By Bernard Hickey

This week's Parliamentary bunfight over whether the big four banks should have passed on all of the surprise cut in the Official Cash Rate has again thrown a spotlight on just how competitive (or not) our banking system is.

The banks argue they fight tooth and nail for market share and don't cooperate to generate super-profits, and at certain points over the last decade that has been true.

That was certainly the expectation (or at least the hope) of Bill English when he was confronted by Labour's accusation in Parliament that the Government was going soft on the banks and its suggestion the banks should be regulated.

"What the banks will listen to is customers shopping around," English said. "That will have a great deal more influence on their behaviour than politicians making statements they cannot follow through on," he said.

That was certainly the case from 2002 until 2010 when Kiwibank was on the warpath, pushing for market share with discounted mortgage rates and an aggressive approach to lending growth. Kiwibank challenged the big four with the support of its Labour Government shareholder and happily went for growth with pricing that was better than Australian-owned rivals. That sort of growth required the Government, through New Zealand Post, to stump up fresh capital and forgo dividends.

It worked to squeeze the net interest margins for retail banks down by 74 basis points to a low of 1.98% between Kiwibank's launch in 2002 and the March quarter of 2009. Collectively, that cost the big four Australian-owned banks hundreds of millions in lost profits over those seven years. That money was effectively transferred into lower interest rates for borrowers.

But those heady days of taking on the big four with big hairy discounts are long gone. New Zealand Post's deteriorating financial position and the Government's own reluctance to stump up more capital has seen Kiwibank pull its head in and focus on becoming just as much of a profit and dividend machine as its rivals. Last year it paid NZ$46 million in dividends and is set produce a profit this year of over NZ$127 million.

Since Kiwibank backed off, the banks have rediscovered ways to nudge their net interest margins back up to around 2.2%. Deposit rates have been cut more than mortgage rates and this week's collective move to pass on just 10 to 20 basis points of the Reserve Bank's rate drove the point home.

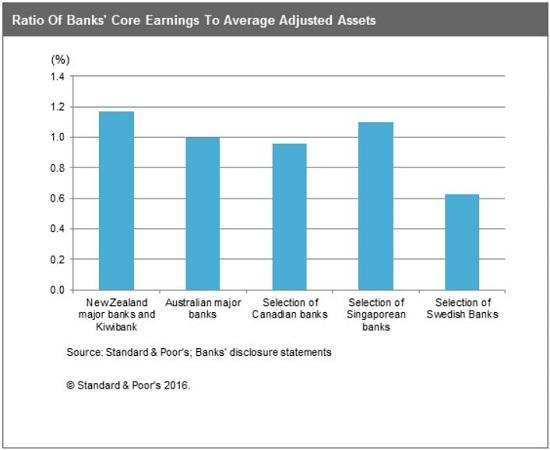

But don't take my word for it. Ratings agency Standard and Poor's, which is paid by the banks to dig into the banks' accounts to assess their profitability and safety, said last month the big four banks could easily cope with the dairy downturn and an Auckland housing slump because they were so profitable.

"Given the oligopolistic nature of the system and absence of overcapacity, we do not foresee that banks would be taking on undue risks, even though some margin pressures may be looming on the horizon," S&P said.

It also published a helpful chart showing the New Zealand banks' net interest margins and profitability ratios were higher than those in Australia, Canada, Singapore and Sweden.

Those looming margin pressures referred to by S&P were dealt with rather deftly over the last week as first ANZ, then Westpac and BNZ, all decided to pass on just 10 basis points of cuts to their floating mortgage customers. They justified their move by pointing to increased funding costs on their foreign borrowings because of global financial turmoil. Only ASB bucked the trend, although it still chose to pass on just 20 basis points of the 25 basis point cut.

The Reserve Bank itself said last Thursday that these extra funding cost pressures were only mild and that it expected the cut to be passed on in full. The big four simply ignored the central bank and took actions to protect their margins.

The other factor that was no doubt looming in the big banks' mirrors was significant losses coming from their loans to dairy farmers. The Reserve Bank said this week that stress tests done by the banks showed they could have to book dairy loan losses of up to NZ$4 billion over the next four years in the worst case scenario. In effect, the banks decided to stock up with some extra profits from their home mortgage loans to offset the coming losses from the dairy loans.

The end result is that the Reserve Bank's surprise rate cut wasn't as potent as it hoped and the Government's hopes for some quick relief for dairy farmers were frustrated. Even less of the official cut was passed on to farmers. Governor Graeme Wheeler may well have to cut his official rate more than he originally expected to get the economy humming enough to generate the inflation he wants. The rate cut did, however, give him some of the exchange rate relief he wanted, and even bigger cuts would do even more. That's great news for exporters.

The ultimate irony of this whole proof of the oligopoly theory is that the banks have actually helped the Reserve Bank avoid one of its feared side-effects of the rate cut -- yet more fuel on the Auckland (and regional) property price fires. Both fixed and floating mortgage rates have yet to fall much after the official rate cut.

The Reserve Bank is expected to cut once or twice more this year, so some of that will be passed on. But the banks' increased focus on protecting their margins and profits will reduce the octane levels of that fuel, and help reassure savers of their safety in the event of more severe downturn. It will also mean exporters may see more of the exchange rate depreciation they need if the Reserve Bank is forced to cut even deeper than it originally planned.

A very competitive banking sector is ultimately good for consumers, but in the short term a well-functioning oligopoly can help the Reserve Bank and the Government achieve its aims.

A version of this article was also published in the Herald on Sunday. It is here with permission.

63 Comments

Most mortgage borrowers are looking down the track for a sharper 1 or 2 year rate atm.

When come off their current 1 or 2 year term. Floating has been a very high rate for some time.

3.99 should be the norm soon.

The Reserve Bank is expected to cut once or twice more this year, so some of that will be passed on. But the banks' increased focus on protecting their margins and profits will reduce the octane levels of that fuel, and help reassure savers of their safety in the event of more severe downturn.

..reassure savers of their safety - c'mon get real - under risk compensated depositors standing as OBR underwriters of a thinly capitalised domestic banking system are at most risk as ANZ and APRA duly note.

Economists at the country's biggest bank ANZ are expressing concern at the blow-out of household debt levels, which has seen household debt-to-disposable income rising to a record high of over 167% Read more

Australia’s house prices, particularly in Sydney and Melbourne, and high household debt levels have become a headache for regulators. Mortgages account for about two-thirds of the loan books of the nation’s largest banks, forcing the regulator to increase supervision and introduce in new rules to protect the financial system from a housing downturn. Read more

These Australian banks cannot help themselves to safety never mind the funding depositors whose wallets they have their hands in to further reward shareholders.

In Australia, analysis by the Reserve Bank of Australia shows (p26) return on equity of the big four banks averaged about 15% by the end of 2015, beating Canada's banks on about 14% and well ahead of US and European banks, which all had ROE below 10%. The New Zealand components of these banks supply even higher ROE returns than their Australian parents. Read more

With Australia's total debt to GDP ratio third only to Japan and the EU, it would seem a ratings downgrade is on the cards.

As of December, mortgage debt over property issued by Australian banks and other authorised institutions has grown to just shy of an eye-watering $1.4 trillion.

In 2008, when APRA first began compiling the statistics, it stood at just $638 billion. In the intervening years, not only has the number of mortgages ballooned, but the average size has grown as the property market has kicked into overdrive.

http://www.abc.net.au/news/2016-02-29/verrender-housing-bubble-is-build…

Hmmm. So how to make sure the creditors get paid? Mass repossession of houses from bankrupt mortgagees and theft of depositors money? Possible, but that is precisely what gives the banks collective power over the government bureaucracy.

More likely is continuing to devalue the currency the debt is denominated in. So watch out for a final purging currency collapse in Aussie and NZ. The NZD went from 88 US cents to 62 US cents in the first fall, so maybe it goes down the same again to 36 US cents. These adjustments tend to be swift and brutal when they eventually happen.

Australasia has a fierce competitor in the form of the United States when it comes redeeming debt with a junked currency.

Federal borrowings expanded at an 18.5% rate, the strongest Washington Credit boom since Q2 2010. Crowding out the rest or just a deficit financing binge preceding an election.

I'm not convinced by the argument that the USD is being junked by their government. The US has it's problems due to it's total inability to reform in a timely or sensible way. The USD, however, is the currency in which most global debt originates, which makes it a most precious commodity.

The key regulatory flaw exploited by the bankers' games is to allow lending in a form the borrower cannot produce themselves. Lending gold to a gold miner so he can expand his mine is quite different to lending gold to a sheep farmer, unless of course the debt can be repaid in sheep.

I'm not convinced by the argument that the USD is being junked by their government. The US has it's problems due to it's total inability to reform in a timely or sensible way. The USD, however, is the currency in which most global debt originates, which makes it a most precious commodity.

{kind=link}

I agree with you that no one wants to see property repossessions and neither do the banks as they generally make a loss on them. But to be honest the NZD really needs to drop in value if we're to help our exports, tourism and to attract quality migrants. Otherwise we'll just keep the debit spiral going if the our dollar remains high.

Sorry Bernard. What is this service the banks offer that is so great that we have to pay them so highly for. It's been their decision for example to plunge into lending that now looks risky. And risky to our entire economy. Perhaps or perhaps not. But not a performance we should be paying any premium for.

At $90 million per week they take a profit of $20 per person per week. Or $100 per week per family say.

Given the limited family incomes in New Zealand thats a huge chunk for a poor performance.

Better that $100 was put to more productive use. For example $100 more dispoable income in the pockets of each NZ family, each week forever, would do much better than your dodgy helicopter.

if that was the outcome I would agree with you, instead the extra is going on servicing debt or even taking on a bigger debt.

as the number of owner occupiers has now fallen below 50% and the number of investor housing has overtaken them we need to come up with another way of boosting consumer spending rather than relying on the blunt tool of the OCR

Suck it up

The screechers got their Central Bank interest rate cut.

Hope they are happy now - will the screaming stop - or will they want more?

The big surprise is the RBNZ did not know beforehand it would not be passed through to the screamers

and

The Banks justified their move by pointing to increased funding costs on their foreign borrowings because of global financial turmoil

Clever, since they never disclose the cost of that foreign borrowing, nor, how much it has increased by

Spent an hour yesterday with a friend who also has money, 'invested', in the Aussie banks. No one is happy with their deposits exposed, we spent the time looking at options, found a few but the lack of income requires some dipping into capital or a change in lifestyle, both options were on the table but staying exposed to the banks was not.

Even my super conservative accountant is unhappy and looking around at options, so I'm thinking that banks taking depositors for granted, could be unwise and eventually lead to a bank run.

Eventually lead to a bank run? Hasn't it already started with people moving their money from NZD to USD?

Where are the US$ invested, not I hope in a bank

https://www.bankofamerica.com/deposits/savings/savings-accounts.go

Some years ago I tried to withdraw a large amount of cash and it is not easy. I wanted to invest some money with another Bank. After discussing all the options, which included a bank cheque by the way, every option meant some days delay before the money was cleared at the new Bank so I asked for cash. There was a fee for that! That fee represented more than the loss of the interest I would have earned over those lost days! Heaven only knows what we can do but I am eager to hear all your views

this day and age depositors are not courted by the banks and are treated as such. it is the debt seekers they fall all over when they come through the door. the bigger the debt the more they look after you

Just curious as to why you needed to do the transfer immediately and not just wait a few days for a normal transfer to take place?

I wonder how many recall the guy in Nelson who had money with Westpac and decided he was dropping them so asked for his cash ( around $200thou I think, could be wrong on that figure) anyway, he took the money down to SBS who at the time were not an actual bank, thus they had their OWN accounts with guess who? The guy really got played

"protect their margins at the expense of borrowers" would be far more accurate if it said "protect their margins at the expense of depositors"

Borrowers already have the lowest residential mortgage interest rates in 50 years and everyone (Mr Hickey, RBNZ, and most politicians) bleat about not passing on another 0.05 percent potential further lowering of their interest rates. Whereas depositors have already taken 50% and more cuts in deposit interest rates.

and how much do the Japanese and Chinese get on deposit? If depositors dont like it, move the money...

To where? Don't be shy with your extensive financial acumen.

Buy gold? No income but safe from devaluation and in event of devaluation should get good capital gain

Longish interview but worth perservering ....explains the rational. If not a physical holder can acquire through ETF like SGLN which is traded on LSE.

https://app.hedgeye.com/insights/49747-rickards-why-gold-is-going-to-10…

Buy .....'some'.... gold. Diversify as much as possible

Would you advise anyone to borrow money to buy gold? You know, like real investments...

typical PI, only knows how to take on debt, there are many things to invest in and ways to invest without borrowing .

I would never advise anyone to borrow....full stop. People with real wealth don't need too. A real investment? like....education? Nah, wouldn't borrow for that either.

Maybe you refer to property Zach? which was created by someone taking out a debt, then sold to service another debt, then bought again by someone else using more 'credit' on & on & on, all the while the initial property has hardly changed but ......what has changed? The value/ buying power of the fiat currency which was created from thin air by the banks involved in the lending cycle. THAT is the only thing that gives an impression of a good investment but Zach.......guess what? It's all an illusion. This perceived wealth is only based on the destruction of currency, a fiat currency, that has a limited lifespan. Your days are numbered mate, just a matter of time is all. Gold can never be destroyed once created. Houses are destroyed quite easily, they burn down, particularly during a riot or mass unrest, or wars, or earthquakes and other natural disasters. Even......financial disasters can bring about their destruction. But not gold. Gold is a good investment. ;-) "Good as gold" they say.

Gold is just a shiny metal mate. It's like you're living in the tenth century.

Won't that gold just weigh you down when the riots and wars come? Wouldn't it be better to invest in guns, ammo and survival equipment?

A little more than just a shiny metal Zach. No computer, cellphone would work without it, satellites and aerospace tech, used is medicine...just to name a few

Yeah but you're not using it for those things and won't be if the SHTF. It's just a dead weight that you are gambling on increasing in value. It's basically mostly just jewelry and baubles. Old Indian ladies stockpile it.

I don't need to use it for it to have value now or in the future. It's greatest value is in its limited supply. Other noble metals even more. I wonder why many of the worlds reserve banks hoard it?

A very good point, then we can shoot the trolls.

Steven, do you know why Japanese moved their money to NZ and other places some time ago?

Has that helped Japan? Be careful what you ask for

Sure, it is known as the "carry trade" in effect. Japan had the unique opportunity to move money offshore to almost anywhere else where the interest rates were higher and it was safe, this no longer applies today. On top of that there seems to be an excess of NZ savers "hiding" in banks after the Finance company disaster plus effectively too few borrowing.

On top of that there seems to be an excess of NZ savers "hiding" in banks after the Finance company disaster plus effectively too few borrowing.

How did you work that out?

Inevitably lenders and borrowers must match on the banks' balance sheets.

Take a look? Bank funding and claims.

Notably, household funding claims are around a third of bank claims - hardly excessive.

Household debts are greater than credit by a factor of ~1.5x

Yeap, funny ain't it how depositors don't even register with so-called financial experts and commentators eh.

Who needs depositors when we can just press a button now and hey presto!......A loan appears from cyberspace!

Man, it's so obvious we are on a road to utter disaster

Well effectively that is the free market in function it is after all a private thing.

How much have the credit card rates gone down ? Zero. How is that even possible. Government /commerce commission intervention required.

Most current retirees never imagined (or planned for) interest rates on Deposits as low as we are seeing now. Inflation was always the NZ bogeyman. Now we have rampany land inflation only..., if the OCR keeps falling and rates go lower it will cause great social harm to our elderly. Winston Peters only needs a few more % to be the balance of power. He is the natural party of choice for elderly people who wish to make a protest vote, anyone imagine interest rates going up before the next election? Pretty obvious what is going to happen politically around farmers and the elderly.

Secondly with rates at 2% and there is a property crash / external shock etc etc.... they have little ability to save us just like the FED... if OCR approached 0% (meaning the crash etc has arrieved...) I am pretty sure funding costs would increase in wholesale market as NZ and the big 4 got credit cuts from S&P etc because of the underlying asset deterioration.

In a logical market NZD would be 50's or lower but who says that type of situation will unfold in a logical way? who imagined -ve interest rates?

Divide and conquer - the powerful few versus the powerless many

Savers are the fodder of the system

You gotta ask - who is looking out for you

Hard choice to accept digital cash when the overpriced, over leveraged residential property is redeemed and cleared of it's debt. What will in the "money" sellers be demanding instead.

Yeah, but as we all know under the Fiat monetary system this was bound to happen. Fiat is not considered a real asset but only a means to fund real assets via borrowing more and more and.... more while making someone else (usually a entity called a "tenant" ) pay for the loan via actually going to a real job and doing work. Meanwhile, in 'parasiteville' which is growing ever larger.........

We only have rampant inflation in some areas, many see little or are even declining.

My view on the elderly is that they as the previous generation(s) were pretty much responsible for the mess we are in now, so its a bit hard to feel hugely sorry for them.

Not just the elderly though, yes WP only needs a few % and I think he will get it. But better the Green's seem to be swerving to the left so much so I for one will probably vote NZF next year.

Interest rates will not be going up ever, WP wont be able to get that. What he is aiming for however is handouts instead like 25% off private health insurance paid for by the public purse.

The OCR cant save us IMHO even at 0.25% and yes wholesale rates would be far higher, now that will be interesting to see (in a bad way I suspect) just how that works out.

" who says that type of situation will unfold in a logical way?" especially as you dont look at the fundimentals of why, ie peak oil.

" who imagined -ve interest rates?"

Some did, such as the Keynesians, add in massive debt and lack of energy and zero inflation is / was expected.

Its the old saying about you owe the bank $10,000 - you have a problem, you owe the bank $1,000,000 - the bank has a problem.

No the depositor and tax payer has a problem.

The banksters have also, since GFC days, enriched their shareholders by running down provisions for bad debts (paid out as dividends). Is that no bad thing either Bernard?

Banks bad debt to farmers quoted in article as $4 billion. That is a nice neat figure as it works out at almost exactly $1000 loss for every man,woman and child in NZ.

"The big four banks may have chosen to protect their margins at the expense of borrowers"?

Anyone remember the days when the media used to have articles about "saving" and "compounding interest"?

Ahhhh,......those were the days eh.

Now depositors are just fodder to government, banks, media, and borrowers.

They 'allegedly' don't need you guys so you know what you must do right?

Sure do

As soon as prime agricultural land is down to $5000 per hectare, that's where I'm going

To Gross' thinking, negative interest rates in Japan and Europe are what happens when this debt star enters its death throes. Investors are left with almost nowhere to turn, as bank deposits, equities, Treasuries and Bunds have returns that are "inadequate relative to historical as well as mathematically defined durational risk." Authorities are even cracking down on cash, "the one remaining escape hatch for ordinary citizens," because of its use by criminals and terrorists. (See also: Why Governments Want to Eliminate Cash.)

These realities have adverse effects on banks, whose profit margins suffer when yield curves flatten and net interest margins narrow. Gross disagrees with commentators such as Barron's who argue that the selloff in bank stocks has created an opportunity. He urges investors to shun the "tantalizing apple" of bank stocks with low price-to-book ratios – Bank of America Corp.'s (BAC) is just 0.6, Citigroup Inc.'s (C) 0.61 – since he expects the sector's future return on equity to resemble utilities'. To illustrate his point, he included a chart of Citigroup's shares (adjusted for dividends) over the past 30 years:Gross adds that insurers and pension funds will also have trouble generating the returns their business models depend on.

Other things to avoid include high yield debt and "the seemingly momentum driven higher prices of Bunds and Treasuries that negative yields have produced," since "a 30 year Treasury at 2.5% can wipe out your annual income in one day with a 10 basis point increase."

As for policy, Gross gives central bankers a D+ for the past seven years, which in turn gives him little confidence in other, more radical solutions such as the "helicopter money" that is increasingly being discussed in financial media. (See also: Finland May Give $850 a Month to Every Citizen.)

http://www.investopedia.com/articles/investing/030316/bill-gross-surviv…

Mr Gross? yeah right, yet in effect the so called financial investors helped cause this mess, and make it worse.

I know how to solve this entire crisis!

Ive invented a product..... but I need the government to set up a system where everyone is 'almost forced' to use my product to get what they need, want and use to get any of life's utilities.

Now, the good thing is I can produce this product at will from thin air almost ...so there won't be any shortages, but.... I'm not about to let everyone do that, no no no, they must work or they get none of it. And they must also pay me back MORE than I gave them. It's a real winner!

Sound great? Let's go to work and end this! yay.

Genius! What will you call it?

I was thinking something like "Poopus"

Can I have 100 Poopus please. Nice 'ring' to it

More Evidence That CalPERS Board (and Staff?) Does Not Understand Finance

http://www.nakedcapitalism.com/2016/02/more-evidence-that-the-calpers-b…

Bernard, I have to ask the purpose of this article? Are you not perpetuating a myth of the goodness of the banks, but which is in reality a house of cards? Ratings agency Standard and Poor's, which is paid by the banks to dig into the banks' accounts to assess their profitability and safety, said last month the big four banks could easily cope with the dairy downturn and an Auckland housing slump because they were so profitable is a statement that pointedly ignores the fact that that profitablility is actually depositors funds, irrespective of the fact that some twisted form of the law states that when we deposited the money into the bank, we effectively gave it to them, for nothing in return! In the event that the banks had to weather the dairy downturn they'd do so by shifting the risk and cost to the depositors funds, which means the average man on the street actually carries the risk, not the banks. They have borrowed from overseas to support their farm and mortgage lending. Do you seriously beleive that they could do this without offering some form of security? That security will not only be the actuall properties mortgaged, but also depositors funds, while the bank itself would suffer not one whit of angst! Our Government is as culpable through not ensureing banks are adequately regulated to protect depositors funds. And despite what Steven says, I am not expecting a taxpayer bailout in the event of a bank collapse. I expect that the banks themselve be required to carry insurance over their activities. You can bet that if the insurance companies are aske to carry the risk, then they would damn sure make sure the banks were monitored a bit more rigourously, or their premiums would be sky high!

I'll be honest, some of Bernard's articles of late make me question whether he has lost the financial plot or is somehow using reverse psychology. He's not working as a teller on the side is he?

Bernard, me thinks, is laying the foundations for a new career as a Labour list MP.

That thought is really scary - if Bernard believes that buying into this BS as a way to establish a political career, it means that he is really no different to any of the other dimwits already there. What we need is someone with the courage to challenge the current conventional wisdom. Someone who will pull together all the research that proves that the current economoc models are as faulty, and that balanced regulation is required to counter rampant greed, and produce stability.

AndrewJ - at least the rise in insurance premiums will help add to inflation... every cloud silver lining...

How about allowing to keep the extra margin but force them to raise the capital ratio to soak it all up (year on year)

What if it goes something like this.

Farmers are struggling, banks are charging more interest and less principle. Instead of paying %5 interest many are on %7.8 and up, like me and my livestock overdraft ,on a no debt farm but for many these are interest only loans.

So then you get into a situation, where farmers are paying %4 over what householders are paying and %6 over what depositors are getting, while farmers only pay the interest, but in reality the principle has been built into the interest, which is a tax deductible cost to the farmer.

So the taxpayer loses and the depositor stays highly exposed to a bank collapse, while the banks repatriate extraordinary profits.

Instead of the farmer paying down debts and becoming less exposed and less likely to default as they would with a 15 or 20 year mortgage they stay at high risk and so do depositors in an OBR event.

example A

http://www.radionz.co.nz/news/rural/298664/farmer-decries-bank-debt-sta…

Don't you know the latest mantra after the GFC. The Banks have to make more profits to keep them healthier to withstand the next GFC. So, let the customers pay in advance by high rates and fees. All Western countries subscribe to and practise this mantra.

If the banks have 'saved' the Reserve Bank the trouble of inflating the property market by not passing on the OCR cut, wouldn't it be much easier, more direct, and transparent for the Reserve Bank simply to not cut the OCR? I mean why cut the OCR and then hope the cut has no effect?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.