they still pay most of their tax. Those still waiting, save and wait for the carnage to stop, then buy.

Sitting in low debt position, and ordering more popcorn to hang on for the ride. #Aboutdamntime

The fundamental problem here is that global interest rates are too low. Keynesian central bankers believe they can create economic growth by flooding the world with virtually free money hot property markets have simply caught fire to counter this they are introducing messy rules upon rules. None of this is going to end well.

Well it's not going so well so far :

http://www.theguardian.com/world/2016/may/17/new-zealand-housing-crisis…

How long can national go on denying there's a problem.. sooner or later they have to realise that none of these people are going to vote national for a very long time.

Yes but did you read the whole article.. it's terrible piece of reporting.

At the start of the article it's a stated fact (totally unsubstantiated) ..

"Hundreds of families in Auckland are living in cars, garages and even a shipping container.."

By the middle facts are finally pushing their way in ..

"Nobody knows exactly how many people are living rough in Auckland.."

Another joke from the same party - http://m.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11640259

Still doesn't top 'sorry to be a man' for me.

I really wish Nats had some decent competition. But these guys are on the funnier side of life.

Agreed. If there was an even half competent opposition they would already be gone. Great opportunity for a small party to be the king maker next time on this issue.

I agree that the DTI restrictions would only hurt the very people that are already feeling some pain. Meanwhile that 3% (sic) of buyers from overseas will make even more hay as the sun shines even more for them.

I think the market could be slowed down by making auctions harder to do. Or charge a $1,000 government levy for holding one. Thanks to the Block etc there's a generation of people that believe that this is how you buy a house. Agents want auctions because a sale is more likely and then they can move on to the next one.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.