The Reserve Bank has slashed its house price projections for the rest of this year and is clearly baffled as to why actual prices have turned out so much weaker than it expected.

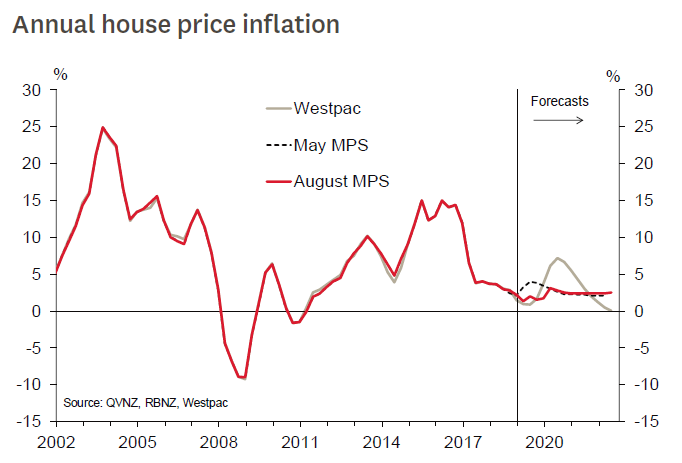

Meanwhile Westpac economists are going counter to this and suggest following the RBNZ's double-cut of the Official Cash Rate (from 1.5% to 1%) on Wednesday there's now upside risk to their pick that house price inflation will go to 7% in the next year.

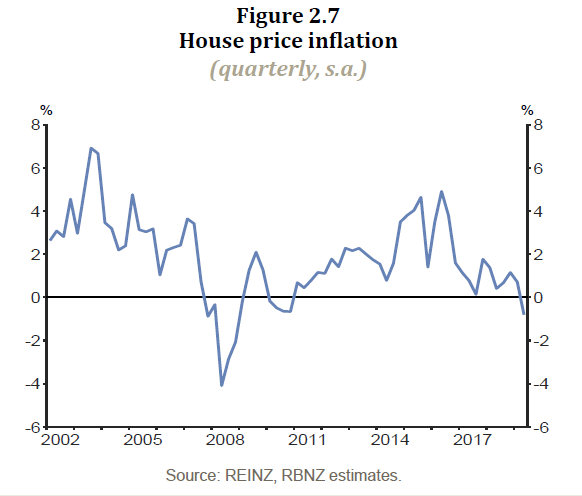

Whereas in May the RBNZ had been expecting the rate of house price inflation to virtually double this year and to reach an annual rate of 4% by September (although then falling after), the central bank is now predicting just 2% annual house price inflation by September, dropping further to 1.5% by the end of the year. It does pick a gradual acceleration in house price inflation to 3.1% by next year, but then falling again and being around 2.5% up to nearly the end of 2022.

The RBNZ has been sufficiently perplexed by the non-performance of house prices that it has even devoted a special section to house prices in its latest Monetary Policy statement.

In its May MPS the RBNZ has been expecting that NZ house prices would rise 0.9% in the June 2019 quarter. In reality the prices dropped by 0.8% in that same period.

"House prices are a key driver of household spending. Recently, house price inflation has been weak, influencing our forecasts for household consumption and residential investment," the RBNZ says.

It says house price inflation has been low despite falling mortgage interest rates in 2018 and early 2019 as lower "interest rates tend to support house prices by reducing the cost of financing home ownership".

"Given house price inflation was actually weak in early 2019, other factors must have had a dampening impact," the RBNZ says.

ASB chief economist Nick Tuffley comments that the RBNZ "appears a tad perplexed about why the housing market has remained so soggy".

He said ASB remains of the view that recent (and likely future) declines in mortgage rates will resuscitate the market.

"...But this is probably not going to show up in the data for another few months. Only in recent months has sales turnover started to recover."

Westpac chief economist Dominick Stephens says the fact that nationwide house prices fell in the June quarter seems to have "been particularly influential for the Reserve Bank".

He says he disagrees with the RBNZ’s conclusions on house price inflation.

"We were previously forecasting 7% house price inflation for next year, due to the sharp drop in fixed mortgage rates that has already occurred," he says.

Following the surprise big OCR cut from the RBNZ and the resulting market reaction, suggesting another round of reductions in fixed mortgage rates "the risk to our 7% house price forecast is now to the upside".

"The RBNZ is extrapolating from the recent house price weakness, but one quarter of negative house price inflation does not a downturn make," Stephens says.

"We have recently observed a pickup in seasonally adjusted house sales and a drop in houses available for sale.

"These are straws in the wind suggesting the market will pick up later this year. More generally, New Zealand is clearly in the grip of a search for yield environment. Banks are seeing slow growth in deposits as people shun the low interest rates on offer. Instead, fund managers are experience strong inflows of funds and share market prices are through the roof. We think it is only a matter of time before Kiwis turn their attention to houses in this environment.

"However, we doubt that signs of a housing market pickup will be clear enough by November to dissuade the RBNZ from cutting the OCR, especially if news on the export front has worsened by that time, as we expect it will."

Going back to the weaker than expected house price performance this year, the RBNZ says in its MPS document that tighter restrictions on non-resident purchases of residential property are likely to have suppressed house price inflation.

"However, ‘now or never’ purchases could have supported prices between the announcement and the final implementation of the restrictions in October 2018."

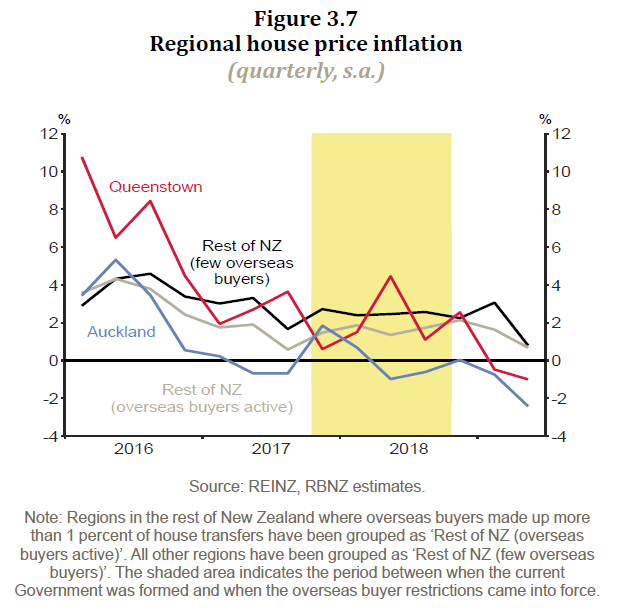

The RBNZ says house price inflation appears to have slowed more in regions that had greater non-resident buyer activity, like Auckland and Queenstown, "but the role of the restrictions in this is unclear".

"Moreover, house price inflation in regions that had low non-resident participation also slowed in the June quarter 2019. Having been in place for nine months, the transitional impact of the restrictions may have largely run its course. Slowing net immigration and strong house building may also be dampening house prices. Building does not appear to be outpacing population growth, consistent with recent elevated nationwide rent growth. However, current house prices should also be influenced by expectations of future demand and supply. Lower net immigration and strong building could be dampening expectations of future supply and demand pressures, weighing on current house prices."

The RBNZ says other factors will have also influenced the housing market. Government policies regarding rental properties may have contributed to subdued demand from property investors.

"Given that many of these policies were signalled some time ago, their impacts on prices may have already occurred. That said, the Government’s decision to not adopt a capital gains tax may provide a temporary boost to house price inflation in the second half of 2019, but we expect its impact on price growth will diminish after that."

Other potential influences on house prices include housing affordability constraints, which may have restrained house prices, and the easing of loan-to-value restrictions, which may have supported house price growth, the RBNZ says.

"Overall, we think lower mortgage rates, the diminishing impact of the foreign buyer ban, and the ruling out of the capital gains tax will outweigh strong building and declining net immigration, supporting prices through the rest of 2019. This is consistent with a recent pick-up in the number of house sales, which tends to lead prices by up to three months.

"Over the medium term, house price inflation is expected to remain relatively low as the support from lower mortgage rates fades. The subdued trend for house price inflation weighs on consumption and residential investment over the projection period."

168 Comments

A resurgence in house price inflation certainly can’t be ruled out - especially with the prospect of the OCR being cut further.....

TTP

Funny thing is it can't be ruled in either.....

With foreign buyers out of the picture, OCR cuts will provide little incentive for NZ residents to leverage themselves given wage growth has remained tepid for salaried individuals making above 60k a year (Stats NZ).

Don't expect the housing market to be hitting new records as long as the broader economy struggles to grow above population surge rate.

Also if the reserve bank has taken a drastic step of reducing by 0.5% - can Understand, how bad the ecenomy is and further down will be worst otherwise why will they jump with 0.5%.

Interesting from here another cut or two and than what..Deflation Ecenomy..............Will be worst than last GFC....................If it happens but such drastic measure indicates that reserve bank is expecting that ecenomy is leading to one direction...that is ..............and trying to infuse some life before it dies.

Does a cut in Interest Rates automatically translate to additional lending capacity? Or does the availability of credit not matter because banks just create credit from nothing? Capital Adequacy doesn't matter, the banks can just scratch every new mortgage up against the RBNZ. Borrow at 1%, clip the ticket at 3.75% easy as, it's a bottomless pit of 1's and 0's.

Please see my comments below

I'm a prospective first home buyer. An OCR cut from 1.5 to 1% does not signal to me that now is the time to buy (to the contrary), nor does it make a significant impact on my ability to service the astronomically large mortgage.

IMO, RBNZ will have to come up with something a little more hefty than a paltry 50 basis point drop to really stoke demand. Trouble is they have no more room to move. Orr is painting himself into a corner at an alarming rate.

In addition, what we don't know is whether the OCR drop will actually see Banks lower their serviceability criteria. It may make a loan easier to service but it doesn't mean that someone, who couldn't get a loan before, will actually be able to get one now.

yeah serviceability is critical. It doesn't matter how low interest rates go, if banks are cautious on lending to investors, FHBs etc

taking the p*ss ....do you ever read what you actually write ...have you ever thought WHY interest rates are going down ? have a think on that question, then see how it relates to what you said above ? You sound like some "stuffy"self-entitled, retired 68 yo commercial property lawyer from Remuera thinking that absolutely nothing will economically or financially change in the way things have been up to now.

Some people only look at one metric: median house prices in the last X years. They never look at metrics that indicate the 'health' of the market or the direction it's going. They think they are very wise until the elephant in the room wakes up and thrashes the house.

TPP, you have been consistently hinting that any change in market conditions could trigger house price inflation increasing, yet you have been consistently proven wrong. At what point do you think its time to start reassessing how you interpret the market?

I doubt he will ever concede, despite what the data and evidence suggests.

Exactly. When house prices go down (as they have been in the past few months), they will just say "now is the best time to buy, since they will soon go up again!". You can say that at -2%, -5%, -15%, -25%.... At one point, they will be right, house prices will go up again. Hmm... this reminds me of that saying about a broken clock. The one that has been mentioned many times on this site by certain commenters. Including TTP.

they will just say "now is the best time to buy, since they will soon go up again!". ... This is what they said in Perth when it had started to fall till it finally went down by 30% to 40% and still no buyers...................Slow fall due to low interest may be more damaging

The illusion of incremental drops and only focusing on a snapshot in time. "oh it's only 0.5% here, 0.7% there, just oscillations". "...wha.....what do you mean it's 20% in 2 years?"

Hi Miguel,

My view (for well over a year now) has been that the housing market would remain relatively flat and there would be no significant increase in prices until 2021 at the earliest.......

But, when I adopted this position I did not foresee the drop in interest rates that has transpired. Thus, I now believe there is a POSSIBILTY of a resurgence in house prices in the foreseeable future.

I note that this is also the view of some mainstream forecasters - such as Westpac Bank.

Happy to wait and see what happens.....

TTP

TTP ....you well and truly "just don't get it" ..... as you are highly likely to be a fan of Mike Hosking and his 'broad sweeping statements' to suit his "vested interests" ....HAPPY DAZE TO YOU

You can frame it in the context of a more general prediction of "I think the market will be flat until 2021", but then why do you consistently take any change in conditions to suggest prices will strengthen? It just seems that you are perhaps misinterpreting the upside prices in the Auckland market.

First it was the lowering of the LVR:

There's increasing speculation that the Reserve Bank will ease LVR's in the not-too-distant future. If so, the housing market will have a further stimulus heading into 2019....... TTP

www.interest.co.nz/property/96868/octobers-house-sales-volumes-155-vers…

And the OBB having no impact:

The evidence is solidifying....... The so-called Overseas Buyer Ban is not having the impact that a number of people here so enthusiastically anticipated. There has been no dramatic fall in sales volumes - and prices are holding firm. Steady as she goes...... TTP

www.interest.co.nz/property/97038/auction-sales-rate-slightly-lower-pro…

Then the CGT being taken off the table:

Hi Cowpat (my bovine friend), There may be a slight lift in Auckland house prices over winter...... First home buyers have become more active. Further, investor interest is picking up again, especially with the recent announcement by Govt re CGT kicked into touch. Happy house-hunting everyone - just a pity that new listings have drifted back. TTP

www.interest.co.nz/property/99471/sales-aucklands-largest-real-estate-a…

TTP does seem to oscillate a lot between saying things will be flat and then saying prices will rise. Hard to know where he stands really.

I think where he stands is on where he WANTS things to go, which is obviously up, but worst case flat (ie. not falling)

There has been speculation he is a mortgage broker. If he is, he might be very worried. I know two mortgage brokers who have totally changed career in the last few months, because of falling business and concern about where things are headed.

Hi Fritz,

You misquote me.

I said prices will remain "relatively flat". This means, obviously, that there will be some fluctuations - up and down - just as you might expect.

Or, in your words, there will be oscillations, which the main data series register on a month-to-month basis.

TTP

Haha.

The oscillation term is most definitely yours TTP.

Hence why every one uses it ironically when talking to you.

Hi Nymad,

Westpac and some other trading banks used the term "oscillation" including several mainstream forecasters (e.g. trading banks, NZIER) long before anyone else used here before.

TTP

"especially with the prospect of the OCR being cut further"

Lower OCR (even at 0%) meaning that economy is sick. In that sense good luck buying a house and raise a mortgage when your job prospect is also nearer to 0%..

yeah.

The other things is that in the 'good times', lots of bonuses are dished out while they start to die out during the hard times. You can't underestimate the bolstering effects of bonuses.

Please serious comments only.

TTP.

The magnitude of the cut this week would suggest that the debt based household credit Ponzi scheme that keeps NZ going is under pressure.

You are always quick to respond on these articles of ‘wonderful news for house buyers’ do you work for a bank?

Hi Tippeetee,

You're welcome to continue speculating on what I do for an occupation - to help fill in your days.

Others have suggested musician, astronaut, broker, financial advisor and various other occupations.

TTP

Here I was thinking you were a retired Hillman Motors Dealer.

As a Real estate Agent who analyses sales and speaks to vendors and buyers, perhaps I can help poor RBNZ. And perhaps they might like to give work to an Agent.....?

Buyers expect lower prices. This has been so for about 9 months in Auckland.

Agents need sales. So, about every few weeks they tell vendors that perhaps the price needs to come down.

THIS is what knocks prices down, NOT interest rate cuts.

Also, to Mr Stephens and his joke re seasonally adjusted pick up.

try looking at 12m trend, 6m trend, 3m trend and 1 month figures, compared to same 12m ago.

This will quickly show you that Auckland sales are down 25% and have been for the periods of 6m, 3m and 1m, for total sales. Buyer absence puts pressure on prices.

Wellington and Christchurch metrics on this measure are deteriorating and have been for 3-4 months now.

RBNZ listens to wrong people and believes theories.

Psychology and demographics, plus money velocity, governs house prices. Not interest rate cuts after those have lost their power because debt-return impact has dissipated.

interest rate cuts of 0.5% plus comment s attached to them will simply scare buyers further, who already have deflationary mindset. Economists have too much attachment to theory and don't ask people on the ground

It's is a religion after all....and that is the problem - dogma prevails and the most sane rational people don't think to question what they have been told or taught and that it may just be WRONG.

Ignorance is bliss!

Opiate for the people! House prices rise forever so we will all be happy!

Well put. Way too theoretical. AND there are problems with the theory.

From Dominick Stephens' comment The RBNZ is extrapolating from the recent house price weakness, but one quarter of negative house price inflation does not a downturn make (and others previously) it is pretty clear he has no idea what a time series forecast actually is.

He doesn't know what he is talking about and should be ignored

From Dominic Stephens

"We were previously forecasting 7% house price inflation for next year, due to the sharp drop in fixed mortgage rates that has already occurred," he says.

Following the surprise big OCR cut from the RBNZ and the resulting market reaction, suggesting another round of reductions in fixed mortgage rates "the risk to our 7% house price forecast is now to the upside".

His econometric model doesn't allow for the increase in the number of mortgagee sales that arise in an economic recession.

I could spend all afternoon demolishing his arguments, but sadly don't have the time

Plus you aren't getting paid for stating your opinion, unlike Dominick Stephens.

..yeah these guys beggar belief. Either completely bloody stupid or liars. .

Yes, in the Auckland residential real estate market, current active buyer price expectations have changed dramatically from those of 2016 / 2017 peak when prices were rising and FOMO was prevalent by active property buyers (both own-occupiers and non-owner occupiers such as property investors, property traders, small time property developers, etc), and fueled by the easy availability of bank credit. This led to fierce bidding at auctions. In 2016, active buyer price expectations were of continuing rising prices,

"QV says the average value of residential properties in Auckland declined for the eighth consecutive month in July, down from $1,050,647 in November last year to $1,025,389 in July this year. "

Given the recent property price falls in Auckland being reported in the mainstream media, active buyer price expectations are now of falling prices, and previously active buyers are now waiting on the sidelines, taking a wait and see approach, leading to fewer active buyers in the property market. The bank credit environment in 2019 is very different to that of early 2017, as banks have tightened up on applying bank serviceability criteria by:

1) verifying actual household expenses in some cases

2) applying discounts to rental property income (previously some banks did not apply any discounts),

3) collecting data on all other loans of a loan applicant and applying bank stress test interest rates to all of a loan applicant's existing borrowings (previously banks did not stress test the other existing loans from another bank of a loan applicant, as they did not have that information).

Also with the reported change in property price expectations in Auckland, some property owners (such as highly leveraged capital gain oriented property investors, highly leveraged negative cashflow property investors, leveraged property landbankers - those who bought a house with a large section looking to sell to a property developer, leveraged land speculators, etc) may choose to sell their property, thereby potentially increasing the number of properties listed for sale

"Wellington and Christchurch metrics on this measure are deteriorating and have been for 3-4 months now" not according to TM2. You are wrong there is plenty of profit to be made in CHCH.. You can ask him!

Mike Kirk, I would not like to be using you as my agent to sell anything!

I would doubt you will be in the industry much longer as you have no idea at all about the ChCh market.

Great post Mike.

Your last paragraph in particular was bang on - the insight on what governs house prices certainly, but the big one that should be bolded and highlighted is that "interest rate cut have lost their power because debt-return impact has dissipated".

Sure you'll pay less in repayments on your loan - but what exactly are you taking that loan out for and is it worth the risk(s)? For investors, on current metrics, not so much - there isn't much capital gain to be had, being a landlord is less and less attractive, stocks are volatile and subject to the whims of crazy people overseas.

Even if you're looking for a house to live in - FHB or in-market swapper, you've gotta be looking at the current state of affairs and thinking - hmm risky.

RBNZ ain't dropping the OCR because things are rosy and on the up and up - they're trying to buffer before a drop. Anyone buying today is on an express-train to negative-equity-ville with no stops in between - and yet thats EXACTLY what Orr wants everyone to do. It's irresponsible.

Interest rates are cut because it is a product people are not buying enough of, as far as banks are concerned.

Why not? Because they are more cautious than they were.

What does a cut of 0.5% tell them? To be more cautious.

Really, if you look at what people did in 2008-11 in response to lower interest rates you would see that it did not boost consumption, for 3 years. And those were much larger cuts, in % terms

It's not only that they are more cautious. Fewer can even afford to pay the crazy prices.

.. the Reverse Bwankers are unhappy that Kiwi house prices are " soggy " ... when we have amongst the highest house prices in the world , as a ratio of our incomes .... Wow ! . . can someone shoulder tap Adrian Orr : " oi , dude ... not everyone in NZ is on a $ 500 000 salary ... less than half of them ...quite a big bit less than that ."

our houses are wet and soggy too

If Japan taught us anything it is, at a certain point, people just won't borrow. No matter how cheap it is. Only two things remain. Accept defeat, or MAKE them borrow by causing them pain when they don't borrow.

For RBNZ and anyone else who might be reading: house prices will fall in Auckland up to and including 2021.

The fall from peak (median $900k) will be 25% to end up at $670k median.

Elsewhere, there will be delay in falls as sales have to fall 3-4 years before prices follow.

hence Wellington and Christchurch prices will continue rising for a bit and then get creased in 2020-21.

Never mind world recession and what effect coming China crackdown in HK will do to NZ prospects

I would think you are better off obtaining real estate listings than making 'look at me' predictions Mike Kirk.

Very one-eyed predictions if you can call them predictions more like wish lists. I wonder how you would react if ttp chipped in with a prediction of his own??

RBNZ would never read our contributions - they are 'above us'

Correction, if it happens, which seems is happening will be between 20% to 30% from the peak.

Not IF but by WHEN it will happen to be watched.

Agent 786786 says "...if....which seems...between...not if....by when"

Sums it up lol

Who will be willing to sell a property , particularly in Auckland given its stagnation, if prices are going to be 5-10 percent higher in a year .

Hilarious. Surprised? Geniuses, not....

"Given house price inflation was actually weak in early 2019, other factors must have had a dampening impact," the RBNZ says.

Oh my god, do they seriously not realise the highly inflated situation the market is in? Of course it’s not going to rise much more, without pumping it with a lot of sugar (which they are trying to do).

They are frankly embarrassing

How dare you?! They are EXPERTS!

ha ha.

Having worked in and around urban development for many years, and been in many hearings and court proceedings, it's clear to me that experts, who are meant to be objective and independent, frequently aren't, although they do their best to pretend to be....

And are remunerated handsomely, by the ultimate consumers, no matter what the actual Decisions are....

But they are wearing a suit and a tie to work to show that they are Highly Trained Professional Experts and they know everything better than you.

I suspect their analysis hasn't included the impact of Foreign Capital on the market. I'd guess the RBNZ relies largely on data provided by NZ banks on credit issued as that will be their most comprehensive data. The OBB has clearly had an impact, but focusing on that misses the foreign capital (and debt) being used by NZ residents.

Just looking at what is happening in similar markets around the pacific, in part due to China's capital controls, I suspect this may be the missing piece in the RBNZ's picture.

Indeed. they did not count money that was not borrowed here in 2014-17 and they still aren't so cannot see that its gone down and by how much.

As China is now pulling in its horns even more, expect worse to come

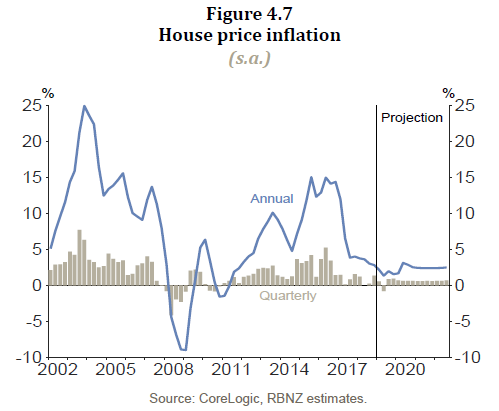

The last graph clearly shows that the 2012 - 2017 price appreciation was not "unprecedented" and that price appreciation in 2002 - 2007 was bigger

My take on the 2002-2007 spike is the Gubmint Stupidity in making 'Welcome Home' loans available to anyone who could fog a mirror, thus sending a Universal Pricing Signal to the entire nation that 'why should one price a cold leaky dump at X (it's reasonable price) when Da Gubmint will lend you Y (the WH Loan amount, where Y > X and by a considerable fraction). Explained in more detail with a real Christchurch example here.

there was a lot of high wealth immigration too.

Lots of poms came here in that period, with 1 pound providing 3 NZ dollars, and at the time NZ houses relatively cheap

There was also the effects of the dot.com bust, the Clark/Cullen tax increase and working for families which all stoked demand for investment properties. Early 2000's saw an increase in management companies promoting investment properties to baby boomers with equity. A tenant paying the mortgage and the tax benefit of negative gearing meant one could have a significantly larger sum of money in retirement than if they saved their own money.

I wonder too what effect 9/11 might have had. Such an existential event

It certainly encouraged more people (including kiwis coming back) to migrate to NZ. it might have had other impacts too in terms of investment

Because of the OCR cut and what it signals...

'Buyers are not buying as they expect interest rates/prices to come down more in the future.

Sellers are not selling as they expect house prices to increase in the future'.

(Meanwhile the economy is tanking in other areas and the currency is falling)

There you go, a stalemate..

A stalemate for now. Buyers are never forced to buy. Sellers on the other hand are sometimes forced to sell.

Sellers lives often can't be put on hold for ever.

My dad's best friend, aged 78, is looking to sell his house in Wellington, to move in to a retirement unit.

He's had his house on the market for months, he hasn't got the price he wanted or what he might have got 9 months ago. He's now ready to drop asking price, because he knows any day soon he could be a lot less able bodied.

He's prepared to get 5-10% less than he might have otherwise got. After all, he's still made a big gain over the last 25 years, and getting say 900k for his house rather than 970K isn't hugely material. But it's huge peace of mind for him to be able to secure the unit, and know he is in a safe and comfortable environment.

He'll get his nice one bedroom apartment for 570K, and have plenty left over to live on, even if he sells his house for 5-10% less.

No need for your fathers friend to sell his overpriced house bought mid nineties for a song. Rent it to ten ants and borrow at low mortgage interest rates for the retirement unit. Make use of rapidly escalating Wellington rents and Wellington housing shortage. Job done. Do not have to put life on hold and get depressed if overpriced home does not sell. There are multiple options

In short, speculate and become a landlord. Is that a good advice for someone who just wants to get out of the 'market', retire, and live the rest of his life in peace?

Being a landlord accidentally or otherwise is not everybody's idea however as fritz said the guy wants to move on. The suggestion to borrow against the house allows the owner to move on and gives an extra option he can consider without taking the vaunted firesale approach!

"the diminishing impact of the foreign buyer ban"

That impact won't diminish very quickly. All that housing stock bought by foreign buyers is going to take quite a while to be released back to the pool of local buyers.

https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

A dump on a steep, south facing site asking over $2 Mill… I think one of the most overpriced houses I've seen

Really not much different than the other cold windboxes of New Zealand. Anyone from the modern world would scoff at our stock.

Just look at the ANZ ad for healthy homes. It's a disgrace.

True but if you bowl this one down to rebuild, you still have a steep, south facing site

Reminds me of that scene in Jurassic Park

"Now that is one big pile of s**t"

When did we put all NZ's eggs in one basket and become a country that revolves around selling houses to each other for CG.

i sure many a small business owner, tourist operator or farmer are sitting there wondering why so much emphasis has been given to this one sector

was it becuase we had a banker in charge for nine years?

Banker? I'm sure that's a typo. Although 'w' isn't exactly close to 'b' on the keyboard...

When did we put all NZ's eggs in one basket and become a country that revolves around selling houses to each other for CG.

It was earlier also but was strongly supported by last National governemnt inviting foreign buyers/money launderers to turn housing market in NZ into Casino and most of them made heaps by selling their property as the people who started knew when it will burst and are now laughing all the way to the bank.

..I think it started earlier than this. Selling fish quota the start of the wealth stripping ( should have remained a govt asset). and it's just gone on and on and on.....

You know, I just want to get all these damned economists into one room and bang their heads together till they see sense. Houses are too expensive we do not need prices of them to rise, shutting more people out of owning their own home. Let's decommiditize housing, please, this is not their purpose.

Is "Let's decommiditize house, please" part of your 'rejig the economy' Plan? Of which plan, btw, you are yet to apprise us. Some of us are Posidively Agog with Anticipation.....

We never used to we can do it again. Work around housing, building, maintaining etc is a commodity and rightly so but existing housing being used the way it has been is not. Rejig your laws so that investors buying existing houses basically ceases to be a thing unless it is for redevelopment purposes not just sitting waiting for capital gain and farming people till it happens. Change tax laws to favor those who invest in proper businesses.

If you want to build a property portfolio then do just that, build it

True, governments used to be all about encouraging home ownership and access to it, not just about encouraging financialisation and portfolio enlargement.

You want a plan?

When the downturn really hits, put all those otherwise-unemployed tradies and all that free money to use with a massive programme of State house building. Build so many of them that no one will ever speak of a housing shortage again. Crash the rental market. The half of our population that currently rent will see a spectacular rise in real income and consumption will boom - because those people have real, unmet needs, unlike rental owners, who by definition have more than they need.

Exactly as I laid out a few years back. My extra topping on the desert would be to abolish every District Plan, fire all the Planners, and staff them Hoosing Factories with 'em.

Ah, we can dream.....

Yeah, it's pretty sad that they actually want house prices to go up further: "House prices are a key driver of household spending. Recently, house price inflation has been weak, influencing our forecasts for household consumption and residential investment," the RBNZ says.

Typical banker mentality. Gambling everything on houses. Tragic that RBNZ which is supposed to regulate the Banks, is joining forces with them, to screw the economy and the people. To hell with protection of customers and consumers.

Let's decommiditize housing, please, this is not their purpose.

Easier said than done. We're too far down the road so to speak. I think the powers that be would prefer any change in behavior and attitudes be left to natural forces; i.e., an economic event that is beyond their control and for which they're ultimately not responsible.

Furthermore, and RBNZ has clearly stated this, changes in house prices are instrumental in negatively / positively affecting the consumer economy. Chances are that substantial downward pressure on house prices would be terrible for the economy. The wealth effect is a lot more important than most people actually realize.

Not enough attention is paid to car sales data and also price / promotions data (from Nielsen). These are real barometers of what's going on. Stats NZ data for retail spending is good, but is rather broad and doesn't give you much insight into actual behavior. I would also think supermarket sales data is a treasure trove of what's going on.

Well spoken, JC. A lot of what's been said above amounts to hand-waving without the faintest notion of how economies actually work: by thousands of millions of individual transactions, across hundreds of thousands of commercial entities. And then expecting Fings to Change by Gubmints brandishing Wands straight outta J K Rowling.

To be sure, legislative and tax changes alter behaviours - because everyone, all the time, reacts in some way to their environment. No argument that tweaks or even major swerves might be needed. But Gubmint needs the consent of the Gubmined.....

And to expect any of that fundamental change to happen over a Parliamentary term, given the leads, lags, prior commitments, incumbent inertia, external shocks, unintended consequences and sheer human cussedness - is simply naive. It took almost two decades to get where we have gotten if one counts from Labour 2002, almost four decades if one counts from the 1984 Labour crew, and six plus decades if one counts from the 1958 Labour Black Budget. Plus ça change, plus c'est la même chose.....

double up

If someone is borrowing $600000 to $800000 (For $900000 Plus House) a slight fally in interest rate will be good as may save few $$ but from this low the borrowing is so high that little drop will be good but not life changing or will not change decession to buy or not to buy a house. Amount of Mortage that is borrowed is important and has to fall and that is possible only with fall in house price.

Mortage of $700000 is still a mortage of $700000 (Interest is historically low at 3.8% and may become 3.5% but still the BIG Mortage will not change unless bank start to give 10 years fixed at low price)

If the 5 year interst rate falls to 3% or below will defenitely make some impact but no so much on floating rate as most home buyers prefer fixed to floating.

Now from here, where.... Interest from 3.8% to 3.5% or 3.3% is good but than what.

Retired or all those who depends upon fixed deposit will to change to get more and may end up with bogus private finance company to maintain their lifestyle or will have to cut down on expenses and result will be less spending and people on crdit may be tempted to borrow more for low interest and the debt bubble will grow.

Intersting time ahead.

Lol... it's like they don't realise it's already unaffordable.

Exactly Lol

I totally agree with many comments here. I am presently discussing best options for my son as a FHB. He has more than enough deposit and his combined income with his partner would cover repayments. For the moment it makes more sense to continue renting as it is cheaper than paying off a mortgage (just) and with the forecast of lower house prices he will just wait. Young people under stand the "millstone" that they will be saddled with until retirement in many instances and won't be lulled into buying by the low interest rates presently. A big driver of FHBs was the "fear of missing out" when prices were rising but that has gone now.

There are buyers who purchased in 2016/2017 in Auckland based on "fear of missing out". Due to market price falls, some are starting to regret that decision. There will very likely be an increasing number of these stories in Auckland.

Here is a story from Milkyone:

"Interestingly I have another firend who bought an aprtment off the plans 18 months ago in Auckland. Still under construction after delays. He is painfully aware that he subsequently could have bought better apartments elsewhere for the same amount, and that his small deposit has basically vanished in terms of equity reduction. He is essentially stuck in this property until

A - he raises another deposit

B - the rising market brings his apartment value back up to where he bought it

Oh well you might say, he can just wait. Sure, but what if his circumstances change? Yikes.

And of course that leaves aside the fact that if he had just waitied, he would have got a much nicer apartment for the same amount."

"The guys a property lawyer, which is good as he will avoid any of those pitfalls, but does beg the question of how he got himself in such a situation to start with...

At one point they hit some issue with the bedrock they hadn't anticipated. He was desperately hoping they were going to pull the plug entirely, as his deposit was protected. No such luck.

Just another victim of the FOMO mentality."

https://www.interest.co.nz/property/100979/new-listings-hit-record-low-…?

Few spelling mistakes in that one wasn't there...

Tauranga sales last month have literally fallen off a cliff. After speaking to a few agents they tell me that they are just not seeing any new buyers coming onto the market. This is very bad news for all of the new developments currently in progress over in Papamoa. The developers, being so greedy, have cut section sizes down to 300 and 400m2 max and they are asking 400k for them? They were selling a year or two ago but not any more. This is going to get very messy for some people. The thing is it is a worldwide phenomenon. There is no stopping this death spiral whatever RBNZ tries to do. The greed game is finally up!

agree. Trouble brewing for the big new developments, in Auckland, Tauranga...

The developers are going to have to cut their losses

Or lenders will call in receivers.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

This was for a completed project which was unable to sell their completed units.

Wait until you get unfinished developments where the project funding dries up, and those buyers become unsecured creditors, and potentially lose their deposits. Also contractors, subcontractors, and tradies don't get paid and become unsecured creditors, leading to potential liquidity problems for those businesses and some start going bankrupt, and then there are the unemployed staff from these businesses. Construction labour goes from shortage becomes excess supply, and labour is willing to work at lower prices due to supply competition.

When unfinished developments start defaulting, then that leaves less funds to finance other new projects.

Mikekirk29 talked about the development funding cycle.

All part of the property development cycle.

Spot on. This is next phase

Prepare for the 2020 Tradie Wash-Out.

Yes, wash them out indeed.

https://www.youtube.com/watch?v=XlINJ8mU6b0

less dickheads tearing around my suburb like maniacs in their Ford Ranger, that would be nice

yeah.

People with short memories forget some of the issues in the past. The late 80s, the mid to late 70s.

When I was growing up in Wellington in the late 70s a house remained half built for about 5 years on the property next to my parents house, off the back of the economic hard times in those days.

It was like a bombed out house, my brother and I used to play 'Commando' through its multiple levels. Great fun

Every new generation of people entering the workforce generally has no experience of market price crashes. How many of the current generation entering the workforce today know about the 1970's, and the stock market crash of 1987? Very few, and almost none know of sufficient detail of the causes (unless they studied these).

So as a result of a lack of interest in financial history, and a lack of personal experience of market price crashes, each new generation of people entering the workforce tends to learn via first hand experience, the same lessons learned from history. That is why these market crashes repeat themselves. Different market participants, same lessons.

For example:

1) Internet coin offering price crashes

2) Internet bubble in early 2000's

3) Property bubbles in 2008/2009 in US, Ireland, Spain.

Due to their personal experience, those who experienced the 1987 stockmarket crash, likely avoided the internet bubble or the Bitcoin crash.

It is also why the next generation take on large amounts of debt, as they have not learned from previous people who went bankrupt (such as the 2008/2009 GFC, 1987 stock market crash, etc). After 10 years or so, the next generation gets the opportunity to learn their lesson firsthand.

Credit bubbles take a long time to build up, the last one in NZ was in late 1980's in commercial real estate (when BNZ had to be recapitalised). It was even longer for the last residential real estate price fall (in nominal terms) - they fell in real inflation adjusted price terms in the 1970's when inflation was high. So the next generation gets their opportunity to learn the lesson firsthand.

"Those who fail to learn the lessons from history are doomed to repeat them"

Yep. I was young and naive in 07. Never studied economic history and thought the good times could go on forever. Then we had the collapse of mezzanine finance followed by the GFC.

I learnt a lot, especially about the importance of diversity, not only in investments but also in terms of personal skillsets.

When starting out, everyone is inexperienced. The question is how quickly do people realise that they are inexperienced / ignorant, how quickly do they choose to get wise, and do they learn the correct lessons of history.

Many times people have to challenge their existing beliefs & unlearn the incorrect lesson / belief that they previously learnt - that is the most difficult part.

For example, previously I extrapolated long term median historical house prices in Auckland to develop future longer term price expectations (this is a very common approach by many property investors to determine their future property price expectations). Subsequently questioned whether that approach was correct, and then unlearnt that approach and now use a different methodology to determine future house price expectations, and expected returns.

That revised methodology led to exiting the residential real estate leasing business in Auckland in early 2017. Had I continued to use the previous methodology, most likely would still be in the residential real estate leasing business in Auckland.

Another belief unlearned is that underlying supply and underlying demand do not determine property prices in the free market, it is effective supply and effective demand that determines property prices in the free market. If you looked at other markets with property price crashes, the common repeated phrase in the run up of rising prices was of a housing shortage (based on underlying supply and underlying demand) and population growth, yet property prices subsequently fell substantially in Ireland, US and Spain.

Many property investors are extrapolating historical property price changes into the future. Historically prices have increased 9.9% per annum since 1965. Many property investors believe that prices will continue to double every 10 years. Is this price increase sustainable?

Let's assume that there is no hyperinflation in NZ, like Germany experienced in the 1930's, Zimbabwe experienced in 2000's, and the current situation in Venezuela. For hyperinflation to occur in New Zealand, would mean for the RBNZ to abandon it's 1-3% inflation target, and focus on different macro-economic metrics - that seems like a low probability scenario given the current environment & legislation in New Zealand.

So with a low inflation economic backdrop, let's assume property prices in Auckland double every 10 years (that means house prices grow at 7.2% per annum). Let's extrapolate what house prices have done in the past 52 years, and extend that into the future - what does the future look like for Auckland house prices?

(Here are some of the other underlying assumptions - rents in Auckland grow 5% per year, household incomes in Auckland grow 3% per year)

You can pick at which point that Auckland house prices might start to seem a little ridiculous to you.

In the year 2019 (today) -

Median house price in Auckland - $0.850mn

Median gross rental yields in Auckland 3.51%

Price to rent ratio 28.5x

Median house price to median household income ratio 8.9x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 1.8x

Equity deposit of 20% required to buy: $0.17mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 41.3%

Median rent cost for renters as % of median household income 31.3%

In the year 2029 (10 years from today) -

Median house price in Auckland - $1.7mn

Median gross rental yields in Auckland 2.86%

Price to rent ratio 35.0x

Median house price to median household income ratio 13.3x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 2.7x

Equity deposit of 20% required to buy: $0.34mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 61.5%

Median rent cost for renters as % of median household income 38.0%

In the year 2039 (20 years from today) -

Median house price in Auckland - $3.4mn

Median gross rental yields in Auckland 2.33%

Price to rent ratio 43.0x

Median house price to median household income ratio 19.8x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 4.0x

Equity deposit of 20% required to buy: $0.68mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 91.5%

Median rent cost for renters as % of median household income 46.0%

In the year 2049 (30 years from today) -

Median house price in Auckland - $6.8mn

Median gross rental yields in Auckland 1.89%

Price to rent ratio 52.8x

Median house price to median household income ratio 29.4x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 5.9x

Equity deposit of 20% required to buy: $1.36mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 136.2% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 55.8%

In the year 2059 (40 years from today) -

Median house price in Auckland - $13.6mn

Median gross rental yields in Auckland 1.54%

Price to rent ratio 64.8x

Median house price to median household income ratio 43.8x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 8.8x

Equity deposit of 20% required to buy: $2.7mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 202.7% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 67.6%

In the year 2069 (50 years from today) -

Median house price in Auckland - $27.2mn

Median gross rental yields in Auckland 1.26%

Price to rent ratio 79.6x

Median house price to median household income ratio: 65.2x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 13.0x

Equity deposit of 20% required to buy: $5.4mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 301.7% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income: 82.0%

In the year 2079 (60 years from today) -

Median house price in Auckland - $54.4mn

Median gross rental yields in Auckland 1.02%

Price to rent ratio 97.7x

Median house price to median household income ratio 97.1x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 19.4x

Equity deposit of 20% required to buy: $10.88mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 449.0% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 99.3%

In the year 2089 (70 years from today) -

Median house price in Auckland - $108.8mn

Median gross rental yields in Auckland 0.83%

Price to rent ratio 120.0x

Median house price to median household income ratio 144.4x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 28.9x

Equity deposit of 20% required to buy: $21.7mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 668.2% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 120.4% (renters have to pay more than their entire household income to rent a house as accommodation)

In the year 2099 (80 years from today) -

Median house price in Auckland - $217.6mn

Median gross rental yields in Auckland 0.68%

Price to rent ratio 147.3x

Median house price to median household income ratio 215.0x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 43.0x

Equity deposit of 20% required to buy: $43.5mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 994.5% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 145.9% (renters have to pay more than their entire household income to rent a house as accommodation)

In the year 2109 (90 years from today) -

Median house price in Auckland - $435.2mn

Median gross rental yields in Auckland 0.55%

Price to rent ratio 180.8x

Median house price to median household income ratio 319.9x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 64.0x

Equity deposit of 20% required to buy: $87.0mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 1479.9% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 176.9% (renters have to pay more than their entire household income to rent a house as accommodation)

In the year 2119 (100 years from today) -

Median house price in Auckland - $870.4mn

Median gross rental yields in Auckland 0.45%

Price to rent ratio 222.0x

Median house price to median household income ratio 476.1x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 95.2x

Equity deposit of 20% required to buy: $174.1mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 2202.4% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 214.4% (renters have to pay more than their entire household income to rent a house as accommodation)

So by the year 2099, owner occupier buyers have to save 43.0 years of gross household income (i.e before tax and any expenses) in order to be able put down a 20% deposit to buy a house.

Remember, that 43.0 years is almost the entire working life of an individual from age 20 to 65 - so they can afford to put down a deposit to buy a house when they are 63.0 years of age (assuming they haven't spent any money for taxes or food or rent for 43.0 years of course).

Remember when banks assess loans and debt serviceability, historically they allowed 36% of gross household income as total debt payments (mortgage payments, credit cards, auto loans, personal loans, etc). The typically allow no more than 28% of gross household income for mortgage payments. As at 2019 current median household price and median household income, that ratio for mortgage payments to median gross household income is 41.3% (using a 30 year P&I mortgage at 4.0% interest).

If you're interested in Tauranga development pipeline, this is a good read, Veros report starting Pg 55.

http://econtent.tauranga.govt.nz/data/bigfiles/committee_meetings/2019/…

"The analysis validates a serious shortfall in development capacity and a constrained supply."

https://www.tauranga.govt.nz/Portals/0/data/council/reports/population_…

If you look at their projection for the required number of dwellings, the underlying assumptions in the future for residents per dwelling are very different to actual levels (refer table 5).

1) in 2013, the residents per dwelling is 2.61

2) in 2063, the residents per dwelling is 2.18

So as a result, from 2013 to 2063:

1) population is expected to grow 66%

2) number of dwellings to grow 98%

Note that these numbers do not make any changes for property prices and consideration whether property prices are affordable or not. If the median house price to income is unaffordable (say 20x), then a large number of those properties may be unaffordable, and many developers may not build as they are unable to sell their developments at those market prices.

105 pages, and it's just the agenda - good grief..

Have these very smart people ever *considered* the possibility that our housing is, simply, massively overpriced?

That when something is massively overpriced it doesn't make sense to buy it? Even if you could get credit to do so?

I suspect that their models are based on expectations of rational behaviour; and thus the possibility that current prices are already far above what is sustainable doesn't figure, because the market 'never would have allowed that to happen...'

'Have these very smart people ever *considered* the possibility that our housing is, simply, massively overpriced?'

You just nailed it.

"Have these very smart people ever *considered* the possibility that our housing is, simply, massively overpriced?"

There was this other very smart person who said "if someone can afford it, it's clearly affordable".

The very smart people are likely to be looking at the reported housing shortage in Auckland and as a result believe that property prices will not fall due to continued strong demand.

Look at the economist at the Auckland City Council - https://www.interest.co.nz/opinion/100853/david-norman-says-auckland-ho…

Having said that, the RBNZ has stress tested bank balance sheets for a 35% property price fall - if there is a 35% fall, let's hope that they're accurate.

well they aren't really that smart are they

That's what it comes down to, isn't it?

All the endless arguments on these very pages.

"It's supply and demand!" vs. "It's an irrational, credit-fuelled bubble!"

I'm firmly in the second camp. Their idea of 'demand' doesn't include people's ability to pay, for some reason. The nice thing is, we will actually find out soon enough.

This.

(Out of vogue now right?)

Talking of surprises, didn't the RBNZ have a 'no surprises' ( to the market ) policy ?

Yesterdays cut would seem to qualify as such.

I could have made a lot of $ in forex if they had only let me in on the secret plan!

Oh for goodness sake ..........how on earth cane the RBNZ not have expected this ? .... the Government has done everything to ensure there is little or no house -price increases .

Effectively removing investors from the market through taxes , ring-fencing , and all manner of heating requirements

Stemming immigration as best they can

Making Asian investors feel about as welcome as a Pork sausage at a Barmitzvah

And then promising everyone a Kiwibuild -almost- for - free- house

Sounds like you're saying the government has been successful at improving affordability of home ownership for New Zealanders. And now the Reserve Bank is working directly against this, as if affordable home ownership is not to be allowed!

But think of the children!

Sorry, I mean bank profits!

RBNZ: Attack!

Half soldiers gone like a sprinkle

And soon vanished in the dark

Few come back with a sluggish eye

They hear the stunning sound says

"Give my money back"

You what?

It probably rhymed in Mandarin....I blame Google Translate....

Sounds like its straight from the RBNZ code book

If you are holding off selling an investment property because you think house prices will go up again then you better be prepared to wait at least 30 years. This bubble has ruined every norm that has preceded due to John Keys foreign money scam. The worlds economy is decaying and nobody has an answer. I promise you this is going to be very painful. The coming recession will make the GFC look like a blip.

yeah.

The smart ones got out 6-12 months ago, but it's not too late to count your losses.

Note: this doesn't apply to all property investors, only the highly leveraged ones who bought in the last few years, with poor yield and largely on the basis of big capital gains.

The Chinese buyers desperate to get their money out of China inflated the house prices in Auckland between 2012 and 2016. Local investors unable to outbid them instead inflated the provincial market.

The Chinese govt stopped the outflow and our govt put the foreign buyer ban in place.

And if that wasn’t enough losses on rentals got ring fenced, even more regulations were put on landlords and there’s currently apartments and houses under construction all across Auckland.

It’s the perfect storm now with prospective buyers who kept their powder dry waiting for the prices of houses (tulips) to fall.

And they will fall big time either quickly or by a thousand cuts over the next 10 years.

I am sure glad I am not an agent.

And the real estate agent is sure glad that they are not a property developer with a large apartment development project in progress, project financing drying up and buyers choosing not to settle ...

"there’s currently apartments and houses under construction all across Auckland."

Even if all these apartments under construction have all been pre-sold, there are likely to be buyers who are unable to settle at completion for various reasons (such as financing - refer the student speculator story https://www.news.com.au/finance/real-estate/buying/mum-sold-me-a-unit-i…).

In a rising price market, property developers could resell these on the secondary market. With current price expectations by many buyers in Auckland, there will be few buyers and many will remain unsold for a period of time. (FYI, 18% of the units of this project are unsold, some have been listed for sale since December 2018 - https://www.trademe.co.nz/Browse/CategoryAttributeSearchResults.aspx?se…)

If a sufficiently large number of properties sold do not settle, this will leave developers potentially short of cash (as the cash proceeds that they expected upon settlement fail to materialise).

Construction loans need to be repaid and they may be unable to be refinanced. So lenders move in and appoint receivers ...

(refer above comment for what happens after lenders appoint receivers)

Yet the Auckland council and many other economists (as well as the property promoters) state that there is a underlying shortage of housing in Auckland, and property prices will not fall by much - https://www.interest.co.nz/opinion/100853/david-norman-says-auckland-ho…

The Reserve Bank has slashed its house price projections for the rest of this year and is clearly baffled as to why actual prices have turned out so much weaker than it expected.

The whole world has an interest rate problem – starting with the fact everyone still calls lower rates stimulus. Eurodollar futures aren’t suggesting a high probability of renewed ZIRP because of some convoluted R* theory (which conveniently would absolve monetary policymakers of twelve years of failure and incompetence). Investors are betting on constant liquidity risk, or the same thing which is driving European bond yields further and further underground.

Global interest rates, global money. Take it from here Milton Friedman:

After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die. Link

Its pretty whacky that the RBNZ isn't able to model the impact of foreign buyers on domestic house prices nor it seems model the secondary effects of the FBB/OBB such as the death of the buy and flip trade.

This nonsense of 7% house price appreciation needs to be called out. Try 10% property price drops per annum for 3 years. If wages are growing at less than 2% p.a. how the fk do they think asset prices are going to miss on the upside ? Its just utter B.S.

It certainly does need to be called out. It's noted too that Zorro has come out with some clangers in the past few years.

If, as many of us suspect, he is very wrong, he really needs to be called out on that, this time next year. Put it in your diaries.

Because, many people (including potential FHBs) respect his opinion given his title as chief economist working for a mainstream bank.

What if a FHB buys, partly on the basis of his 7% rise prediction, and their property falls 10% in the next 2 years???

now you can say 'buyer beware' and all that, but he's in a position of authority and trust

That is the reason for many commenters on here offering a different opinion, backed by quantitative data and market observations, to counter the financial vested interests of those promoting property market activity such as real estate agents, property developers, property promoters, bank economists promoting bank lending, mortgage brokers promoting bank lending, etc.

All in order for first home buyers and owner occupiers to make more fully informed decisions, and avoid being collateral damage and losing their hard earned deposits.

yeah exactly.

'to counter the financial vested interests of those promoting property market activity such as real estate agents, property developers, property promoters, bank economists promoting bank lending, mortgage brokers promoting bank lending, etc.'

Add - media outlets beholden to real estate advertising revenue.

We provide a rare counterpoint to the property spruiking BS that proliferates in the media.

Hard to know how many people might take in what we say, but say it we will.

"Hard to know how many people might take in what we say, but say it we will."

There have been comments on this site by a few potential first home buyers who have delayed purchasing. If even one of those avoided losing a large percentage of their equity deposit, then that is worthwhile. (Also, I recall Carlos67 saying he sold his house in Auckland, and that the value of that property is now less than when he sold it)

FYI, it is interesting to note one reason made by the property bulls to ignore the warnings regarding property prices in Auckland (and how they got to current price levels):

"The DGM have been pronouncing that we are about to experience large falls in house prices for well over a decade....... The issue is that these imminent large falls have never transpired."

The warnings were ignored when property prices kept rising in Auckland and there was FOMO, but now that they have started flattening out / falling, and that these are being reported in the mainstream media, and the changed property price expectations by more and more of the public, the warnings are being given more consideration.

Also in light of recent property price falls in Auckland, some are beginning to question their existing internal framework and understanding on how property prices work. Here is a comment from a mortgage broker:

"Maybe it's just me but I don't get it. We have a national shortage of over 100,000 homes. We have low unemployment. We have steady immigration inflow and low interest rates which will not rise dramatically anytime soon. What am I missing?"

One of the main reasons I post here is because one of my biggest hates in life is BS spun by parties full of vested interest. Really can't stand it

I'm a FHB, who found this site maybe 6 months ago. I was already inclined to wait, but the intellegent analysis by many of this sites commentators had a reasonable part to play in strengthening my resolve. As well as providing the ammunition I need to convince my fiancee that waiting is the right thing to do.

If you all turn out to be correct, you will have my gratitude.

cool

even if we aren't correct, I'd be very confident that any upswing in prices will be very mild

Agree with Milkyone and sounds like we're in the same position..I'm a FHB, who now reads this site daily to stay informed about the reality of current market conditions. The commentary and array of perspective/insight on this site v.s. mainstream media & other commentators with vested interests, has helped us hone in on what to research to validate our decision to wait for the time being.....coupled with the fact that RBNZ announcement won't have a major impact on the number of AFFORDABLE properties on the market, regardless of how much we can borrow/interest rates.

...long time reader; first time commenter, rest assured your commentary is valued and read/liked!

It goes well beyond the irresponsibility of Bank Economists as it’s endemic across our mainstream media.

It was revealed that in Ireland the media played a huge role in the housing bubble. When you read about why went on there it is clear the same conflicts of interest are at play in New Zealand.

https://www.tandfonline.com/doi/abs/10.1080/13563467.2013.779652

What is there to be perplexed about? Couldn't be house price to income ratio could it? There comes a point when you look at houses and go '800k for a 3 bedroom rundown shack? Yeah nah'.

Brian Fallow has a good looking critical piece in the Herald behind paywall on the OCR decision. Will read the hard copy tomorrow.

Fallow is one of the very few journos at the Herald I rate. Most are lightweights.

I guess it is hard to accept the party is over when you're having fun but eventually you have to accept you have to go home.

Seriously, many of you just prattle on about house prices dropping as if you know what you are talking about!

Reality is that prices around the country are not generally dropping at all, it is mainly an Auckland thing, and anyone that knows about property would know at some stage the Auckland market would flatten and drop a bit.

This has happened now due to several factors including the fact that wages in Auckland are not much if any any higher than other places in NZ.

I can confirm that ChCh market is as stable as any other area in NZ and prices will be increasing due to the desirability and unbeatable good value that it offers.

The thing is that personally we have more than enough properties and there are still opportunities that we may well look at.

What the intelligent buyers are currently doing is exactly what many of you are not doing and I can guarantee that if they buy well now, they will be years of head of the ones that are sitting on the sidelines.

Interest rates are great, affordability is as good as it will be in most places in NZ, so just do it!!!

Seriously many of you just try to convince FHB now that investors are gone, good try.

Unusually gloomy perspectve from the RBNZ which is concerning by itself!

Some of these other economists need to learn some Math. You cant keep expecting house prices to double ever 10 years while wages increase by 25% over the same time and expect that pattern to continue infinitely...

Its pretty obvious after the foreign money has left Akld that prices would drop. OCR cuts dont help save for a deposit.

You can expect the clowns at the RBNZ to lower the LVRs next when this OCR cut fails

MilkyOne, good that you found this site 6 months ago.

You read and take notice from many on here that are telling you not to buy at the moment!

However, the very same ones were saying this 10 years ago and they were blatantly wrong for all of that time.

What I would suggest if you have a sufficient deposit at the moment is consider buying if you see the right property and is in your price range, because if you like it, then others probably will as well.

You are far better off living in your own home than in a rental property for several reasons.

I love seeing our tenants buy their own home as it is the only way they are going to get ahead financially in life

MilkyOne can and will decide for himself / herself, after weighing up the very different views.

No one can predict with certainty what will happen next, even though some of you think your views are bullet proof.

Comparing predictions of today to those of 10 years ago - irrelevant. The circumstance are totally different today to 10 years ago.

Having said all that ,yes there will be times when buying now makes sense for some people.

Many property investors are extrapolating historical property price changes into the future. Historically prices have increased 9.9% per annum since 1965. Many property investors believe that prices will continue to double every 10 years. Is this price increase sustainable?

Let's assume that there is no hyperinflation in NZ, like Germany experienced in the 1930's, Zimbabwe experienced in 2000's, and the current situation in Venezuela. For hyperinflation to occur in New Zealand, would mean for the RBNZ to abandon it's 1-3% inflation target, and focus on different macro-economic metrics - that seems like a low probability scenario given the current environment & legislation in New Zealand.

So with a low inflation economic backdrop, let's assume property prices in Auckland double every 10 years (that means house prices grow at 7.2% per annum). Let's extrapolate what house prices have done in the past 52 years, and extend that into the future - what does the future look like for Auckland house prices?

(Here are some of the other underlying assumptions - rents in Auckland grow 5% per year, household incomes in Auckland grow 3% per year)

You can pick at which point that Auckland house prices might start to seem a little ridiculous to you.

In the year 2019 (today) -

Median house price in Auckland - $0.850mn

Median gross rental yields in Auckland 3.51%

Price to rent ratio 28.5x

Median house price to median household income ratio 8.9x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 1.8x

Equity deposit of 20% required to buy: $0.17mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 41.3%

Median rent cost for renters as % of median household income 31.3%

In the year 2029 (10 years from today) -

Median house price in Auckland - $1.7mn

Median gross rental yields in Auckland 2.86%

Price to rent ratio 35.0x

Median house price to median household income ratio 13.3x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 2.7x

Equity deposit of 20% required to buy: $0.34mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 61.5%

Median rent cost for renters as % of median household income 38.0%

In the year 2039 (20 years from today) -

Median house price in Auckland - $3.4mn

Median gross rental yields in Auckland 2.33%

Price to rent ratio 43.0x

Median house price to median household income ratio 19.8x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 4.0x

Equity deposit of 20% required to buy: $0.68mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 91.5%

Median rent cost for renters as % of median household income 46.0%

In the year 2049 (30 years from today) -

Median house price in Auckland - $6.8mn

Median gross rental yields in Auckland 1.89%

Price to rent ratio 52.8x

Median house price to median household income ratio 29.4x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 5.9x

Equity deposit of 20% required to buy: $1.36mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 136.2% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 55.8%

In the year 2059 (40 years from today) -

Median house price in Auckland - $13.6mn

Median gross rental yields in Auckland 1.54%

Price to rent ratio 64.8x

Median house price to median household income ratio 43.8x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 8.8x

Equity deposit of 20% required to buy: $2.7mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 202.7% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 67.6%

In the year 2069 (50 years from today) -

Median house price in Auckland - $27.2mn

Median gross rental yields in Auckland 1.26%

Price to rent ratio 79.6x

Median house price to median household income ratio: 65.2x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 13.0x

Equity deposit of 20% required to buy: $5.4mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 301.7% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income: 82.0%

In the year 2079 (60 years from today) -

Median house price in Auckland - $54.4mn

Median gross rental yields in Auckland 1.02%

Price to rent ratio 97.7x

Median house price to median household income ratio 97.1x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 19.4x

Equity deposit of 20% required to buy: $10.88mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 449.0% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 99.3%

In the year 2089 (70 years from today) -

Median house price in Auckland - $108.8mn

Median gross rental yields in Auckland 0.83%

Price to rent ratio 120.0x

Median house price to median household income ratio 144.4x (purchase cost for owner occupiers)

Equity deposit of 20% required (multiple of median annual gross household income to be saved as deposit): 28.9x

Equity deposit of 20% required to buy: $21.7mn

P&I mortgage pmt (@ 4% int rate, 30 years) as % of median household income: 668.2% (i.e have to pay more than entire median household income as mortgage payment)

Median rent cost for renters as % of median household income 120.4% (renters have to pay more than their entire household income to rent a house as accommodation)

In the year 2099 (80 years from today) -

Median house price in Auckland - $217.6mn

Median gross rental yields in Auckland 0.68%