The Reserve Bank "needs to reconsider" reinstating loan to value ratio (LVR) restrictions next month, ASB economists say.

In the ASB's Economic Weekly ASB senior economist Jane Turner said the "RBNZ’s job just got a lot trickier than usual".

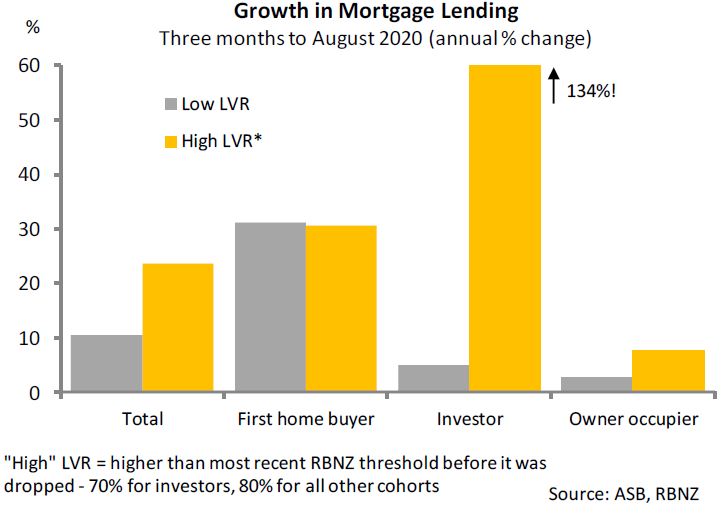

"The RBNZ needs to recognise that the housing market risks have shifted dramatically – no longer are they facing the risk of falling house prices, but that of strongly increasing house prices.

"And by doing nothing, the RBNZ faces the risk of fuelling the fire of a housing market bubble, which, if underpinned by highly leveraged buyers, can increase financial stability risks down the line," Turner said.

The subdued inflation figures last week will likely support the RBNZ’s conclusion that additional monetary support will still be needed for some time, she said.

"Which means the RBNZ’s needs to consider reinstating the LVR lending restrictions at the November Financial Stability review [on November 25] – even if it means going back on its previous forward guidance."

The RBNZ has previously indicated that the LVRs would be lifted for at least 12 months, although last week RBNZ Governor Adrian Orr noted the rising pressures in the housing market in terms of lending and borrowing behaviour and indicated that the central bank was "looking at" bringing back LVRs.

Turner noted that the RBNZ "has multiple jobs to juggle" – it has its Monetary Policy objectives - a dual target of inflation and maximum sustainable employment.

But at the same time, it must also balance Financial Stability Risks.

"Most of the time, it can juggle both responsibilities, as the various risks move together through the economic cycle so relaxing Monetary Policy settings does not conflict with the RBNZ’s Financial Stability goals.

"However, there was no modern precedent for the COVID-19 pandemic, and during this highly unusual time we are all learning as we go."

She said in the early days of the Covid-19 pandemic, the RBNZ was quick to grasp the seriousness of the situation and was quick to deliver policy support via slashing the Official Cash Rate (to 0.25% from 1.25%), putting in place a range of monetary implementation measures and introducing Quantitative Easing in NZ.

On the Financial Stability front, the RBNZ relaxed Loan to Value (LVR) lending restrictions across the board, in large part to support the housing market.

"Alas, economists (including ASB) got it wrong, and the surprisingly resilient economy, plus large falls in mortgage rates, plus relaxing LVR lending restrictions proved a very potent mix for the housing market.

"Strong housing demand across the board (it’s not just investors that are buying), coupled with chronic housing shortages means the housing market is now very tight and house prices have lifted strongly to reflect that."

45 Comments

Good article. Well done on writing it when the mainstream media is ignoring the issue.

I hope you can convince Adrian Orr of this. At the moment he is just "watching the market". Orr managed quickly to decide to QE money print $100 billion, take rates to zero and remove LVRs to save the housing market but now its out of control he is watching the market.

Your 100% correct the housing market bubble is risking future uncertainty of our banks.

Unfortunately Orr is only focused on saving the debt fueled and appears to have zero concerns for fiscally conservative savers.

Deposit holders face greater risk the more the housing market runs for zero returns and no bank guarantee.

An old saying goes- if you owe 1 million to the bank, you are in trouble and if you own 100 billion to the bank, the bank is in trouble.

Here, collectively, property investors owe a heck lot more to the banks and so banks are going to be in trouble. Therefore, Adrian Orr is going to throw savers under the bus to save the banks.

It seems it pays off to be reckless. If you don't read/understand history, you are bound to repeat it.

So do you think Orr has serviced and fueled up his OBR chainsaw to haircut all the savers? It will be short back and sides!

At some point Adrian wont be able to save them if unemployment numbers are big enough.

We know from the 'forward guidance' that promises were made. But the image of RBNZ ' "looking at" bringing back LVRs' does beg the question of whether they are holding the binoculars the right way around......

Jeez, so much love for LVR. 30% and 20% deposits are "high LVR" now? So we just change the definition of "high LVR" to push a narrative? Left wingers love to dictate what others should/shouldn't be doing. Really hope Orr sees through all the BS being pushed :|

"we are all learning as we go."

That's the problem, Jane. We aren't....By and large, I'll bet you still use the same tools and techniques; analyse the same variables that you did 10 years ago?

Lesson 1 of this particular seminar was given in 2008, the latest instalment in March 2020 and yet here we are.

It's because very few people have learned anything that we are here.

What was it Judith told us? "If you want to lose weight, stop eating"

Sorry, couple of this nice 'trying articles' recently. Leads to just a certain leeway of preservation method of the same old same old.

Nope, I really suggest RBNZ to steadfast in their course. LVR must be put off permanently, more stimulus are needed in big surge before mid of next year. Nov FLPs, QEs, wages subsidy, living subsidy etc. Kiwis should know by now where to put their cash/banking systems.

To either real Bank which focus on productivity? or the 4 OZ parent banks account, which surely in Aus$ & TD guarantee if necessary, my advise? do a very short term for TD.. much better to be liquid in daily accounts.

Simple, do it now. Remember your cash is king to buy basic staples, Not your illiquid assets.

Reimplementing LVRs is a no-brainer.

Not taking them away in the first place was a no brainer.

Agree should be implmented asap. In many countries like Australia LVR restriction was removed but only for FHB.

RBNZ as have already made its intent clear out in public domain (by thinking aloud) that they want house price to go up... Rising house price movement should continue so why will they do anything to disrupt the ponzi AND yhey have been successful and though hiuse orices were string after lockdown but git real fire after deputy govetnor of RBNZ came out in media and batted for housing market ponzi to continue.

Do the RBA have LVR's for property investors? Please provide a link or proof.

Hussman chillingly illustrates the scale of problem may be (literally) off the charts, suggesting can may be too big to kick much further (needed $20T+ to counter 21Feb-23March "bear market fall" yet in context only a correction). When cycle he describes ends, if NZ took hard option earlier (partly defuse, for NZ to weather it best), or easy option following the herd, may define this Govt for decades. Hard to think s/thing other than Covid might become defining feature of Ardern/Lab. Govt. Tough call for any Govt/CBank. Thx Andrewj for link:

"Herd mentality" (17 Oct): https://www.hussmanfunds.com/comment/mc201016/

"Yikes" (`1 Sep): https://www.hussmanfunds.com/comment/mc200901/

“Easy money doesn’t reliably support stocks when investors are inclined toward risk-aversion. But when they view low-interest cash as an “inferior” asset, look out. Once interest rates hit zero, so does the IQ of Wall Street” ...would be funny if it wasn’t so true.

If aware that house market is running amok why wait till november and not act now, just like RBNZ acted promptly to support housing market and acted when it felt may fall.

Same logic if have to act - do now and not announce in a month time and impliment in 3 months time giving window opportunity to speculators.

i it not ironic that the person that lends the debt to fuel the fire is asking someone else to put a bit of water on it and cool it down,

Anyone have any idea what these high LVR "investors" are thinking? are they?

Is is short term speculation on rates going even lower house prices peaking in one to three years time? (I can see the smart or first to panic likely making some money here.)

Do they believe the inflation hype? or was the bank just saying no due to the LVR.

I think it would be brave bet to think we will have a negative OCR in five years time and current rental rates.

Edit: Nevermind, just spoke to workmate who wants to buy a house in Christchurch and make some capital gains while his son is at uni.

High LVR for investors in that chart means >70%. Most are probably in the 70-80% range, so not high relative to owner occupiers.

Most people I've talked to (including valuers and agents) believe prices are going to continue increasing.

They think they have to be in property to get a return on their money, they believe it is safe, and because prices are only going to go higher, the sooner the better.

Maybe they're right. Or maybe it's classic irrational exuberance at the top of a bubble. We'll only know for sure in hindsight.

Do they associate lower mortgage rates with higher prices? and if they do to they believe a zero lower bound exists?

Money printers go "wurrrr", RBNZ goes "no LVR, Speculators go "crazy". All the noise about returning cashed up kiwis looks like fud.

Is anyone surprised?

Many properties sold in Auckland are in 1.1 million to 2.5 million plus range (May be that is the bottom price now) so wonder if NZ is so rich that FHB are buying million or two million dollar properties.

Easy solution: Investors must pay 80% cash for 2nd property, and 100% cash for the 3rd property.

price will cool down.

Ugh banks are always wanting it all ways aren’t they? Absolutely nothing stopping them from imposing the LVR restrictions themselves.

Constantly arguing to self-regulate, but then also point the finger at that meddling government when it suits their narrative with their customers.

Yeah but if one bank says no then the customers will just go to their competitor who will say yes.

True, but it doesn’t really remove the obligation of each individual bank to practice what they’re preaching unless they’re okay with being hypocritical.

The message I’m hearing from their economists is save us from ourselves, and increase your regulation of us. Meanwhile their CEO’s and chair people are saying trust us to evaluate our own capital requirements we know what we’re doing. So reading into the first point, kind of makes you feel the second point is more, “we all know you’re going to have to bail us out when shit hits the fan anyway, so please don’t make us hold more capital going into a recession.”

All the while they’re saying “we don’t need a Royal Commission because we behave differently from our parents” it’s all wearing bloody thing and the sooner an inquiry is stood up, even if only to prove them right, the better.

I note further that it’s a bit ridiculous to say that they want those capital obligations deferred, when said capital has never been cheaper.

I mean give me a break. Can’t wait for them to start releasing their reports this week, God help them if it’s another year of record profits once the increased allowance for doubtful debts provisions are removed.

Breaking news: Monthly mortgage advances reach record high of over $7.3 bln in September.

Mr Orr with your action you are inflating the already inflated Market.

Add house price index also to your inflation data and see the real inflation.

Investors are sitting on a lot of equity at present, either in their own home or in their investment properties. Now they can unlock that equity and use it on a "no money down" purchase. They dont need much equity in the property they buy, or to leave much in the one that they are using the equity from. So 40% equity unlocked on a single home can enable the purchase of three or four houses. Is it any wonder they are going on a buying binge? And all that RBNZ "jawboning" will do is push even more investors into the market in the next month in order to get ahead of the RBNZ before they shut the gate (after the horse has well and truly bolted)

Where will the couple of billion coming out of Bonus Bonds end up, that's just the tip of the iceberg , as investors take flight from the stock market, no where for it to go, other than a new car, or property.

Lot of money coming out of Term Deposits as they mature, and going straight into cash account awaiting a house buying opportunity. Not helped by the terrible low TD rates. If they had some way of increasing TD rates, to make them more attractive, and give an incentive to save, not borrow and spend, that may help. But there is no political motivation to fix it, as anyone who owns a house feels richer when house prices go up.

Maybe they feel richer, but Reddell did an analysis of the so-called "wealth effect" in one of his articles recently, and found there's very little or no correlation between increasing asset prices and increased household consumption (which is what the RBNZ is aiming for).

https://croakingcassandra.com/2020/10/13/housing-the-reserve-bank-and-i…

We've just received the 2020 QV assessment for our house, it's gone up $300k on the 2017 valuation. However, over the same period, our monthly income hasn't increased significantly although the monthly outgoings have gone up slightly. Our spending pattern hasn't changed and is unlikely to as the disposable income in the bank at the end of the month is roughly the same as before the increase in asset value. Despite being 'worth more', we can't actually spend it!

Equity maaate! You can tap that $300k for a deposit on an investment property.

IMO it should be done under urgency. Hopefully the central government can do something about it, or bring in some urgent policy. It is only going to make the housing crisis (disaster)worse and someone will have to clean it up. Kicking the can down the road doesn't work.

This is insane. I have lost all respect for the RBNZ.

The chart in the article clearly indicates that the mortgage growth is coming mainly from investors.

The LVRs should have never come off.

We can live with either flat or slowly declining house prices.

Yet more NZ money going into bidding up land prices, the most unproductive use of capital possible.

Not impressive are they.

Orr and his chief economist dude don't come across as especially articulate or insightful.

Really sick and tired of hearing how the investors are borrowing too much to purchase houses, they are only doing what Mr Adrian Orr wanted them to do regardless of who or what they were. ( 1st home buyer , investor , mum and dad investor ). Im sorry to say that when you pump 100 Billion into the economy and expect nothing to happen. This was going to happen regardless as the dollar is gone baby , it will not be around in 5 - 10 years.

The RBNZ will already be working on a Crypto currency behind closed doors, same as the Aussies.

No way will they reinstate LVRs in 2021. Would lead to less investors in the market, less confidence in the market and prices starting to fall. Cannot see someone as spineless as Adrian Orr doing something like this

David...could you ask your colleague Mr Ninness if he agrees with your sentiment. I have a feeling that he would never write or suggest anything that may have a negative impact on property prices. He seems unable to stop singing from the Ashley Church hymn book.

If the RB hadn't done anything, and interest rates remained high, would our house prices gone up as much as they have?

If there was no risk of the NZ housing market falling, would the RB have stepped in at all?

There could have been severe debt defaults (globally) this year if central banks didn't intervene in the markets - asset prices would have tumbled, unemployment would have been very high.

But as Key points out in the other article (just posted) we're now creating asset bubbles and zombie companies. If you think that is good news, long term, for the prosperity of economies, we should think again. But the central banks have prevented armageddon, for now....job done (until when?).

Adrian Orr and his Team are qualified to handle all situations including challenges to the current housing shortage fuelling the house price inflation . Economists have always got it wrong and Banks have always kept their own interest upper most always . A nation with a history of lack of alternative to housing as an investment option cannot learn the stock market investment game overnight or in less than 6 months although it is changing . Asb Securities an arm of ASB Bank has been a leading example of the bank backed brokerage firm.

Only RBNZ has been able to bring some confidence in the minds of home owners and general public to go out and borrow and use the money to spend to support small businesses which Banks including ASB have been less supportive of due to their own limitations .

If once the investor confidence goes down again it is hard to shore up and then no Bank , Economist and Politician can bring it back . Let the housing take the lead in continuing to shore up this confidence and let market activity increase rather than buyers of goods and services waiting and watching with folded hands.

Your mindset seems to illustrate the whole problem pretty well. "bring confidence...to go out and borrow". "Let housing take the lead"." Adrian Orr,,qualified to handle situation". Man, I really hope you are just trolling.

The only ulimate solution is for people to loose money in the property market, serious loses. Its been an almost guaranteed bet for so long leaving an increasing number of population severely disavantaged. Current policy settings are unlikely to bring this about any day soon. So until migration numbers are controlled in the meduim term, the overall housing stock increased and credit available reduced the game will continue. A shorter term issue for the market is possibly once Australia gets up and running again younger Kiwi's leave on mass driven by crippling local house prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.