A much more severe shortage of housing than earlier thought is one of the key reasons for New Zealand's super hot housing market, according to ASB economists. And they say house price inflation of around double-digits will prevail for the first half of next year.

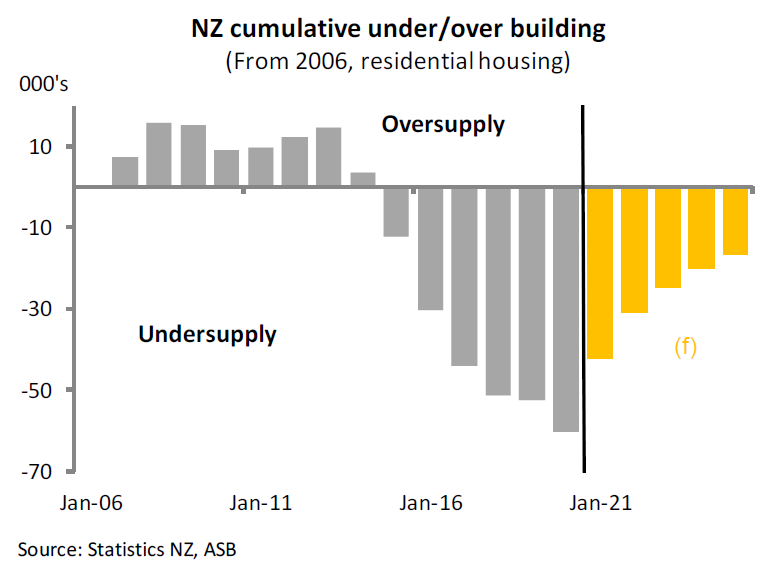

In an ASB Home Economics publication, following release of red-hot September housing figures by REINZ on Tuesday, ASB senior economist Mike Jones now pegs the shortage of houses in this country, due to our "longrunning residential construction under-build" at between 60,000 and 65,000.

He says that is "around twice what was previously assumed".

"Getting a precise estimate on this sort of stuff is impossible due to data quality issues. But our larger housing shortage estimates reconcile more readily with the sheer strength in housing activity and prices we’re witnessing now," he says.

All of the economic stimulus that has been provided this year, much of it "either directed at, or found its way into, the housing market" has "simply exacerbated" the position of excess demand and the tightness of the market that is now evident, Jones says.

"In short, there’s a scramble for houses."

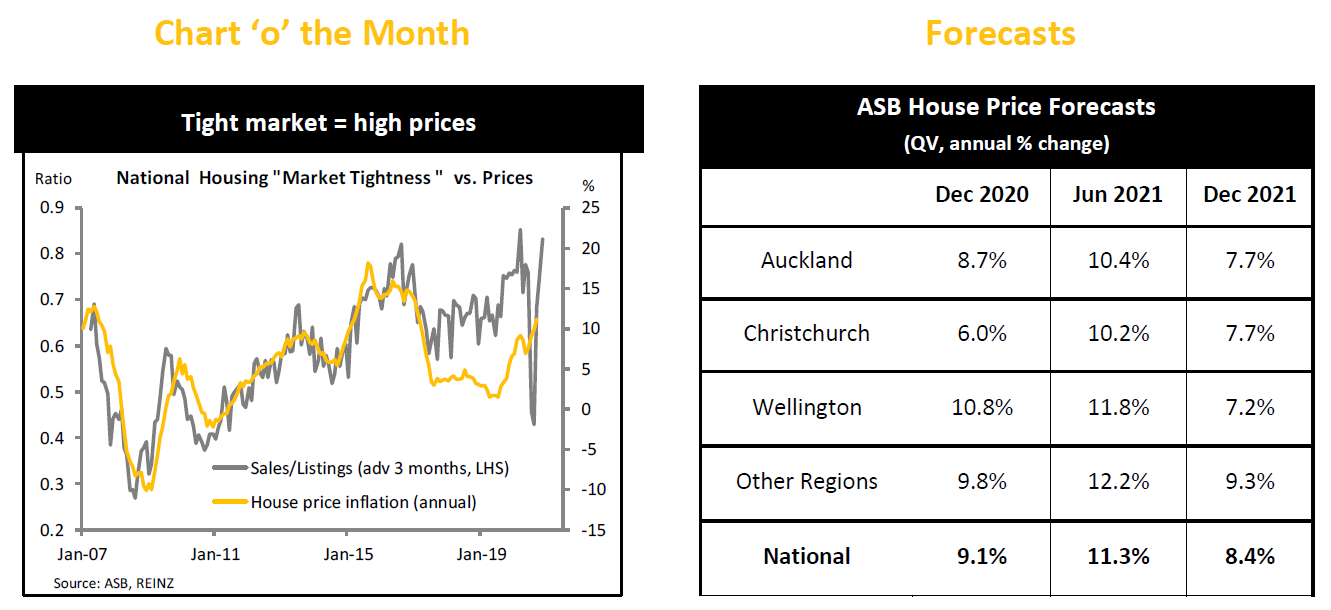

ASB economists have "materially upgraded" their house price forecasts.

They now expect annual house price inflation of 9% by year end, and "have flipped the small negative we had in for June 2021" to an 11% positive annual increase.

"...With the labour market outlook now looking much less gloomy and the RBNZ seemingly actively egging the market on, we think house price inflation will hold up at near double-digit growth rates at least through the first half of 2021," Jones says.

Flat-lining net migration and some roll-back of policy support will "slow rather than stall" the market next year, he believes.

ASB's Jones notes that measures of housing inventory are now "back down to outrageously low levels".

"For example, September figures from realestate.co.nz show national listings close to the lowest level on record, equivalent to just 12 weeks’ worth of sales. The long-run average is 28 weeks’ worth."

Jones says it is worth noting that NZ’s recent experience in all of this is not unique.

"Most of the developed world has experienced surprise housing strength in the face of Covid’s various challenges. As The Economist notes, house prices rose in eight out of 10 high and middle-income countries during lockdown. And most of these countries are suffering noticeably worse health and economic conditions than NZ."

Jones acknowledges the longer-term outlook "remains murky", but at least in the short term "it appears there is plenty of fuel in the market’s tank".

65 Comments

Housing in NZ = debacle.

The only way it will stop is IF we can get some really good unemployment numbers March onwards when mortgage holidays come to an end.

IF we get this these clever bankers may change strategy when they stop getting principal payments back as negative interest rates wont help.

Sounds very negative but I prefer that we have a clean out than let the money printing and artificial interest rate world of Orr and Robertson and house price inflation and trickle down nonsense.

its funny how all the forecaster now rush to advise this sudden change in outlook after it has already happened

Yep. Propaganda at work. "Hey look over there. 65,000 houses missing. Nothing to do with us and the lending of money into existence."

Yeah, let's wait for a once-in-a-lifetime crisis to spring into action on supply-side issues we've known for years, while still not proposing remedies to the factors that are fueling demand (controlling migration and removing incentives on housing speculation).

Yes, easier to forecast in hindsight....

Thinking about the number migrants accumulated during the past 9 years right before the COVID19, there should be about 450,000 of them (50,000 X 9), which is roughly 100,000 families demand a place to leave.

The newly built residential properties during same period are far less.

Even if there were no new migrants for the coming three years, it would still take many years to digest the huge number accumulated before.

Since the beginning of 2011 there have been 260021 consents issued in Auckland alone.

Exactly, and not all migrants stay permanently, plus we have been having Kiwis leaving the country.

65k houses short

Record low interest rates.

Demand ain't gunna stop anytime soon.

Outcome......house prices increasing.

Borders closed though. Long may it continue.

There was an apparent oversupply in 2006-2011. Aside from the GFC house prices have been inflating during that period? Let’s face it, this notion of a shortage of houses is clearly a guess at best

Truth is a bank can't tell, they just give an estimate and don't even account for unoccupied homes.

There’s a shortage of housing because investors have bought and some are continuing to buy homes in the first home buyer bracket. Sort out that issue and you’ll sort out the “shortage”. Saw 6 new build projects now for sale on my facebook feed yesterday all quoting yields all aimed at investors.

Accidentally reported this while trying to give it an upvote :(

We're also seeing a lot of houses come online that are no bigger than the two bed units of old, which used to be an attractive option for FHBs, but now they're priced at $600K+. There's a one bedroom 60sqm home in the Red Hills development that is priced at $600K. How does that even begin to stack up for anyone other than investors looking for a rental?

How'd you manage that when the report button is next to the reply button and the upvote button is on the far right-hand side of the text?

Reportgate,

Nothing wrong with investors buying new builds though, since that's creating new supply.

lmao...what happened to last months poster child for oversupply?..have a look at ASBs projections for Christchurchs RE inflation....so much BS presented with a straight face.

It's like watching the 6pm news, doesn't matter which channel. Doom and gloom last month, now the boom is back and house prices have never been higher. FHBs are getting their fair share though..

You look at all the data coming out and all it shows is barely anyone bought property in April. I wonder why - lockdown? But now its ramping up again like nothing happened, because people still need shelter. Especially if there is risk of not being able to travel/move overseas, all of a sudden buying in NZ is really important. FOMO.

Hang on, so those 8/10 other countries with prices rising all suddenly realised that they had been underbuilding for years too?

Seems much more likely that shared financial (and psychological) factors are at play.

Idea: ban property investment on lower quartile houses

Idea: tax property investment heavily for 3rd property onwards

Idea: online voting

Idea: if you aren’t going to tax property than remove my income tax too, please and thank you (Jk, I believe tax is a good thing for our greater society)

I don't see what online voting has to do with anything, aside from it also being a terrible idea.

How do you propose to actual 'ban' investment on lower quartile houses, or tax property investment heavily for the 3rd property onwards?

shssh, logic, practicality and reason aren't needed here, there is a crisis and somebody needs to be punished, so ready, fire, aim!!

Yes, and how dare someone question the status quo of ever rising prices!

tsk tsk you horrid little pleb, go back to your corner and count yourself lucky you haven't been sold yourself.

If you want to get rid of ever rising prices, you need to get rid of inflation targeting by the RBNZ.. inflation targeting is a promise of ever rising prices, by govt agency intervention if necessary.

But Cryer, where will First Home Buyers live if their prospective Landlords weren't outbidding them with a higher deposit they did not save for, often at Interest Only residential mortgage lending rates while claiming all the other costs associated with owning a property as deductibles against their taxable income?

Tax is love, right?

Two figures, neither of which I can reference. 1) 7% of Auckland dwellings are empty 2) 25% of NZ dwellings have one occupant. Firstly any idea where to prove/disprove these figures and secondly if they are near the reality do we really have a housing shortage? If they are both real and we have a housing shortage what sort of nudges could remedy it.

Generally, I'm an advocate of the free market system .

When it comes to Housing, the dynamic between supply and demand is far more inelastic than in other markets.

This is where free market principles have to be put aside, somewhat, and wise leadership and policy needs to step in.

In this current real estate cycle , it started with John Key allowing the Building Sector to fall into its biggest depression ( 2008-2010 ) since the Great depression... Enuf people saw this at the time, that John Key should have known. ie. Shortage of houses in Auckland in 2010 while building sector in depression.

https://www.interest.co.nz/charts/real-estate/building-consents-residen…

So..while we have building sector in depression ...we open the flood gates to immigration.

https://www.interest.co.nz/charts/population/net-long-term-migration

Throw in Local Body/Council ineptitude and their focus on control and extracting income from the building process...

Going back to my point about the non-simultaneous movement in the demand and supply of housing and its not hard to see the implications of what was unfolding.

Commentators were alluding to a housing shortage and building depression, back in 2010. https://www.interest.co.nz/opinion/50880/pressure-goes-why-property-inv…

Nzs' leadership needs to help coordinate population growth with the supply of housing. A balance of policy that allows market forces to respond to demand/supply dynamics more elastically.

Labour seems to be doing more in this regards than National ever has..??

TOP party is dreaming if they think a rent tax on housing will actually solve anything...??

I wonder if the halt in overseas travel has something to do with it. Everyone is now looking inward and they see houses, only houses.

Certainly will be, I have 2 immediate family members who got nice refunds back for cancelled overseas trips and went and bought new houses instead.

We got a nice refund on our flights to the UK and Spain plus some accomodation which came to around $20k for 4 of us. Absolutely no where near the deposit for a house. I think it’s more a case of them borrowing to the hilt.....which is what I’m hearing from my contacts.

How about, RBNZ comes up with a new rule along the lines of property investors can not get mortgages for investing in an existing dwelling, only for new builds.

Simultaneously increase property supply while reducing demand/competition for existing, older stock which should be cheaper for FHBs.

Far too sensible.

Or align the property investor "business"with other businesses, I can't get a loan at 2-3% for my business and certainly not one for hundreds of thousands of dollars...

Some of us buy old dwellings with enough land for an extra 1 or 2 houses and then build those as finance permits.

Others buy existing Mac Mansions to demolish them and build 5 or 6 terraces in their place. Your policy would block both the above options.

Wouldn’t be too hard to flesh out my idea to allow for developers working with a genuine intention to add to the housing stock.

Maybe an exemption if the current house size/land area ratio is under a certain amount and the section would be considered prime for development.

Such a section would likely be too expensive for FHBs anyway so would be fitting with the spirit of the policy which would be to keep investors away from the lower quartile priced properties.

Nice work RBNZ. Double digit house price inflation during the worst recession in living memory.

The best financial decision for most non-homeowners is now to jump in front of a train.

Why spend your life working to live for a meagre salary and paying tax on it to boot. Why bother saving. There really is no point going on anymore.

Unfortunately, there are some who under severe financial hardship will do exactly that. Friend has a debt solutions business and they get through messages everyday from people who are really, really desperate.

I posted this on another thread but posting here again.

https://www.rbnz.govt.nz/research-and-publications/speeches/2016/speech…

This is a speech from 2016 highlighting the concerns on the financial impact of a severe housing correcting due to banks being heavily exposed. This is over four years ago. It talks about the need for a broad policy response to address this. It also talks about the role the RBNZ can do to reduce the risk of mortgage defaults such as LVR's, tightening lending conditions etc.

The question is why has none of this been addressed, why is the Reserve Bank now doing the opposite to what it is suggesting in this article by removing LVR's?

The question is why has none of this been addressed, why is the Reserve Bank now doing the opposite to what it is suggesting in this article by removing LVR's?

Why? Have you ever heard of the expression 'Hail Mary' used in NFL?

It seems we are being lied to. If banks have been implementing LVR's as suggested in the speech, this should have helped to reduce their losses in the event of downturn. Why are they then doing everything they can to prevent this from happening?

Because the world’s bankers have been on an expanding debt cycle for at least the last 40 years. The entire financial system is based on both countries and individuals taking on ever increasing amounts of debt. They have deferred recessions by issuing more debt, households are borrowing at higher and higher levels in the hope that salary increases and inflation will somehow pay off the debt. A significant number of households have no savings. They live month to month. Governments have handed out more cash to people than ever before. Rent and mortgages being deferred for months. They have a policy of not allowing businesses or individuals to go bankrupt which is part of the natural business cycle. It’s the same policies all over the world, more and more and more debt! In Aus and NZ the business of the day is buying houses. Aus are seeing some real falls in property sale prices where people are forced to sell and retirees are deciding to downsize earlier as they are seeing prices dropping in their area. We have high unemployment if you include people who are now under employed, in both countries. The US stock market is pumping on the back of a couple of handful of stocks propping up the rest of it. Unemployment is as high as it has ever been. Larry Kudlow is wheeled out once a week so say how great the US is doing but even that doesn’t get the same market reaction as a couple of months ago. It really is becoming a game of fight to the death..... lots of hardworking people here and around the world are going to get really badly hurt. But lets just carry on hiking people up on debt and just hope it all turns out for the best. Hopium - The new drug of choice.

How about all the closed houses we have in the country? Last numbers were around 150,000 which more than doubles the numbers ASB gives, which they completely ignore in their forecast. We can say confidently we will see another forecast from ASB in three months correcting this one with the developments at the time.

It’s really impressive how these bank economists can provide such great insight after the event. Surely we have reached a point where economists should not be relied upon for providing any reputable forecasting of our property market. Best approach is that they provide commentary on factual data and nothing more.

These economists are making fortune tellers look good.

Remind me - how many empty homes do we have in NZ?

Doesn't matter IO, there could be 100,000 but if they are not for sale you cannot live in them unless your promoting the idea of becoming a squatter ?

Check this out, you might be surprised about the real numbers.

https://www.stuff.co.nz/life-style/homed/latest/103024164/is-it-time-to…

The problem is not squatters but investors that choose to keep houses closed since in many cases do not have an incentive to rent.

Thanks b21:

'Figures from the last census showed there were 141,366 empty dwellings in New Zealand, which are separate from houses that are vacant because their owners are away around census time. More than 33,000 houses in Auckland were officially classified as empty in 2016'.

So lets just make it unbearable for people to own houses as tax free stores of capital wealth. Tax the shit out of empty/vacant houses until they are either owner occupied or available for rentals. Add supply to market.

I am thinking of joining the ghost house owners group. Buying a few and installing monitor alarm and locking the doors and having a gardner visit once a month.

My situation is I have zero return on cash in the bank for maximum risk of an OBR event.

Zero deposit guarantee on cash in the bank.

Over taxed on investments in foreign equities.

Orr and Robertson pushing a no deposit no problem and no repayment no problem banking system.

I have no desire to deal with residential tenants but I am loosing money due to zero return and inflation.

Further banks want to lend at 5% to 7% on commercial property and 2% on residential.

There's no way to look at it other than our tax system and regulations are #%@%^ and NZ'er have a mental retardation (they can't look at it from a rational perspective - its very emotive) when it comes to property and property investment. And that isn't a good thing.

Similar boat to you with international investments - I just have moral issue with property investment when I see how stressful and depressing it has made life for younger people in NZ (and Australia) and the downside risk it has.

So you don't care your actions would create a problem for other people? Do you really need returns on your money or is it something you just _want_?

Councillor Chris Darby is quoted extensively in your Stuff article abou the ghost houses. He is head of the planning committee that fights every attempt to develop greenfield housing - the only way to increase supply at low cost. It is staggering he has the arrogance to tell people what they should be doing with their houses - to solve the housing crisis he more than anyone else has created.

The government could always force them to either rent them out, live in them, or sell them. This is a housing crisis after all. These missing houses from NZs housing stock are at least partly to blame for the housing crisis / housing disaster.

1st home buyers have been around since beginning of time and I just wish they stop moaning about house affordability , this is not a new issue and if 1st home buyer purchased a house 10 years ago they wouldn't be moaning today about house prices. One has to remember this is all driven by the Reserve Bank they pull the strings and create this , its not investors causing this they just take advantage of what has been presented to them.

Yes, all those couples in their twenties should have just each bought a house as a single teenage kid. And all those graduates facing a tough job market should have just applied for jobs when they were in intermediate school.

Yes. As soon as someone becomes a property owner, they have a vested interest in house prices going up. This IMO is one reason why the right decisions haven't been made that would have solved the housing crisis.As soon as the market is flooded with houses, and interest rates rise, then property prices would have come down. But that isn't in the best interests of people who already own a home.

And numerous people standing in the way of change.

Last terms Nats tried to reform RMA but were voted down by Labour and Maori party, then started the redevelopment of social housing by knocking down older houses to build more in the same space - like Glen Innes.

This term Labour resorted to Kiwibuild (failed), and 2 separate government agencies such as HUD to try and short circuit barriers to building expansion but that didn't make any progress (or perhaps Twyford again). Now they want RMA reform.

Its politicised, and not all about keeping house prices up, its more about the inability of political parties to resolve a way forward when voters tend to believe outlandish promises, and politicians want to score points, If they were in it for us, they would sort out their s*@t and make land available, and make it easier for decent apartment buildings to go up along transport routes.

I think you have a broken concept of what moaning means, I can see people around talking about something that obviously is an issue, they complain of course, the opposite would be ignoring it and behaving like cattle, is that would you would prefer? It would be convenient for some of course, but be thankful people just "moan" for now since this could become a problem of civil unrest and public health.

I think walking into the sea is more my vibe.

What about the 100,000-200,000 houses in NZ that aren't being lived in? Also the 'Ghost houses' with non local owners, who just leave them empty rather than rent them out, and just sitting on them for the capital gains.

Didn't NZ banks economists say just a few months ago, that house prices in NZ would fall 15%?

That was before our central bank and finance minister when a bit mental and decided that housing is no longer a free market and now sponsored by every tax payer - even those that don't own any property.

And got so much better during the current government......how is that overseas buyer blaming going now?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.