The deadlock has been broken.

Until now, all the major banks offered 4.75% for a fixed two year home loan rate as did five of the six challenger banks. Those that didn't were slightly higher.

But now, TSB has broken from the pack, launching a 4.49% two-year rate. That is -26 bps lower than their previous rate for that term.

At this level, it puts TSB out on its own. It is even lower than the Wairarapa Building Society's low two year fixed rate of 4.59% which was the previous low.

With the spring real estate selling season kicking off, and more volume likely in the market, this change signals that home loan rate competition is likely to be fierce.

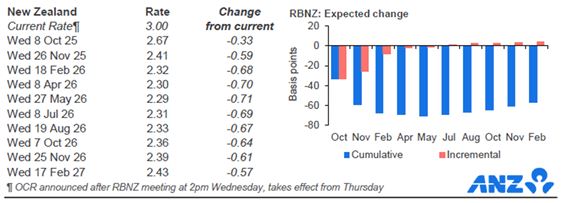

And the background is changing. The RBNZ's August 20 rate cut of -25 bps has been just the start. The very weak Q2-2025 GDP result last week brought a very sharp renewed downward shift in wholesale swap rate, and built the expectation of at least a -25 bps rate cut again on Wednesday October 8, 2025.

In fact, financial markets are eyeing a -50 bps cut, with half of the extra already priced in. So it is a 50/50 chance of either a -25 bps or -50 bps reduction coming in two weeks, according to this wholesale pricing.

These same markets see our current 3.00% OCR down to about 2.25% by February 2026. Of course before then we will have the Q3-2025 GDP result and if this is also unexpectedly weak, this market pricing may change sharply again. But many economic observers are not currently expecting that, seeing a stabilisation and some minor expansion setting in.

Currently, 4.49% is the lowest rate for any term in the market. But most one year and 18 month rates are still at 4.75%. So reactions to today's TSB move could come from any direction.

We haven't seen a 4.49% rate previously since March 2022 for a two year rate, June 2022 for a one year fixed rate.

TSB did not announce any matching term deposit rate changes at the same time.

To compare mortgage rate offers in a way that includes the application and account fees costs (or break fee costs if you need to do that), and applying the impact of a cashback/legal fee reimbursement/ or other incentive, you can now use our new home loan comparison calculator. You can find it here. Or, for convenience, we have added it to the bottom of this article.

We sense that the ability to achieve meaningful discounts from carded rates is now much harder, so the impact of the incentives offered are currently playing an outsized role. Reader-reported mortgage rates are welcome, so please record them if you have them. We need you to record them in the comment section below, which helps us stay on top of this aspect of the home loan rates market.

And still negotiate. How flexible banks may be will depend on the strength of your financials.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is below.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now.

Here is the snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at September 24, 2025 | % | % | % | % | % | % | % |

| ANZ | 4.99 | 4.75 | 4.75 | 4.75 | 4.99 | 5.59 | 5.59 |

| 5.04 | 4.75 | 4.75 | 4.75 | 4.99 | 5.29 | 5.49 | |

| 4.99 | 4.75 | 4.75 | 4.75 | 4.95 | 5.09 | 5.39 | |

| 5.05 | 4.75 | 4.79 | 5.05 | 5.39 | 5.59 | ||

| 5.09 | 4.75 | 4.75 | 4.75 | 4.95 | 5.09 | 5.39 | |

| Bank of China | 4.98 | 4.68 | 4.68 | 4.78 | 4.88 | 5.35 | 5.35 |

| China Construction Bank | 5.09 | 4.75 | 4.75 | 4.75 | 4.95 | 5.99 | 5.99 |

| Co-operative Bank (*=FHB only) | 4.99 | 4.65* | 4.75 | 4.75 | 4.99 | 5.39 | 5.49 |

| ICBC | 5.09 | 4.55 | 4.79 | 4.89 | 4.99 | 5.35 | 5.39 |

| (*=FHB only) |

5.09 | 4.29* | 4.75 | 4.75 | 4.99 | 5.39 | 5.39 |

| |

5.09 | 4.75 | 4.99 | 4.49 -0.26 |

4.99 | 5.39 | 5.49 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

6 Comments

Anyone care to guess how far off the first sub 4 rate we are?

It's 0.50% away, lol

Haha.

I'm picking sometime following the February OCR review.

Is NZ inc, that level of completely stuffed?

If we weren't getting a new RBNZ governor I would say Xmas. But I agree probably Feb.

Everyone forgets rates were under 4 before COVID. I think that 4 is where we will settle.

Yes a foreign governor could throw a slight spanner in the works. We'll just have wait and see.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.