By Roger J Kerr*

A marginally weaker than expected GDP growth number in Australia (+0.2% actual against a +0.3% consensus forecast) for the December quarter sent the AUD into another tailspin lower this past week as bets were increased that the Reserve Bank of Australia will cut their official interest rate sooner rather than later.

The AUD depreciated against the USD from 0.7100 to a low of 0.7015 on 7 March, pulling the Kiwi down from above 0.6800 to a low of 0.6755.

However, subsequently both currencies have recovered upwards by half a cent each as the US dollar weakened on global markets on Friday 9th March on very soft US employment figures.

Primarily due to adverse winter weather conditions there were only 20,000 jobs added in the US in February (prior forecasts were for+180,000) following the very strong 300,000 increase in the month of January.

The previously forecast 0.6800 to 0.7000 trading range for the NZD/USD exchange rate still seems reasonably robust over coming week/months provided the influential Aussie dollar can hold its composure above 0.7000 against the USD. The short-lived Kiwi dip down to 0.6755 was an opportunity for USD exporters to top-up hedging levels.

Why FX markets are always looking ahead

How the FX markets reacted to the weaker Australian GDP growth numbers was a little surprising as financial markets are normally forward looking to future expected economic conditions, not what happened historically four, five and six months ago in October to December last year.

There was a lot of uncertainty in the final few months of 2018 with the US/China trade wars, tumbling global share markets and the US Federal Reserve signalling three interest rate hikes in 2019.

Those negative offshore factors coupled with falling residential real estate prices in Australia were sufficient to cool off construction and consumer spending activity levels in the December quarter.

However, there has been a paradigm shift in sentiment and outlook since the start of January that dramatically improves Australian economic performance going forward in this commentator’s view.

Equity markets have recovered, the US is close to a historic trade agreement with the Chinese, commodity prices have increased sharply and the previously priced-in US interest rate increases have disappeared.

Whilst there may have been justification for a weaker AUD exchange rate six months ago, however that is not the case today.

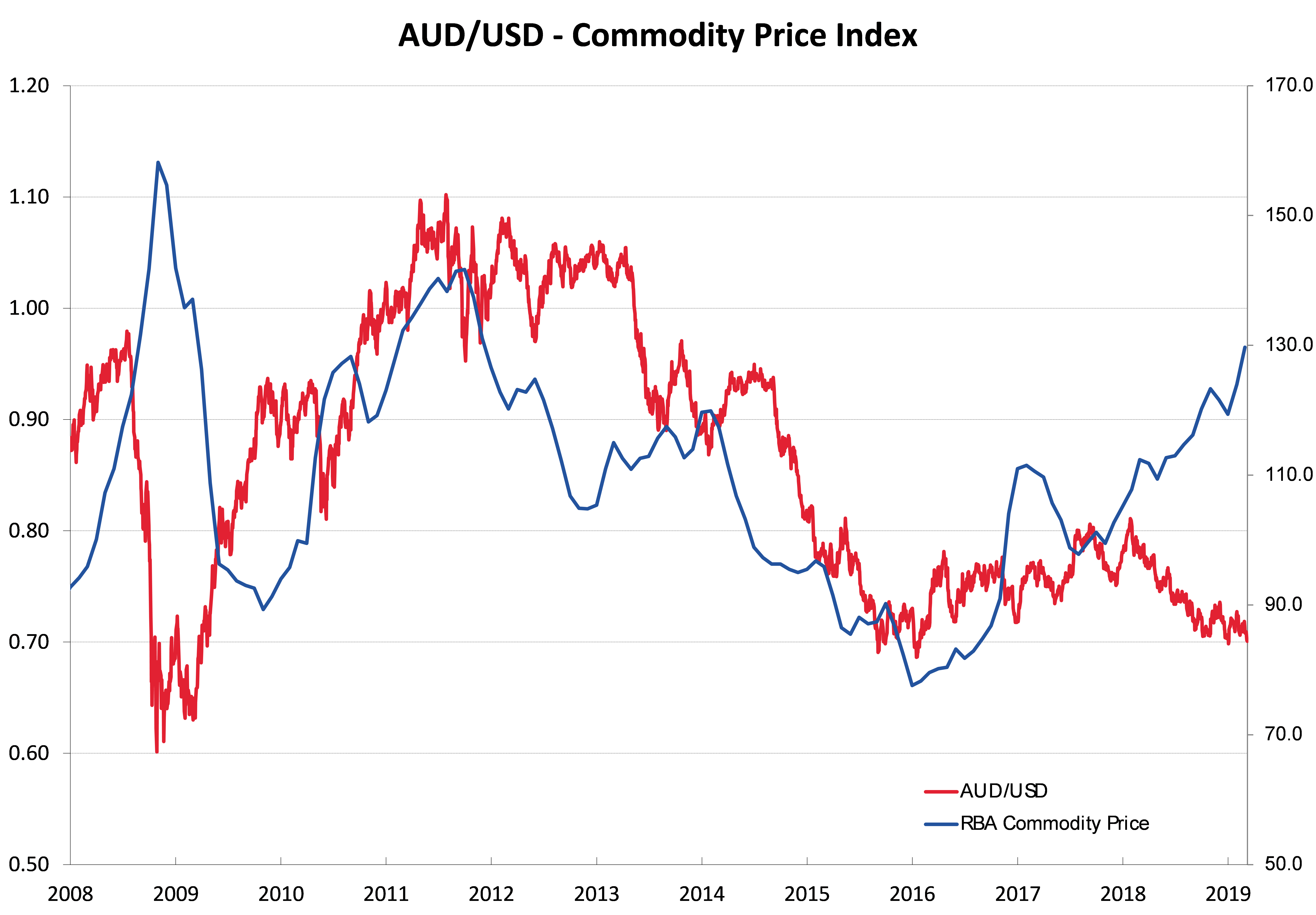

Profitability (thus activity levels and investment) in the mining and resources sector has always played a dominating part in the performance of the Australian economy, and the recent higher commodity prices (iron ore and copper) combined with the weaker AUD exchange rate has substantially increased prices and profits for the mining companies.

Mining and resources stocks have driven the Aussie share market back up to new highs over recent weeks.

For this reason alone, the outlook for the Australian economy in 2019 cannot be as negative as the majority of economic forecasters are currently predicting.

The Reserve Bank of Australia has stated that they will not be cutting their OCR interest rate until they see the unemployment rate increasing.

That looks unlikely given the sharp improvement in the mining and resources sector. Against this backdrop, I would still contend that the AUD is oversold against the USD at 0.7050. The hedge fund currency speculators remain heavily “short-sold” AUD’s in their positioning and when it fails to depreciate below 0.7000 many will be hurriedly buying the AUD back.

Parity-party prediction likely to fail yet again

Some local NZ bank economists are starting to comment on the possibility of “parity-parties” for the NZ and Aussie currencies as the NZD/AUD cross-rate moves higher to 0.9650.

The historical pattern has been that the NZD/AUD rate heads in the opposite direction back to the low 0.9000’s as soon as the economists start predicting parity parties.

There is nothing on the horizon that would suggest the NZ dollar will be sold off on its own account to drive the NZD/AUD cross-rate back to 0.9300 from 0.9650.

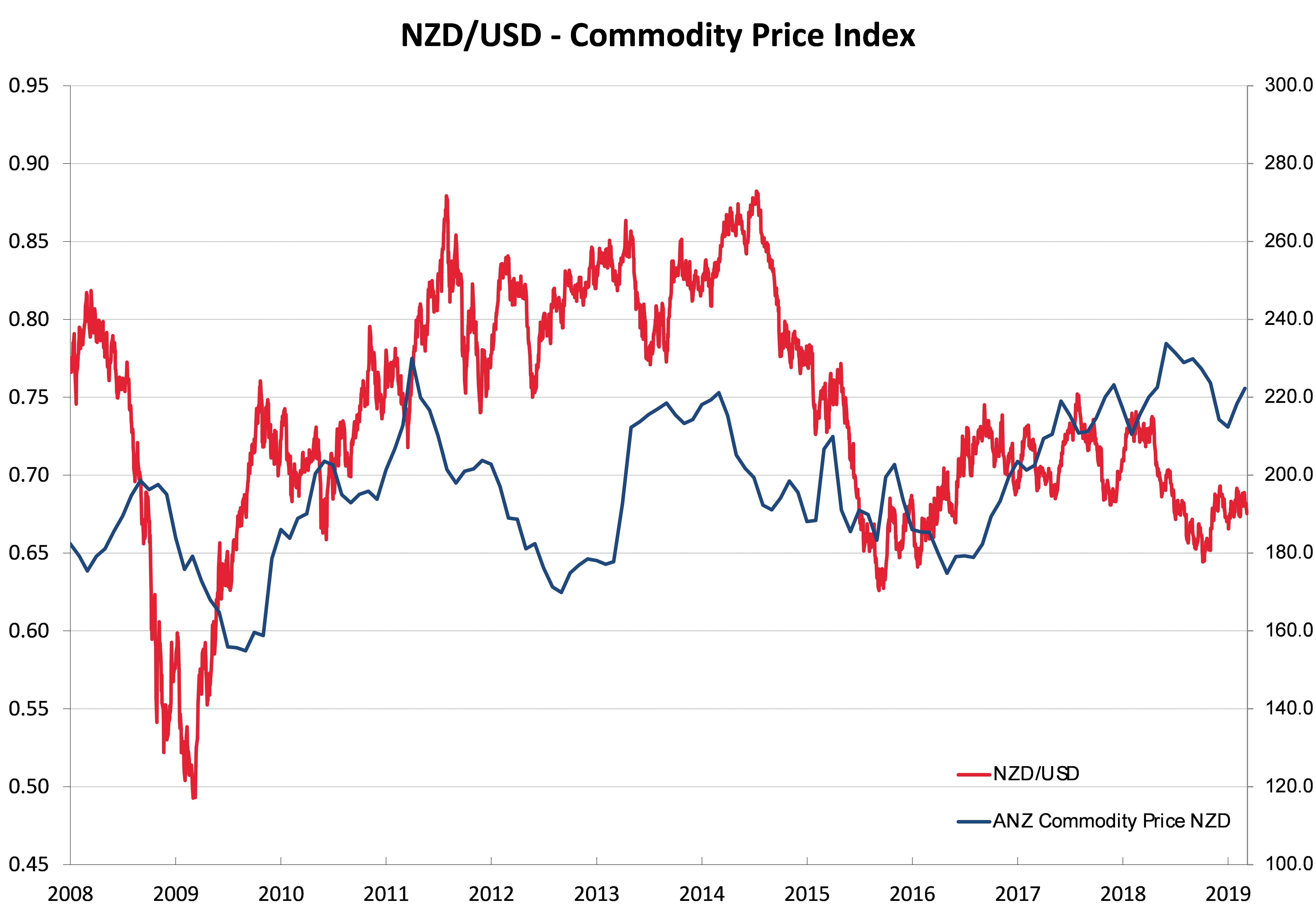

Therefore, it will need to be a substantial turnaround in the fortunes of the AUD against the USD (and the Kiwi not following to the same extent) to pull the NZD/AUD cross-rate lower. The current massive divergence of the AUD/USD exchange rate away from Australian export commodity prices cannot be sustainable going forward, therefore a significant AUD recovery has to be on the cards over coming months.

NZ share market and currency defy pessimistic economic forecasts

If the outlook for the NZ economy in 2019 and 2020 is as negative as the majority of local economic forecasters are currently predicting, the NZ share market and exchange rate value would both be heading south at this time.

Unfortunately for the gloom-merchants, the opposite is happening with the share market hitting new record highs and the NZ dollar up four to five cents from the lows of last October. Recent economic data, such as retail sales are on the improve and our major industries of construction, tourism and agricultural exports are all experiencing buoyant trading conditions.

The economic negativity is not justified and it seems to be based around one narrow indicator of marginal decreases in Auckland house prices (after years of spectacular increases!). Local commentators also seem to place too much store on overseas economic events creating uncertainties for the NZ economy.

Brexit and weak European economic growth in reality have little influence on our economy or currency. A recent survey of NZ company Chief Executives by a CA firm reported that more than 50% saw global economic uncertainties being negative for our own economic outlook.

The survey must have been conducted some months ago, as more recent developments such as the real possibility of US/China trade agreement, rising share markets and the Chinese enacting fiscal and monetary stimulus are all very positive for New Zealand. Add on the continuing increase in whole milk powder commodity prices and the outlook is much more positive.

It is difficult to see the NZ dollar falling away given the still positive local economic outlook, a recovering AUD and a weaker USD on the international stage.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

7 Comments

Billy T, Joan Rivers, Robin Williams, Aziz Ansari, Eddie Murphy , Billy Connolly , and Roger Kerr the Monday morning fixed income stand up act.

Since Roger has a contract to write a weekly commentary on currencies I s'pose he has to come up with something fresh and slightly contentious every week. Since he's been doing it since 1981 I'd love to see a graph of predictions vs outcomes over all those years. Nothing like some hard and fast numbers to bolster the claims. I reckon any economist worth his salt would be all over that like seagulls on a tip!

However, there has been a paradigm shift in sentiment and outlook since the start of January that dramatically improves Australian economic performance going forward in this commentator’s view.

The outlook has actually deteriorated, which I suppose is why it is "in this commentator's view" rather than providing some examples? Here are a few: credit growth and leading indicators down, business confidence down, job ads down, house prices down, construction forecasts tanking, etc, etc, etc.

Profitability (thus activity levels and investment) in the mining and resources sector has always played a dominating part in the performance of the Australian economy, and the recent higher commodity prices (iron ore and copper) combined with the weaker AUD exchange rate has substantially increased prices and profits for the mining companies.

This is a good model for Australia in the 1990's. That was 20 years ago. Three questions you need to ask yourself - (1) does higher profitability in the mining sector flow into wages. Answer: No (2) Will higher commodity prices drive further capital investment in mining. Answer: No, not at this stage in the cycle. (3) Will mining profits be retained in Australia? Answer: No, the miners are mostly foreign owned. In other words you're barking up the wrong tree, as always.

Interest.co.nz excels by having a range of diverse opinions and respectful debate of ideas - but this column seriously undermines this website's credibility. I don't want to make negative comments but the combination of willful ignorance AND bias AND lack of accountability for poor forecasting make this too much to stomach.

Australia's falling currency is justified. They have the highest household debt to GDP ratio in the world. About 30% higher than NZ's. Coming into a bubble pop, it's bad m'kay.

Do you have any "evidence" as to how how high h'hold debt negatively impacts a country's currency? The Swiss have the highest h'hold debt in the world (relative to GDP), yet CHF behaves like a safe haven currency when things are bad. If you said NZD and AUD are speculative currencies, which is driven by an interest rate differential, then you would make more sense to me.

It would appear that the rest of the world has understood the flow on effect of having all your eggs in one basket! Property prices are falling in Vancouver, Australia and are we are starting to see falls in New Zealand too. The banks, especially in Australia, are very reliant on lending to the property sector so it looks as though these warning signs are being factored into our currency too.

Oh all you naysayers. You see Roger Kerr is right and its the market that is wrong. Ha ha ha ha ha.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.