Here's the latest economic outlook - for 2019 and beyond - from Kiwibank's economists.

By Jarrod Kerr & Jeremy Couchman

Our Key Points are…

• Global growth remains strong, amid some signs of cooling. Trade wars represent the biggest threat.

• The Kiwi economy is in a bit of a sweet spot. Growth is close to trend, the fiscal position is strong, and interest rates have fallen and will remain low. Inflation, particularly foreign inflation, is weak. Wage inflation is the key, and likely to strengthen.

• Kiwi interest rates are expected to stay well below US rates, so the Kiwi dollar can glide lower once more.

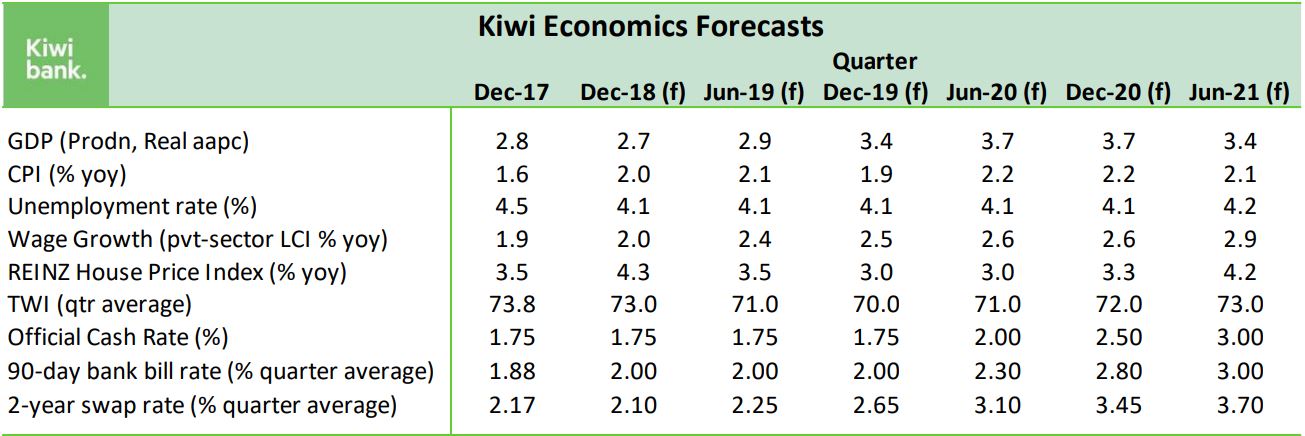

In our last economic outlook in May, we ran the title "New Zealand’s outlook is fine and partly cloudy”. Since May, the clouds on the global horizon have darkened. But our economic performance has strengthened. And there are growing divergences between the cities and the regions. In May, we provided above consensus forecasts for growth, employment and inflation. And since May, we have seen an economic trifecta with strong growth, strong inflation and very strong employment. We have also uncovered a much more dovish RBNZ Governor than previously thought. And we thought Orr was a dove to start. Low interest rates are here to stay, and the RBNZ’s reaction function is asymmetric. It will take a lot to get RBNZ rate hikes. Even if inaction eventually leads to the need to do more, later. A problem unseen in the last 10 years (post-crisis). We still need pro-growth settings, for investment.

In terms of economic trifectas, we’ve seen one of the greats. Employment, higher. Inflation, higher. And Growth, higher. That’s 3 from 3 of the great economic glamour stats. The most unbelievable decline in unemployment and surge in jobs is likely to be partially unwound next quarter. But the labour market is undeniably strong. We’re near full employment and forecast to go through full employment. Wages are finally starting to lift and should pick up over 2019-20. Weak wage growth has been the main source of frustration across most countries. And weak incomes have exacerbated inequality and caused the spike in populism and protectionism. The strength of the Kiwi labour market confirms the strong economic growth already recorded. We’re growing at trend and will likely grow above trend next year. We can thank strong Government spending for much of the forecast uplift in growth. And the Government has yet to spend what they’ve promised, while tax receipts pleasantly surprise. The fiscal war-chest for the next election is building already. Net debt is moving swiftly to 20% of GDP, a miser target we don’t need.

The weakest of the economic trifecta, inflation, has stepped up. Sure, we had to bear a surge in petrol prices, but inflation is finally running close enough to the RBNZ’s 2% year-on-year midpoint. Core inflation, which strips out volatile stuff like petrol, is a little more stubborn at 1.7%, but should move higher next year. The good news here, is wages are likely to rise in response to rising inflation. Real wage growth has performed as one might expect in the cycle, but the lack of actual inflation has held nominal wages down. And that’s simply disappointing. We’d argue good workers are much more likely to get wages rises next year, than when they asked in prior years. Go on, prove us wrong. It’s worth the chat.

The good news is our above consensus economic forecasts are largely unchanged. And we expect a slow-to-react RBNZ. So the settings will remain on “full noise” for longer. We may now see a little more growth and inflation compared to our forecasts. It’s nice to update one’s forecasts without actually moving much. But we’re wary of darkening clouds on the horizon. A cooling will be somewhat inevitable over 2020, but not through a lack of fiscal firepower, or access to debt markets.

The time is now for investment

Businesses continue to complain of sharp labour pain. Businesses complain of Labour policies and labour shortages. Complaints that have yet to translate into weaker growth. But votes of no-confidence in the Labour coalition may restrict investment. And at this point in the cycle, we need more investment. Most of the problems we face, including traffic congestion and creaking infrastructure, are a product of underinvestment. Normally, when interest rates drop to (historic) low levels, businesses and governments respond with substantial investment. Savings is the supply of money, investment is the demand. The price has fallen with increased supply (demographic savings glut, inequality, and QE money printing) and reduced demand (regulation, price of capital). We haven’t utilised the fall in interest rates, yet. And there’s no excuse. Here’s a snippet from our May report:

Ratings agency Moody’s rates New Zealand as AAA, as good as it gets. S&P rates New Zealand as AA+, pretty much as good as it gets. By comparison the US are rated AA+. They are the global superpower, with the largest bond market, and have arguably the most powerful military in history. If they’re not AAA, well, it doesn’t matter… The UK was downgraded following the Brexit vote in 2016, not once, but twice! The UK’s double-notch downgrade took them beneath New Zealand’s rating... For international investors, ratings are important and useful. But they’re not the be all and end all. Diversification is more important in a world with a diminishing pool of highly rated assets (A+ and above). New Zealand has ample room to lift debt and expand. So much so, we’re in an enviable position.

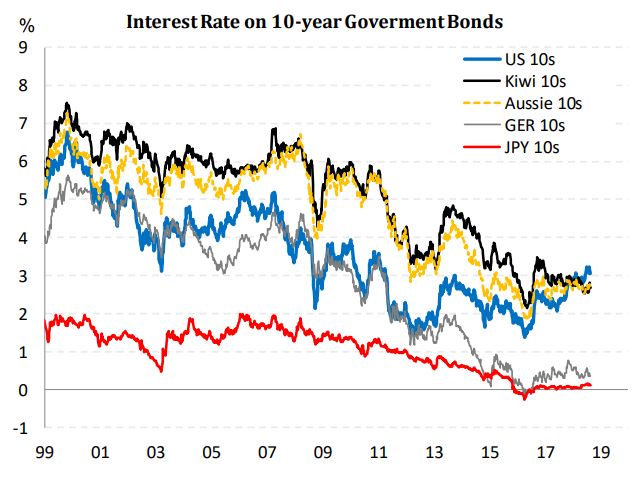

We have loads of capacity to increase public debt, and private debt to a lesser extent. We are a highly rated nation. The 20% net debt target is not required for our credit ratings. Debt targets are a great discipline on spending, not investment. Debt should be deployed to tackle our huge infrastructure deficit. So why the lack of conviction? Apparently, we risk an investor revolt. An investor revolt is simply not going to happen. NZ, and Australia, offer global investors desperately needed diversification. We won’t get punished for adding another 5-10%pts of debt to an existing 20% load that is 20- 100%pts below our peers. The proof is in the interest rate. We are paying lower interest rates than the US, out 30 years. Our Government could issue a 30-year bond below 3% - a historically low rate that should inspire long-term thinking and investment. Fundamentals drive interest rates, rarely ratings. And Kiwi interest rates will stay lower for longer (see Box A below).

The point is debt must be used for good infrastructure. And the regions are crying out. There is a dramatic difference in confidence across cities and regions. The regional disparities are growing. See “The performance of the provinces: improves beyond Auckland”. In the regions, businesses are much more upbeat. The cities are slowing, and confidence has sunk. The regions are expanding, and the pains they feel are growing pains. The hunt for labour is proving difficult and may become costlier. Regional investment is needed to boost physical capacity and attract labour. Some regions simply don’t have the accommodation available to house the required workforce.

Box A: Snow white of the seven dwarfs

When you look at central bank officials, you look for feathers. Some are hawks (predators looking to strangle growth), some are doves (prey looking to loosen the claws) and some pigeons. US Fed Chair Janet Yellen had whiter dove’s feathers than her predecessor Bernanke. And Bernanke had more dove feathers than the slow to hike Greenspan. Their feather headdress reflected the economic environment of their time. Bollard was a dove and slow to turn hawk. Wheeler was a dove, with one hawk feather.

But he added loud peacock macroprudential feathers, that covered some pigeon communication feathers. And now, in terms of birds, our Governor is snow white in dove feathers without a trace of a hawk’s influence. All seven internal and external members of a newly formed Monetary Policy Committee (MPC) are likely to exhibit similar headdress. We have a fairy-tale of a snow white dove leading the seven MPC dwarfs. Of the 4 internal members, Orr will command a dovish bias. Of the 3 external members, well, they’re outnumbered. But they may be naturally dovish, or even selected for a dovish bias. We must play the man/committee.

In May, we thought our forecasts would warrant an RBNZ hike in the second half of 2019. We underestimated the dovishness of Adrian Orr. In the August MPS, Orr delivered what we described as a blatantly dovish (forget about hikes, we’re considering cuts) statement. The change in stance, without much change in the data, led us to start playing the man, not the ball. In August we pushed out our forecast RBNZ OCR hikes to commence from May 2020. The man/committee, are more willing to let the economy run hot. And we’re not opposed. We’ve had 6 years of weaker than expected price and wage inflation. The signal given in the RBNZ’s November MPS shows a bank willing to let inflation run above the midpoint of the band over the medium term. Pay back of sorts. Note, the less they do up front, the more they may have to do later. Although to be fair, that hasn’t been the experience over the last 10 years. As we said in May: “the message is clear, don’t fear rampant inflation or rapidly rising interest rates. But both will rise in coming years. This is good news.”

Still plenty in the tank to keep the wheels of growth turning

We expect to see much stronger growth in 2019. But some key drivers of the economy look to be in decline, and include:

▪ Business confidence has been surprisingly weak. The important measure of firms’ “own activity” sit below average. There is an element of protest voting against Government policy. The uncertainty generated out of the Beehive has persisted all year, especially in regards to labour market reform, tenancy reform and taxation reform. However, the strong economic data fails to match the downbeat business sentiment. Nevertheless, if firms continue to express displeasure, we could see a reluctance to hire and invest. We need firms to hire and invest.

▪ Population growth has slowed. Net migration is still elevated, but is gradually waning. In October annual net migration hit 61,700 a level last seen in 2015. And the down-trend now looks set in train.

▪ The elevated Kiwi terms of trade (purchasing power with the rest of the world) is falling, with recent developments causing a stagger. Oil prices had marched north most of the year, lifting our import prices, and lowering our ToT. But then the Trump administration manoeuvred to lower the oil price ahead of US mid-term elections, causing some capitulation. Commodity prices in general have lost ground, as global economic momentum cools. Key Kiwi exports prices, such as dairy, have also fallen with demand concerns, and a record production year with Kiwi dairy farmers milking it.

▪ The construction sector is no longer a primary driver of growth and hasn’t been since 2017. But tradies are still building full tilt, and will have to for the next decade to address the 100,000 housing shortage. The industry is unable to build at a much faster clip, given constraints on materials and staff. The high-profile failure of major construction firms, have only made matters worse.

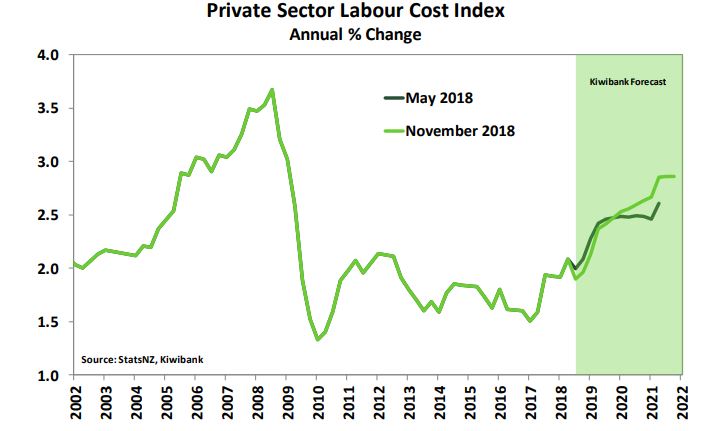

Despite these developments, there is still plenty in the tank to keep the wheels of growth turning. Household confidence should lift, from lacklustre levels. General uncertainty seems to be playing a larger role, rather than the reality on the ground. Consumers’ expectations of future conditions have driven confidence lower. In contrast to consumer confidence, the labour market is surprisingly strong with the unemployment rate dropping to 3.9% in the third quarter. Employment growth is robust, and the labour force participation rate is at a record high 71.1%. The third quarter figures may have overstated things a bit. But what is clear, is that people want to work, and they are finding work. Wage growth is also rising thanks to the tight labour market, and the start of large minimum wage hikes. Further large hikes are in the pipeline. Some chunky hikes to the minimum wage will be needed if the Government is to hit its target of $20/hr by April 2021. The labour market should play its part in lifting confidence and spending over 2019. We are picking that wage inflation will begin to accelerate from around 2%yoy now to 2.4%yoy by mid-2019. We see further upside into to 2020s, see LCI chart.

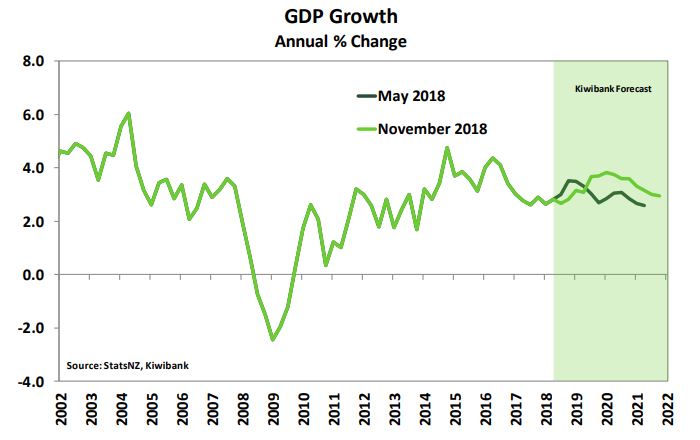

To date, there is only limited evidence that fiscal policy is spurring activity. It is simply a matter of time. The Families Package came into effect from 1 July, and the corresponding transfer payments are supporting household incomes. The payments help those households more likely to spend rather than save. In addition, there are many competing interests for the Government’s purse at present, including pay negotiations from health and education professionals, and the pressing need for infrastructure investment. The increased demand for funding will be addressed in time. Finally, the Government’s Kiwibuild programme will gather pace over 2019, and into the 2020s. The process of enacting Government policies are slow, but will inevitably lead to a significant boost in growth. Based on the slightly more gradual impact of fiscal policy to date, we have pushed out the timing of these impacts. See GDP chart.

Heading into the RBNZ’s November MPS, inflation surprised the RBNZ, hitting 1.9% yoy, to be just shy of the RBNZ’s 2%yoy target midpoint. Only 1.4%yoy had been expected by the RBNZ. A spike in petrol prices was a key element of the surprise. And we would expect that the subsequent tumble in petrol prices to weigh on December quarter inflation. The roller coaster ride in global oil prices represents short-term volatility. The RBNZ looks through short-term volatility. What is more important for the underlying engine of inflation, is GDP growth. Or more precisely, how growth is tracking relative to NZ’s long-run potential, or Goldilocks rate – seen as being somewhere between 2.5-3.0%yoy. With an economy expected to grow above its potential over much of 2019, and into 2020, we are forecasting inflation to lift. Monetary policy is still in expansionary mode.

The RBNZ even pushed the case for an OCR cut in August. Wholesale interest rates fell to reflect the risk of a cut. However, the recent economic trifecta of growth, employment and inflation, led the RBNZ to a more neutral stance in November. But the RBNZ’s more neutral stance fell short of what would have been expected given the sharp turnaround in the data. We simply have a more dovish Governor. The stubbornly dovish bias is understandable given inflation has been too low for too long. And the RBNZ is likely to be more sensitive to downside surprises in future. The OCR is unlikely to head higher in 2019. Rate hikes are a 2020 story at the earliest. Extraordinary stimulus will remain in play. Mortgage rates hit historically low levels in November, as wholesale rates fell. The fall in lending rates is yet another positive development for households, with debt servicing costs down. And low rates support housing.

The 3 Ps of property are positive

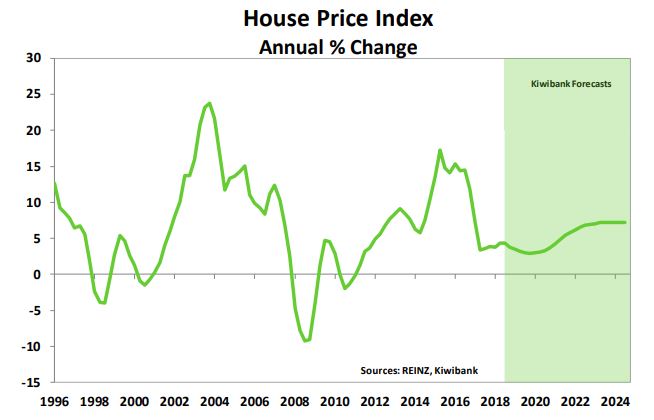

The housing market has entered a period of consolidation (see our Property Insight note for details). National house prices have risen just 4%yoy since mid-2017, and we expected prices to move broadly sideways for the next year or so. Meaningful house price appreciation is not expected until we approach the mid-2020s (see our forecast chart). We used a divining rod made up of the 3 Ps of property – population, preference and policy – to formulate our view. We modelled an undersupply in the order of 100,000 homes, and the shortage is likely to get worse before it gets better. Preferences are slowly changing too, in part by the shortage, and in part by demographic change. For younger buyers priced out of the cities, or boomers looking to unlock equity, the regions are increasingly attractive. And the regions are likely to continue to outgrow the cities in a period of catch-up.

The housing market is well supported, and unlikely to experience a sharp Australian-style correction, in our view. Mortgage rates are very low, and the unemployment rate has dropped to 3.9%. NZ’s population has outgrown the supply of housing for the last 10 years. And while population growth is slowing, thanks to easing net migration, it will continue to grow. Eventually, the current shortage in housing will be addressed, but it’s a fair way off.

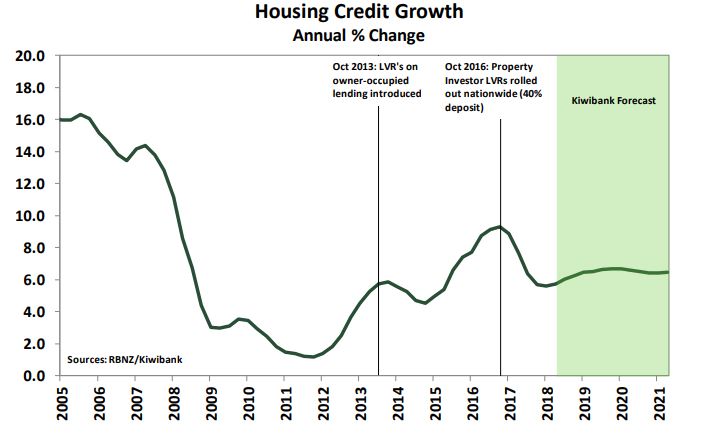

The housing market has been contained by Government policy uncertainty and tough restrictions on investor lending. Investors are likely to stay cautious for a while longer. We still have a few policies in the pipeline, such as the removal of the negative-gearing tax loophole, and the debate around capital gains tax. The RBNZ has loosened LVR restrictions in November (see Box B below). The minor LVR tweaks are unlikely to ignite loose lending or fuel house prices, the changes are for stability.

Box B: Lending is a little less restrictive

Annual system-wide mortgage growth has stabilised at around 6%yoy in response to past lending restrictions and a cooler housing market. Strong financial stability, with tighter lending standards, has given the RBNZ reason to ease the foot off the macroprudential pedal. And as we had expected the RBNZ loosened Loan-to-Value Ratio (LVR) restrictions as part of the November 2018 Financial Stability Report (FSR). These changes come into effect from 1 January 2019 (see The RBNZ has lifted speed limits on lending). More easing will come.

Before the November announcement the RBNZ had to be satisfied that housing credit growth wouldn’t just take off again if LVR’s were to be loosened. We are confident that a debt-fuelled housing boom is unlikely to transpire following recent developments. For starters, similar changes to LVRs at the beginning of 2018 had only a small, stabilising, impact on credit growth. Our medium-term view on the housing market points to a well-behaved market over the next few years, in part as investors remain largely side-lined. Remember, the new Government has already acted and has pipeline policy targeted at property investors. The policies include the tightening of the Bright-line test, restrictions on foreign ownership, the removal of the negative-gearing tax loophole, and a possible capital gains tax following the next election. Finally, bank lending standards have sharpened, encouraged by the RBNZ.

Our housing credit growth forecasts already incorporated some loosening in RBNZ restrictions, and the risks are towards slightly stronger credit growth, for a change.

Long white clouds have darkened

The global economy had a solid year in 2017, recording 3.7%yoy growth, the highest rate since 2014. But that’s old news. In recent months, financial market traders have expressed concern over lost global economic momentum. The IMF revised down its global growth outlook in October, noting that downside risks had risen. Global equities and commodity prices have fallen with concerns around demand. And in most major economies, data no longer shines so bright.

Investors are overloaded with global risks and are highly uncertain. The outlook is positive, but there’s a seemingly never-ending barrage of disruptive headlines, and now some volatility in markets. Much of the madness can simply be explained by US Federal Reserve (Fed) tightening and US dollar strength. The sucking sound of cash leaving Emerging Markets is all-too USD familiar, so too is the revaluation of equities under higher interest rates. What’s impossible to judge, however, is the madness that is Brexit, Italian debt, China’s geopolitical manoeuvre called silk road, and Trump’s ability to step back from the global stage with gravity defying hair. For a world hell-bent on globalising and capitalism, the losers are fighting back with a vengeance. The rise of the populist protectionist threatens what we take for granted.

The various clouds on our horizon, have various shades of grey. We start with a lighter shade of pale, look to the ominous darker shades, and end in the darkest of potential torrential.

The normalisation of ultra-extraordinary monetary policy is a great known unknown. The US Fed is leading the normalisation of the massive policy response to the GFC, with both cash rate and balance sheet adjustments. Policy tightening is contributing to volatility in financial markets. The Fed will continue tightening for a wee while longer. But Fed officials are now signalling a more neutral stance. US Fed Chair Powell noted that interest rate settings were “just below” neutral – the rate that neither stimulates nor constricts demand. Not long-ago, in October, Powell said interest rates were “a long way” from neutral. Much has changed in just 2 months. The Fed are closer to neutral than once thought. Fed hikes in interest rates finally caught up with financial markets in October and November. And financial markets have pushed back on Fed tightening. Equities have fallen, as they tend to do when interest rates rise.

Furthermore, the QE inflated balance sheet needs unwinding. Stopping rate hikes will arrest the rise in short-end rates. AND then allowing for a full QE unwind to inflate long-end yields. A nice balancing (re-steepening, not inverting) of US interest rates is needed to stop trader talk of an inevitable recession. Most market analysts believe in the religious-like signal of interest rate inversion. It’s kind of like watching a prophet walk across your computer screen. The Fed is now rebalancing expectations. If the Fed tightens too aggressively from here, all the hard work done to date would be undone. Not tightening any more, however, would be the signal of the end, and admission the economy is faltering. Normalising policy was always going to be like landing an A380 at Wellington airport with 8 on the Beaufort scale, earth shifting on the Richter scale, and concerns with runway length.

The ECB also wants to stop printing money (QE), and look to normalising policy. But we all know they are kidding themselves for now. They’d love to try and land in Wellington, but the control tower won’t accept old WWII planes running on one German engine (the other French engine is in flames), and without landing gear.

And then there’s the rise in EM crises. Concerns around future growth does not just centre on developed economies, with emerging economies having a tough time in 2018 – in particular Turkey, Argentina, Venezuela and Brazil. Emerging market currencies have plunged and falling commodity prices are ravaging EM current accounts. When the US Fed hikes interest rates, there is much pain for EMs to bear. That’s because their debt is denominated in US dollars and we have seen USD strengthen through much of 2018. Debt repayments become more expensive and (unlike NZ), EMs bear the currency risk, not the investors. When their currency falls, the local currency amount of USD debt required to be repaid lifts violently. And global capital is a fickle beast. Interest rates have been trending higher in the US. Emerging markets must now pay up to convince investors to stay in EM. A cost they can not afford without the nominal growth to pay for it.

The fall in commodity prices, most notably the price of oil, means the outlook for global inflation is looking a little weaker. Oil prices have dropped over 30% since the start of October, and geopolitics is at the heart of developments. The US Trump administration kept the pressure on their key ally Saudi Arabia to force oil prices down into the US mid-term elections. The pressure has continued after the US mid-terms. Even international outrage at the killing of journalist Jamal Khashoggi at the Saudi consulate in Istanbul didn’t weaken the bond between the US and Saudi Arabia. Oil markets are looking oversupplied at present, and it might take some time before prices recover. OPEC may once again intervene in the market to lower supply. But that’s hard without the help of the Saudis, and the recent exit of Qatar.

The dispute between two economic titans worries all. The Trump administration’s ‘America First’ mantra is heard loud and clear. The Trump administration has pulled out of the UN human rights council, and stepped back from bodies such as the WTO and NATO. Trade disputes have started. To date, import tariffs have been lumped onto +US$250bn of Chinese imports. China has responded in kind. But on bilateral trade, China holds a losing hand. President Trump is threatening to double the 10% tariff to 20% on existing, and extent tariffs on an additional US$267bn imports if China refuses to alter its trade practices. Markets participants are rightly worried. The US-China trade spat is a moving beast, and markets still hold out some hope that a trade deal will be reached – similar to the ceasefire reached between the US and the Eurozone earlier in the year. Talk from last weekend’s G20 produced a 90-day ceasefire. But the conditions of the ceasefire are near-impossible for China to accept in just 90 days, without losing face. The trade-dispute will most likely reignite in March. For NZ, the ongoing US-China dispute is concerning as we are heavily export reliant, and reliant on the smooth running of global financial markets. So far, the tariff wars are not yet reminiscent of full blown trade wars. The difference is country of origin. If a trade war were to develop, the US would start physically diverting trade away from China, not taxing trade. The potential for escalation scares us. The trade dispute is symptomatic of a larger, geopolitical, pushback on China.

Europe is a never-ending source of uncertainty. Italy’s newly formed populist coalition government is facing off with the European Commission (EC) over budgetary constraints, exposing a potential debt crisis in the making. Italy argues that years of fiscal austerity have unnecessarily weighted down growth, and they’re right. Italy wants to be able to break the shackles of the EU’s fiscal rules to reverse the post-crisis malaise. Finance Minister Giovanni Tria is aiming to lift Italy’s 2019 budget deficit to 2.4% of GDP and the EC is not happy. Italian government bond yields have shot up in a sign of investor risk aversion, making it more expensive for the Italian government to borrow. Adding more concern to the mix has been the Italian banks (a banking sector that is shaky in itself) increasing their share of Italian Government debt as foreign investors take flight. A broader concern is the rising risk of a debt crisis emerging that draws in the whole EU, as Grexit did. The level of Italy’s Government debt is eye wateringly high at over 130% of GDP – remember NZ’s is around 20%. Another complication is that Brussels will not want to be lenient towards Italy, as it could open the door for other highly indebted European economies to try and spend their way out of trouble. The faceoff could send Italy towards the exit door too. An Italian debt crisis is by no means inevitable, but it is worth keeping an eye on. Greece, or Grexit, was the decidedly harsh precedent set for this very reason. When speaking of PIGS, Greece is a rounding error in terms of debt (~85bn), whereas the PIS in PIGS are impossible to bailout. Italy has the 4 th largest bond market in the world. It’s hard to write down over 3 trillion in debt

Meanwhile in Britain it’s all go on Brexit as the UK moves closer to the crunch point. On 29th March the UK is due to leave the EU, with or without a deal. UK Prime Minister Theresa May has managed to get the EU to approve a withdrawal agreement. Now she must convince the UK Parliament. This is no easy task with protest from all sides of the House of Commons, including within her own Conservative party. The talk of another referendum (we want back in the EU we never managed to leave) is growing. For now, the UK is weak, and unable to argue on anything other than Brexit, for fear of needing to stay open to (free-trade) deals if they’re spat out of the EU. The EU’s withdrawal agreement is a “take it or leave it deal”. And if Greece is any example, the EU are ruthless negotiators. The Bank of England has warned of the recession-forcing consequences of a hard Brexit. Brexit is a generation defining moment in UK politics, and the British people are deeply divided. Make no mistake, Brexit is Britain’s populist movement. People are divided by class, wealth, education, and region. Globalisation, immigration and disruption (like Amazon) has torn apart some labour-intensive industries, favouring the rich, well-educated workers of the city, at the expense of the poor(er) classes in the regions – somewhat similar to Trump supporters…

Populism and protectionism is the root cause of most of the risks we face today. And the rise in populism has weakened many Governments, enabling China, Russia and other nations to take a bigger role on the global stage. Especially as the US pulls out of human rights councils and scorns trade bodies. China and other countries with well documented human rights violations may be left unchecked. The biggest threat in the post-crisis world is the rise of populist politics. In the developed world, wage growth for most has been disappointing ever since the GFC, while those at the top of the tree have had a massive QE induced injection in wealth. We’ve seen a sharp lift in inequality. Populism has cultivated protectionism, a worrying and potentially destabilising force for the forever globalising global economy. If left unchecked, we may find ourselves looking up at a fullblown trade war, geopolitical manoeuvring, and the end of the EU itself. It’s simply impossible to gauge the impacts, but they’re not positive. To date, the political resolve to hold trade and established regimes together remains.

Financial markets continue to work in New Zealand’s favour

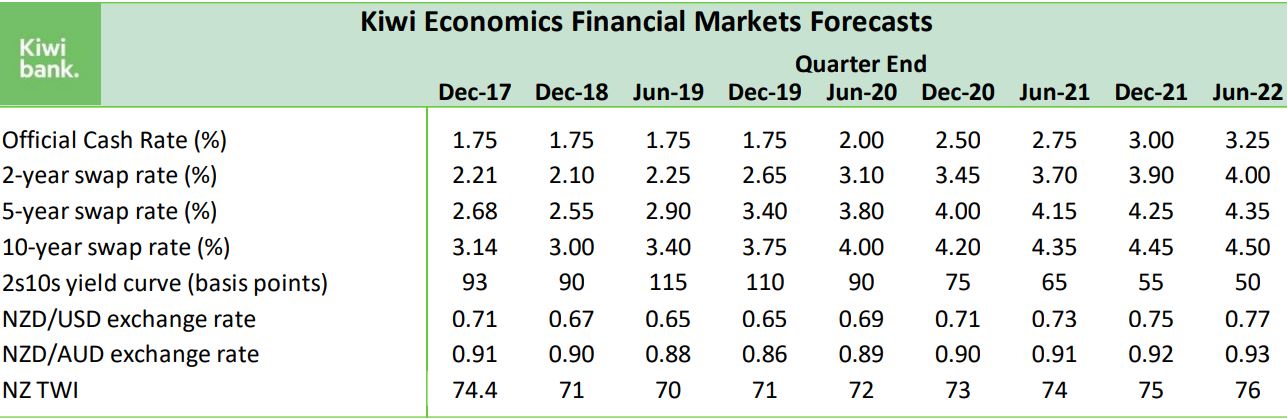

In terms of financial market forecasts, our 2-year swap rate forecasts are tracking nicely, off a much more dovish RBNZ. The 2-year swap rate is used by banks to offer 2-year mortgage rates. Our forecast of 2.1% by year end looks bang on. So our forecast 2-year swap rate over the next few years remains unchanged. The price of longer term money, however, is cheaper than we thought. We’ve had to lower our 5-year swap rate and 10-years swap rate forecasts by 10 and 20bps respectively. The reason: US interest rates are 10-20bps below our August forecasts. Our outlook for the Kiwi dollar is a little higher also. Because the US dollar has weakened of late. The US data has cooled and the US Fed is closer to neutral than they originally thought. The NZ dollar had depreciated since May, in part because the Fed continues to tighten, while our central bank the RBNZ is comfortable to sit tight. We believe these forces will hold well into 2019, and continue to expect a depreciation in the bird.

Please note we will publish a more in-depth financial market outlook next week.

Here’s a quick summary of our forecasts

New Zealand’s economic performance has lifted, and since May we have seen an economic trifecta of strong growth, strong inflation and very strong employment. This despite downbeat business confidence survey readings. We expect growth will strengthen from 2.8% yoy seen in the June quarter through much of 2019 to peak in early 2020. Consumers face several supporting factors and low interest rates is one of them. We have also uncovered a much more dovish RBNZ Governor than previously thought, which means low interest rates are here to stay. This should help underpin growth in the near-term. However, most of the above trend growth built into these forecasts is expected to come from the uplift in Government spending. The Government has yet to spend what they’ve promised. This delay has in part led us to push out the expected impact of fiscal policy well into 2019, compressing the impact of fiscal policy on growth.

Inflation has moved much closer to the RBNZ 2% target midpoint, at 1.9% yoy in the September quarter. A sharp rise in petrol prices was a major driver, and the subsequent fall in pump prices is expected to weigh on inflation in the fourth quarter. However, above trend growth sees annual CPI inflation move above 2%yoy as we head to 2020. This should also lead to higher wage growth. The labour market surprised us with its strength in the September quarter, the unemployment rate plunging to 3.9%. The lower unemployment rate starting point, combined with the more positive run of local data led us to lower our unemployment rate forecast. Wage growth will strengthen as the labour market tightens and some big minimum wage hikes are undertaken. The Government is still committed to lifting the adult minimum wage to $20/hr by April 2021. To achieve this goal there would need to be some sizable hikes planned for the coming few years. We have assumed that the minimum wage will add between 0.3-0.5%pts to June quarter wage inflation over the coming few years.

The housing market has entered a period of consolidation. National house prices have risen just 4%yoy since mid-2017, and we expect prices to move broadly sideways for the next year or so. The 3 Ps of property – Population, Preference and Policy – have all conspired to create an estimated undersupply in the order of 100,000 homes, and the shortage is likely to get worse before it gets better. Also, Government policy uncertainty and investor-related credit restrictions have contained the housing market. But on the bright side, the housing market is well supported and unlikely to experience a sharp Australian-style correction. A well-behaved housing market should keep the reins on mortgage-related credit growth.

Looking at the export sector, the prices for some of NZ’s major export commodities have not been spared from a general funk in commodity markets. Dairy has experienced months of price declines on the Global Dairy Trade (GDT) auction. NZ has also had a mild spring, and production is strong. We see NZ’s ToT fall from record highs in the near term in part because of lower export commodity prices. But the ToT should remain at a respectable level and even recover over the medium term. It’s important to remember that NZ produces plenty of what a growing world needs, that is food. But NZ is not just agriculture, and the lower NZ dollar is a positive for our services exports too. Our Tourism sector remains hot, and this has perhaps become a case of having too much of a good thing. Capacity constraints are present in this industry, with accommodation occupancy rates stretched. Nevertheless, the medium-term outlook for tourism remains solid, people are happy to queue up to see our little corner of the world. Investment is the answer.

*Jarrod Kerr is Kiwibank's chief economist and Jeremy Couchman its senior economist.

49 Comments

Have a closer look at some of those graphs, Jarrod, especially the House Price Index, Annual % Change and tell me you don't see a double-top formation! And we all know what that means, don't we....( A clue: The projection into the light green area is in the wrong direction!)

I disagree bw.

Rather than looking at patterns of cycles it is better to look at factors that are influences in the wider economy and the housing market as this article does.

We still have low interest rates, historically high immigration, and an economy apparently trucking on not too badly, which are all supporting the housing market at current levels. It would seem that these factors - aside from external threats - are likely to continue.

Also RBNZ have some influence on the housing market through interest rates through OCR and demand through LVRs. In the event of either an external threat or an overly cooling of the market then RBNZ are going to ease the LVRs. The easing of LVRs for FHB and investors from 1 January will provide support for the market going into the new year and I think RBNZ ensuring that the market does do this. It is worth noting that six months ago Orr commented that he saw a stability to mild growth in the housing market (2 to 3%) and I think that RBNZ will be wanting to achieve this which is reflected in the housing index graph projection.

I think a great well reasoned article looking at current factors. Analysis of cycle patterns is less reliable.

FHB should note the comment "Low interest rates are here to stay"; that window of opportunity to buy and pay down debt may be a little longer than the 1 to 2 years as has been widely anticipated.

I'm a FHB currently in the market, and I'm getting reasonably nervous about putting any offers on property. Yes a lot of the factors are pointing in the right direction for our economy currently, but haven't the figures been very similar in Australia, and we've all heard enough about their market. The only difference I see is now that it has turned in Australia the RBA are more in a mood to let the market run on its own than prop it up. Where as the RBNZ is a lot more proactive trying to keep the market in a similar or improving condition.

There's a member on this site, his name is PropertyPrices2Fall. He's also a FHB, been at it for 8 years now, so if you have any advice have a chat with him. One of the most experienced Sidelines Dwellers out there.

Well I feel since I've been in the market for a maximum of 6 months, I've got a few more years to go then!

NZ Dan makes a good point (although a sarcastic one), be careful not to be a FHB for the next….10 years. It's very easy to get talked out of buying by people telling you the sky is about to fall. If you can afford it, get your finance sorted first, choose an area you want to live in, then look at A LOT of houses until one stands out for you and put a conditional (upon finance) offer in. Looking at a lot of houses is very important because it gives you the confidence to act quickly when the right house comes along, and it will.

Once you have bought it, hammer the mortgage down best you can

Seem to be talking from experience eh, you sound very much like a street dweller

Hi Big Saint, i am a future FHB on the sidelines at the moment. If you do compare our current news with Australia 18 months ago you find that the arguments are the same, high immigration, under supply and cheap interest rates will mean prices wont fall. Australia had a tightening credit situation through their banks and now prices are going downhill due to lack of demand and lack of available credit to prop up higher prices. Their banks are our banks.

I personally think prices will fall within the next 3 years, especially if (when) we enter another global recession. Even if its a 20% drop, that matters hugely in the long run. My main fear is buying a house now and losing the flexibility to move if something happens to prices.

Hi TM (and BS)

So you area potential FHB.

So TM, from what you say, your fear is based on the proposal that you are going to buy your first home now and then sell and exit home ownership in three years time.

To put it mildly - that is absolute rubbish.

You will own a home for considerable period of time - and like the KS growth fund which may be volatile in the short term - in the long term it is more than likely to show considerable capital growth.

Unless you are overly highly and risked leveraged - and your bank, to protect their own butt, is going to make sure that isn't the case - you will survive any temporary downturn in the market.

So what if the market drops 10% or 15% in three years time you will still have and be living in the same house. Yes your equity may be temporarily lower, but hey - you and the wife/husband/partner and tribe of kids are still going to get up every morning in the same home without the sky having fallen in - and as a certain - the sun will be coming up in your front window each day.

So what if prices fall and you want to trade up or move somewhere else - smile big time, as the price differential in a depressed market between your cheaper home and that one you want is going to be less. Trade sideways - you will be selling and buying on the same market.

Your problem is that you are a victim of fear based on things that really won't affect you. You are simply presenting invalid reasons for not having the balls to invest in your and your family's future.

If I was to be currently looking to invest in property for the three year period that you suggest - then that is different mater and you need to really think about why that would be. I am interested in your response.

This is the dumbest advise I've read on this site. FHB in this market are almost certainly going to need to be highly leveraged. How many FHB have a 30%+ deposit?

If prices fall the FHB is the first in line to get screwed over. Prices fall you and end up with <20% equity ... enjoying paying a premium on interest rates and Lender protection insurance.

And if you want to trade sideward or upwards? Good luck when your initial equity of 150K has shrunk to 50K due to price falls.

Thanks for that Printer,

I'm very much in the mindset that if I find a property which I like(which I may have), if I can get that property for what I feel is a reasonable figure. Which hopefully should help cover any shortfall in the future, as well as something I can add some value to. Then even with a correction, unless its in the 20-30% margin with having not paid rent I'll be in a very solid position. However I'm just a Millennial trying to get ahead.

"So what if prices fall and you want to trade up or move somewhere else - smile big time, as the price differential in a depressed market between your cheaper home and that one you want is going to be less. Trade sideways - you will be selling and buying on the same market."

Not quite right!

Do the sums on a Big fall, say 50%.

That $750k house you 'own' that you had 20% equity in, and owe the bank $600k; and you want to move up to the $1 million one ( at today's prices)?

at 50% fall ( not out of the question!) your present house is worth $$375k and you still owe ....$600k ( less time decay of payments made). That $1,000,000 has fallen to $500k, and you only need a deposit of $100k. BUT you syill owe $ 600k! Is the bank going to let you sell 'their' house for $375 to buy one for $500k?

No, is lilely to be the answer, unless you pay them back the' missing' $200k difference at 80% LVR.

Trading...anywhere, up down or sideways.. is not as easy as it seems when prices fall....

Yes bw I agree

If there is a 50% fall we all will be in really, really big trouble. In fact there will be an economic apocalypse and most will fortunately hunkering down and not worrying about trading up in such circumstances.

Fortunately I don't know of any commentators anticipating such a fall - other than possibly in a very extreme catastrophic scenario.

It all depends on your equity and the likelihood of having to sell/move.

If you have 40% equity and your job/location is very stable, a 10-20% fall is nothing to worry about.

If you only have 20% equity the equation becomes very different.

No one ever anticipates a 50% fall, in anything. That's why it occasionally happens.

Be it Irish/Spanish/Portuguese/Dubai etc property; US and Global shares or bitcoin. No one ever expects it. Yet it can and does happen....

Will it happen here? Well if it did, it's only the unwinding of the last doubling in property prices, and there have been 4 or 5 of those over the last few decades. So there's heaps of room to move!

Just make sure that you continue to save after buying the house. Don't get the absolute biggest mortgage that you can. Put pay rises into savings or pay down the mortgage quicker.

50% drop in value is unlikely. A 20% drop would wipe out the initial equity but if you save $60K-$100K over 3 years and LVRs are further reduced you'll be in a decent position to consider upgrading to that $1M house (now $800K), or at least only 1-2 years more savings away from it.

Don't get the absolute biggest mortgage that you can. Put pay rises into savings or pay down the mortgage quicker.

One thing I wonder if there are simply enough Kiwi families or couples who can afford to do that with the current house prices.

Usually there are jolly good reasons house prices relate to other economic factors such as incomes. Reasons called fundamentals.

Prices and the money that enough numbers of Kiwis are making are quite out of kilter, according to international coverage. It just remains to be seen whether the NZ market can stay stable yet fundamentally disconnected for a long period of time.

Maybe it can, with the help of the RBNZ and other measures (e.g. WFF, accommodation supplement, first home buyers' grant) propping it up. Maybe not. Maybe National can get back in and throw the immigration and foreign buyer gates open as wide as they possibly can to suit their greyer voters at the cost of young Kiwis. Who knows.

Something we'll all just have to wait and find out.

Why Australia is different....

https://www.qv.co.nz/property-insights-blog/nz-vs-australia-a-property-…

Why Australia isn't different...

http://motu-www.motu.org.nz/wpapers/16_04.pdf

Section 5 on page 15 is particularly intriguing.

"Thus there are three groups of citiesin terms of price dynamics: leaders (Melbourne, Sydney, Adelaide, Canberra, Brisbane); followers (Perth, Hobart, Wellington, Auckland, Darwin); and laggards (Dunedin, Christchurch, Palmerston North, Hastings, Tauranga, Hamilton).

All leader cities are within Australia and all laggards are within New Zealand, while the (mid-group) followers comprise a mix of Australian and New Zealand cities. The cities within this group are all geographically very distant and/or separated by water, from the core Australian cities of Sydney and Melbourne.

Together, these results indicate that non-stationary shocks to Australasian house prices are first experienced in the major Australian cities, then flow through to the more peripheral Australian cities plus Auckland (New Zealand’s largest city) and Wellington (New Zealand’s capital city), and subsequently flow through to the more peripheral New Zealand cities"

TM, I'm really don't want to contradict you or upset you but be very, very careful that you don't end up being a FHB for 10 years or more. You will always find a reason why it's not a good time to buy a house but at some stage if you want to own, you will have to take the plunge. I hope you find the courage soon.

Sincerely

Yvil

I'm with you Yvil, you need to be very wary about taking financial advice from the disproportionate number of others here that are anti-housing or you will end up renting for life.The decision to buy is based on many variables, not just your financial position. Seeing as there is just a bunch of essentially anonymous people here, I would be assessing my own situation because you simply cannot post enough information here about yourself for others to make the informed decision for you.

Hey Yvil & Printer, Definitely wont end up being a FHB for the rest of my life. What i do know is that NZ got off lightly in the last financial crisis and with my opinion we have a larger financial crisis coming up within the next 2 years. Prices fell last crisis and they will fall next crisis and even its is only 5-10% then i win as my current financial situation lets me save 50k a year. All in all i would rather wait and see what happens between the global financial situation, Australias meltdown, FBB, ring fencing and trade war. Too much uncertainty to lock down a 400k mortgage on a half decent house at the moment when i don't need too.

There are way too many similarities to ignore. Every argument for NZ prices holding up were used to describe Sydney and Melbourne prior to the falls (economy, low rates, immigration). Auckland prices have already stalled (just like they did in Sydney over a year ago).

Even once prices started dropping everyone was predicted peak to trough falls wouldn’t exceed 5-7%, due to all the same reasons. Fast forward a few months and price falls have already exceeded those predictions, and the velocity of prices falls is only increasing. The positive feedback of rising prices (increasing owners’ equity, thus boosting purchasing power) works in the reverse as well.

So what will be the trigger? At this point I'm worried continued falls to AU prices alters the risk appetite of the big AU banks (and their NZ subsidiaries). 80% of our mortgage lending is done by those banks.

Thanks for the lively debate - a great Friday afternoon.

Having said that, I wish all FHB the best of wishes and that they get to fulfill the Kiwi dream of home ownership for both all the intrinsic reasons and financial security.

Just don't procrastinate; don't find any reason not to buy, and certainly don't put your and your family's lives on hold. With every action there is usually both some risk and a need for commitment.

Have a great weekend.

Cheers

"Rather than looking at patterns of cycles...." Some people are paid big money to do nothing else but that. And as technical analysis such as Charting shows us....time will tell!

NB: Tell me there aren't any number of commentators on this site that don't regularly start with "At this stage of the property cycle....". If they believe that 'there's a cycle' then maybe there is one! The trick is to see the turns in advance....

I believe in Santa... maybe there is one!

There is, there is! I've been to his village in Rovaniemi. -40*c, it was; Christmas Eve and pitch black by1 pm; on the back of a skido. Unforgettable....

Not in Nelson.

how optimistic kiwibank's forecasters are, apparently NZD will go under 0.5 if that happens as the US Fed and RBA are not as positive as NZ bankers.

Besides the private sector labour cost graph the rest look like the editor fell asleep when they got to the light green part. I almost fell asleep when I read "snow white dove". An ok article but not sure these guys are worthy of a wage increase.

Most of the problems we face, including traffic congestion and creaking infrastructure, are a product of underinvestment.

Not true. Our biggest city is undertaking massive sprawl. Sprawl is expensive and causes congestion - in Auckland overinvestment is creating these problems.

For instance an effective light rail system offers interconnected travel allowing people in compact high density living to mass transit. Auckland sprawl uses light rail on elongated spokes through very low density areas to mimic motorways. An incredibly expensive misuse of infrastructure funded by overinvestment.

Full employment (apparently, but this is NZ so I'll take it at face value), rising wages, low interest rates, Labour government, it's Party Time. I thought I was reading a Party Political Broadcast at first, the authors are so chipper, but these two do seem to be looking at the data.

My problem is this, from the perspective of my business interests this is all great stuff (I made the mistake of investing in the productive sector when I first got here, long since remedied), but from the perspective of NZ being a nice place to live, not so much. The celebration of debt fueled partying leads to nasty hangovers. Presumably if NZ continues to track along nicely then the NZD goes up and up (parity with USD?). So great for overseas holidays. NOT so good for exporters, including tourism. Good for house contruction too, as parts get cheaper. So the inequality issues get worse and worse, caused by immigration and low interest rates leading to higher debt burdens on younger generations. The export sector and import substitution sectors gets hollowed out even more. That seems to be what people want, but it makes no sense to me.

Far from a new beginning, the NZ business model of Shareholder Dilution is unchanged from the days of Clarke, Cullen, Key and English. As a nation we choose house price inflation and immigration over productivity every time. Every time. It is as if we are intent on self harm.

Everything is wonderful, have a great, happy weekend folks!

'The outlook is strong but uncertain' - you don't release the doves when the outlook is strong. In fact quite the opposite!

New Zealand's business model demands it. It needs more immigration and more mortgage debt. It is based on shareholder dilution, not profitability derived from productivity. The management do well (banks, bureaucrats and politicians, real estate agents, lawyers), but the shareholders and workers pay for it. It's a variation on the Ponzi scheme, with new immigrants being the new shareholders. We all end up owning something that gets less valuable, in this case the right to live here. The price of the shares (house ownership is the proxy here) goes up, but the benefit of ownership goes down. Why else do generations of young kiwis leave for Aussie?

In layman's terms Roger, what you seem to be describing is the 'Mordor business model' - keep stoking the fires of mount doom with more debt each year and more slaves, and don't stop until their 'rings' hurt?

I prefer thinking of it as a Debt Farm, where the livestock happily compete with each other to pledge more of their lifetime earnings for a better barn. The sad thing is, it doesn't have to be that way, NZ still has good choices.

Someone called it the Teenager Model, always make the easiest choice. Trouble is, as time goes by your field of choice gets narrower, until you end up with no good choices, just bad ones and awful ones.

Since May, New Zealand has achieved

Higher greenhouse gas emissions.

Dirtier water.

Decreasing biodiversity.

An ecological trifecta. Three from three of the great ecological disgrace stats.

All for growth achieved from a draw-down on natural capital Why can't these people connect the dots?

Do you have a current URL? My info shows little or a small drop but its only to 2016.

Which ever it is we still have terrible stats fr a so called "green country" https://www.radionz.co.nz/news/national/331646/nz-seventh-worst-on-emis…

And in Auckland you can't drive anywhere and young people can't afford a house.

But hey! Everything's rosy!

Thank you to the doves above, and a good balance from the hawks in post. I love this site.

Look at those OCR predictions - in the out-years they start with a 3....Dovish????

Now where was that link to the research that found that inflation gets unstable above 3%? Darn, can't find it. I'll keep looking. This one bears re-posting daily though:

https://finance-commerce.com/2018/10/paul-volcker-whats-wrong-with-the-…

Well we have had low interest rates for a while now and the only 'pickup' I can see is in asset values which brings me back to Hussman

"Our view is that no form of investment risk is always worth taking without regard to valuations, fundamentals, economic conditions, or market action. The strategy of buying and holding index funds for the long run is essentially a strategy that says that market risk is always worth taking. Yet the iron law of investing is that a security is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment.

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on stocks (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that current stock prices are higher also implies that future long-term returns will be lower, but that's part of the deal.

https://www.hussmanfunds.com/wmc/upd02d.htm

The idea that some salaried govt bureaucrat can somehow fix interest rates, 'set the market' in a way that guarantees long term growth is as ridiculous as some religious cult predicting the end of the world on Thursday.

The farm we purchased for 600k in 2000 now has a value of nearly 3 mill, the income is almost exactly the same as it was 20 years ago when I paid %12 interest.

China is having a go at government controlled/induced growth

"Under his presidency, China’s economic policies are favouring workers more than at any other time in recent decades. One doesn’t need to look far for evidence. Since 2015, the People’s Bank of China has showered 3.3 trillion yuan ($475 billion) of helicopter money on shanty-town redevelopments. As much as 60 percent of that money went as cash settlements to poorer households.

By now, loans to policy banks for shanty-town projects have ballooned to two-thirds the size of the PBOC’s medium-term lending facilities, its primary vehicle for injecting liquidity into the broader economy"

https://www.bloomberg.com/opinion/articles/2018-11-26/china-workers-ris…

Unproductive assets are not the economy, the deflationary forces have been building for a while and I see no sign of them abating.

And example would be hospital cleaners getting $25 dollars an hour when already self drive cleaning systems are widely used in places like Walmart.

The benefits from AI will flow to the owner of the technology not the wage earner, therein lies the rub.

And the bond market is telling us that out further the big money is betting on no growth.

The only way they can keep this economy growing with continued low interest rate policy, is with a lot more debt, mostly invested in the wrong things. We just push the debt crisis out further and make it worse

$everything $is $just $fine $so $long $as $it $all $starts $and $ends $with $.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.