The country's bank economists have been honing their forecasts of future interest rates after last week's Reserve Bank update, which clearly signalled a rate cut for next month.

The Official Cash Rate currently stands at a historic low of 2.25%, but the now widely expected cut next month would see this likely go down to a new record low of 2%.

But the major bank economists don't see it ending there. Kiwibank economists are now the 'market leaders' if that's the right term with their new pick that the OCR will ultimately have to be dropped to 1.5% by early next year.

The Kiwibank economists said the Reserve Bank had last week provided a "dovish assessment", which had noted that the outlook for inflation had weakened since the RBNZ released its June Monetary Policy Statement, on the back of weaker global growth and a stubbornly high dollar.

"We believe the change to the inflation outlook warrants 50bps of extra cuts on top of the 25bps signalled in June – and we expect this view to be reflected in the RBNZ’s August MPS," the Kiwibank economists said.

BNZ, ANZ and ASB economists are all picking a low of 1.75% for the OCR, while Westpac economists (the first among the major banks to pick the OCR going as low as 2%) are still officially picking a 2% low, but "concur that the risks are now skewed to a sub-2% OCR, though much will depend on the NZ dollar".

ASB economists say they continue to expect the RBNZ to cut the OCR to 1.75%, with 25 basis point moves in August and November.

"The main difference between now and last week for our forecasts, is the second rate cut is now much more likely in our view, with markets now giving a 87% chance of a rate of 1.75% by the end of the year."

ANZ economists noted in their weekly Market Focus that the RBNZ came out "all guns blazing last week" in an attempt to tackle low inflation, an elevated NZD and housing strength.

"An August OCR cut now looks assured," the economists said.

"The RBNZ’s economic update noted it likely that further easing 'will be' required rather than 'may be', leaving little doubt.

"We don’t believe the economy is in need of additional easing right now given accelerating growth, an improving labour market (we’re picking strength in the HLFS data next week, which will serve as a reminder of how strong the economy is) and evidence of growing capacity strains."

The ANZ economists said they doubted the New Zealand dollar would move aggressively lower in the absence of a global meltdown (though they do regard there currently being "a non-trivial risk" of such an outcome).

"...There may be a few more cents left in the current NZD move lower, but the brutal reality is that: New Zealand’s growth story remains intact, we have far more political stability than others and interest rates – while low and set to be lower – are still well above international peers (refer our bond ladder below).

"...So we see the latest RBNZ moves as knocking the extremes off recent currency action as opposed to changing the trend."

57 Comments

I'm not an economist but..

Aren't they afraid capital will flee NZ? Or is it all about lowering the NZD? because there are some other ways to achieve that..

Isn't already probed that lowering interests does not always generate inflation?

One example of deflationary scenario with lower interests:

Amazon is using their capacity to borrow a lot at very low interests to gain a better position in the market and gain market share. It is well known they don't make money but they destroy competition that cannot survive without a profit while prices go lower and lower.

As per Phillips curve.. if you want inflation why not to decrease unemployment hence increasing wages? And for that, aren't the current immigration policies an impediment to higher wages and lower unemployment?

I just don't get it how can lower interest rates help the economy when at the same time it's creating huge distortions and generating bubbles everywhere..

Low interest rates makes credit cheaper for companies. They can expand more, hire more, innovate more, take more risks, etc. This leads to more jobs, etc. So low interest rates are good for the real economy.

While screwing competitors that had to borrow at higher interest rates, in turn to be screwed by new competitors are lower interest rates. The reality of a descending interest rate environment we have been in for 30 years.

except that is not happening, the credit is being used for M&A, share buybacks, dividends. none of which is increasing employment or consumer spending

Don't be silly. Companies that are buying back shares are using cash from profits. Not from loans. e.g. Apple.

maybe you should read this, a lot of companies have brought back more stock than they have made profits. its the new favourite thing for CEO with stock options and cheap credit, they only have to cover the interest payments not the debt itself.

http://www.reuters.com/investigates/special-report/usa-buybacks-canniba…

Almost 60 percent of the 3,297 publicly traded non-financial U.S. companies Reuters examined have bought back their shares since 2010. In fiscal 2014, spending on buybacks and dividends surpassed the companies’ combined net income for the first time outside of a recessionary period, and continued to climb for the 613 companies that have already reported for fiscal 2015.

In the most recent reporting year, share purchases reached a record $520 billion. Throw in the most recent year’s $365 billion in dividends, and the total amount returned to shareholders reaches $885 billion, more than the companies’ combined net income of $847 billion.

That's the US. The last 16 years has taught us all that the US is guilty till proven innocent. NZ is different. Hence low interest rates here will actually do us good.

the only difference is NZ.s asset bubble is houses. same principal more cheap credit more poured into it and very little towards the productive economy or the consumer spend to expand the economy

You can't have it both ways. First you post that it is silly to say that companies are using borrowed money for share buybacks, then when confronted by evidence that this is exactly what is happening, you backtrack and say, oh that's just the US, it's different here. Except, here, most lending is going to property. Sadly, NZ has a poor labour productivity record and that points to a lack of corporate investment in technology or training.

it is also happening in our stock market as well , but a lot less visable than the USA as an example fletcher building borrowing to buy formica and not getting a return to justify the borrow, its only because of cheap credit that it happened.

as for most of NZ's cheap credit there is no doubt it is poured into houses and would it happen if the credit was not so cheap and plenty of it?

last debt has fueled asset bubbles all over the world, from china building programs to europe M&A to USA shale oil production.

its only a matter of time before one pops and then the flow on effects to the other bubbles will be felt and for us in NZ that is houses

They can, but they don't. Reduced consumer spend impacts business decisions far more than interest rates.

The average consumer is spending less - why?

- They aren't earning enough

- Uncertainty means they are using disposable income to pay down debt

- saving for a house deposit

- paying through the nose on mortgages.

From what I have seen expansion has all but stopped in most industries.

Hiring is down, in fact most companies are restructuring to reduce staffing levels.

innovation? Lets look at NZs stunning innovation - Milk Powder, Raw logs, raw wool, live sheep. Wow talking about innovation.

risks? no one is taking risks, every sane person on earth is worried. As many other comments have noted, its not about return on investment anymore, its about return of capital.

Lower interest doesn't even fuel the property boom anymore - that is all offshore.

So why is the real economy stalling then? There are commodities and oversupply everywhere but low prices and weak demand. Basically its the end of growth. The only companies doing any "growing" are takeovers and capital buybacks which temporarily makes eps look better. Producers are in real trouble.

Here come 1960 mortgage rates at 3%

With the USA trying to raise rates by .25% this year dropping to 1.5% would put our 10 year rate less than the USA. Surely that would have a massive effect on any carry trade??

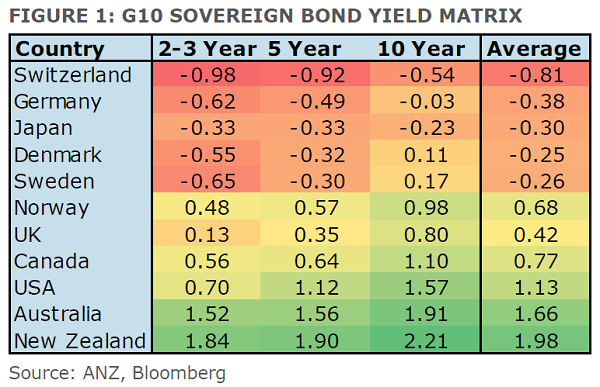

More to the point how long will they be low, hence how long can we survive paying back wall to wall existing debts without a growth forecast of substance in sight, according to the sovereign bond yield matrix above.

Ben Bernanke always claimed: Ultimately, the best way to improve the returns attainable by savers was to do what the Fed actually did: keep rates low (closer to the low equilibrium rate), so that the economy could recover and more quickly reach the point of producing healthier investment returns. Read more

Japanese depositors have been waiting 25+ years whilst Europeans and their US saving compatriots are containing their frayed, but nonetheless enduring, patience close to a decade.

Interest rates are only going in one directing, down. There might be a blip or two along the way, but we are destined for zero, or even negative interest rates. Of course the dialogue will be that growth will return one day, and this will persists right up until the money supply collapses from the flaws engineered into it.

Just to be clear. US interests rates are only going up. NZ interest rates are only going down (for at least 2 years I guesstimate..)

If you have the IQ, and attention span, of a gnat. I made the prediction in 2012 that interest rates were heading down, I have been proven right so far.

Indeed. Right now I see nothing that indicates that will ever change, ever.

Sure champ. US interest rates are going up. You will be wrong again.

Read my comment again in full, and lift your focus from in front of your nose and out to ten years. The next ten will be like the last 30 and remain in a downward TREND.

Long term I do not agree. US rates as a long term trend are staying at or near zero for ever Now that does not mean that Congress or the Fed can and will do something stupid and raise rates. When they do however they will reverse it as the US economy implodes. So at best they will create noise on the trendline and make things way worse.

There is already evidence of inflation in the US economy. Mark my words, the FED will raise rates this year. Wheeler will lower rates at the wrong time. Just like he raised rates at the wrong time. I'm not complaining though. Makes my debt cheaper.

Correct, except the flaws are grow for ever on a finite planet using more and more fossil fuels to do it.

ie increase global growth by 4% == 2.5% more oil used. if there is no more oil and in fact less per year (which we will see shortly) then you cannot grow for ever more. This is of course the fundamental long term effect, on top of that there are short and medium term effects that hide this effect/trend.

Switzerland says, "we'll pay you to borrow".

Is the world headed in the right direction?

More like lenders saying "we'll pay you Switzerland to look after our money". We don't trust anyone but we trust the other's less than you. CB's monetary experiments are taking us to places we've never visited before.

More like: We'll hide your money for you so you don't need to pay your fair share of tax.

http://www.aol.co.uk/news/2016/07/24/exbhs-owner-sir-philip-green-brand…

Scams pay..with cheap interest rates.

Some floating rates have recently increased so they are expecting the cuts, but usual story of strecth them out and retain a % I know of people fooled into believing cuts would happen quicker so they stayed on floating at a premium.

Thank you for the table (Figure 1). Everybody should look at it, if you're amongst the 99% of population who doesn't live in NZ and you want a little return on your cash (bank deposit , term deposit...) in a safe country with a stable government, where do you put it ??? NZ of course. That is what's propping up the high NZ$, because we have high, yes high OCR compared to other developed countries. (it doesn't matter that the OCR is "historically" low, we are not trading with the past, we are trading now, with countries whose National bank rates are much lower than ours).

Yes, great idea.....not. This will only further Inflate more unsustainable borrowing, kill saving completely and risk an OBR for what?

Honestly, this would be a huge mistake cause continued lowering is just a road to nowhere where others have gone... and still... are with no improvement in their economies.

The inflation they are trying/thinking they can create via this method to inflate all this debt away won't work, because the most debt being created ....the most... is around house price inflation which they almost totally disregard in their failed formula.

This is so going to end badly. Depositors will leave in droves, but I can only assume that is what they really want cause they believe those people will take out a mortgage instead.

The share market hits another high....

THIS has to stop right now. This is nothing but treason! Are we insane?

Seriously, any of you bringing up kids think this is great for their future?

http://www.stuff.co.nz/business/industries/82465472/ray-white-signs-dea…

NZ Real estate agency to list NZ houses on China's largest Real estate agency's website.

What's next? Buy up all the fishing quota?

Who's in for a sweepstake on when NZ finally wakes up and goes all Fiji 1987?

Fair tax is oxymoron! Why should anyone pay tax? We should not!

What does tax get us? Absolutely nothing!

How much tax do we pay? Too much!

What are taxes? A transfer of wealth from the masses to the elite, the infamous two percent of humanity!

When will too much be enough? Never, we're schmucks on our way to financial nirvana, and we will be rich!

HG,

"Why should anyone pay tax? We should not." What does tax get us? Absolutely nothing."

Quite right. We might not have hospitals,schools, roads,police,firefighters,DOC and a few other things, but hey, who needs them?

As Leona Helmsley once said after being convicted of tax evasion, 'only little people pay taxes'.

Can't we pay for it ourselves? Privatize the lot and a better system will emerge. Clinics are better than hospitals.

Firefighting was a private enterprise, you would pay a fee and post the sticker on your front door.

Do we really need police? They're good at giving citations, but they don't prevent crime.

As for the Department of Conversation, the only ones that would miss them would be the sellers of 1080, since they purchase 80% of worldwide production, to save us from the possum!

But nah, you're right we need them to feel safe, like sleeping withn the lights on, we need them to educate our children, and we need them to control us children. Obviously we can't do any of this ourselves, is not like we have been doing this since time began. We need more taxes, more control, more working hours and less freedom. But nobody wants freedom? ...or does he?

We are born a slave and die a slave and all because some people are so scared of life itself.

income tax is voluntary...you can simple ring ird and close your account if its bothering you...

Thank you for proving my point by voluntarily giving away your tax dollars. Although I am sure if you were to change your mind and decided not to pay your 'fair share of taxes', you might be surprised at the outcome. But then again, you may not...

I keep hearing "income tax is voluntary" but never has the IRD or any other bureaucrat ever fully informed the public of this right.....so are they lying to the public?

I don't know about Fiji 1987, I think we are closer to NZ 1987.

We could do both. Won't that be fun for everybody?

Instead of changing the flag, why don't Mr Key and the Mr Whippy party just change the name of the country instead? Say, something like 'New China' sounds about right..

Spot on.

With western nations no longer producing what they once did , economies or more so government relies on low interest rates which spike a housing boom . Investors seek out property , with ever increasing capital gains but reducing yields . Rents will rise and generation rent pays the price . For those who relied on savings many will already be spending them to live on , so money then moves from one section of society to another . I had 40 years in business and paying 5 to 8% on loans was never a problem . So all i can see is our young people being enslaved to a life of renting . So who exactly will the winnners be and who will the losers be ? If interest rates have been used as what appears to be the only tool to devalue the dollar it isn't working very well . A life controlled by central bankers i fear will not be a happy one . If government debt is an issue there are alternatives , like the Bradbury pound , zero rated sovereign debt .

Never in the history of finance have so few made so much at the expense of so many!

Look over the hill, not at the hill. About two years out, we'll have seen an increase in house demand , price and construction, labour shortages, companies investing in in technology for long awaited productivity gains, hence inflation rises , interest rates rise.

What we have got to be careful of is consequences of the current solutions - a house overbuild and price crash when rates do rise again. That's what David Hisco was talking about.

Its not a hill we are staring at ... its actually a cliff. The seneca energy cliff. We are currently in mid air courtesy of Ponzi debt. Future planned productivity gains are too late to save us now.

Dave 2,

"companies investing in technology for long awaited productivity gains". I admire your optimism, but what evidence do you have for this? Why would a few more interest rate falls stimulate companies to do what so many of them have failed to do so far? There are of course shining exceptions like F&P Healthcare which has had a major R&D budget for many years, but there just aren't enough like them.

I’m picking a 50 basis point cut next month, the scene has been set with the changes in housing policy which were very abrupt.

I agree with that. They have been setting the scene for it.

Agree - might be catch-up time.

AUSTRALIA HAS IMPOSED TAX ON FOREIGN BUYER AND NOW SO HAS CANADA

http://www.stuff.co.nz/business/82489325/canada-tax-targets-foreign-hou…

WHEN WILL OUR GOVERNMENT COME OUT OF DENIAL AND ACT.

Mr PM you can delay in bringing tax to forieger buying properties but will not be able to avoid so why harm ecenomy more by delaying. Please act NOW.

Question to be asked is How Low will our government go....before taking action...............

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.