Economists at the country's largest bank are warning that rising mortgage rates could make the housing market "flip more abruptly than expected" from a support - to a drag - on household spending and construction activity.

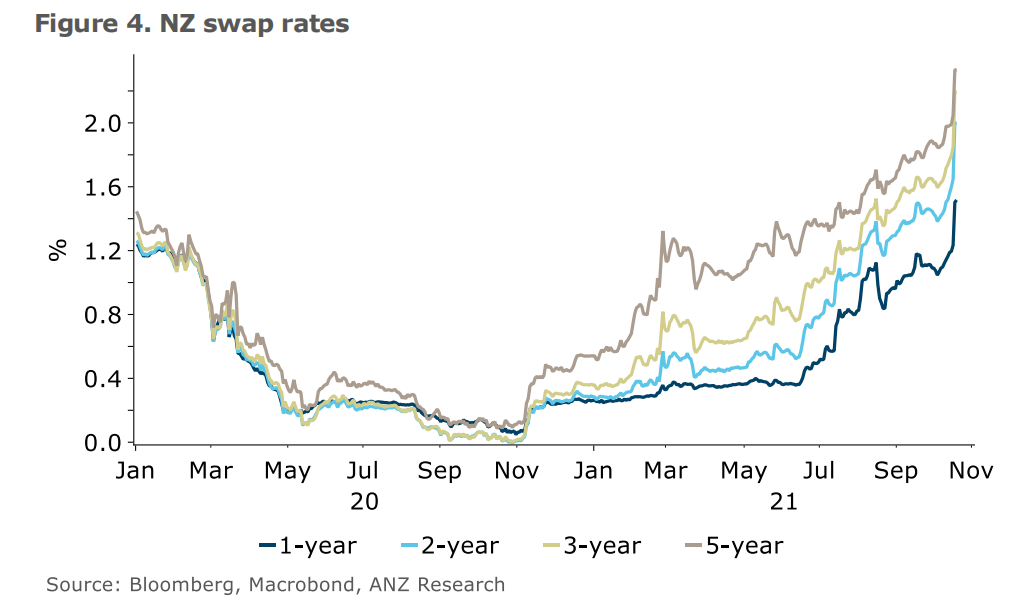

In a Forecast Update following release of the latest super hot inflation figures this week ANZ economist Finn Robinson, chief economist Sharon Zollner and senior strategist David Croy note that the "dramatic increase" in wholesale swap interest rates earlier in the week "was so large there is real pressure for mortgage rates to rise further before long".

"This increases the chance that housing market momentum could turn more sharply than forecast and flip more abruptly than expected from a support to a drag on household spending and construction activity," they say.

"And globally, a reassessment of the likely average cost of borrowing over the next few years poses a challenge to asset valuations that underpin household wealth."

They also note that the longer Covid restrictions in Auckland drag on, the greater the risk of a hit to firms’ investment and employment plans – "though so far, they’ve been remarkably robust".

"All up, it is far from a given that the wheels will stay on the bus while the RBNZ steadily increases the OCR [Official Cash Rate] for the best part of a year."

In the wake of the inflation figures, the ANZ economists have changed their OCR forecasts.

They've added in 25-basis-point hikes in the April and July Monetary Policy Reviews, "in addition to the hikes we were already forecasting at the next four MPSs [Monetary Policy Statements]".

"This new track sees the OCR reach 2% in August 2022."

But the ANZ economists are continuing with their cautionary view that something could go wrong in the meantime that will force the RBNZ to re-evaluate the interest rates picture.

"It is important to highlight that although we are raising our central OCR forecast, we still think there is a significant risk that something happens to derail the hiking cycle before its completion," the economists say.

"Indeed, these risks are intensifying, if anything."

The economists have also updated their inflation forecasts.

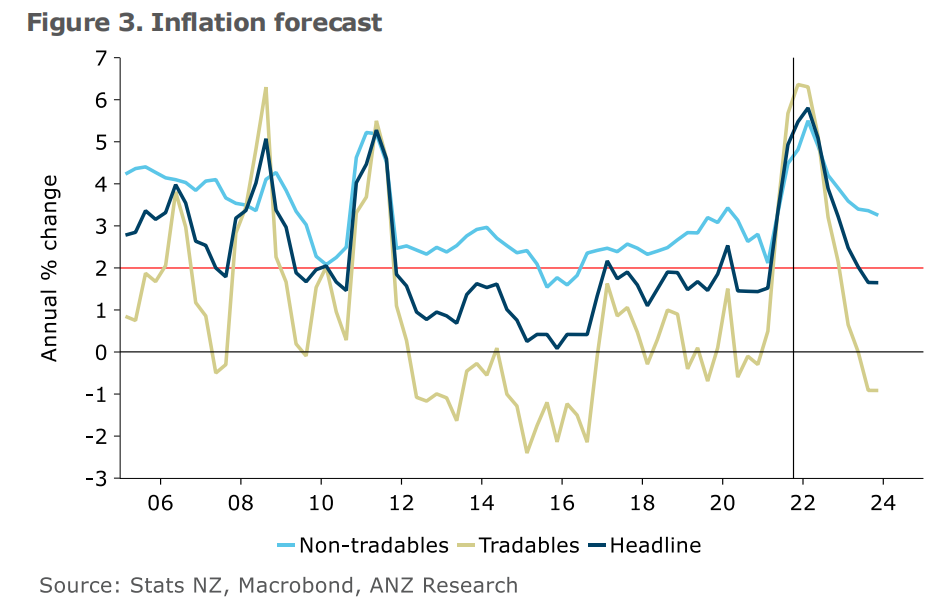

"...Inflation pressures are likely to get worse before they get better, and we now expect inflation will peak at 5.8% [year-on-year] in the March quarter of 2022."

The ANZ economists note that 'short-end' wholesale interest rates aren’t far off pricing in their new forecast, with an OCR of around 1.92% priced in by August, "by which time we expect it to have reached 2.00%".

"Given the intensity of medium-term inflation pressures, we are now forecasting the RBNZ to take every opportunity it gets over the next while to raise the OCR.

"In short, the very strong inflation pulse has taken away the luxury of time and caution, as the OCR has more work to do.

"...We estimate the OCR needs to go to around half a percent above neutral, which we estimate to be around 1.5% currently. The RBNZ estimates neutral to be 2%, so we expect the November MPS will show the OCR rising steadily to around 2.5% or a little higher."

The economists note that supply chain disruptions have been a key driver of prices over the past year, and as the Christmas rush builds, these pressures are likely to get worse over the next few months.

"More concerning for the Reserve Bank is the steep rise in measures of core inflation. It’s still highly uncertain how high and when exactly inflation will peak – but it’s very clear that more needs to be done to get ahead of the inflation curve.

"...We continue to expect that inflation pressures will moderate in time. Supply chains should eventually adjust to the post-COVID norm, and in fact we’re forecasting tradable inflation to dip into negative territory as price levels normalise. As the RBNZ removes monetary stimulus from the economy, domestic inflation pressures should also ease."

112 Comments

"It is important to highlight that although we are raising our central OCR forecast, we still think there is a significant risk that something happens to derail the hiking cycle before its completion," the economists say.

"Indeed, these risks are intensifying, if anything."

What's this 'something' they talk of... perhaps a new strain of covid in which Orr will take OCR negative, remove LVRs and QE printing of billions?

The challenge with most mainstream economist is they don't understand the kiwi psychology when it comes to the NZ housing market.

If there's anything that most kiwis love more than their children, it's real estate. They'll scrip and save money and avoid buying their children toys and new clothes so that they can install a new deck or swimming pool to generate more uplift in their real estate portfolio holdings.

It's the behavioural dynamics and psychology that underpins the confidence in the housing sector rather what's happening in the world. Most kiwis are too insular and lack understanding of global macroeconomics so they have no idea what's happening outside the island country except for COVID-19 is out there.

"If there's anything that most kiwis love more than their children, it's real estate."

Correct but who has to be blamed for it. Politicians and bureaucrats time and again have not only in words but also by their action fuel greed.

Did RBNZ and PM have not by their words and action not created a sense of false security and confidence that whatever happens, will be saved.

Aren't the politicians a reflection of 'Us'? Rather than the other way round.

Aren't the politicians a reflection of 'Us'?

Yes. They are a caricature of their constituents' emotional needs. They tap into the emotional touchpoints of the general public to garner popularity.

Yes there is now an inter-generational addiction to the housing legend of large tax free capital gain, sadly based on reality.

Its going to hurt very much when people realise that property prices can't double every 7 years.

I wouldn't put it past the RBNZ to allow the value of their shitcoin to halve. They have no credibility left.

Actually for most of us the so called addiction is just to own ones own home - cap gains are the addiction of the leaches in society i.e landlords and flippers.

Flippers buy the houses you wouldnt touch with a barge pole and get your hands dirty.

They clean up all the shit left behind by the great unwashed, and present you with a near new house to lord over.

That is extraordinarily untrue, in Auckland at least.

Flippers use the collateral they have in existing properties to outbid the FHBs who would happily buy run-down properties and fix them themselves. You confuse 'unwilling to work' with 'unable to purchase'.

All peak inflation forecasts seem to be progressively being moved upwards and outwards. International bank economists are taking about supply chain pressure meaningfully easing in 2023 now (which makes sense, it takes a few years to build new ships) and energy longer than that.

I'd take all these forecasts with a big pinch of salt, like trying to forecast peak house prices has been over the last decade it's anyones hill to die on. The Reserve Banks forecasting is poor, they have to to manage the inflation situation as it presents itself and at the moment that looks like it'll take at least a quarter of back-to-back 25bps raises to even hold inflation.

Does inflation number has any meaning today. Even if it shoots to 10% RBNZ will be able to defend with valid arguments as are experts in manipulation to suit their narrative. Best example is "Temporary Inflation" started by Fed and picked by rbnz, not realising that US with the diversity and size of its economy may manipulate but not NZ - may be for short term but not long.

Does anyone know what is the defination of Temporary, is it one quarter, two quarter or........

Which other industry is in NZ besides housing ( instead of diversifying even RBNZ and politicians only concentrating in housing market as a result has turned it into gambling / speculative chip, which is and should be actually a basic necessity).

Another point to remember that 5% is by excluding what does not suit reserve bank for calculation otherwise in reality for average person ( spending since last year) has gone up by 15% to 20% and this is as are not spending as much as they use to on travelling and restaurants because of various level of lockdown.

......have to come to roost.....not IF but WHEN

Which other industry is in NZ besides housing

That's what happens in asset bubbles. It becomes the be all and end all.

What happens to our extremely high house prices with stagnant incomes and mortgage rates hitting 4% or 5% or 6% or more...?

Was bidding up prices as if 2% rates were going to last forever a wise thing to do?

Orr has been expressing concern that prices are "well above sustainable levels" for quite some time now. He has done the math.

We have yet to hear a definition of "sustainable" from Orr & Grant & Jacinda...

The housing crisis has also been "unsustainable" for more than a decade now. There's an entire generation growing up with the dream of home ownership taken from them. Well, unless mum and dad are well off.

Applicants are stressed tested for 6% so unless they have falsified their expenses not a lot

New borrowers do their best to look good for the stress test - before borrowing, not after. Lifestyle expands, monthly costs increase, a new car loan... Of course most would sell their car before their house, but the effects can be still quite significant. A single percentage point increase could be a 20-30-50% decrease in disposable income.

I might be imagining things, but I recall reading somewhere that in the GFC more Americans (%-wise) would rather give up their home than their car, primarily because a car is needed to get to work.

No because they figure they can live in the car ? Besides, just selling the car will not help you anyway when things really go south when 95% of what you own or owe is in the house.

If we're in an environment with higher interest rates, it's because inflation has forced the RB to raise.

In that environment, household costs have risen as well as the size of the necessary repayments. I wonder if the bank stress tests take that into account?

Yes that has been my question in the past also. Property bulls are always saying 'buyers are stress tested at a much higher interest rate than the current market rate so no problem - banking system can never get in trouble...therefore status quo forever'.

But if people have been stress tested at 7%, does that assume that inflation and the cost of goods and services has also gone up by that amount, meaning there is less left over in peoples take home pay to service a mortgage? Or do we assume that wages are also going up by that amount (which to me sounds like very wishful thinking!)

Any bankers out there no the answer?

Income is assessed as not increasing over the life of the loan.

Yeah but don’t forget if you need to sell the next buyer might be stress tested at 9-10%

I take that stress test with a grain of salt.

Speaking of my own situation, my household could potentially cope with 6%, but it would be extremely tight, and involve some pretty drastic cut backs and contingencies.

I think 5% is a much more realistic stress test.

I specifically asked, what happens to house prices.

New applications are going to be stress tested at 8%, 9%, 10%. Given that house prices are a function of credit availability. What happens when that credit availability is shrunk?

Good question, although it will be 7 or 8% max.

But still a big difference from 6%.

*if* they do genuinely stress test that it's going to kill the market.

You already know the answer, house prices fall.

I get that banks claim they stress test - but I dont believe them

They do, it's the quality of the stress testing which is the problem. Stress testing is only as good as the assumptions used for the scenarios and the actual modelling. Probably all spreadsheets with hard coded numbers but all regulated banks would be stressing liquidity and capital/solvency requirements.

Better to ask what happens to rents when mortgage rates rise to 5% and none of it is tax deductible.

Post redundancy income may be insufficient to pay the mortgage/bills & food.

Most people will pay down their mortgage over time mitigating the risk from interest rate rises and the test rate is much higher than any rate we'll reach any time soon so they shouldn't be under pressure. The other thing is that people can always downsize their house to reduce or repay their remaining mortgage amount.

The people who might be in trouble are those who where reliant on housing, or other assets devalued by rising interest rates, for their pension. That said you always run that risk if you don't diversify.

They can downsize as long as the bubble doesn't burst. It's those sort of situations where people lose their footing in the property ladder. Some will downsize, some will go back to renting and who knows what happens to prices while they are out of the market.

"Should flip more abruptly"....fixed it for you. In a bubble model this is known as the "bull trap". It catches all the greedy and late to the party specuvestors. The immediate future includes "fear, capitulation and then despair" as there is a return to the long term mean.

{kind=link}

The problem with the bubble model is that it ignores all the creative ways a bubble can be propped up. Reserve banksters are no longer afraid to do the unthinkable (like printing a third of all the USD that's ever existed in a single year), since the past has proven that there are no negative consequences (for them).

The housing market seems to work on the principle that people will always borrow to the absolute maximum and perhaps a little bit more. Have interest rates gone up in the past and what impact did it have?

I also wonder how much home buyers should be protected from the folly of borrowing to the max on historically low interest rates. Obviously they need a bit of protection but the heat should be turned up a little at least to suppress excessive house price inflation.

"I also wonder how much home buyers should be protected from the folly of borrowing to the max on historically low interest rates."

Zachary Smith...now rbnz and government are not protecting home buyers but themselves as it is their reputation which is at stake (have been warned but ignored and pursued their support to promote ponzi).

When home buyers take a mortage, they are not worried about defaulting as RBNZ and Government is more worried and home buyers knows that whatever happens Aunty Jacinda and Uncle Orr will be always stand to cover and protect them, come what may.

Can anyone counter this argument that RBNZ and Government are now protecting their ass than anyone else. Also as they are guilty in prompting people to borrow in extreme by creating greed and when head of the country - Jacinda Arden give personal assurance than who is to be blamed.

Who would've thought in a year's time OCR hikes to 2.5% while back then everyone was talking about OCR going negative? If OCR can go down, it can go up. This is the nature of monetary policy. So please don't say something like OCR can only go down this kind of silly statement. You could seriously mislead people and that can cause them lose everything.

Yeah there is some bad advice on here with people talking up what they want to happen rather than what is actually happening. I believe historic long term average interest rates are around the 6% mark and people should prepare for that in 12 months time.

Average OCR or a certain point on the yield curve is 6%?

The long term trend is down so it would take some selective date cutoffs for Carlos67's claim of "historic long term average interest rates are around the 6%" to be valid.

Economists say...

You lost me at "Economists"

Think 2020 and what they said.

Even the market-maker-by-definition, Jerome Powell sold a million dollars worth of shares at the bottom in 2020. Perhaps it's time to admit that economists (just like every other person) can't predict market movements. Someone eats a bat soup in China and suddenly the world is on fire. Elon Musk posts a picture of a dog and boom, 10 billion dollars are pumped into a meme crypto. I don't see how anyone could possibly predict the effects of events like these.

The only thing I have noticed is that predicting calamity rarely pays off. Even when calamity seemed obvious at the outset of the virus crisis it turned out to be a spectacular windfall for property owners. Anyone who betted on calamity lost big time and has tended to almost always lose historically.

"The only thing I have noticed is that predicting calamity rarely pays off"

Having no consideration to the calamity can also be seriously destructive when it does occur, and it does, there are plenty of examples 'historically'.

What I am really saying is that it is rare to profit from calamity. I'm thinking of all those people who commented that they are waiting to swoop in and pick up bargains in mortgagee sales. Or those that cashed up hoping they had dodged a bullet. I've never really seen it work out well.

There is a movie about this: “The big short”. Also look up the man who broke the Bank of England: George Soros. Those are just the classic examples, there are tens of thousands of others who fly under the radar because they aren’t as high profile.

Yeah its so rare they make movies about it. Tens of thousands of others yet millions who profited by betting on things being good. I feel it's risky to bet on calamity like cashing up and waiting for a drop in prices. Not saying it wouldn't work, it's just really risky.

Maybe the bargains are still to come? Perhaps it depends on the timeline. Maybe there will be a crash and bargains to be had? I've never been a position to be in any market, but I remember in 2009 there were plenty of bargains to be had in different markets (eg classic cars, holiday homes being sold off etc).

Every property bought in the 1960's looks like a bargain now. Every one.

Every property bought in the 1970's looks like a bargain now. Every one.

Every property bought............(you know where this is going)

If you took the money you bought a property with in the 1960s and had invested it in the stockmarket the returns would be vastly greater.

Every property bought in the 1960's looks like an opportunity cost.

Every property bought in the 1970's looks like an opportunity cost.

(you know where this is going...)

Its correct in principle if you get the timing right, the right timing seems quite near - many recessions have started in Oct/Nov.

Well lets be honest here the Pandemic was a doozy. I predicted a 25% property price crash that was pretty logical on the face of it but what I did not factor in was crashing interest rates and basically free money being thrown about like it was a giant billion dollar lolly scramble for the already rich. It was a case of adapt fast or die in the new reality.

That Big Short dude done ok

I think that just highlights how irrational (and desperate) the masses have become.

... 48 % still think Jacinda is our best choice for PM .... OMG ! ... you gotta larf at the gullibility & irrationality of the " masses " ...

So who else? Seymour is an affable clown, but I couldn't vote for his policies.

or his party. I mean he clearly doesn't trust anyone but Brooke to do anything on a public level. What really is the point of ACT outside of being a business-centric voice of 'reason'. They can't govern in any way unless you want National in power... and frankly that's a terrifying option at present.

Good observation.. I think perhaps economists overthink things. By nature they are highly qualified academically, but often neglect to appreciate the base level mob mentality. Perhaps they should employ a few more average folk in the economics department to get insight into how joe or jane doe will respond to economic factors - rather than make assumptions based on the purely theoretical economic / rational man.

No- really - who would have thought.

After all the IMF and ratings agencies have been saying all year that if Interest rates rise - the NZ housing market will be in a world of trouble.

Welcome to a world where FOMO is replaced by FOPTM- the question is how big will the bubble burst by.

They won't go above 1.5% maximum, see below.

And add to those reasons the fact they WILL NOT let the housing bubble burst, which it almost certainly would if the OCR was 2%.

That's not a fact its a fragile assumption.

You know what they say about assumptions being the mother of.

Yes the housing market can easily take a 2% OCR mid next year. I will say this is subject to house prices not crashing due to some other event before then. By mid next year the current house prices will be baked in and many people will have fixed their mortgage. I could see fixed rates being 5 to 6% easily by the the middle of next year. Only a very small number of home owners couldn't handle this but go beyond 6% and those that cannot handle it will rise exponentially. Something like 8% now would be pretty fatal for many recent buyers.

It's not about those holding on to house though.

It's about those transacting. If buyers can't borrow as much due to much servicing costs, prices may not be baked in at all.

Would you or Brock like a 1k wager with me on whether the OCR will be higher than 1.5% next year?

How about 0.001 bitcoin?

I was using 'fact' in a colloquial way.

What do you think the OCR will be this time next year?

'" was using 'fact' in a colloquial way" Haha too funny, like you said "what a knob"

Well you are knob. And a not very clever one at that.

Grow up

What in the RBNZ'S behaviour over the past few years makes you think they WILL allow the housing market to crash?

They won't. Because they are a political beast, the 'independence' is a facade and remember they have financial stability and employment imperatives.

There's an awful lot of cognitive dissonance at play in your thinking.

That all comes down to how you define "crash".

They WILL let house prices drop, significantly, if faced with a choice between that or a wage/price spiral. Out of control inflation causes financial instability and unemployment.

They have gone on record several times and said asset prices are not within the remit of monetary policy.

The market is bigger than any RB and you just cannot beat numbers. If the number of sellers forced or voluntary exceeds by a margin the buyers and Banks are still lending prices fall, if not water starts flowing uphill.

Economists are becoming increasingly valueless.

... that assumes they had some value to start with ... debatable !

haha

Maybe 30 years ago they were 'right' more often, because the world was a less complex, interconnected and volatile place.

But clearly economists are flailing and failing in the context of this modern world, to the point there they are effectively worthless.

..they are only ever right because there are so many with some many different opinions - by chance one of them will look brilliant in hindsight.

ANZ are the only bank not to have lifted their fixed rates in the last week - they will lift this week and I wouldnt be surprised if their 12 month rate has a 3 in front of it instead of a 2

Zero credibility

Economists get confused when they are asked 'out of syllabus' questions by life!

Something ref is to Chinese deflation coming here from their housing crash

interesting...

"And globally, a reassessment of the likely average cost of borrowing over the next few years poses a challenge to asset valuations that underpin household wealth."

Leverage goes both ways. Some may come to learn that the hard way.

"...Inflation pressures are likely to get worse before they get better, and we now expect inflation will peak at 5.8% [year-on-year] in the March quarter of 2022."

So we can expect it to go over 6% based on previous predictions.

There's time for the overleveraged to exit the market gracefully, with handsome profits, because there is still strong organic demand from FHBs.

Those at risk are the developers, whose costs are huge right now, and who might be selling into quite a different market a year from now when their projects are finished, if rates are forced to keep rising.

Exactly.

I've said many times over the past few months that it's highly likely that the residential development sector will crash next year.

If I was in an area of employment heavily exposed to that sector I would be looking at employment contingencies NOW.

They are talking through their backsides, as usual.

The OCR will be raised two or three times in quick succession - then we'll start to see the economy slow, in particular construction. Because the OCR has gone so low, the economy will be super sensitive to increases.

That will result in a halt in OCR raises, and potentially it might drop down again as things really weaken.

I think the OCR will peak at 1.25, or maybe 1.5 at a stretch.

So let's do a little exercise.

James and Katie are FHBs, and have a gross household income of 150K. They bought a new 2 bedroom townhouse in Avondale in July 2021 for $800K. With a 100K deposit, they have a 30 year mortgage of 700K. With a low deposit, they have a mortgage rate of 3.5%. They pay $725 per week on their mortgage. With body corporate, rates and insurances, their total outgoings on housing are $810 per week, which represents around 40% of their net income.

Shoot forward to March 2022. Their friends Mark and Jacqui, earn the same income. They are interested in a 2 bedroom townhouse in the same location, with rising build costs etc the townhouse is selling for 850K. Like James and Katie, they have a 100K deposit. The OCR has since risen to 1.25%, with their low deposit they would need to pay a mortgage rate of 4.25% on a loan of 750K. They would need to pay $850 pw on their mortgage, with all other costs their total outgoings on housing are $930 pw, or 46% of their net income!!!!

So...see where this is going?

If the OCR goes to higher than 1.5%, it is going to totally nuke the construction sector, much of the strength of which in recent years has been gained from FHB's buying new build townhouses.

Once the OCR goes to 1.25%, we will see the economy and inflationary forces start to weaken, which will limit further rises, especially given the RBNZ's employment mandate.

Good example.

I agree with your last sentence, except: there's a possibility - just a possibility - that inflation continues to rise globally even as the economy is weakening here. We can have demand destruction internally and imported inflation pressure at the same time. If it's bad enough, it can force the RB to raise rates more, even knowing that it will have a recessionary effect.

good point.

But won't they 'look through' those global pressures, especially if raising the OCR has little if any impact on them?

I think the employment mandate is significant. If you nuke the residential construction sector, then that's potentially a lot of job destruction - builders, tradies, designers, engineers, surveyors, RE agents etc etc.

Yeah but you are also reversing the unsustainable price rises over the past year and a bit which they are also mandated to keep an eye on. That's part of the problem with giving them too many targets...

Yeah exactly. They are going to be between a rock and hard place.

All self inflicted, of course, by cutting the OCR too far.

But the GDP and employment impacts will win out, right? We know how they operate by now.

It doesn't matter what we *think* they should do...

What do they do if 'looking through' means the NZD goes lower and those global pressures get worse

yep.

no easy answers from here on in, and again they have snookered themselves.

Whatever happens there's pain ahead.

Why can't they continue to go mad with QE? Provide banks with an extended FLP to keep rates low? None of this mattered months ago. They haven't cared about the wealth divide, why would they care now?

Not really. At one point on a single income I was paying 70% of my take home pay on the mortgage so what ? You adapt and you cut back if you have the personality and skill to do that. Most people simply cannot pull their heads in because of the things in life they think are "Must haves" and they cannot live without them.

Much easier if single.

Also try getting a mortgage from the bank if your housing outgoings are more than 50% (unless you are a very high income earner)

I did the same when I bought my first place 13 odd years ago.

Now with a kid and one on the way I don't have those kind of options. Although the mortgage is a non event these days.

Most of my friends have only just got into the housing market. They are older now and have relationships / kids.

Cut back p/w for many (dollar value differ from individuals)

Drinks/alcohol/coffee $80

Dinner out/brunch $80

Subscription/membership of any kind $50

Cut road trips to save gas $80

luxury items $30

Lunch for work (home made instead) $50

takeaways $40

Less junk food from supermarket or craps from Kmart $20

easily extra $400+ per week and the list goes on.

Let’s say that’s two bedroom house went down 20% to 640 k and mark and Jacqui had 100 k deposit the OCR was 2.5% and they got low interest rate at 5.5% this would cost them $705 a week a lot more affordable. I think this is more like what is going to happen, unfortunately jame and Katie will be in negative equity for a few years.

Will RBNZ come out with a much bigger OCR rise in response to the 5% inflation figure being way above their mandate? They might just do a whole 1-2% jump in the next update and be fully justified to do so, based on inflation. That would certainly put the cat amongst the pigeons.

I don't think they will, but am throwing out that it is possible given their main goal is controlling inflation. And at the moment it's looking like it's running away and not so temporary...

Mr Orr : Temporary = Decade or Two

Mr Orr 🤣

NO chance. Although a 50 BP increase might be possible.

Interest deductibility will remain in place for investors in new builds. They will be the only buyers if fixed interest rates ever start with a 4 or higher again. It will be cheaper to rent. FHB's will not be able to compete. You will own nothing but be happier. All those newly minted PR visa holders currently being exploited in the regions on work permits will drift to Auckland to increase housing rental demand. Underwritten by the accommodation supplement. To be replaced by new work visa holders in the regions. That supercity debt bomb wont defuse itself.

Well.. it's really a master/sub relationship. It's known this debt-based-monetary-system is a scam.

The master's whips and chains are manifest in money-printing and banks [like those on a river] directing the liquidity into housing/assets-bubbles.

The subs LOVE it !!.. until they wake up one day from their hyper-sexualization, I mean hyper-financialization and find their lifetime spent in fin-roticism has dried out their conscience, impoverished their society..

..they are FULLY dependent on their master now, I mean the debt-based-monetary-system.. they are reduced to begging for scraps and accepting unwelcomed abuse.

Now make sure you wear your mask while out-n-about lol.

This article or prediction is what should happen but WHAT WILL HAPPEN is a question mark.

Knowing Mr Orr's approach can confirm in advance that may not increase and if under tremendously pressure to increase will increase by 0.25%.

It does not matter if you can personally afford a higher interest rate or not - it only matters what the next purchaser can afford. If due to higher interest rates they can no longer afford $1m but now can only pay $900k - that is what the market will align to.. the market never stalls completely - and while some will say “if the market goes quiet I’ll just sit tight” that is simplistic.. others have divorces, down sizing, relocations, inheritances etc - and the price they sell for sets new market values across the board.

Once those new values take hold - SMEs cannot borrow more to invest and construction activity slows… as the cost to value relationship has suffered.. the trades lay off staff and hence more people need to sell which leads to a self reinforcing loop. This continues until a price floor is reached based on the then current affordability overlaid with the level of fear / confidence in the future for the public’s personal economic outlook and house prices…

The housing market is a big beast with lots of inertia and it cannot change direction quickly… it’s like a container ship.. any pundit who thinks the market can be contained within a 1-3% price inflation band lacks an understanding of land economics and human nature..

Time will tell - and gravity cannot be defied forever :)

Cost of borrowing may impact asset values negatively overseas but not for housing in this country.

On the other hand, rising costs may actually help in building up a powerful momentum.

?? that’s pretty much the opposite of what happens..

We're Diffrunt

Look the other way when everyone else is looking this way. ?

I think the last 24 months have shown that "economists" don't know their ar$e from their elbow when it comes to predicting NZ house prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.