It isn't market-leading but it is notable all the same.

TSB has trimmed its one year fixed mortgage rate to 4.39%.

That is a 10 basis points (bps) cut from its previous rate card for that term. But more importantly it also undercuts all the main banks who had settled on a 4.49% one year fixed rate.

TSB started the current cutting cycle with a 4.49% two year rate when all the majors had a 4.75% rate, back on September 14. Subsequently all the main banks moved down to 4.49% for that term.

And then most banks moved to 4.49% for a one year fixed term, TSB included.

This latest move sees this challenger bank move it lower again, back to early 2022 levels.

But to be fair, 4.39% for one year fixed is not the lowest offer for one year. ICBC has 4.25% and Bank of China has 4.28%. These are themselves notably lower than even TSB's new setting.

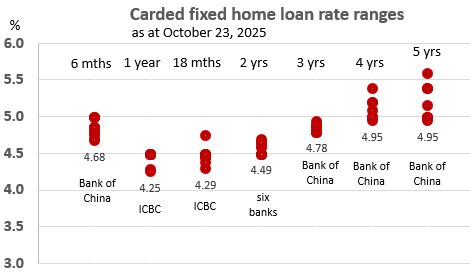

The latest TSB move does not change where fixed rates have now landed overall:

TSB did not announce matching term deposit rates changes at this time.

To compare mortgage rate offers in a way that includes the application and account fees costs (or break fee costs if you need to do that), and applying the impact of a cashback/legal fee reimbursement, or other incentive, you can now use our new home loan comparison calculator. You can find it here. Or, for convenience, we have added it to the bottom of this article.

We sense the ability to achieve meaningful discounts from carded rates is now much harder, so the impact of the incentives offered are currently playing an outsized role. Reader-reported mortgage rates are welcome. So please record them if you have them in the comment section below, which helps us stay on top of this aspect of the home loan rates market.

And still negotiate. How flexible banks may be will depend on the strength of your financials.

One useful way to make sense of the changed home loan rates is to use our full-function mortgage calculator which is here.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options. Break fees will be minimal in a rising market. But they become important in a falling market, like now.

Here is the snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at the moment.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at October 29, 2025 | % | % | % | % | % | % | % |

| ANZ | 4.79 | 4.49 | 4.49 | 4.49 | 4.79 | 5.39 | 5.39 |

| 4.85 | 4.49 | 4.45 | 4.49 | 4.79 | 5.09 | 5.15 | |

| 4.79 | 4.49 | 4.45 | 4.49 | 4.79 | 4.99 | 4.99 | |

| 4.75 | 4.49 | 4.49 | 4.85 | 5.19 | 5.39 | ||

| 4.89 | 4.49 | 4.45 | 4.45 | 4.75 | 4.99 | 4.99 | |

| Bank of China | 4.68 | 4.28 | 4.38 | 4.58 | 4.78 | 4.95 | 4.95 |

| China Construction Bank | 4.79 | 4.49 | 4.49 | 4.49 | 4.79 | 4.99 | 4.99 |

| Co-operative Bank | 4.79 | 4.45 | 4.49 | 4.49 | 4.79 | 4.99 | 5.19 |

| ICBC | 4.69 | 4.25 | 4.29 | 4.59 | 4.79 | 4.99 | 4.99 |

| |

4.99 | 4.49 | 4.49 | 4.65 | 4.85 | 4.99 | 4.99 |

| |

4.99 | 4.39 -0.10 |

4.75 | 4.49 | 4.89 | 5.19 | 5.39 |

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.