The Reserve Bank (RBNZ) has kept the Official Cash Rate (OCR) on hold at 1.75% as expected, but decisively moved to an easing bias.

Governor Adrian Orr has ditched his line the direction of the next OCR move "could be up or down," saying the "more likely direction" is down "given the weaker global economic outlook and reduced momentum in domestic spending".

Where he previously noted "upside and downside risks," he now says the balance of risks "has shifted to the downside".

With gross domestic product (GDP) growth undershooting the RBNZ's forecasts in the December quarter, Orr acknowledges: "Domestic growth slowed in 2018, with softness in the housing market and weak business investment contributing."

While he at the last OCR review in February said trading partner growth was expected to "moderate," he now says the global economic outlook has "continued to weaken".

Orr also notes this weaker outlook has "prompted central banks to ease their expected monetary policy stances, placing upward pressure on the New Zealand dollar".

He has removed the line from his previous statement: "We expect to keep the OCR at this level [1.75%] through 2019 and 2020."

However his concluding remark remains the same: "We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation."

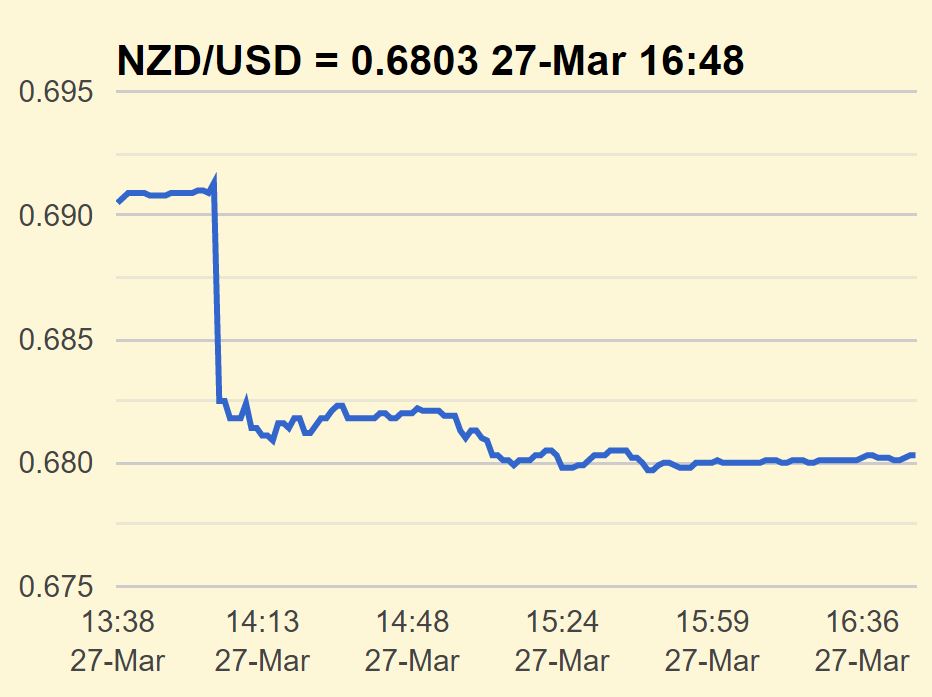

The New Zealand dollar plummeted on the news, and then fell a bit more, settling just over a cent lower at 68.0 US cents by mid-Wednesday afternoon.

Orr throws the cat among the pigeons; economists see cuts (plural) on the horizon

As shown by the shift in the dollar, Orr's tone is considerably more dovish than the market expected.

Some bank economists can now conceivably see a cut happening as soon as May 8 – when the decision will for the first time be in the hands of the soon to-be-announced Monetary Policy Committee.

Kiwibank economists have drastically changed their outlook, saying there’s a 60% chance the RBNZ will cut the OCR in May.

They go further to say: “One cut wouldn’t touch the sides, so we expect another follow up move to 1.25% in either August or November.”

ANZ economists – previously the outliers among their peers for forecasting three cuts to bring the OCR down to 1.00% by next year – continue to see the RBNZ making its move in November. But they acknowledge the “risks have now shifted in the direction of an earlier move”.

While ASB economists had believed the RBNZ could afford to sit tight for a bit longer to gauge the state of the economy, they now expect the OCR to fall to 1.25%.

They see the RBNZ making its first move in August, but haven't ruled out earlier action.

BNZ economists say: "While the door to a May rate cut may have been opened, we do not believe the evidence will be sufficient at that time to actually take the plunge.

"Unless we see weakness in the labour market or falling inflation we will rail against a May cut view, albeit ever mindful that we do not see justification for the Bank’s current stance either."

Westpac economists are “very surprised,” because in their eyes the economic situation has not changed much since February.

They raise the point: “Perhaps the main reason for the change of stance was the actions of other central banks.

“The RBNZ said that a weakening global economic outlook had "prompted central banks to ease their expected monetary policy stances, placing upward pressure on the New Zealand dollar".

“In other words, the RBNZ might have tailored this statement to meet the expectations of financial markets, who are pricing OCR cuts, thereby avoiding a lift in the exchange rate.”

Orr's full statement

The Official Cash Rate (OCR) remains at 1.75 percent. Given the weaker global economic outlook and reduced momentum in domestic spending, the more likely direction of our next OCR move is down.

Employment is near its maximum sustainable level. However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.

The global economic outlook has continued to weaken, in particular amongst some of our key trading partners including Australia, Europe, and China. This weaker outlook has prompted central banks to ease their expected monetary policy stances, placing upward pressure on the New Zealand dollar.

Domestic growth slowed in 2018, with softness in the housing market and weak business investment contributing.

We expect ongoing low interest rates, and increased government spending and investment, to support economic growth over 2019. Low interest rates, and continued employment growth, should support household spending and business investment. Government spending on infrastructure, housing, and transfer payments also supports domestic demand.

As capacity pressures build, consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

The balance of risks to this outlook has shifted to the downside. The risk of a more pronounced global downturn has increased and low business sentiment continues to weigh on domestic spending. On the upside, inflation could rise faster if firms pass on cost increases to prices to a greater extent.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

67 Comments

Holy smokes, good news. With no indication that interest rates will rise anytime soon, property prices are set to stay flat until the upward phase of the cycle in a couple of years time. With the economy in relatively good shape and interest rates low, there is no reason for vendors to sell for cheap, so they won't. Volumes may continue to slip, but looks like prices are set to stay as flat as a wonky pancake.

Gosh - this is a bit grim. Speaks volumes about the state of the Global and domestic economy when current interest rates (already at 80-year lows) are still too high.

Since the previous RBNZ release where rate movement was balanced either way, the situation has clearly deteriorated. Low inflation morphing into a deflationionary cycle is clearly a threat and thankfully, Central Banks are taking it seriously.

Ha-ha :) Nah, not at all. I can see why the heavily indebted such as yourself are celebrating the moment. Hell, I would be. But, as deflation arrives, everyone wants to part company with debt. I already have. ....and besides, what's wrong with me seeing a future littered with REAL bargains? Isn't this something you concur with? This generations relentless deleveraging is going to be a boon for the next generation of FHB's

Opportunities :-)

Poor Eeyore had nothin to do and nothin he could celebrate in his house made of sticks. Maybe he should have taken on some debt and at least bought himself and the missus a decent home ;)

It's 'relatively good' now. Will it be in 6 months? I'm not so sure.

If on May 8th RBNZ drops, where does everyone think Home Loan rates will be by years end?

About where they are now, or higher pending the bank capital decision.

Somewhere higher than the OCR.

3.7% (i.e. 3.5% for those with plenty of equity and over $1m in loans).

DON'T PANIC. If house prices start falling in Wellington we will cut interest rates.

Exactly! so don't worry

Westpac traders will be having a long afternoon.

Local boys all long

""keep the OCR at an expansionary level for a considerable period"...

So the expansionary level OCR is not leading to expansionary results then? More of the same then?

Maybe somethings wrong.

Nah -what could possibly be wrong? this is a SCIENCE.

Hi ham n eggs.

You write, "So the expansionary level OCR is not leading to expansionary results then?"

Think again! The economy is buoyant enough - with good levels of economic growth (GDP) being recorded.

TTP

The economy is buoyant enough - with good levels of economic growth (GDP) being recorded.

Yes, well, the Smartshares NZ Top 50 is going gangbusters since the dovish announcement and up 13% over P52W. Consumer spending is bubbling along too.

There is no depression in NZ.

Apart from an upwards blip about five years ago rates have been around the current lows since the GFC 2008. Whatever stimulus provided by this, has now run its course, well and truly. Don’t think any further drop will make much difference at all. with over ten years experience of these conditions borrowers and investors alike are simply resigned to the status quo and will carry on as usual.

Foxglove, lower rates will be stimulatory or may stave off contraction. All those properties bought in Auckland with 3% net yields, may become cash-flow positive. Avoiding diverting of wages into topping up negative cash-flow investment properties. Owner occupiers tend to divert the savings due to reduced mortgage rates, to paying down debt when the economic future is cloudy. This was the scenario from 2009 to 2013.

Which makes me think that when GFC2 truly kicks in (or is it just an extension of GFC1?), we might start to see rates more akin to say the UK...which for a 2 year fixed is about the same as our OCR. No wonder HSBC can come here and happily offer 3.69 - double what they'll get back home.

Yeah, it's hilarious when people talk of our mortgage rates being so low( granted they are by our own historic standard). Much of the world is 2% or less

Note that NZ's employment growth has been good as well.

In fact, NZ's economic performance has been pretty good overall compared with most of our trading partners. Would you rather be living in England right now?

TTP

I think DC at 16.12 articulates, much more succinctly, what I was fumbling around with, sort of.

Yeah but watch as the OCR falls and the interest rates stay the same. There is no direct link between the two and as we no longer even own any of the major banks they are doing what they want.

RBNZ's message (re interest rates) is likely to strengthen the housing market.

In any case, with continuing strong economic growth, low unemployment and relatively high wage increases, the NZ economy continues to perform pretty well.

But more needs to be done to increase the supply of new houses - and put the brakes on soaring rents.

Local authorities can make a contribution here: they need to reduce the costs of building/resource consents - and reduce the inefficiencies and stresses imposed on developers. (Ask anyone who's ben through the process in recent times. It's a nightmare.)

TTP

Rush in quick, house price can only go one way with such low interest rates

(if you can find the correlation between mortgage rates and OCR)

Hi Chairman Moa,

You write, "Rush in quick, house prices can only go one with such low interest rates."

That's your opinion - but I beg to disagree with you.

The housing market has been relatively flat for around 2.5 years now - especially in Auckland.

Further cuts in interest rates in the short/medium term might possibly have some impact on lifting sales volumes in some localities - but I'm highly sceptical re your suggestion/implication that house prices will rise significantly.

Realistically, the flat market will eventually come to an end - and house prices resume their long-term upward trend. But that would seem most unlikely in the next year or two - at least.

If I'm wrong, I'll take it on the chin!

TTP

TTP, did I say it will go up or down?

Anyhow, think of lowering the OCR is like fuel dumping when something isn't quite right on a plane. It'll be all depending how much fuel the pilots decided to keep for safe landing.

Can't you see sarcasm when it's staring you in the face?

He's that deeply embedded in his little bubble he's got a Labrador with a red jacket to go with the stripey cane.

So the article picture with Adrian Orrs head on a dove kinda freaks me out. NZD is down 1% on RBNZ announcment. Should keep exporters happy and give some general confidence to the economy. Biggest issue i see is we had a lot more easing room last go around, should a major recession hit there not as much dry powder left.

Since 2008, there is unlimited dry powder. It is called quantitative easing, and you can drive rates as negative as you like. The zero bound, no longer exists.

and if inflation comes knocking, good luck with interest rate hikes.

THE NZD fall made my hedging strategy look smart again, hopefully more than momentarily.

One way of looking at this is how many bank mortgage books have been kept in good standing by offering a 3.99% rate? If there is an OCR cut that produces a real drop in bank rates is that to help out the economy or a bank or two?

That is only if a lower OCR setting influences bank funding costs. Not much, I think. The main driver (70%) is the cost of customer deposits. The interest rate paid for these would need to fall significantly to allow significantly lower home loan rates. The OCR may in fact not influence wholesale rates much. That 20% or so of funding might get cheaper - or it may not if the risk premium for New Zealand rises because most of that is funded from offshore. And don't forget the Core Funding Raio requirement.

Just saying, a lower OCR may not necessarily mean much lower practical interest rates. Perhaps for those on floating mortgage rates (SMEs, credit cards) but not many others.

I have to agree. We saw the banks rates decouple from the OCR with the last move. I also do not think the banks have much room to move on the 3.99% rate. It seems like a promotional offer which is either break even or only has a few basis points of profit.

Dead right. OCR is not the main factor. For much of the media it's something they can make dramatic. You see more commentary sometimes before the announcement that after it.

Exactly right David, some of my TD's are coming out soon and if 3.4% is still on offer then realistically how far can mortgage rates fall in the short term ? also factor in the banks are now being forced to build in some reserve so they are trying to attract term deposits from investors.

why have money in TD now, the risk is high and the return is bad

I'm not surprised our NZX is still rising this year some of the dividend yields are starting to match TD rates

same as corporate bonds,

Indeed, my Mercury shares are up 16% since I bought them 6.5months ago, and they pay a ~4% dividend too. When my TDs mature I'll be moving them out of the bank and into a few more reliable dividend paying shares.

Hey Sharetrader, because I'm on like $40K a year while sleeping at night. If TD's are "Risky" then we are all screwed anyway.

This is a telling sign in itself of where things are at and its not a good sign either. For many years Central banks have been trying to normalise rates globally and the majority haven't been able to budge on their record low rates and now some are either having to reverse policy or drop even further. This is all happening while times are still relatively good but seem to be souring very quickly. A global downturn has started and god help us all if we face another financial crisis of some sorts as both Australia and NZ especially will not have the same amount of ammunition to fight with this next time around. The OCR may be kept low but bank capital requirements and risk premiums may even have the potential to push rates up slightly so lets not get too excited just yet about lower rates.

“However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.”

Or if one was to rewrite it “however, our efforts to devalue people’s hard earned savings and incomes while increasing inequality aren’t reaching our targets necessitating increased devaluation of the aforementioned.”

Yes related to that...

Jonathan Pie on brexit and broken social contracts

also this little gem, did neoliberalism and austerity cause the brexit?

IMHO the overlords are terrified of a switch from monetary to fiscal policy because despite all the talk they dont actually want inflation.

It certainly doesn’t leave much in the tank if they start lowering rates in a couple of months, even before the property market has started dropping nationwide. They must be very conscious of the plummeting Australian housing market, and that the RBA thought that would not happen as was caught off guard. Preemptive strike to help stop the same happening here? And then the start of massive QE as that property bubble does burst. Really not a good situation. Simultaneous property declines in China, Australia and NZ is likely what we’re looking at.

I do some work with a fairly big Chinese developer and they are notably bearish right now.

By way of comparison, here is Orr's statement from February, which looked very similar to the statements that came before it.

The Official Cash Rate (OCR) remains at 1.75 percent. We expect to keep the OCR at this level through 2019 and 2020. The direction of our next OCR move could be up or down.

Employment is near its maximum sustainable level. However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.

Trading-partner growth is expected to further moderate in 2019 and global commodity prices have already softened, reducing the tailwind that New Zealand economic activity has benefited from. The risk of a sharper downturn in trading-partner growth has also heightened over recent months.

Despite the weaker global impetus, we expect low interest rates and government spending to support a pick-up in New Zealand’s GDP growth over 2019. Low interest rates, and continued employment growth, should support household spending and business investment. Government spending on infrastructure and housing also supports domestic demand.

As capacity pressures build, consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

There are upside and downside risks to this outlook. A more pronounced global downturn could weigh on domestic demand, but inflation could rise faster if firms pass on cost increases to prices to a greater extent.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

Seems to be talking the dollar down without actually doing anything!

Be surprised it the OCR actually drops without any significant change in circumstances

The game is rigged in favour of asset prices, you can fight it or you can join in. Most here seem to fight it, though they are noticeably absent today

Well, the economists are well behind the eight ball. I have said for weeks there will be plural (2-3) cuts over the coming year.

Unfortunately the economists are in ivory towers rather than in the real world.

And Westpac are the worst culprits, 'surprised'....???? They only have to look at the housing market and talk to a few developers. What a waste of space (most) economists are. Taleb is right.

Bank economists are reluctant to call rate cuts as they make significant money on fixed rate loans and interest rate hedging products. Neither are required in a falling rate environment. Their collective track record is woeful in Australasia

I thought they were 'independent', ha ha

The RBNZ might also be referring to offshore risks to mask the real risks thst exist in the domestic economy. Given their mandate around stability, don't want to spook the locals TOO much.

"Government spending on infrastructure, housing, and transfer payments also supports domestic demand." - That is where the focus should be now globally and in NZ. Lowering the OCR won't do much at all. Either the cuts won't be passed on or even if they are households have so much debt they can't borrow much more , no matter how cheap. We certainly won't be!

Agree.

But this government is so useless (although I think Ardern is great) that they don't have a chance in hell of getting a coherent infrastructure and housing programme humming along. We have a total clown in charge of both key areas.

Both governments have been useless around the supply side of housing, both put their Inspector Clouseau in charge, NS and PT.

it makes you wonder if they even want to fix that side of the equation or like the movie put people in charge so it does not get solved

This is a scary thought - as regulars know I am far from a National Party apologist - but Twyford is making Smith look quite good.

Smith was instrumental in the Unitary Plan, and although SHAs were far from perfect, I think overall they delivered more positives than negatives.

So far Twyford is 'all talk, no action'. Let's see if he can surprise us this year and introduce meaningful policy....

Excellent commentary CS....may I also add stagflation is now a serious risk. Not good at all...

Mmm I can't see high inflation on the horizon

I can't either. Stagflation in my opinion was fundamentally linked to a supply-side shock, namely OPEC increasing the price of oil in a political manoeuvre, a key commodity essential for everything. This combined with a highly unionised labour force and capital that felt willing to pass on price increases led to a wage price spiral - indexation of wages for example was involved. I don't see any negative massive supply shock as on the horizon. Nor the labour market conditions for a wage-price spiral. We need better ways to deal with supply shocks than simply slashing demand and creating unemployment. If a key commodity massively increases in price we need a way of sharing that real burden between capital and labour without resorting to a wage price spiral. But the experience of 70s stagflation should not prevent us from using fiscal policy now in the current situation. It as almost as if the 70s stagflation has become a ghost with inordinate power over today's economists. Stagflation may have been tough but to my mind, a lot of today's economic problems are pretty much as bad.

Valid argument, but I think most central banks including the Reserve bank are set on weakening the currency to stimulate growth. I also suspect that we might just import inflation higher, quicker and faster than expected. How does the reserve bank respond in this case? Raise rates, suppress any lingering growth while raising consumer default rate or let inflation run hot ? It's a juggling act no central bank wants to play, but might just be the discussion in the not too distant future.

Much to say here but I would read MMT economist Bill Mitchell

"Is exchange rate depreciation inflationary?"

http://bilbo.economicoutlook.net/blog/?p=32922

In short, "The real world tells us that the ERPT (exchange rate pass through) is weak in most nations for which coherent empirical research has been conducted.There is some pass-through but not enough to trigger a hyperinflation and certainly not enough to derail a full employment program based on stimulating domestic demand."

IMHO, unemployment is always and everywhere a bigger "cost" than some inflation.

I'm feeling decidedly Japaneses these days...too much debt...stagnation...deflation....GFC never really went away it seems to me we just piled cheap money over it to try and hide it then looked away to watch our house prices go up and up...but its still there....and about to remind us of that fact shortly.

Yep

We're an economy of forever blowing bubbles

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.