Summary of key points: -

- Market conditions and incentives shift in favour of the US dollar

- New USD strength directly impacts NZD/USD rate

Market conditions and incentives shift in favour of the US dollar

Game-changing events that cause major turning points in the value and direction of exchange rates do not occur very often and are nigh impossible to identify in advance. However, when they do happen, more often than not it is not just one thing that causes the sudden reversal in market pricing, but a combination of developments and realisations that prompts the herd to change their behaviour and thus buying or selling actions.

Over recent weeks a combination of political, economic and medical factors in the world’s largest and most influential economy, the USA, may be culminating to provide a substantial change in sentiment towards the US dollar.

To incorporate some perspective on the view that the US dollar is more likely to appreciate from current levels than remain under further downward pressure, we first have to understand where we have come from and why.

When the EUR/USD rate was trading in the $1.1000 to $1.1200 region throughout the year of 2019 the trade wars between the US and China were keeping the US dollar strong as it was seen a safe harbour currency against global trade and economic uncertainty. The medium term forecast for the USD at that time was that it should weaken under the weight of the US economy’s dual deficits (international trade deficit and internal Government budget deficit).

However, there was no catalyst or trigger to shift the EUR/USD out of its established range. The environment for the USD changed dramatically in 2020 with the Chinese trade tensions reducing, the Covid pandemic causing economic carnage and the US Federal Reserve printing billions of additional US dollars to save the US economy from freefall into depression.

In response to those changed circumstances, the USD depreciated from below $1.1000 to $1.2350 against the Euro by late December 2020. Growth and commodity currencies such as the AUD, CAD and NZD were preferred by the currency speculators over the beleaguered USD. Political risk factors surrounding the US Presidential election in November 2020 added to the USD’s woes at the time.

The US dollar has depreciated 12% against the Euro over the last 12 months. The question on its likely value going forward, is whether it has already weakened to a point where European investors are prepared to buy US dollars to buy US Treasury bonds to provide the funding for the US’s ballooning budget deficit and debt amounts. The incentive to shift investment capital into the US from Europe has suddenly improved with US 10-year Treasury Bond yields now above 1.00% compared to German Bunds at -0.50%.

Recent signs are that global investors will be more attracted back to US dollar investments given these new market conditions, compared to what Euroland has to offer: -

- The interest rate yield differential for long-term interest rates is significantly in the USD’s favour.

- This week new US President, Joe Biden will be pushing through his US$1.9 trillion fiscal stimulus package that will certainly boost US economic numbers in the short-term. The “blue-wave” of the Democrats controlling the Presidency, House of Representatives and the Senate allowing a swift passage for the legislation.

- The Covid vaccine roll-out is being sped-up in the US, whilst Europe has distribution problems. The US economy is set to recover faster than Europe.

- Political risk has reduced in the US, however increased in Europe with the Dutch Government resigning and the Italian Government on the verge of collapse (is it not always!).

- Investment flows into Emerging Market economies (and thus currencies) over the last nine months are likely to reverse as rising US long-term interest rates is never good news for these countries.

One further factor that typically causes US dollar strength is a “risk-off” mode in global equity markets, the USD seen as safe-haven currency by investors. To date we have not seen any sell-off in equities. However, many are questioning the sustainability of the rising values of the FANG technology stocks in the US. A downward correction in equity markets is inevitable at some point, we just do not know the timing. The NZD/USD exchange rate will follow that downward adjustment when it does happen.

New USD strength directly impacts NZD/USD rate

The EUR/USD rate has already reversed engines from the Euro high of $1.2350 reached on 6th January and has pulled back to $1.2080. The closely-tracking NZD/USD rate topped-out at 0.7315 on the same day and his since retreated to 0.7130. As highlighted in last week’s commentary, a NZD/USD close below 0.7200 signals a breaking of the uptrend line on the charts that the Kiwi has kept above since 0.6600 in early November 2020. The turn-around in the EUR/USD market sentiment and direction could see that rate return to the $1.1500/$1.1600 area over coming weeks/months. The forecast 5% appreciation of the USD against all currencies would reduce the NZD/USD rate back to the 0.6700’s.

The US dollar side of the NZD/USD currency pair for the above reasons is expected to dominate the Kiwi’s movements (i.e. lower) in the short to medium term. The local economic and market influences on the NZD side of the exchange rate are more of a mixed bag: -

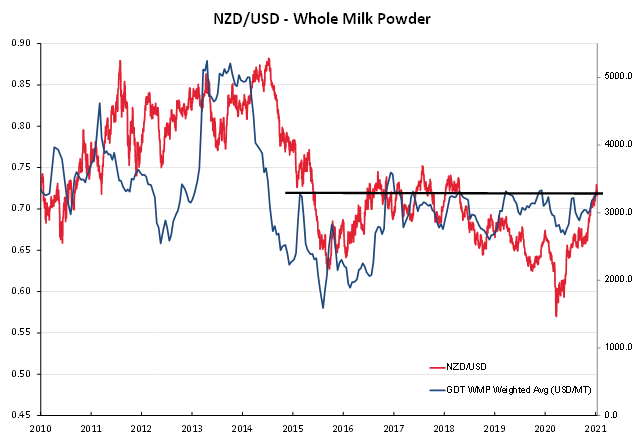

- Whole milk powder (WMP) prices above US$3,000/MT have always been supportive of the Kiwi dollar (except for when the RBNZ was slashing interest rates in 2019 and 2020). Over the last four years WMP buyers have substituted other protein for WMP when the price has moved above US$3,300/MT, therefore producing a cap on the WMP prices (and perhaps the NZD/USD rate as well – refer chart below). A Global Dairy Trade auction this week may see an end to the price increases witnessed over the previous four auctions.

- NZ inflation figures for the December 2020 quarter being released on Friday 22nd January will be above RBNZ forecasts of +0.20%, a positive for the NZ dollar.

- The local share market (NZX50 Index) hit a peak of 13,624 on 7th January, however a subsequent wave of selling has sent the market down 4.5% over this last week. Disinvestment by offshore investors from NZ equities and the NZ dollar is likely to continue as they take profits on sizeable gains on both legs over the last nine months.

Local USD importers should have already increased their hedging percentages to maximums of policy. Whereas the risk of further adverse currency movements has reduced for USD exporters, who can therefore allow hedging percentages to reduce by attrition (not replacing maturing hedges).

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.