The future direction of New Zealand’s economic performance and also therefore the future direction of the NZ dollar value will be governed by varying doses of good luck and good management.

As the economy seeks to recover from the latest shock of the largest city, Auckland being locked down for the last 10 weeks, it is timely to reflect on what the positive and negative influences will be on the economic outlook i.e. The Good, the Bad and the Ugly!

The Good

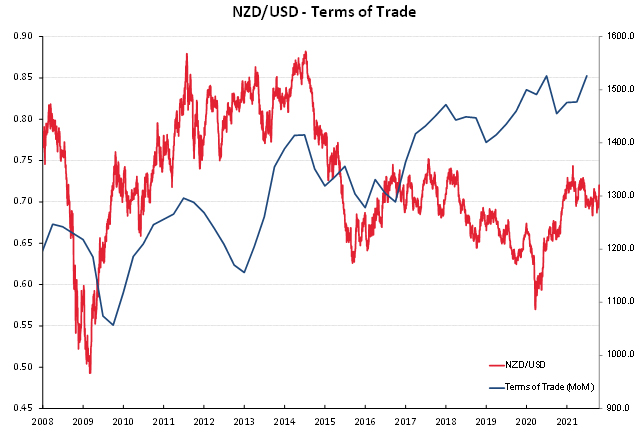

- Export commodity prices: On a wider economic front there is no question that high export commodity prices have been the saviour of the economy in 2021. Dairy, sheepmeat, beef and horticulture prices are at very attractive levels and the extra income coming into in rural New Zealand encourages spending and investment. Farming groups have suddenly gone very quiet compared to the protest marches of a few months ago against excessive Government interference and regulation on water, carbon and land use. With the milk price above $8/kg and this season’s lamb prices at record levels over $9.50/kg it may mean that it cannot get much better than this. Our Terms of Trade Index which measures export prices relative to import prices has returned to over 40-year highs (refer chart below). Luckily for the economy, export prices increased 8.3% in the June quarter to more than compensate the 4.8% increase in import prices.

- UK:NZ Trade Agreement: Non-tariff access for our export produce into any international market is always good news for the NZ economy. The recently announced UK free-trade deal is a fantastic development and enhancement for our wine, honey, dairy and lamb exporters into the UK market. There is a massive touch of irony in that the Brits are now abandoning their tariffs and duties on our exports, having abandoned New Zealand’s exporters in the 1970’s when they joined the EU. Now they have decided to pull out of the EU they are looking for trade friends. However, we should not kid ourselves that the UK has singled New Zealand out for some special attention. Their prime objective with this free-trade deal is to get invited into the CPTPP club so that they have better access into Japanese and Canadian markets.

- Higher NZ interest rates: Whilst increasing interest rates are negative for leveraged residential property investors, bond investors (bond values/prices go down as yields rise) and arguably share investors, the higher yields have traditionally been positive for the NZ dollar value. However, a feature of the rapid increase in the two to 10 year interest rates over recent months (as they price-in successive OCR hikes form the RBNZ) has been the lack of response by the FX markets to buy the NZ dollar. Offshore investors who loved the NZD “carry-trade” a few years back when our two year yields were 3% above those available in the USD, are today not attracted to the NZD as our 1% yield differential is insufficient to compensate the FX risk.

- NZ tech companies take on the world: Whilst the media have concentrated on our technology companies being sold out to offshore owners (e.g. Vend, Timely, Seequent, Ninja Kiwi, Rocket Lab), the real success story is the NZ tech companies expanding globally by buying complementary businesses elsewhere in the world (e.g. Straker Translations, Eroad, Pushpay, Vista, ikeGPS, Joyous and many more in the fintech and medical/health space). Our immigration policies need to be adjusted to allow tech people resources into New Zealand, otherwise the tech companies will relocate to Sydney or Singapore.

- AUD appreciation/USD depreciation: The NZD/USD exchange rate being pushed higher due to a stronger Australian dollar (which we follow) and a weaker US dollar against all currencies in 2022 has been well canvassed in this column over recent months. In the short-term, one last bout of USD gains against the Euro to $1.1500/$1.1400 cannot be ruled out due to potentially large US jobs increases in October and November and the Fed making the tapering a fact at their 3 November meeting.

The Bad

- Chinese slowdown: Whichever way you look at it, a slower pace of economic growth in China is not good news for the NZ and Australian economies. We may see the first signs of the changes and problems in China impacting directly on the NZ economy through export log prices. Log inventory levels in China have increased due to electricity outages, environmental restrictions on sawmills and uncertainties in their property/construction sector. Lower prices to NZ forestry exporters and slower harvesting rates over coming months seem inevitable.

- Inflation: The RBNZ may have to be more cautious about ramping up interest rates to slow demand in the economy and control inflation. Sharply higher petrol, food, rental and electricity prices will already be reducing discretionary spending for many households without having substantially higher mortgage interest rates on top. In any case, higher interest rates will not control the underlying sources of the inflation which is all coming from the supply side. Expect to see the RBNZ dial-back on the current higher market pricing of future interest rates in January/February when we will have the weaker economic data coming through from the August to November lockdowns.

- Government and household debt levels: Finance Minister Grant Robertson has somehow hoodwinked the mainstream media into believing that the massive additional Government borrowing for Covid is not a problem for the economy as our government debt/GDP ratios are lower than other countries. When combined with enormous increases in household debt levels from the property boom, overall debt levels are unsustainable and potentially dangerous as we have nowhere to go if another global shock hits us.

- Government economic policies: Policies to stimulate investment and economic growth to repay all the extra debt are not on the current Government’s agenda. Unforgivably, labour market regulations, immigration policies, foreign investment turn-offs, water and climate change/carbon policies are adding cost and restrictions to the business sector. Why New Zealand has to be world-leader in climate change policies that imposes costs and lower incomes is a mystery to the majority.

And The Ugly! (or potentially ugly)

- Commodity price risk: New Zealand’s economic recessions always come from a collapse in our export commodity prices (1990, 1999 and 2009). We could easily go there again if for some external reason the current high prices dramatically reverse. In addition, should the RBNZ go too hard too early with monetary policy tightening over coming months which causes a domestic downturn in 2022 due to lower house prices, the economic outlook would turn really dark. It is not being suggested that this “doomsday scenario” for the NZ economy is likely, however it is a risk that cannot be totally ignored.

- Covid ill-preparedness whacks SME’s hard: The belated additional government support payments for Auckland businesses announced last week has perhaps come too late for many. The damage to the economy from the delta lockdown is not yet evident in the official statistics, but it will come out over coming months. Not being prepared for the arrival of the delta strain and thus implementing the only response policy they had (lockdowns) has been a disaster and the public of New Zealand should feel let down by our elected politicians in this respect.

- Equity market correction: Despite all the positives for the Kiwi dollar in the form of high commodity prices, higher interest rates, a rising AUD and a lower USD, the one potential party-pooper is a correction downwards in global equity markets. The NZ dollar always moves lower in the forex markets on equity investor’s switching to a “risk-off” mode. Rising US interest rates have always been seen as the one catalyst to spark an equity market sell-off from the continuous rally upwards over the last 18-months. The Fed’s 3 November meeting may be the reality check for the equity markets that changes the sentiment and direction.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

7 Comments

Well rounded article.

Another excellent article.

I agree with your bearish position on the extent to which the OCR will be raised.

The upside for the Labour Govt from here on in is all downhill. It's hit the expected 4th Year blues that most NZ govts seem to go through. After spectacularly dropping the covid ball in 2021, after getting so much right in 2020, Labour trajectory will need skis for any momentum. Their segregationist policies involving health & water show their real hand & it is stark. Handing power to Maori who have no idea how to run their own households let alone water entities of health services, is a sure sign of their ineptitude. Strewth, they can hardly run their own tribes without much shouting & screaming & gnashing of teeth. Not saying they can't do it, Just pointing out they're a long way from ready as of today.

It will be a sale of a lifetime for farmlands and tech start-ups ups just as Harry Dent has hoped.

Excellent article thanks.

"enormous increases in household debt levels from the property boom, overall debt levels are unsustainable and potentially dangerous as we have nowhere to go if another global shock hits us."

Household net financial worth is up $300bn in the last two years - and mortgage debt as a % of financial wealth has been trending down since 2009 (from 19% to 16%). Important to recognise therefore that risks associated with household debt levels are limited to a subset of the population - and that the net position has actually improved over the last couple of years.

Govt has plenty of places to go if another global shock hits us - it is not 'money' that we are short of, it is energy, resources and productive capacity (the real stuff that economists typically ignore.)

I wonder also if there will be a skills crunch, the hermit kingdom will soon have to join the rest of the world and we could see a mass exodus of skilled labor moving overseas. Australia is expanding infrastructure on a large scale and there is also a big drive over there for extra health care workers. IT, especially cyber security is also in high demand as the growing threat of China increases requirements for better security. One of the easiest markets to get labor from is NZ and many are fed up in NZ with the socialist behavior of the hermit kingdom and the division of this country between different groups who seem to hold hostage or accuse the majority of racial disadvantage (but still want our tax dollars), often promoted indirectly by hermit kingdom policy and agenda. Only a working middle class professional fool would choose to stay in NZ now that covid has opened the doors to WFH and many smaller nations start to offer digital nomad visas at near zero tax levels.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.