Four months on from when the global pandemic forced shutdown of the New Zealand economy there are still a stack of unknowns, uncertainties and risks ahead of us. However, arguably the economic situation today is considerably better than the dire picture painted for us by most economists back in March and April.

Looking ahead, the following eight questions for the NZ economy (therefore, in part, for the NZ dollar value) require some analysis and balanced answers: -

1. What happens after the wage subsidies end and the retail sugar rush is over?

Consumer spending has rebounded more dramatically over recent months than most imagined. The reasons for the bounce are apparent now, however they were not so obvious in advance. (a) Kiwis spend $9 billion per year in overseas holidays (European and Pacific Island holidays at this time of year in particular), this winter that money is being spent in the domestic economy. (b) The residential property market has not tanked as all the gurus predicted - due to lower mortgage interest rates, returning expats buying houses and job insecurity not being as bad as originally feared. (c) Outside of foreign tourists, life in New Zealand has pretty much returned to normal and so has consumer behaviour.

The retail rebound appears sustainable over coming months, as again outside of the tourism/travel sector, job losses are not looking as severe as earlier forecasts. Overseas travel is off the agenda for a while and the cash saved is being spent elsewhere. It is always about confidence for consumers (and thus business) and that is why the Government needs to make some decisions and announce their ongoing support programmes (for those who genuinely need it) for the economy after the wage subsidy scheme ends on 1 September.

2. What is behind the massive rallies higher in NZ shares and the NZ dollar when the economic outlook is so uncertain?

The local financial and investment markets are reflecting where investors with cold hard cash to deploy are preferring to invest their funds. NZ dividend stocks are in hot demand as the alternative investment homes of bank deposits and bonds offer close to zero yield returns. A number of our large listed companies are also beneficiaries of the new world order (e.g. F&P Healthcare and A2 Milk). The offshore investors into our shares and dollar are also providing a signal that our economy is poised to outperform others due to the dominant trade connection to China, who (as expected) are well ahead in economic recovery terms compared to the US and Europe. The markets generally provide a clearer and more accurate picture of future conditions than economic forecasters.

3. Has our local political risk suddenly increased?

Up until very recently “political risk” was observed as being relatively low for the Kiwi dollar exchange rate. Jacinda’s “kind and sharing” public popularity providing a sleep-walk to a sole Labour victory or a return of a Labour/NZ First Coalition at the upcoming 19 September general election. Latest polls point to NZ First disappearing and the Green Party potentially replacing them in a coalition with Labour. Should that result occur and the Greens secure big policy concessions in the post-election coalition negotiations, the Kiwi dollar is likely to depreciate as anti-farming, anti-business and anti-development policy changes damage the economy and investment. Expect to see increased FX market responses to political opinion poll trends over coming weeks.

4. Why is China so important to the NZ economy?

It is no coincidence that the NZ economy has enjoyed on average higher GDP growth rates over the last 12 years since the China/New Zealand free trade agreement was signed in 2008. Our exporters have direct access to 400 million middle-class consumers of imported food. Our importers of consumer products from China receive the benefits of manufacturing economies of scale. Booming exports and lower inflation are good news for everyone in New Zealand. The argument that our economy is overly dependent on one market and we are at enormous risk if something goes wrong in China does not wash with the writer. As the response to the coronavirus pandemic has shown us over recent months, the Chinese are much more disciplined and organised at dealing with crises/shocks than our American friends.

5. Will we import global deflation?

The economic theory goes that a global recession results in lower prices for goods and services as consumer demand wilts. The RBNZ will be building-in global deflation to their updated forecasts on NZ inflation when they deliver their upcoming Monetary Policy Statement on 12th August. Will they be correct in that assessment? The current world economic downturn is different to all previous recessions. Faster down and faster back up. Commodity prices have not reduced as the theorists would normally expect, many have increased! Supply challenges are in abundance and New Zealand’s inflation is always supply side driven, not demand driven. The view is that we will not import deflation to the extent most predict and domestic (non-tradeable) inflation continues to run at +3% per year.

6. Where is the Government’s economic plan?

Most pundits would agree that the Ardern/Robertson Government team of two made smart decisions in respect to the March health emergency and life-support measures for the economy. However, time is moving on and we still seem to be waiting on the Government’s plan for the recovery phase for the economy. Election campaign tactics delaying Government policy announcements is currently frustrating business who is seeking more certainty on the future landscape. Or, it could be that there is no plan and the Government is relying on “hope” that the economy will recover without doing anything differently to the past. The universities have a plan for re-booting their large foreign student industry, however the Government is not taking any risks ahead of the election.

7. Is it good luck or good management that the agriculture export sector is the saviour of the economy?

It is with considerable irony that the Government is now lauding the agriculture/horticulture export industries as the good guys who saved the economy from oblivion. Not so long ago the relationship between the Government and the rural sector was strained due to anti-farming policies on carbon, water and resource consents required to itch your bum! Agriculture science has always been the backbone of our economic well-being and will continue to do so through forward-thinking rural woman and men who seek new ways to sell quality food and products to the world. Luck really does not come into it.

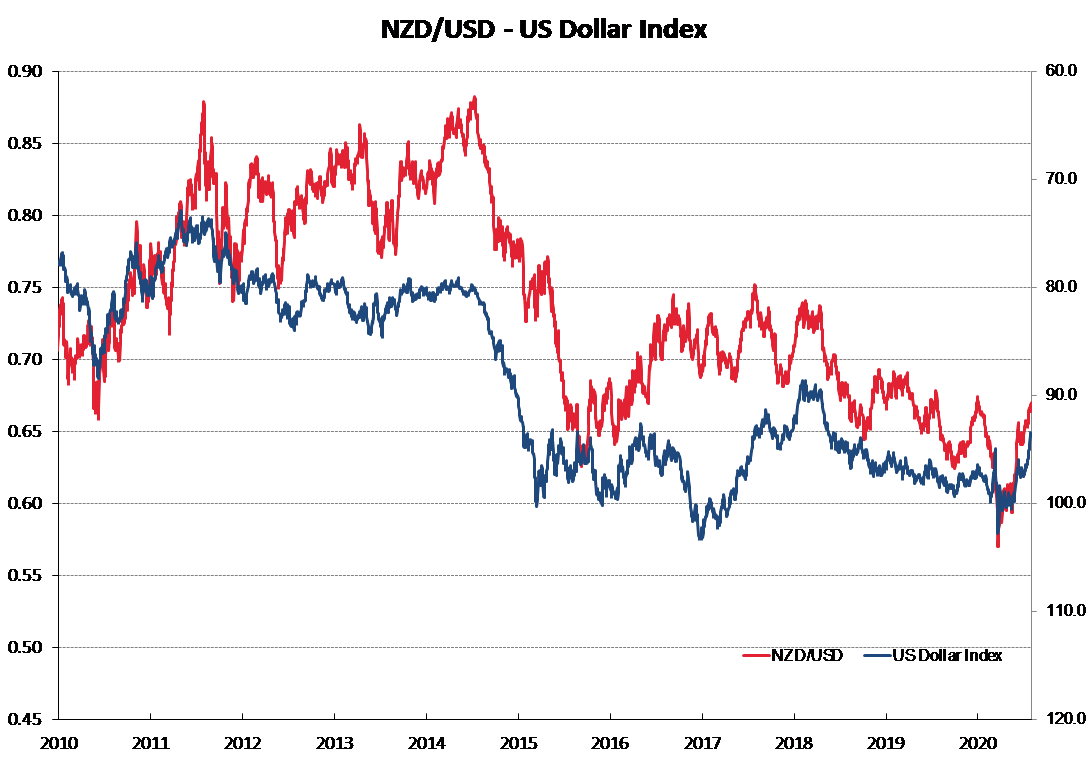

8. Will US dollar value shifts still dominate NZD/USD exchange rate movements?

Absolutely! Over the month of July, the US dollar suffered its worst month in the FX markets for over a decade – down 4.4% against is biggest peers. The US’s poor response to the Covid-19 pandemic and a for a host of other reasons cited by this column over many months, the US dollar is undergoing a paradigm shift in value as the deficit and debt chickens come home to roost. The USD has weakened 6% against the Euro from $1.1200 to a high of $1.1900 over the month, by comparison the NZD has only gained 3% from 0.6500 to a high of 0.6700. The Kiwi dollar’s underperformance vis-à-vis other currencies against the USD is due to the proximity of our election and the lack of speculative interest in the currency at this time. In the short-term, the USD is due for a correction upwards after its recent sell-off, therefore there is still a greater probability of an NZD/USD pull-back to 0.6500/0.6400 from the current 0.6625 spot rate. In the medium term (three to nine months) the US dollar still has a lot further to depreciate, resulting in a higher NZD/USD rate. A US dollar Index down to 80 (currently 93.5) would have the NZD/USD rate at 0.7500.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

28 Comments

NZ economy is not fully insulated to overcome this pandemic. The real pain will start from next month.

“Yawning gap between the real world and the stock market that has become increasingly divorced from

reality “

https://www.abc.net.au/news/2020-08-03/why-your-house-isnt-worth-what-y…

Terrible article when the author doesn't understand how housing market crashes cannot be read from indicators like sales or price indexes. Mind you, this is how the majority of people think ("I can't see a property crash therefore it doesn't exist or can't happen").

So what would you prefer is used? Mortgage lending (up), auction clearances (stable to up), residential building consents (moving up), mortgage deferrals and IO arrangements down. Mr Kerr stated a fact - the foreshadowed "crash" by so called experts hasn't eventuated. I'd say he probably knows what he's talking about and writes a good relevant article.

So what would you prefer is used? Mortgage lending (up), auction clearances (stable to up), residential building consents (moving up), mortgage deferrals and IO arrangements down. Mr Kerr stated a fact - the foreshadowed "crash" by so called experts hasn't eventuated. I'd say he probably knows what he's talking about and writes a good relevant article.

My comment is not related to Kerr's article. It's related to the quoted article from the ABC.

But if Kerr is stating that a bubble cannot crash because it hasn't, he's not worth the time time of day similar to to the ABC.

I didn't read it because I really don't care about aussie and haven't been following very closely what's happening over there.

I didn't read it because I really don't care about aussie and haven't been following very closely what's happening over there.

Probably best not to comment if you're not informed. Regardless, Aussie or NZ is irrelevant in regards to suggesting to understanding how property bubbles unwind by looking at sales data and indexes at a point in time like now.

Well Ben didn't help by posting a comment related to Australia first up. You're right though, I should have read the article first, which incidentally I don't think is particularly applicable to NZ at this point in time. I do agree it's far too early to call - let's see how the next 6-9 mnths go

It astounds me that people can be so color-blind to China's misbehaviour.

Talk about corrupted by the CCP's influence!

Apart from N Korea & Iran, China seems to have few real friends and much of the World is pointing a finger at China for Covid 19 and by now perception will likely trump any facts that China may espouse in mitigation. This will change buying habits and supply chain changes all of which are negatives. Should the 3 Gorges Dam breach the devastation for the 400 Million Chinese living alongside the Yangtze River from the Dam to Shanghai is unimaginable and China will need urgent help from the world, especially food so China may need to rebuild some bridges and change its stance to get such help.

Lots of right of centre commentators sudden conversion to the good nature of government spending and intervention is a massive hypocrisy. Spent 45 years telling us all the it is bad for economy. Now that business "needs" this that and the other, the tune has magically changed. it is a larger version of socialising risk (which banks only are supposed to be guilty of) on an economy scale.

Yes MK29. They're starting to engage in 'self preservation.' Also, those higher up the right-of-center chain of command have always been quite partial to cronyism only if it benefits them.

It just shows them up as the self serving individuals they are.

Little government when it's good for them.

Lots of government when it's good for them.

The only consistency is their self interest.

Finally , someone has said the RBNZ may use the "D" WORD in the update on 12 August .

Lets hope so , we cannot continue to pretend this risk of deflation, which has been evident for a while now, is not recognized and dealt with .

Its a very real risk , and I have said for a while now that the inflation / deflation numbers have been fudged .

Can you explain, please, why imported deflation is negative for the economy? Lower costs of capital goods, cheaper consumables, e.g. petrol, and less expensive consumer discretionary items -- I don't see why those would encourage less economic activity inside the economy. Thanks.

@fishoutofwater ......the problem with deflation, is it comes with a fall in consumer spending ( this may seem counter-intuitive at first glance ) as people put off spending in anticipation of even lower prices .

A secondary issue , is that wages either fall ( due to less work ) or hours are shortened , and we are seeing evidence of this already . We are also seeing some trades in the construction sector becoming very competitive in pricing .

Now this fall in prices would not apply so much to immediate needs like food , but it manifests itself elsewhere, like say commercial lease renewals or if you take my practice where we lease our vehicles ....... the vehicle leasing company is offering really good deals to take out new leases ( early ) with quite enticing offers .

What they dont realize , because we have not told them , is that we are not going to renew the leases at all . Its way cheaper to buy the end-of -lease vehicles right now or buy new vehicles and get the long warranties on offer.

In fact we are going to buy 3 of the existing lease-fleet vehicles and give them to staff to run themselves ( with a fuel card limited to one tank or $100 per week) . Our current employment contracts do not make provision for us to give them cars , and its always been clear that this is purely discretionary.

The other places where its problematic with deflation , is where prices of commodities fall , like aluminium which is sued to build aricraft , which means that Tiwhai can no longer make a profit , even if electricity were almost free .

Deflation is way worse than inflation ......... there are no monetary tools to fix it , and it erodes asset values , affects pensions and can gut savings and investments.

Over the medium to long term deflation is very destructive

Boatman - last week I had my first experience of deflation when selling 4 Prime Cattle at $1.5 a Kg Live weight against $3.20 pre christmas.

Even if you are in the South Island, if they were truly prime cattle that's not deflation, it's robbery.

Time for NZ to think of new fields where we can do better, like Healthcare software, start ups for new entertainment on phones/tablets.

Our companies may have to lessen their dependence on Aussie and the European markets.

China has still a way to go, so we should strengthen that, though it will be tricky with the politics placing the hurdles.

I also believe that NZ needs mode medical universities to produce more healthcare professionals for the future. We may have to team up with appropriate instituions overseas for this, but taking it as a challenge it may pay off very well.

The Education Sector needs an overhauling and again we may need some outside help in conceiving plans for that. Politics need to understand that.

We should leverage our current goodwill and reputation for sensible governance during crises and attract funds for new jobs creating ventures. In Tourism and Agriculture and Fisheries, Transport Infrastructure, etc. There is much money floating around and even if we manage to get a small percentage it will be very fruitful. A brain storming session of the Great Minds of Aotearoa is necessary to identify. Can Auckland University take the lead for gathering such minds soon ?

This was a good article except for this giant piece of speculative fear mongering:

“Should that result occur and the Greens secure big policy concessions in the post-election coalition negotiations, the Kiwi dollar is likely to depreciate as anti-farming, anti-business and anti-development policy changes damage the economy and investment.”

Labour has proven to be very secure with economic policy, and calling the greens “anti-development” is laughable - the greens policy is for massive intensification of housing density in cities and big investments in public transport infrastructure, healthcare, education and massive sustainable energy projects - all of which would really juice the economy.

They would, if anyone in the private sector was incentivised to fund them from work or as an investment, the Greens current tax policies heavily discourage both.

Yes agree. Ridiculous scare mongering over the highly likely Lab Green coalition post Sep 19. It will be far more stable than what we have at the moment. Dragging farning into the 21st century isnt such a bad idea. James and Jacinda seem to get on well and act sensibly without grandstanding.

I am still picking 88 Kiwi cents to the US$ within a year .

The Fed wants and needs a weaker US$ to stimulate the US economy , otherwise why would it print so much in QE activities ?

With worldwide deflation evident in its trading partners ( primarily the EU, JAPAN and CHINA ) those countries weak or managed currencies render US products uncompetitive and will destroy what is left of US manufacturing , so the US will almost certainly want to see a weaker US$ in the short to medium term .

Mineral Commodity prices ( other than gold and silver ) are under immense strain , and and bulk food (grain ) prices are all over the place, as China shifts its buying patterns .

Devalue of US$ will nominally inflate commodities traded, but in real terms prices could remain flat to deflated as local currency will need to move in lock-step.

US economy is mainly internally driven.. US multinationals will not be affected as cost structure is where manufacturing is - China, SEA etc..

QE was/is done to holdup low-productive, debt fueled corporations... the so called stimulation is running out fast of stimuli and will do nothing for man on the street

"The argument that our economy is overly dependent on one market and we are at enormous risk if something goes wrong in China does not wash with the writer."

Suggest you read the main export market for tourism, dairy product, logs, education etc.

No export market should ever comprise more than 25% of the overall market.

That China got above that comes back to laziness and greed.

And political interference and buying of NZ assets by mainland companies. It's a shambles.

Roger has almost never ceased to amaze me in the years I have followed his column. He's been consistent though.

The article says that CBA says house prices will be 11% down over the next 3 years. So all those with a bit of equity will be okay. Just check the time frame of the last 11% rising of house prices in Aussie.. Anyone who bought before then and has paid a bit of their mortgage off will be equity okay. If their unemployment goes to 15%, then 85% will still have jobs, and a percentage of the 15% won't own a house anyway , so something substantially under 15% of mortgage holders will be in trouble and at risk of enforced sale. Remember that it is not depressed house prices which is the problem for Aussie home owners, it is having to sell your house at those depressed prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.